Use the following information to answer the question(s) below.

Rearden Metal imports ore from South America. Rearden Metal is worried that the

South American mines may enter into a long-term contract with the Chinese to sell all

of their ore output to China, hence cutting off Rearden Metal’s supply. In the event of

such a contract with the Chinese, Rearden Metal will face much higher costs for its raw

materials causing its operating profits to decline substantially and its marginal tax rate

to fall from its current level of 35% down to 10%. An insurance firm has agreed to

write a trade insurance policy that will pay Rearden Metal $2,500,000 in the event of

the South American supply of ore being cut off. The chance of the South American

supply being cut off is estimated to be 20%, with a beta of -2.0. The risk-free rate of

interest is 4% and the return on the market is estimated to be 12%.

To protect the firm against the loss of earnings if the business operations are disrupted

due to fire, accident, or some other insured peril a firm would purchase

A) property insurance.

B) key personnel insurance.

C) business liability insurance.

D) business interruption insurance.

Answer:

Which of the following statements is false?

A) With registered bonds, on each coupon payment date, the bond issuer consults its list

of registered owners and mails each owner a check (or directly deposits the coupon

payment into the owner’s brokerage account).

B) If a coupon bond is issued at a discount, it is called an original issue discount bond.

C) The face value or principal amount of the bond is denominated in standard

increments, most often $10,000.

D) In a public offering, the indenture lays out the terms of the bond issue.

Answer:

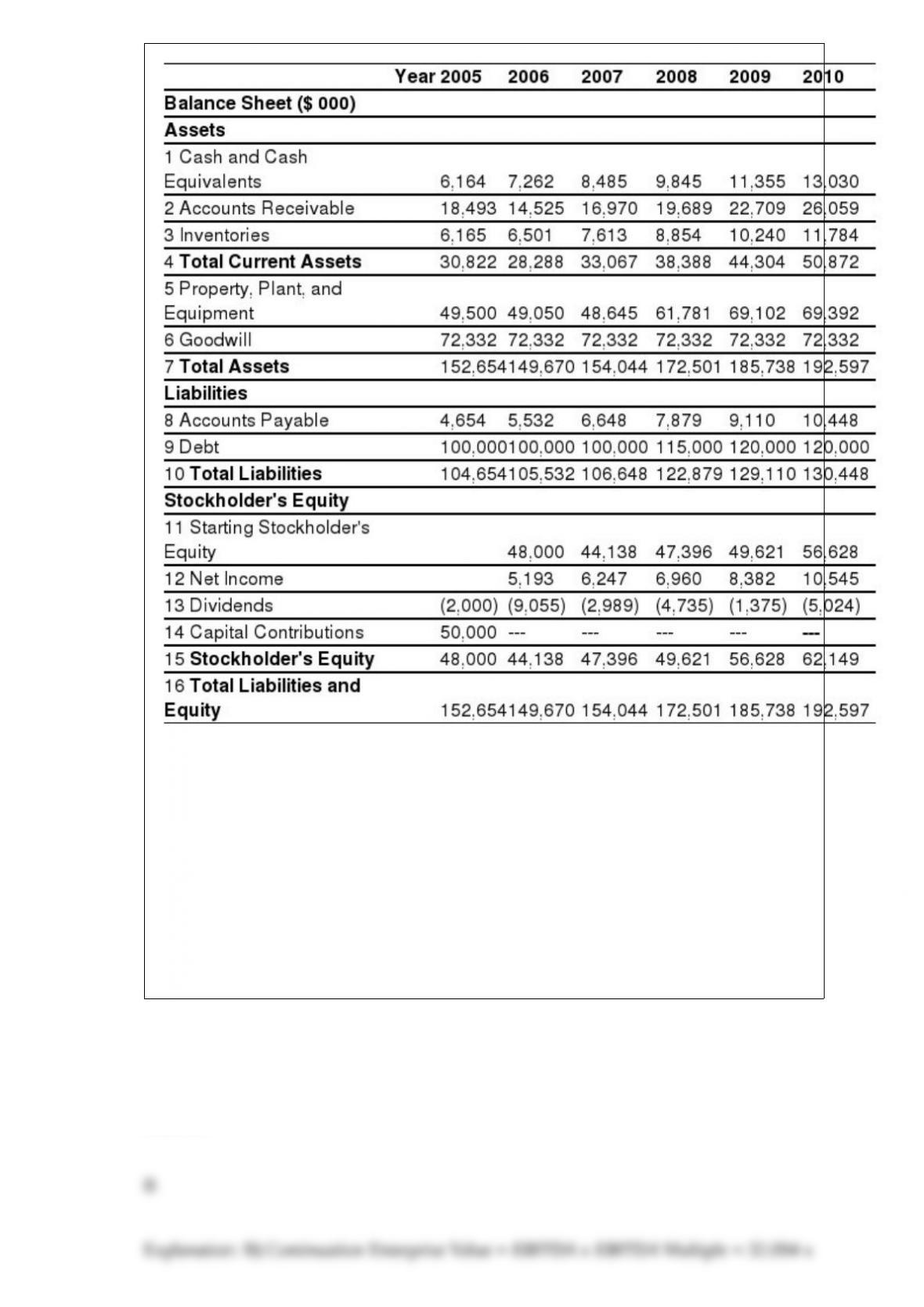

Use the tables for the question(s) below.

Pro Forma Income Statement for Ideko, 2005-2010

Pro Forma Balance Sheet for Ideko, 2005-2010

Assuming that Ideko has a EBITDA multiple of 8.5, then the continuation enterprise

value of Ideko in 2010 is closest to:

A) $152.8 million

B) $272.8 million

C) $301.7 million

D) $181.7 million

Answer:

Use the information for the question(s) below.

KT Enterprises is considering undertaking a new project. Based upon analysis of firms

with similar projects, KT has determined that an unlevered cost of equity of 12% is

suitable for their project. KT’s marginal tax rate is 35%, its borrowing rate is 7%, and

KT does not believe that its borrowing rate will change if the new project is accepted.

If KT expects to maintain a debt to equity ratio for this project of 1 then KT’s project

based WACC, rwacc, for this project is closest to:

A) 11.1%

B) 10.8%

C) 9.6%

D) 10.5%

Answer:

Collection float is made up of all of the following except

A) disbursement float.

B) processing float.

C) mail float.

D) availability float.

Answer:

Nielson Motors has no debt, and maintains a policy of holding $80 million in excess

cash reserves, invested in risk free treasury securities currently yielding 3%. If Nielson

is in the 35% marginal tax bracket, the cost of permanently maintaining this $80 million

reserve is closest to:

A) $0.85 million

B) $1.6 million

C) $24.0 million

D) $28.0 million

Answer:

Use the information for the question(s) below.

Luther Industries has $5 million in excess cash and 1 million shares outstanding. Luther

is considering investing the cash in one-year treasury bills that are currently paying 5%

interest, and then using the cash to pay a dividend next year. Alternatively, Luther can

pay the cash out as a dividend immediately and the shareholders can invest in the

treasury bills themselves. Assume that capital markets are perfect.

If Luther decides to pay the dividend immediately the dividend per share will be closest

to:

A) $1.05

B) $5.25

C) $5.00

D) $4.75

Answer:

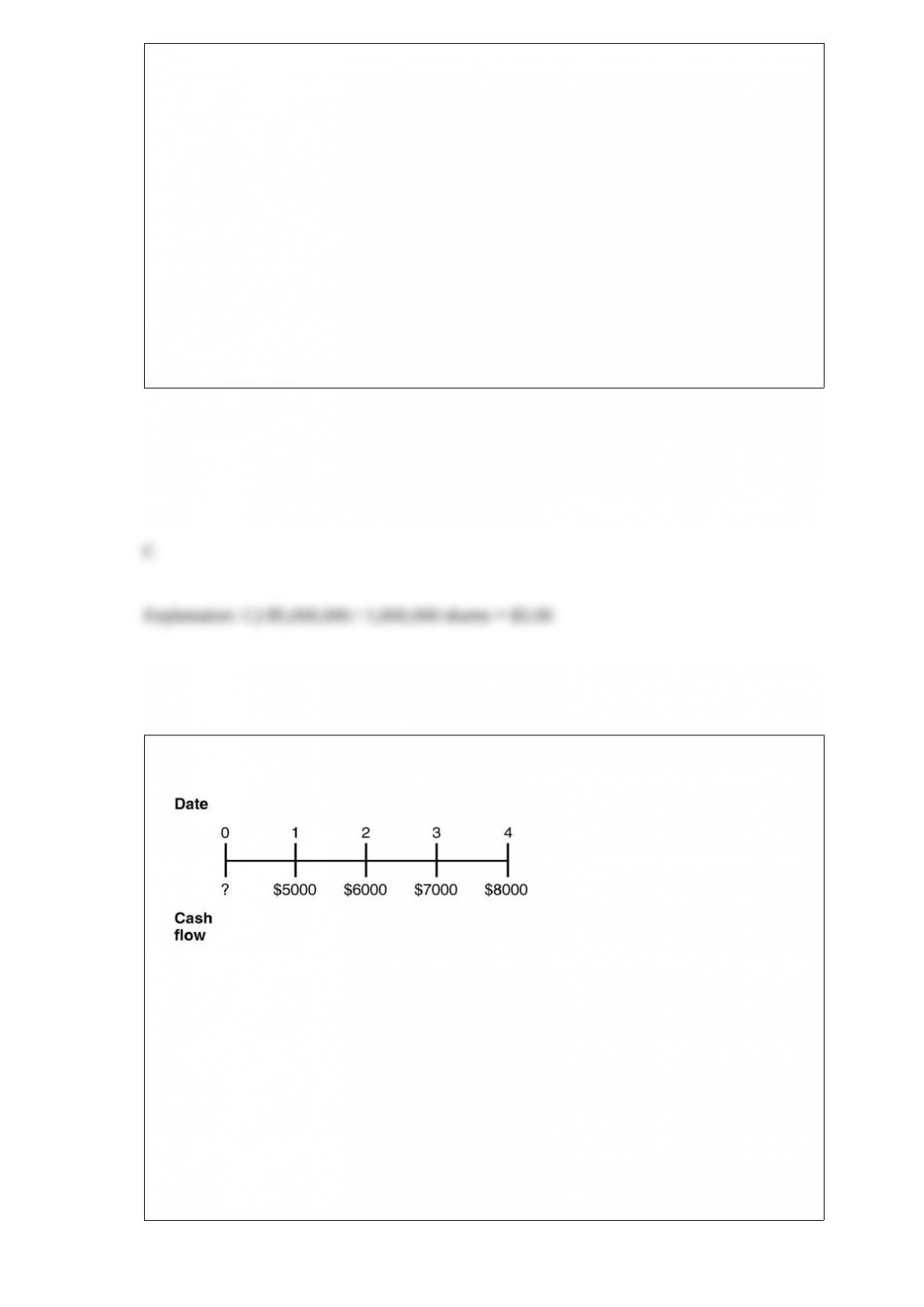

Consider the following timeline detailing a stream of cash flows:

If the current market rate of interest is 8%, then the present value of this stream of cash

flows is closest to:

A) $22,871

B) $21,211

C) $24,074

D) $26,000

Answer:

In practice which market index would best be used as a proxy for the market portfolio

in the CAPM?

A) S&P 500

B) Dow Jones Industrial Average

C) U.S. Treasury Bill

D) Wilshire 5000

Answer:

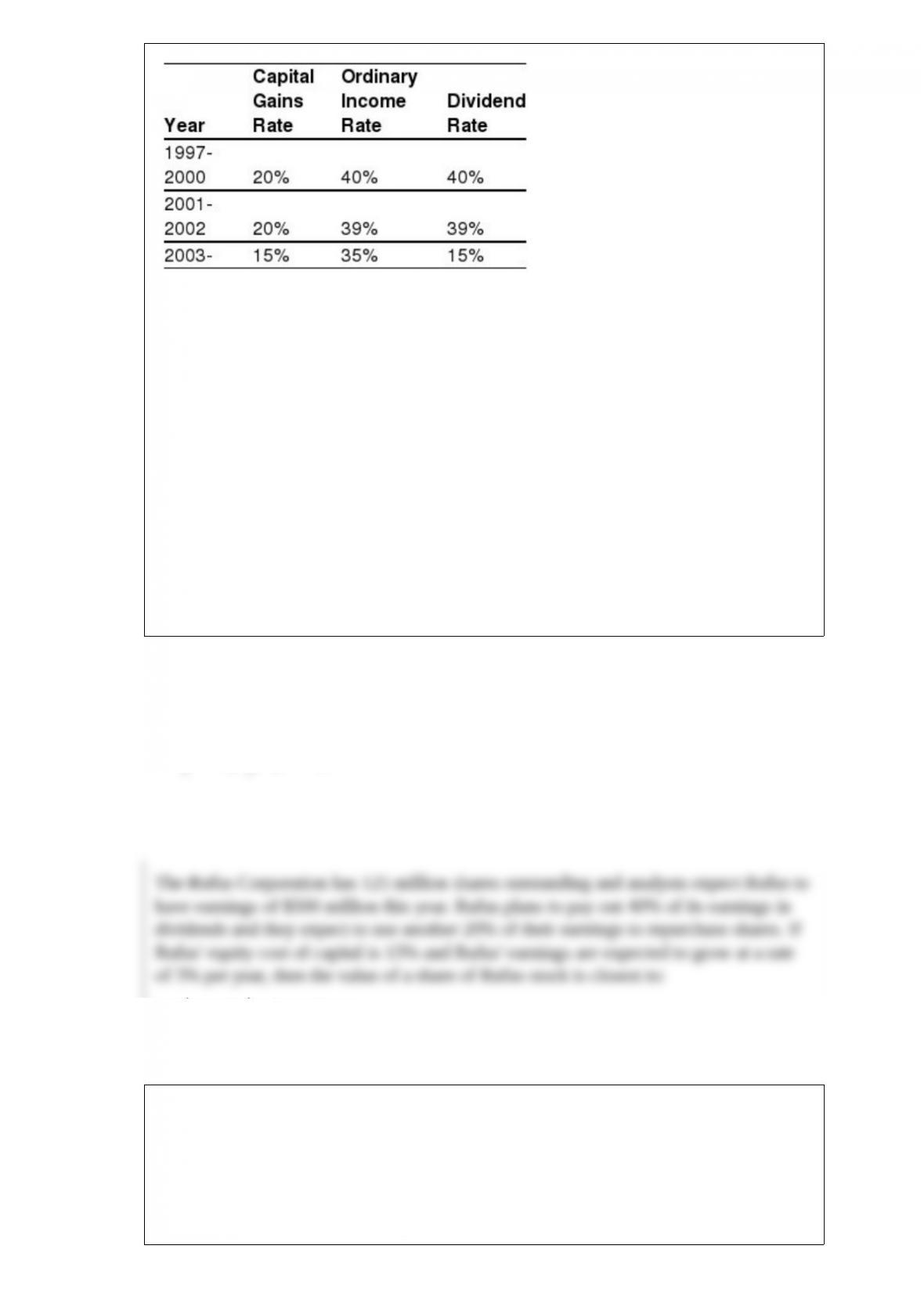

Use the information for the question(s) below.

Consider the following tax rates:

*The current tax rates are set to expire in 2008 unless Congress extends them. The tax

rates shown are for financial assets held for one year. For assets held less than one year,

capital gains are taxed at the ordinary income tax rate (currently 35% for the highest

bracket); the same is true for dividends if the assets are held for less than 61 days.

The effective dividend tax rate for a pension fund in 1999 is closest to:

A) 40%

B) 20%

C) 0%

D) 25%

Answer:

The Rufus Corporation has 125 million shares outstanding and analysts expect Rufus to

have earnings of $500 million this year. Rufus plans to pay out 40% of its earnings in

dividends and they expect to use another 20% of their earnings to repurchase shares. If

Rufus’ equity cost of capital is 15% and Rufus’ earnings are expected to grow at a rate

of 3% per year, then the value of a share of Rufus stock is closest to:

A) $13.35

B) $33.50

C) $20.00

D) $16.00

Answer:

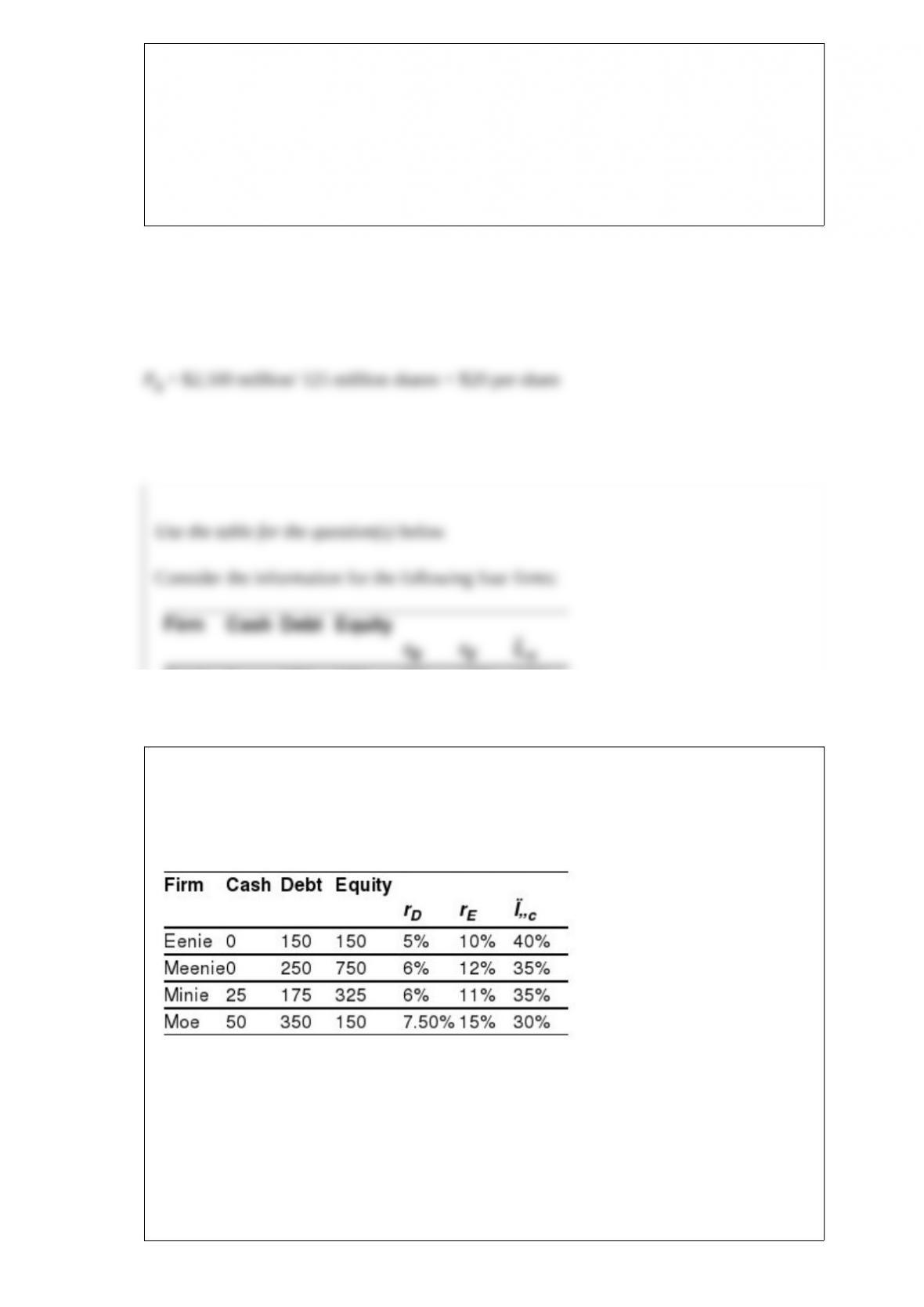

Use the table for the question(s) below.

Consider the information for the following four firms:

The unlevered cost of capital for “Eenie” is closest to:

A) 6.0%

B) 5.5%

C) 7.5%

D) 6.5%

Answer:

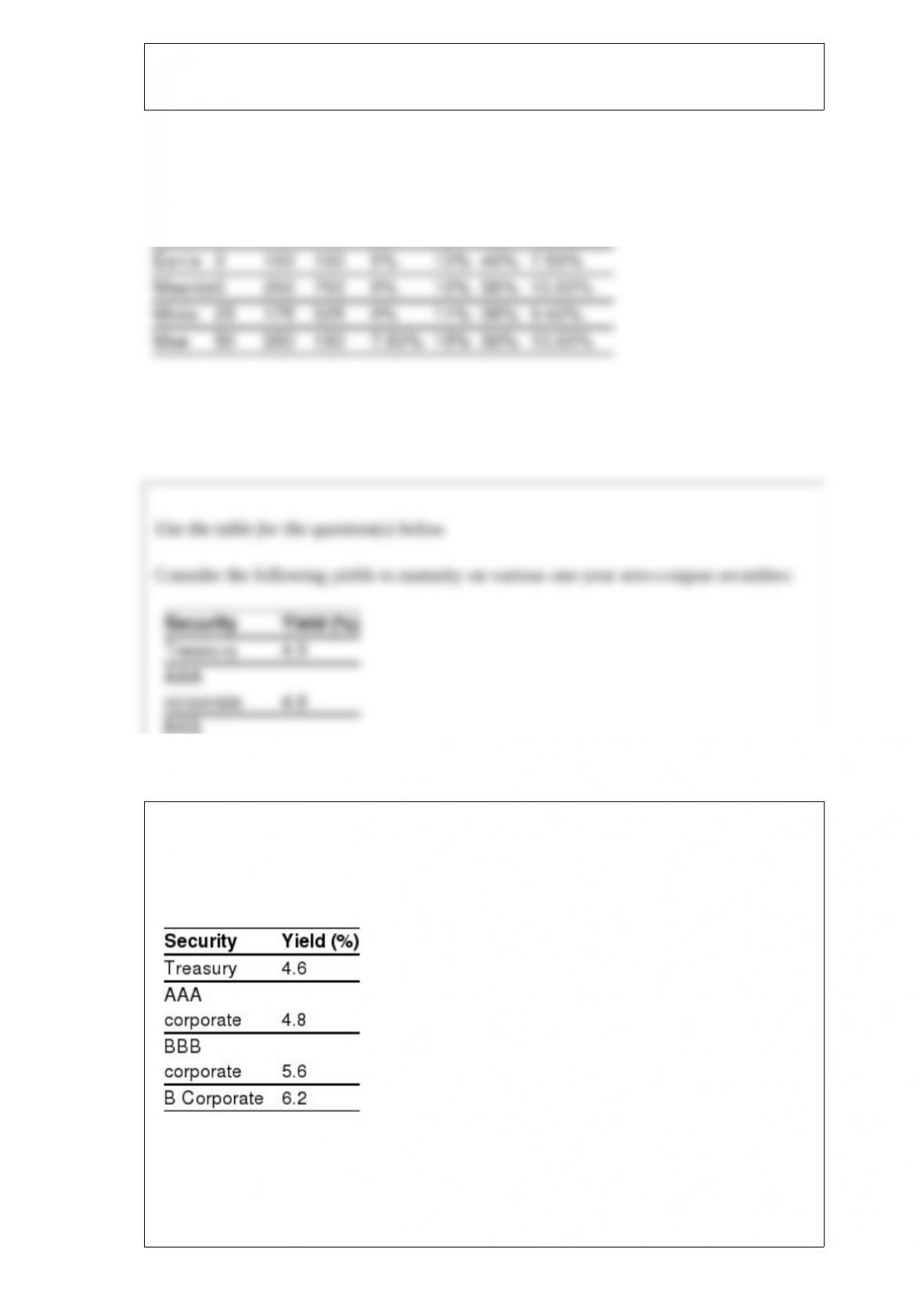

Use the table for the question(s) below.

Consider the following yields to maturity on various one-year zero-coupon securities:

The credit spread of the BBB corporate bond is closest to:

A) 1.0%

B) 5.6%

C) 1.6%

D) 0.8%

Answer:

This period is known for hostile, “bust-up” takeovers, in which the acquirer purchased a

poorly performing conglomerate and sold off its individual business units for more than

the purchase price:

A) 1960s

B) 1970s

C) 1980s

D) 1990s

Answer:

Which of the following statements is false?

A) A convertible bond can be thought of as a regular bond plus a special type of call

option called a warrant.

B) On the maturity date of the bond, the strike price of the embedded warrant in a

convertible bond is equal to the face value of the bond divided by the conversion

ratiothat is, the conversion price.

C) Calling a convertible bond transfers the remaining time value of the conversion

option from shareholders to bondholders.

D) If the stock price is low so that the embedded warrant is deep out-of-the-money, the

conversion provision is not worth much and the bond’s value is close to the value of a

straight bondan otherwise identical bond without the conversion provision.

Answer:

The beta for the risk free investment is closest to:

A) 1

B) 0

C) Unable to answer this question without knowing the risk free rate

D) Unable to answer this question without knowing the markets volatility

Answer:

Which of the following statements is false?

A) The intrinsic value of an option is the value it would have if it expired immediately.

B) A European option cannot be worth less than its American counterpart.

C) Put options increase in value as the stock price falls.

D) A put option cannot be worth more than its strike price.

Answer:

Which of the following statements is false?

A) If we increase the fraction invested in the efficient portfolio beyond 100%m we are

short selling the risk-free investment.

B) As we increase the fraction invested in the efficient portfolio, we increase our risk

premium but not our risk proportionately.

C) To earn the highest possible expected return for any level of volatility we must find

the portfolio that generates the steepest possible line when combined with the risk-free

investment.

D) Every investor should invest in the tangent portfolio independent of his or her taste

for risk.

Answer:

Which of the following statements is false?

A) When following a conservative financing policy, a firm would use long-term sources

of funds to finance its fixed assets, permanent working capital, and some of its seasonal

needs.

B) An aggressive financing policy also increases the possibility that managers of the

firm will use this excess cash nonproductivelyfor example, on perquisites for

themselves.

C) A firm could finance its short-term needs with long-term debt, a practice known as a

conservative financing policy.

D) To implement a conservative financing policy effectively, there will necessarily be

periods when excess cash is availablethose periods when the firm requires little or no

investment in temporary working capital.

Answer:

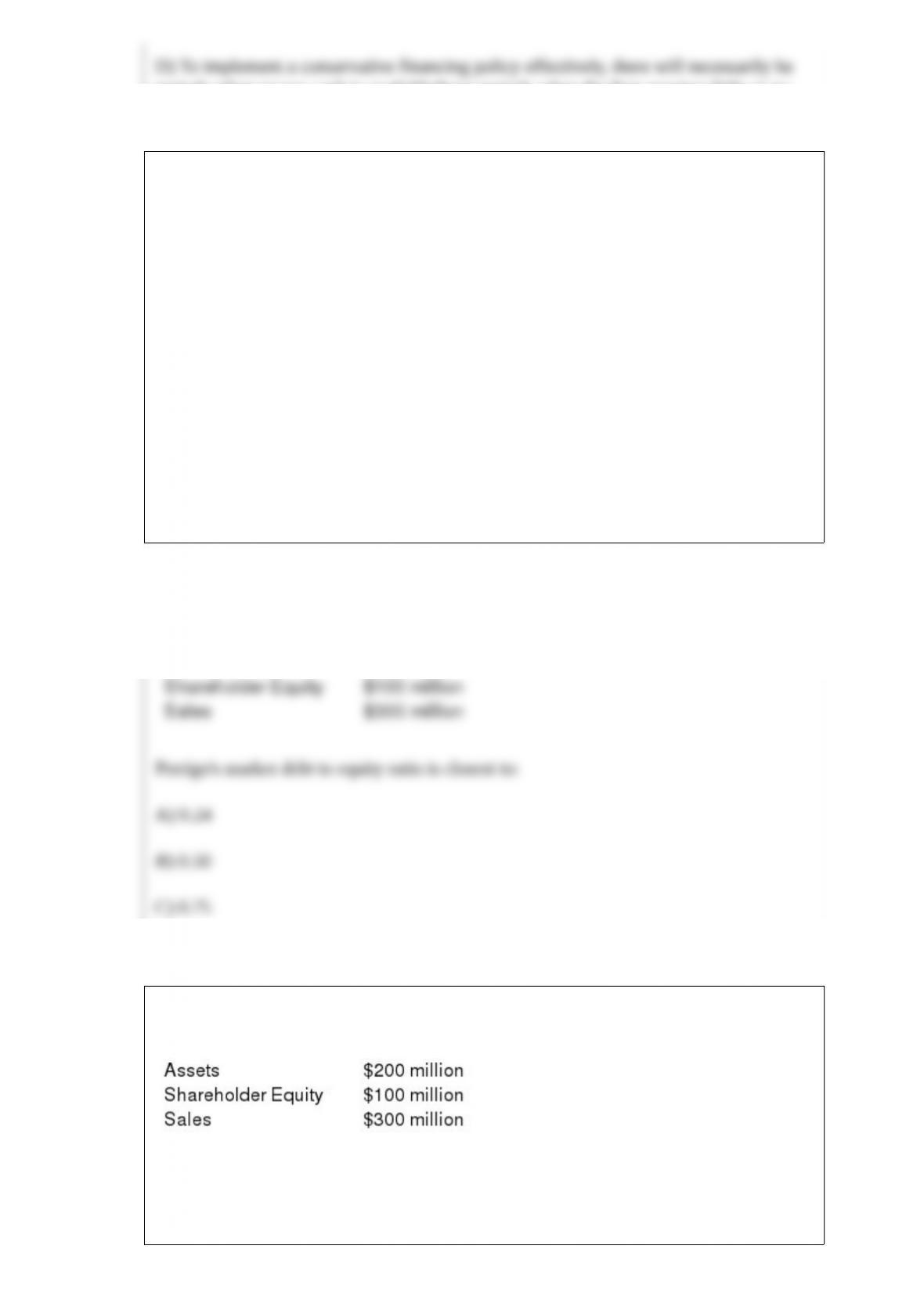

Use the following information for ECE incorporated:

Perrigo’s market debt to equity ratio is closest to:

A) 0.24

B) 0.50

C) 0.75

D) 0.89

Answer:

With a(n) ________, the buyer pays a premium to the seller and receives a payment

from the seller to make up for the loss if the underlying bond defaults.

A) equity option swap

B) credit default swap

C) risk-free swap

D) interest rate swap

Answer:

Which of the following statements regarding growing perpetuities is false?

A) We assume that r < g for a growing perpetuity.

B) PV of a growing perpetuity =

C) To find the value of a growing perpetuity one cash flow at a time would take forever.

D) A growing perpetuity is a cash flow stream that occurs at regular intervals and grows

at a constant rate forever.

Answer:

Use the information for the question(s) below.

You are in the process of purchasing a new automobile that will cost you $27,500. The

dealership is offering you either a $2,500 rebate (applied toward the purchase price) or

1.9% financing for 48 months (with payments made at the end of the month). You have

been pre-approved for an auto loan through your local credit union at an interest rate of

6.5% for 48 months.

If you forgo the $2,500 rebate and finance your new car through the dealership your

monthly payments (with payments made at the end of the month) will be closest to:

A) $520

B) $573

C) $595

D) $799

Answer:

Which of the following is not one of the four characteristics of IPOs that puzzle

financial economists?

A) On average, IPOs appear to be underpriced.

B) The long-run performance of a newly public company (three to five years from the

date of issue) is superior to the overall market return.

C) The number of issues is highly cyclical.

D) The costs of the IPO are very high, and it is unclear why firms willingly incur such

high costs.

Answer:

Consider the following prices from a McDonald’s Restaurant:

A McDonald’s Big Mac value meal consists of a Big Mac Sandwich, Large Coke, and a

Large Fry. Assume that there is a competitive market for McDonald’s food items and

that McDonalds sells the Big Mac value meal for $4.79. Does an arbitrage opportunity

exists and if so how would you exploit it and how much would you make on one extra

value meal?

A) Yes, buy extra value meal and then sell Big Mac, Coke, and Fries to make arbitrage

profit of $0.68

B) No, no arbitrage opportunity exists

C) Yes, buy Big Mac, Coke, and Fries then sell value meal to make arbitrage profit of

$1.09

D) Yes, buy Big Mac, Coke, and Fries then sell value meal to make arbitrage profit of

$0.68

Answer:

Which of the following statements is false?

A) Because investment in permanent working capital is required so long as the firm

remains in business, it constitutes a long-term investment.

B) Because temporary working capital represents a short-term need, the firm should

finance this portion of its investment with short-term financing.

C) Temporary working capitalis the difference between the lowest level of investment

in short-term assets and the permanent working capital investment.

D) The matching principlestates that short-term needs should be financed with

short-term debt and long-term needs should be financed with long-term sources of

funds.

Answer:

Use the information for the question(s) below.

Rosewood Industries has EBIT of $450 million, interest expense of $175 million, and a

corporate tax rate of 35%.

The total of Rosewood’s net income and interest payments is closest to:

A) $270 million

B) $355 million

C) $290 million

D) $450 million

Answer:

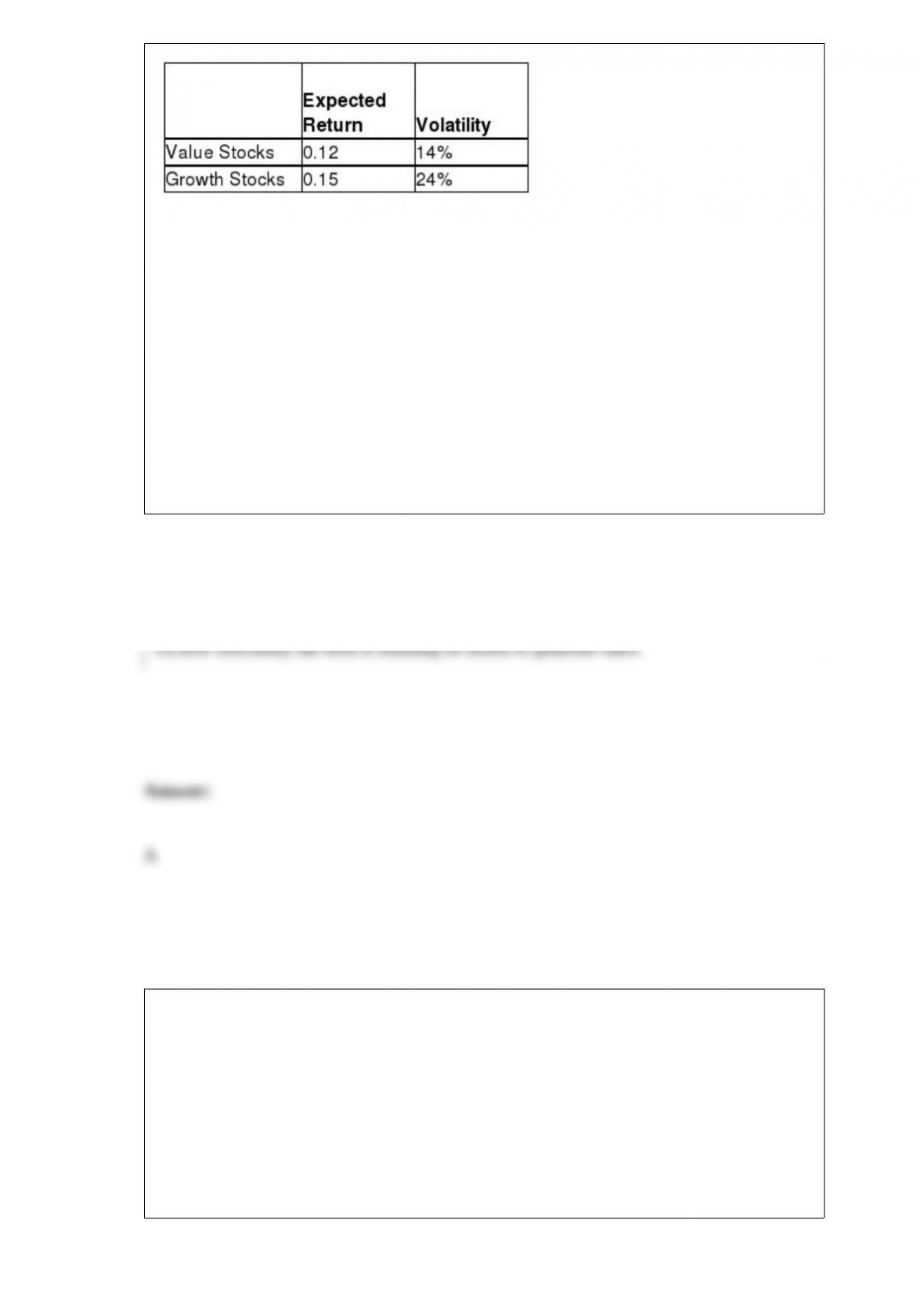

Use the following information to answer the question(s) below.

Suppose that all stocks can be grouped into two mutually exclusive portfolios (with

each stock appearing in only one portfolio): growth stocks and value stocks. Assume

that these two portfolios are equal in size (market value), the correlation of their returns

is equal to 0.6, and the portfolios have the following characteristics:

The risk free rate is 3.5%.

The volatility on the market portfolio (which is a 50-50 combination of the value and

growth portfolios) is closest to:

A) 13.5%

B) 15.2%

C) 17.1%

D) 19.0%

Answer:

The firm’s equity multiplier measures

A) the value of assets held per dollar of shareholder equity.

B) the return the firm has earned on its past investments.

C) the firm’s ability to sell a product for more than the cost of producing it.

D) how efficiently the firm is utilizing its assets to generate sales.

Answer:

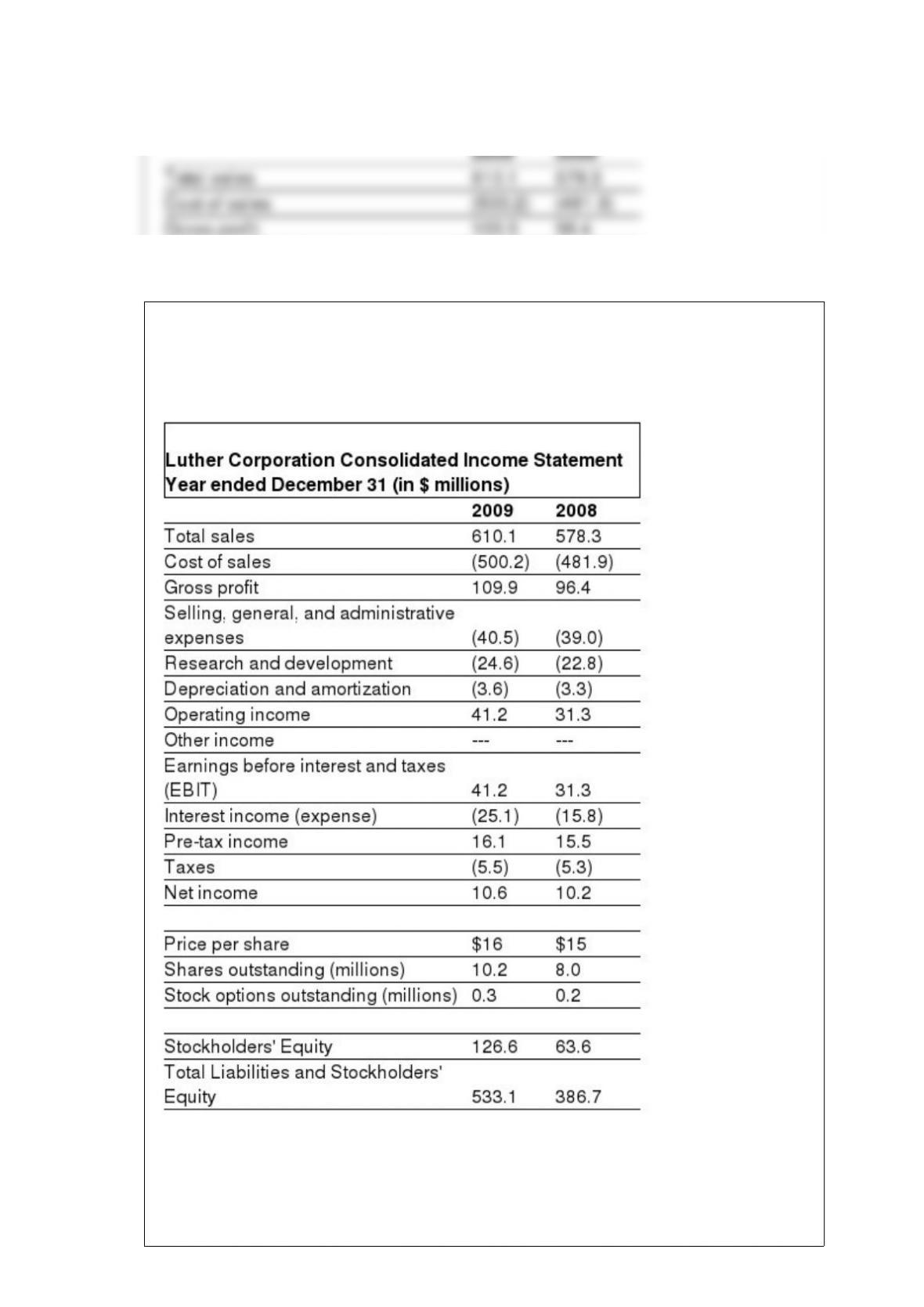

Consider the following income statement and other information:

Luther’s earnings before interest, taxes, depreciation, and amortization (EBITDA) for

the year ending December 31, 2009 is closest to:

A) 19.7 million

B) 37.6 million

C) 41.2 million

D) 44.8 million

Answer:

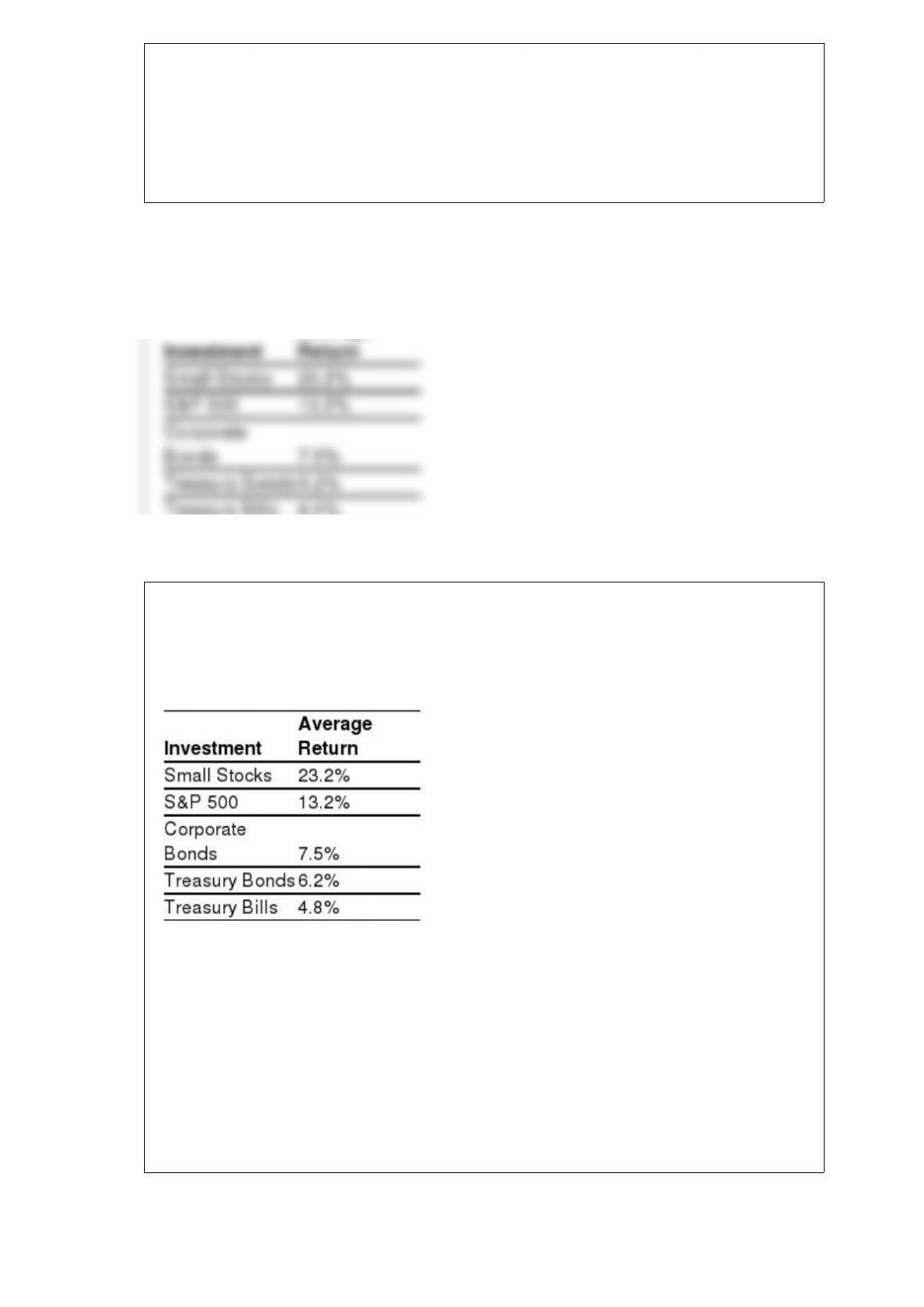

Use the table for the question(s) below.

Consider the following average annual returns:

What is the excess return for corporate bonds?

A) 2.7%

B) 1.3%

C) -5.7%

D) 0%

Answer:

Which of the following statements is false?

A) The equity cost of capital for a stock is the expected return of other investments

available in the market with equivalent risk to the firm’s shares.

B) The price of a share of stock is equal to the present value of the expected future

dividends it will pay.

C) If the current stock price were less than P0 = , it would be a negative NPV

investment, and we would expect investors to rush in and sell it, driving down the

stocks price.

D) The law of one price implies that to value any security, we must determine the

expected cash flows an investor will receive from owning it.

Answer: