An FI can eliminate its currency risk exposure by matching its foreign currency assets

to its foreign currency liabilities.

Answer:

Futures contracts are the primary security that insurance companies and banks use to

hedge interest rate risk prior to originating mortgages.

Answer:

The on-the-run yield curve of U.S. Treasury securities is the yield curve for

outstanding, previously issued securities.

Answer:

Considering the market risk of traders’ portfolios for the purpose of establishing logical

position limits per trader in each area of trading is a resource allocation benefit of

market risk measurement.

Answer:

As of June 2012, commercial banks held more forward contracts than futures contracts

for trading.

Answer:

Deposit insurance is often blamed for the deterioration in depositor discipline that

allowed FIs to accept more risk in the asset selection process.

Answer:

It is likely that the discrepancy between book value of equity and market value of

equity will increase as volatility in interest rates increases.

Answer:

A life insurance company that is a parent company is not required to hold an equivalent

amount of risk-based capital to protect against financial downturns of affiliates.

Answer:

Depository institutions serve as the primary conduit through which monetary policy

actions impact the economy.

Answer:

The concept of pull-to-maturity reflects the increasing variance of a bond’s price as the

maturity of the bond approaches.

Answer:

An FI buys a collar by buying a floor and selling a cap.

Answer:

When a finance company pools mortgages with similar characteristics and securitizes

the pool, the loans are removed from the balance sheet of the finance company.

Answer:

The discount window at the Federal Reserve is a suitable substitute for deposit

insurance and a possible method of preventing bank runs.

Answer:

The Financial Services Modernization Act of 1999 and other regulatory changes have

been the cause of the increase in interindustry mergers of investment banks and

securities firms.

Answer:

A hedge using a put option contract completely offsets gains but only but only partially

offsets losses on an FIs balance sheet.

Answer:

The smaller the leverage adjusted duration gap, the more exposed the FI is to interest

rate shocks.

Answer:

Delivery of the underlying asset almost always occurs in the futures market.

Answer:

Off-balance-sheet activities generally have risk-reducing attributes, but seldom have

risk-increasing attributes.

Answer:

Which of the following observations concerning the federal funds rate is NOT TRUE?

A. The cost of fed funds for the purchasing institution is the federal funds rate.

B. The federal funds rate is set by DIs that trade in the fed funds market.

C. The federal funds rate can vary considerably within the day.

D. The federal funds rate can vary considerably across days.

E. Rate variability has increased since the introduction of lagged reserve accounting.

Answer:

The all-in-spread (AIS) used in the Moody’s Analytics model is the difference between

the interest rate on a loan and the prime lending rate at the time the loan was

originated.

Answer:

Although secure communications can be carried out between an FI and their customers

in dedicated message centers, the centers have yet to replace e-mail communications as

the primary means of customer contact.

Answer:

Most individuals who invest in mutual funds for the first time realize that mutual fund

investments carries some risk.

Answer:

An FI can control its FX risk exposure by on-balance-sheet and off-balance-sheet

hedging.

Answer:

A loan sale occurs when an FI originates a loan and sells the loan without recourse to an

outside buyer.

Answer:

Prior to World War II, most international debt was in the form of bank loans.

Answer:

More frequent regulatory examinations and stricter regulator standards will cause

greater discrepancies in book value of equity and the market value of equity.

Answer:

Finance companies have relied primarily on short-term commercial paper and other

debt sources to finance asset growth.

Answer:

Relationship pricing involves pricing for specific services which depend, in part, on the

amount or number of services that are used by the customer.

Answer:

Which of the following observations concerning the production approach to measure

the cost function of FIs is TRUE?A. It views FIs’ outputs of services as having three

underlying inputs.

B. Labor and capital are the only inputs.

C. It views the output as being produced by labor, capital and the funds used to

produce intermediated services.

D. Deposit costs are viewed as an input in the banking and thrift industries.

E. None of the above.

Answer:

CHIPS guarantees that any wire transfer is final at the time it is made.

Answer:

Most profits or losses on foreign trading come from taking an open position in

currencies.

Answer:

The marginal mortality rate is the probability of a bond or loan defaulting in any given

year after it is issued.

Answer:

Increases in the rate of innovation of new financial products, whether successful or not,

is often credited to advances in technology.

Answer:

A total return swap involves exchanging an obligation to pay interest at a specified rate

for payments representing the total return on a loan or a bond of a specified amount.

Answer:

Insurance companies have resisted the investment in technology that banks and other

financial service firms have pursued.

Answer:

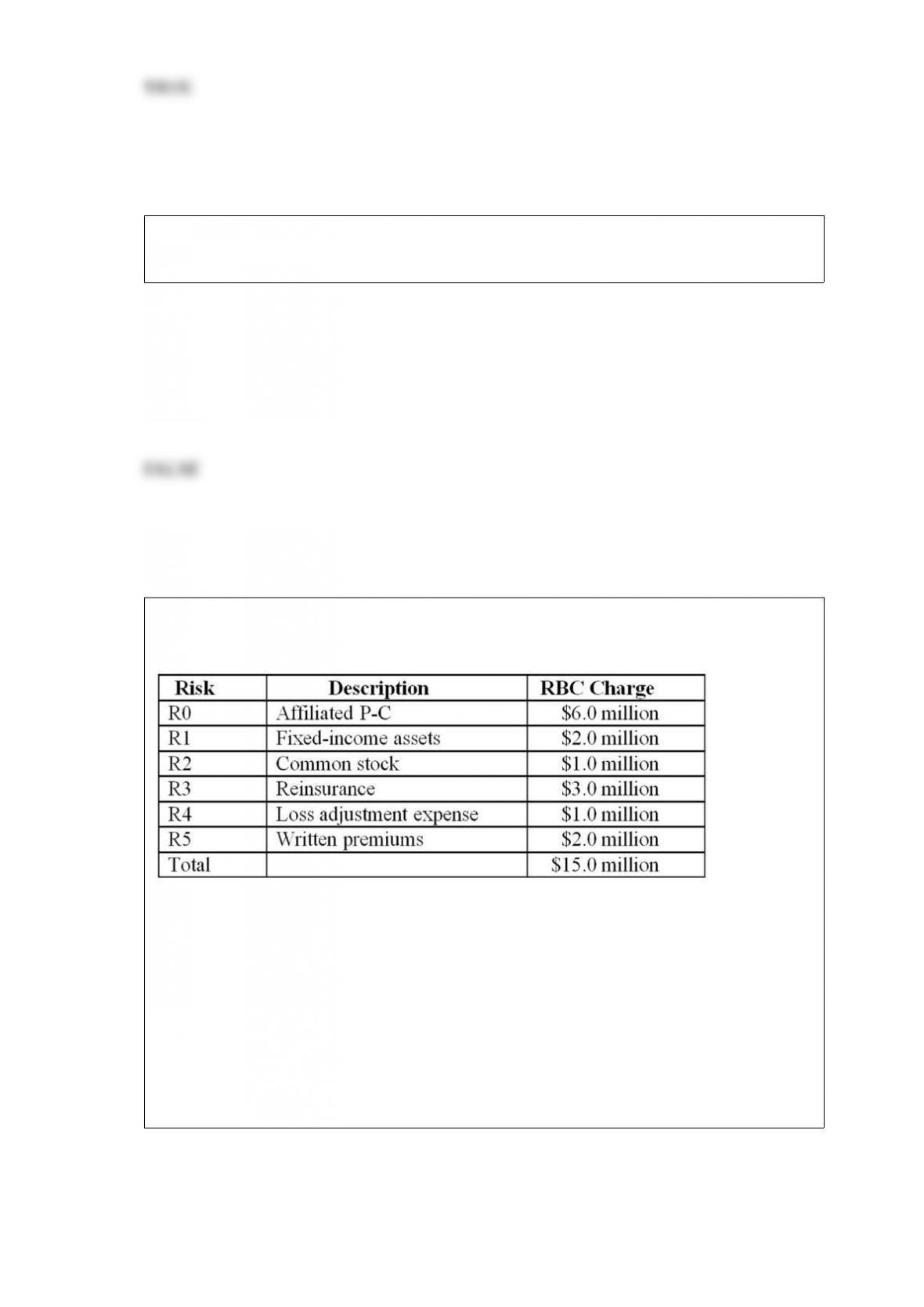

A property-casualty (P-C) insurance firm has estimated the following risk-based capital

charge for its individual risk classes:

Using the

model recommended by the National Association of Insurance Commissioners (NAIC),

what is the total risk-based capital charge for the P-C firm? A. $4.36 million.

B. $10.00 million.

C. $10.36 million.

D. $12.50 million.

E. $15.00 million.

Answer:

As of January 2012, which of the following represented the highest percent of the dollar

value of noncash transactions worldwide? A. Checks.

B. Card payments.

C. Debit transfers.

D. E-money payments.

E. Credit transfers.

Answer:

The risk that a German investor who purchases British bonds will lose money when

trying to convert bond interest payments made in pounds sterling into euros is called A.

liquidity risk.

B. interest rate risk.

C. credit risk.

D. foreign exchange rate risk.

E. off-balance-sheet risk.

Answer:

What is replacement risk in the swap market? A. The risk of substituting a defaulted

swap with a new swap at less favorable terms.

B. The cost incurred by the swap dealer in replacing the defaulting party on the same

terms as the original swap.

C. The risk involved in exchanging fixed interest payments for floating interest

payments by two counterparties.

D. The risk associated with long-term hedge sometimes for as long as 15 years.

E. The comparative disadvantage faced by swap seller in making variable or floating

rate payments.

Answer:

An investment company has purchased $100 million of 10 percent annual coupon,

6-year Eurobonds. The bonds have a duration of 4.79 years at the current market yields

of 10 percent. The company wishes to hedge these bonds with Treasury-bond options

that have a delta of 0.7. The duration of the underlying asset is 8.82, and the market

value of the underlying asset is $98,000 per $100,000 face value. Finally, the volatility

of the interest rates on the underlying bond of the options and the Eurobond is 0.84.

Using the above information, what will happen to the market value of the Eurobonds if

market interest rates fall 1 percent to 9 percent? A. Increase $8,018,182.

B. Decrease $8,018,182.

C. Decrease $4,354,545.

D. Increase $6,735,272.

E. Increase $4,354,545.

Answer:

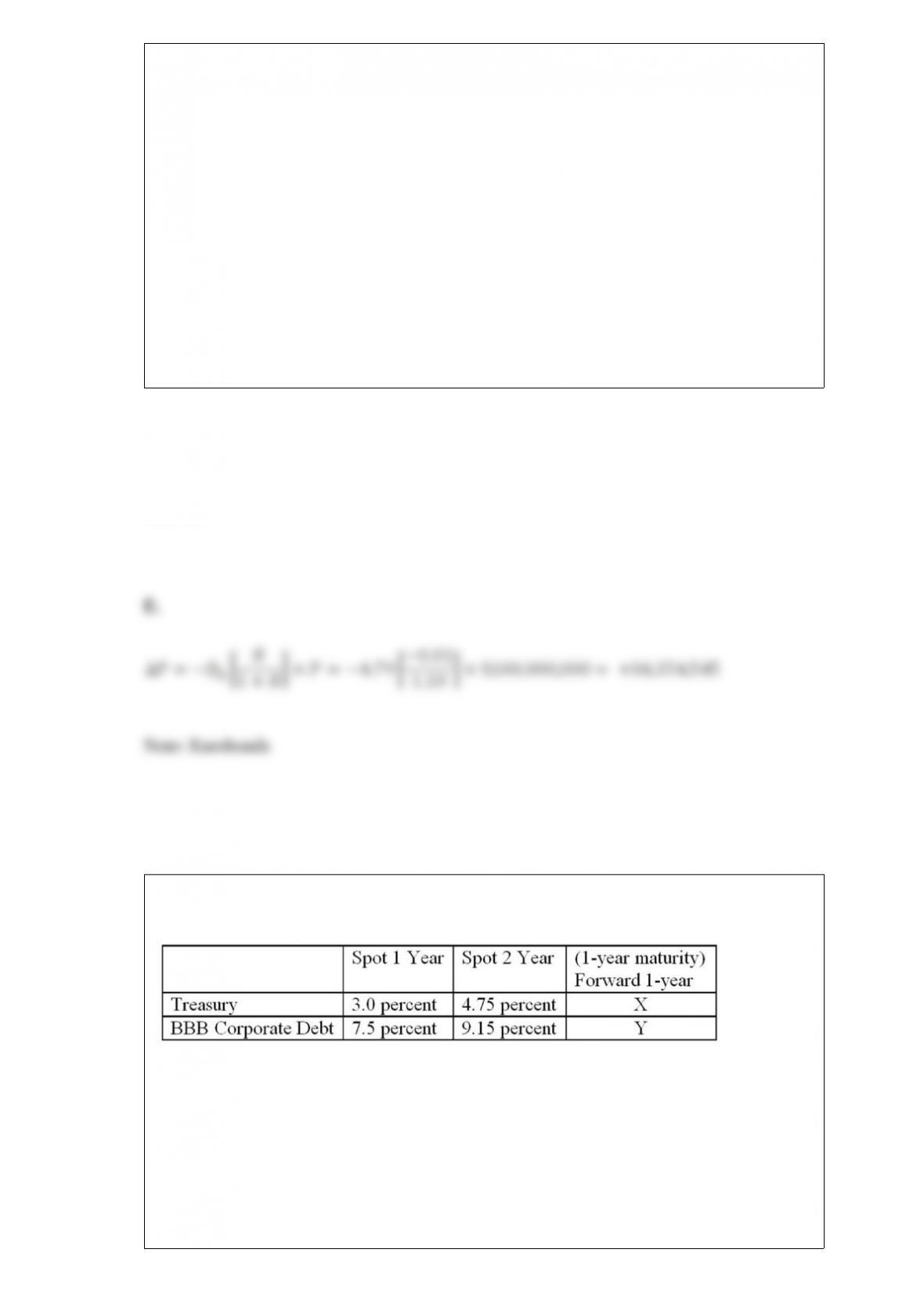

The following is information on current spot and forward term structures (assume the

corporate debt pays interest annually):

Calculate

the value of y (the implied forward rate on one-year maturity BBB corporate debt to be

delivered in one year). A. 6.53 percent.

B. 10.83 percent.

C. 5.75 percent.

D. 6.925 percent.

E. 1.017 percent.

Answer:

What is the effect of a 100 basis point increase in interest rates on the market value of

equity of the FI? Use the duration approximation relationship. Assume r = 4 percent. A.

-27.56 million.

B. -28.01 million.

C. -29.85 million.

D. -31.06 million.

E. -33.76 million.

Answer:

If an FI embraces the concept of good bank/bad bank, A. bad bank assets are passed on

to the institutions correspondent bank that is required to accept the assets.

B. good bank assets are organized into a closed end mutual fund which then sells

shares to raise funds for the bad bank.

C. the bad bank is a special purpose vehicle (SPV) that is organized to liquidate

non-performing loans.

D. the bad bank assets are funded by FDIC insured deposits.

E. the bad bank is placed under the supervision of the Resolution Trust Corporation.

Answer:

Price and quantity restrictions in regulation are usually aimed at determining whether

an FI is meeting certain A. consumer protection guidelines.

B. credit allocation guidelines.

C. investor protection guidelines.

D. safety and soundness guidelines.

E. entry regulation guidelines.

Answer:

As interest rates increase, the writer of a bond call option stands to make A. limited

gains.

B. limited losses.

C. unlimited losses.

D. unlimited gains.

E. Answers A and B only.

Answer:

The risk that an investor will be forced to place earnings from a loan or security into a

lower yielding investment is known as A. liquidity risk.

B. reinvestment risk.

C. credit risk.

D. foreign exchange risk.

E. off-balance-sheet risk.

Answer:

When does “duration” become a less accurate predictor of expected change in security

prices? A. As interest rate shocks increase in size.

B. As interest rate shocks decrease in size.

C. When maturity distributions of an FI’s assets and liabilities are considered.

D. As inflation decreases.

E. When the leverage adjustment is incorporated.

Answer:

An insurance policy in which fixed premium payments are invested in mutual funds of

stocks, bonds, and money market instruments is calledA. term life.

B. universal life.

C. whole life.

D. endowment life.

E. variable life.

Answer:

How is the cost of a systemic risk exemption to the least-cost resolution of bank failures

shared among banks? A. It is shared equally among all other insured banks.

B. Additional deposit insurance premiums are imposed on FIs based on their size as

measured by their total deposits and borrowed funds excluding subordinated debt.

C. Additional deposit insurance premiums are imposed on FI based on their size as

measured by their total deposits and borrowed funds including subordinated debt.

D. It is shared equally among all other insured banks based on the profits earned by the

FI during the year.

E. The cost is borne by the bank whose run was responsible for the contagion.

Answer:

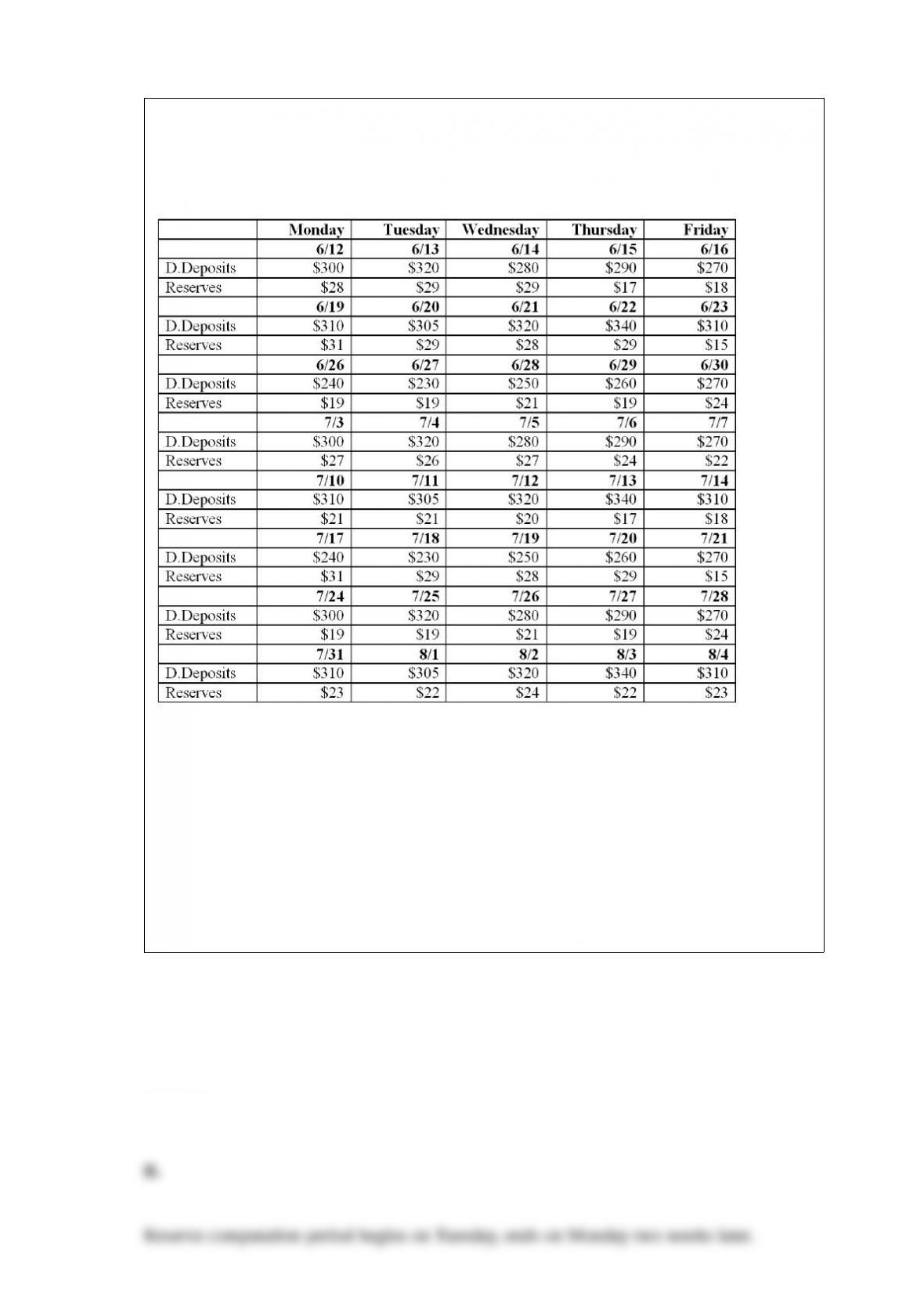

The following demand deposits and cash reserves at the Fed have been documented by

a bank for the computation of reserve requirements (in millions). Note that reserves are

vault cash and reserves at the Fed.

What are

the average daily demand deposit balances over the reserve computation period

beginning the week of June 12? A. $286 million.

B. $296 million.

C. $306 million.

D. $326 million.

E. $352 million.

Answer:

This broad class of loans constitutes the highest percentage of total assets for all U.S.

commercial banks as of the end of 2012. A. Commercial and industrial.

B. Commercial and residential real estate.

C. Individual loans.

D. Credit card debt.

E. Less developed country loans.

Answer:

If purchased liquidity is used by a DI to fund an exercised loan commitmentA. the

balance sheet will decrease by the amount of the new loan.

B. only the asset side of the balance sheet will increase.

C. the balance sheet will increase by the amount of the new loan.

D. only the liability side of the balance sheet will increase.

E. there will be no effect on the balance sheet.

Answer:

An investor invests $100,000 in a mutual fund that has a 5 percent front-end load,

charges a management fee of 0.5 percent, and a 12b-1 fee of 0.25 percent. The investor

plans to leave the investment for one year. What is the dollar amount of the total

shareholder cost? A. $5,000.

B. $5,500.

C. $5,750.

D. $750.

E. $500.

Answer:

Which of the following would be a key area of activity for an investment bank

specializing in the commercial side of the business? A. Purchase of existing securities.

B. Sale of securities in the secondary market.

C. Brokerage of existing securities.

D. Underwriting issues of new securities.

E. All of the above.

Answer:

What does Moody’s Analytics Portfolio Manager Model use to identify the overall risk

of the portfolio?A. Maximum loss as a percent of capital.

B. Historical loan loss ratios.

C. Default probability on each loan in a portfolio.

D. Market value of an asset and the volatility of that asset’s price.

E. Mean of the value of loans in a portfolio.

Answer:

The sellers of domestic loans and HLT loans include all of the following EXCEPT A.

major money center banks.

B. foreign banks.

C. U.S. government and its agencies

D. non-financial companies.

E. investment banks.

Answer:

If Bank C splits into two separate institutions at ½ its original size each, what is the new

Herfindahl (HHI) Index? A. 60.

B. 340.

C. 2,538.

D. 2,847.

E. 10,000.

Answer:

Concern about potential abuses of fiduciary responsibility has been used to justify

product segmentation on the grounds of A. safety and soundness issues.

B. economy of scale and scope issues.

C. conflict of interest issues.

D. deposit insurance issues.

E. regulatory oversight issues.

Answer:

Which of the following refers to the term “mortality rate”? A. The success rate of new

investments.

B. A one-period rate of interest expected on a bond issued at some date in the future.

C. The probability that a borrower will default in any given year.

D. Historic default rate experience of a bond or loan.

E. The probability that a borrower will default over a specified multiyear period.

Answer:

The combination of being long in the bond and buying a put option on a bond mimics

the profit function of A. buying a put option.

B. writing a put option.

C. writing a call option.

D. buying a call option.

E. buying a floor.

Answer:

Calculate the duration of a two-year corporate bond paying 6 percent interest annually,

selling at par. Principal of $20,000,000 is due at the end of two years. A. 2 years.

B. 1.91 years.

C. 1.94 years.

D. 1.49 years.

E. 1.75 years.

Answer:

In October 2008, the opportunity cost of holding excess reserves for U.S. DIs A.

increased because new reserve requirements imposed by the Federal Reserve as a result

of the financial crisis.

B. decreased because subsidiary DIs were first allowed to issue commercial paper

directly, rather than through the parent holding company.

C. decreased because the Federal Reserve began to pay interest to DIs on excess

reserves held at the Fed.

D. increased because the Federal Reserve no longer accepted government securities as

meeting excess reserve requirements.

E. None of the above.

Answer:

Assume that instead of investing in Euro bonds at a fixed rate of 6.5 percent, it invests

them in variable rates of LIBOR + 1.5 percent, reset every six months. The current

LIBOR rate is 5 percent. What is the annual spread earned by the bank if LIBOR at the

end of six months is 5.5 percent? Assume both interest and principal will be reinvested

in six months. Assume the exchange rate remains at €1.75/$ at the end of the year. A.

0.50 percent.

B. 0.68 percent.

C. 0.86 percent.

D. 0.90 percent.

E. 0.95 percent.

Answer:

What is the net gain or loss to the investment company resulting from the change in

rates given that the hedge was placed?A. Lose $2,131.

B. Gain $2,131.

C. Lose $695,191.

D. Gain $695,191.

E. Gain $2,382,858.

Answer:

On the advice of its chief financial officer, Allright wants to hedge the balance sheet

with T-bond option contracts. The underlying bonds currently have a duration of 8.82

years and a market value of $97,000 per $100,000 face value. Further, the delta of the

options is 0.5. What type of contract, and how many contracts should Allright use to

hedge this balance sheet? A. puts; 447 contracts.

B. calls; 625 contracts.

C. puts; 625 contracts.

D. calls; 447 contracts.

E. puts; 206 contracts.

Answer:

Which benefit of market risk measurement (MRM) provides senior management with

information on the risk exposure taken by FI traders? A. Regulation.

B. Resource allocation.

C. Management information.

D. Setting limits.

E. Performance evaluation.

Answer:

Open-end mutual fundsA. require that NAV consider the amount of discount or

premium in the share value.

B. calculate the NAV based on the total value of assets held divided by the number of

fund shares outstanding.

C. may experience fluctuations in the number of shares outstanding on a daily basis.

D. All of the above.

E. Answers B and C only.

Answer:

In international finance, the debt service ratio is found by dividing interest and

amortization payments by the A. total foreign exchange reserves.

B. real investment.

C. gross national product.

D. value of exports.

E. money supply.

Answer:

Which of the following statements best describe a derivative contract?A. Contractual

commitments to make a loan up to a stated amount at a given interest rate in the future.

B. Contingent guarantees sold by an FI to underwrite the performance of the buyer of

the guaranty.

C. Agreement between two parties to exchange a standard quantity of an asset at a

predetermined price at a specified date in the future.

D. Trading in securities prior to their actual issue.

E. Loans originated by an FI and then sold to other investors with recourse.

Answer:

What should be the net price of a $5,000,000 collar if the bank purchases a three-year 6

percent cap and sells a 5 percent floor, if the current (spot) rates are 6 percent? A. The

bank will receive net $2,010.

B. The bank will receive net $31,651.

C. The bank will pay net $31,651.

D. The bank will pay net $2,010.

E. price = $0

Answer: