1) Bowman, Inc., has only variable costs and fixed costs. A review of the company’s

records disclosed that when 200,000 units were produced, fixed manufacturing costs

amounted to $800,000 and the cost per unit manufactured totaled $11. On the basis of

this information, how much cost would the firm anticipate at an activity level of

205,000 units?

A.$2,235,000

B.$2,222,000

C.$2,214,000

D.$2,200,000

E.None of the other answers is correct

2) For the year just ended, Cole Corporation’s manufacturing costs (raw materials used,

direct labor, and manufacturing overhead) totaled $1,500,000. Beginning and ending

work-in-process inventories were $60,000 and $90,000, respectively. Cole’s balance

sheet also revealed respective beginning and ending finished-goods inventories of

$250,000 and $180,000. On the basis of this information, how much would the

company report as cost of goods manufactured (CGM) and cost of goods sold (CGS)?

A.CGM, $1,430,000; CGS, $1,460,000

B.CGM, $1,470,000; CGS, $1,540,000

C.CGM, $1,530,000; CGS, $1,460,000

D.CGM, $1,570,000; CGS, $1,540,000

E.Some other amounts

3) Cornwall Corporation manufactures faucets. Several weeks ago, the company

received a special-order inquiry from Yates, Inc. Yates desires to market a faucet similar

to Cornwall’s model no. 55 and has offered to purchase 3,000 units. The following data

are available:

Cost data for Cornwall’s model no. 55 faucet: direct materials, $45; direct labor, $30 (2

hours at $15 per hour); and manufacturing overhead, $70 (2 hours at $35 per hour).

The normal selling price of model no. 55 is $180; however, Yates has offered Cornwall

only $115 because of the large quantity it is willing to purchase.

Yates requires a design modification that will allow a $4 reduction in direct-material

cost.

Cornwall’s production supervisor notes that the company will incur $8,700 in additional

set-up costs and will have to purchase a $3,300 special device to manufacture these

units. The device will be discarded once the special order is completed.

Total manufacturing overhead costs are applied to production at the rate of $35 per

labor hour. This figure is based, in part, on budgeted yearly fixed overhead of $624,000

and planned production activity of 24,000 labor hours.

Cornwall will allocate $5,000 of existing fixed administrative costs to the order as “part

of the cost of doing business.”

Required:

A. One of Cornwall’s staff accountants wants to reject the special order because

“financially, it’s a loser.” Do you agree with this conclusion if Cornwall currently has

excess capacity? Show calculations to support your answer.

B. If Cornwall currently has no excess capacity, should the order be rejected from a

financial perspective? Briefly explain.

C. Assume that Cornwall currently has no excess capacity. Would outsourcing be an

option that Cornwall could consider if management truly wanted to do business with

Yates? Briefly discuss, citing several key considerations for Cornwall in your answer.

4) A statistical control chart is best used for determining:

A.direct-material price variances

B.direct-labor variances

C.whether a variance is favorable or unfavorable

D.who should be held accountable for specific variances

E.whether a particular variance should be investigated

5) Which of the following is not a provision of (nor an outgrowth of) the

Sarbanes-Oxley Act?

A.A public company’s annual report must contain a separate disclosure that assesses the

company’s internal controls

B.Management is essentially responsible for establishing and maintaining internal

controls

C.A company’s Chief Executive Officer (CEO) and Chief Financial Officer (CFO) can

be held criminally responsible if their firm’s financial statements are fraudulent

D.A company must prepare a balance sheet, an income statement, a statement of

stockholders’ equity, and a statement of cash flows

E.A new body, the Public Company Accounting Oversight Board, oversees and

investigates the audits and auditors of public companies

6)

If the cost of goods sold for the year was $427,500, what was the cost of goods

manufactured for the year?

A.$402,100

B.$422,300

C.$417,100

D.$427,500

E.None of the other answers are correct

7) Taurus Company has set various goals, and management is now taking appropriate

action to ensure that the firm achieves these goals. One such action is to reduce outlays

for overhead, which have exceeded budgeted amounts. Which of the following

functions best describes this process?

A.Decision making

B.Planning

C.Coordinating

D.Controlling

E.Organizing

8) Consumption ratios are useful in determining:

A.the existence of product-line diversity

B.overhead that is incurred at the unit level

C.if overhead-producing activities are being utilized effectively

D.if overhead costs are being applied to products

E.if overhead-producing activities are being utilized efficiently

9) Astro’s customer service department follows up on customer complaints by telephone

inquiry. During a recent period, the department initiated 10,000 calls and incurred costs

of $312,000. Of these calls, 3,800 were for the company’s wholesale operation; the

remainder was for the retail division. Costs allocated to the retail division are:

A.$0

B.$31,200

C.$118,560

D.$193,440

E.$203,000

10) End-of-period figures for accounts receivable and payables to suppliers would be

found on the:

A.cash budget

B.budgeted schedule of cost of goods manufactured

C.budgeted income statement

D.budgeted balance sheet

E.budgeted statement of cash flows

11) DiAngelo Products uses a standard costing system to assist in the evaluation of

operations. The company has had considerable employee difficulties in recent months,

so much so that management has hired a new production supervisor (Joe Simms).

Simms has been on the job for six months and has seemingly brought order to an

otherwise chaotic situation.

The vice-president of manufacturing recently commented that ” Simms has really done

the trick. Joe’s team-building/morale-boosting exercises have truly brought things under

control.” The vice-president’s comments were based on both a plant tour, where he

observed a contented work force, and review of a performance report that showed a

total labor variance of $14,000F. This variance is truly outstanding, given that it is less

than 2% of the company’s budgeted labor cost. Additional data follow.

Total completed production amounted to 20,000 units.

A review of the firm’s standard cost records found that each completed unit requires

2.75 hours of labor at $14 per hour. DiAngelo’s production actually required 42,000

labor hours at a total cost of $756,000.

Required:

A. As judged by the information contained in the performance report, should the

vice-president be concerned about the company’s labor variances? Why?

B. Calculate DiAngelo’s direct-labor variances.

C. On the basis of your answers to requirement “B,” should DiAngelo be concerned

about its labor situation? Why?

D. Briefly analyze and explain the direct-labor variances.

12) Peach Company uses a weighted-average process-costing system. Company records

disclosed that the firm completed 40,000 units during the month and had 10,000 units in

process at month-end, 20% complete. Conversion costs associated with the beginning

work-in-process inventory amounted to $231,000, and amounts that relate to the current

month totaled $966,000. If conversion is incurred uniformly throughout manufacturing,

Peach’s equivalent-unit cost is:

A.$23.00

B.$23.94

C.$24.15

D.$28.50

E.None of the answers is correct

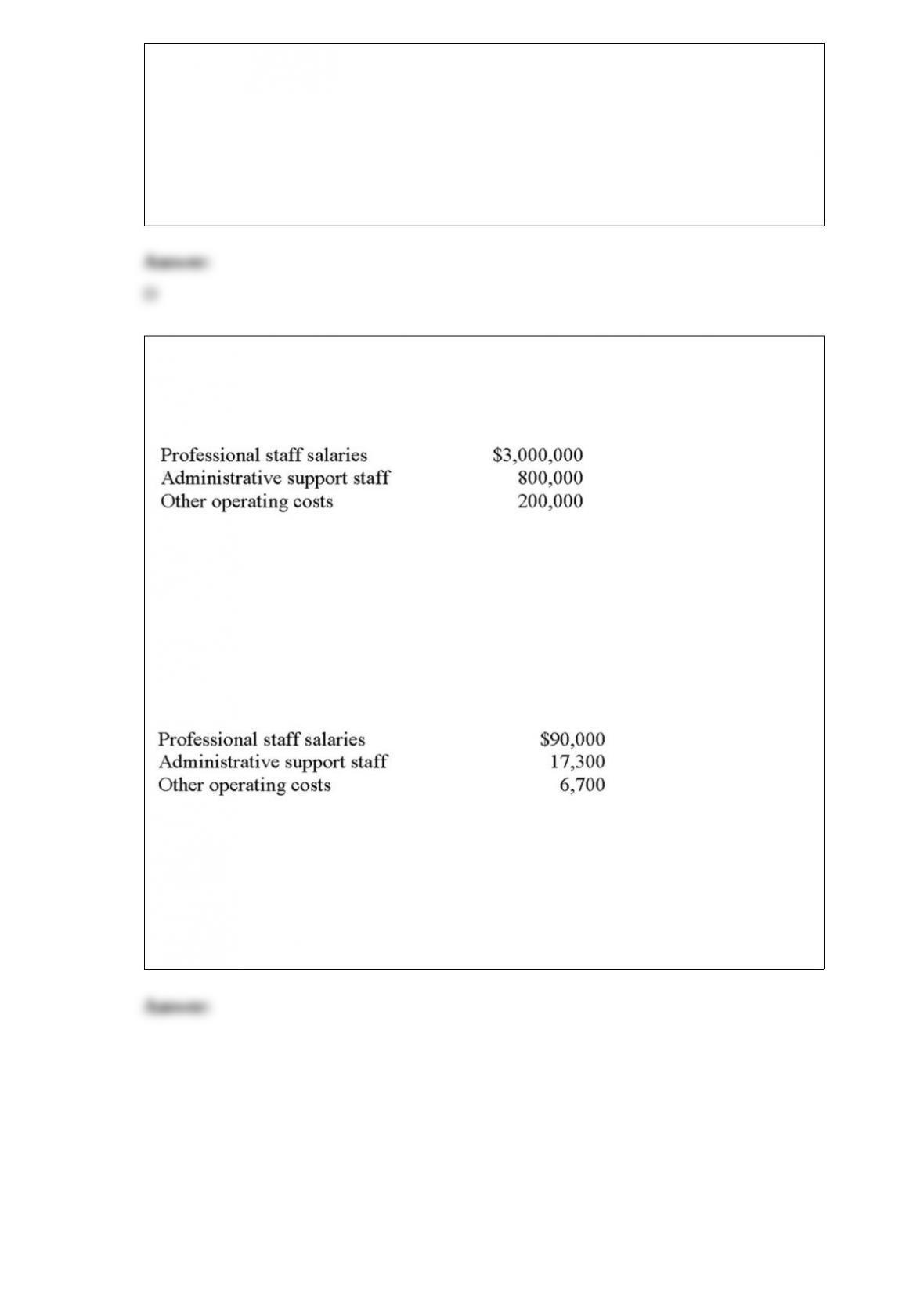

13) Boxworth and Associates designs relatively small sports stadiums and arenas at

various sites throughout the country. The firm’s accountant prepared the following

budget for the upcoming year:

Eighty percent of professional staff salaries are directly traceable to client projects, a

figure that falls to 60% for the administrative support staff and other operating costs.

Traceable costs are charged directly to client projects; nontraceable costs, on the other

hand, are treated as firm overhead and charged to projects by using a predetermined

overhead application rate.

Boxworth had one project in process at year-end: an arena that was being designed for

Charlotte County. Costs directly chargeable to this project were:

Required:

A. Determine Boxworth’s overhead for the year and the firm’s predetermined overhead

application rate. The rate is based on costs directly chargeable to firm projects.

B. Compute the cost of the Charlotte County arena project as of year-end.

C. Present three examples of “other operating costs” that might be directly traceable to

the Charlotte County project.

14) Electricity costs that were incurred by a company’s production processes should be

debited to:

A.Utilities Expense

B.Accounts Payable

C.Cash

D.Manufacturing Overhead

E.Work-in-Process Inventory

15) Phanatix, Inc. produces a variety of products that carry the logos of teams in the

Southern Football League (SFL). The company recently paid the league $85,000 for the

rights to market a popular player jersey and immediately began production. The

following information is available:

Number of jerseys manufactured: 25,000

Cost of jerseys manufactured: $625,000

Amount of manufacturing costs paid to-date: $410,000

Number of jerseys sold to-date: 0

Estimated future marketing costs: $330,000

Anticipated selling price per jersey: $42

The SFL is about to file a lawsuit to stop jersey sales and is demanding another $50,000

from Phanatix for the manufacturing rights. Conversations with Phanatix’s attorneys

indicate that the league has a strong case and is likely to win the suit. If this situation

arises, Phanatix will be unable to recover any amounts paid to the SFL.

Required:

Phanatix’s sales department anticipates very strong demand and a sellout of all jerseys

manufactured.

A. Determine the overall profitability of the jersey product line if Phanatix settles the

disagreement with the SFL and the anticipated sellout occurs.

B. Should the company pay the additional $50,000 demanded by the league or should

the jersey program be dropped? Show computations to support your answer.

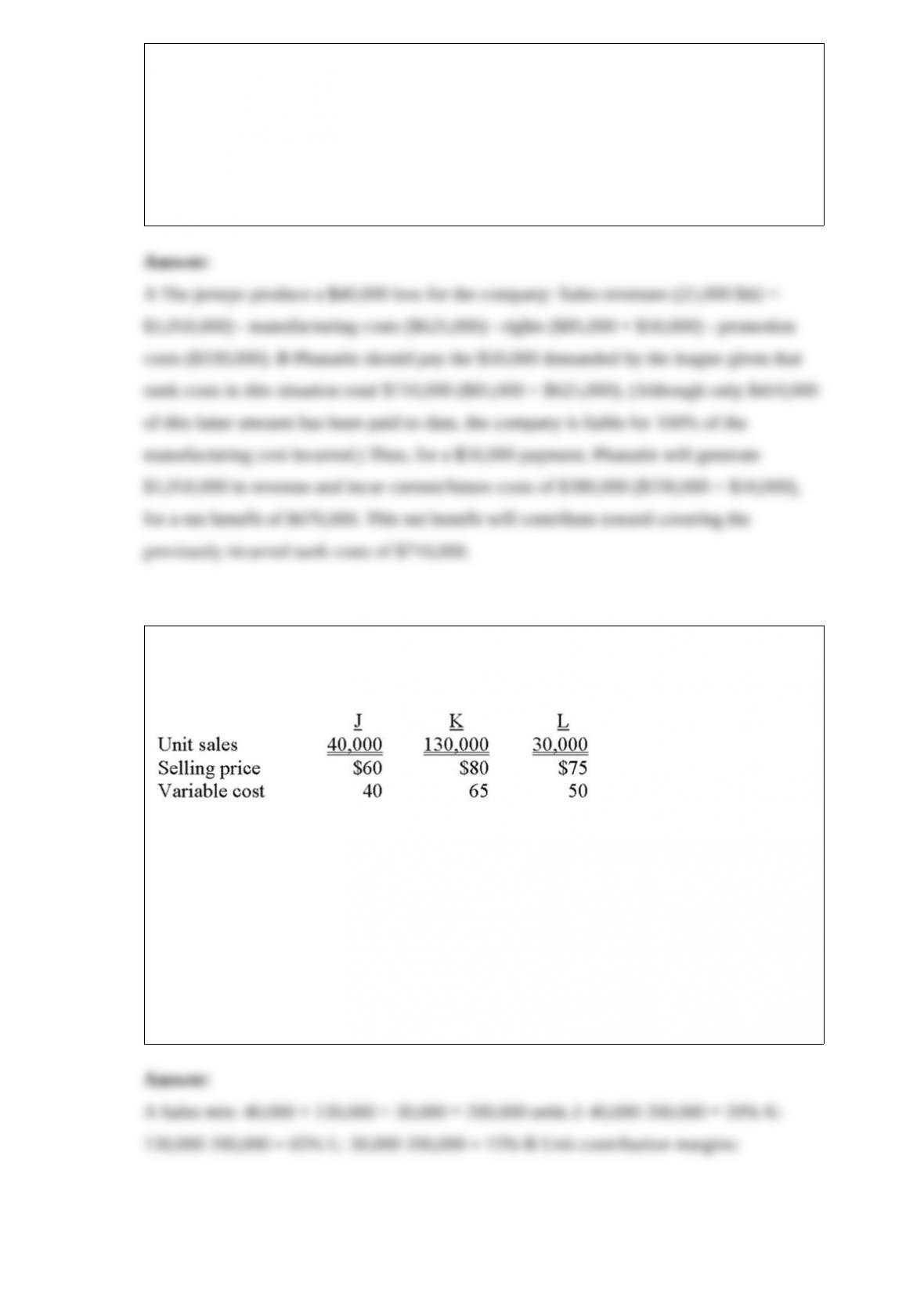

16) Alphabeta Corporation sells three products: J, K, and L. The following information

was taken from a recent budget:

Total fixed costs are anticipated to be $2,450,000.

Required:

A. Determine Alphabeta’s sales mix.

B. Determine the weighted-average contribution margin.

C. Calculate the number of units of J, K, and L that must be sold to break even.

D. If Alphabeta desires to increase company profitability, should it attempt to increase

or decrease the sales of product K relative to those of J and L? Briefly explain.

17) All other things being equal, a company that sells multiple products should attempt

to structure its sales mix so the greatest portion of the mix is composed of those

products with the highest:

A.selling price

B.variable cost

C.contribution margin

D.fixed cost

E.gross margin

18) The following events took place when Managers A, B, and C were preparing

budgets for the upcoming period:

I. Manager A increased property tax expenditures by 2% when she was informed of a

recent rate hike by local authorities.

II. Manager B reduced sales revenues by 4% when informed of recent aggressive

actions by a new competitor.

III. Manager C, who supervises employees with widely varying skill levels, used the

highest wage rate in the department when preparing the labor budget.

Assuming that the percentage amounts given are reasonable, which of the preceding

cases is (are) an example of building slack in budgets?

A.I only

B.II only

C.III only

D.I and II

E.II and III

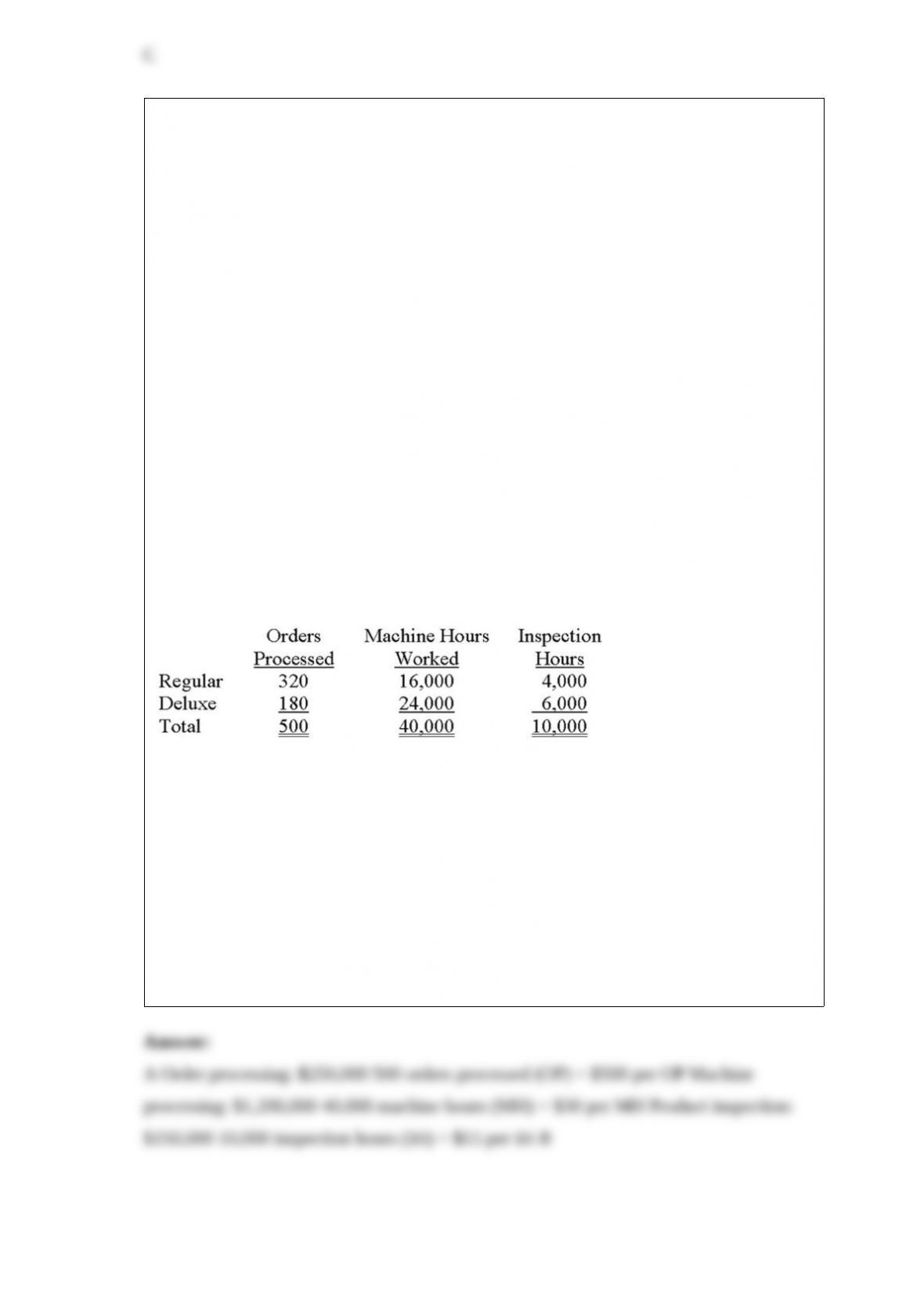

19) Scott, Inc., manufactures two products, Regular and Deluxe, and applies overhead

on the basis of direct labor hours. Anticipated overhead and direct labor time for the

upcoming accounting period are $1,600,000 and 25,000 hours, respectively.

Information about the company’s products follows.

Regular

Estimated production volume: 3,000 units

Direct materials cost: $28 per unit

Direct labor per unit: 3 hours at $15 per hour

Deluxe

Estimated production volume: 4,000 units

Direct materials cost: $42 per unit

Direct labor per unit: 4 hours at $15 per hour

Scott’s overhead of $1,600,000 can be identified with three major activities: order

processing ($250,000), machine processing ($1,200,000), and product inspection

($150,000). These activities are driven by number of orders processed, machine hours

worked, and inspection hours, respectively. Data relevant to these activities follow.

Required:

A. Compute the pool rates that would be used for order processing, machine processing,

and product inspection in an activity-based costing system.

B. Assuming use of activity-based costing, compute the unit manufacturing costs of

Regular and Deluxe if the expected manufacturing volume is attained.

C. How much overhead would be applied to a unit of Regular and Deluxe if the

company used traditional costing and applied overhead solely on the basis of direct

labor hours? Which of the two products would be undercosted by this procedure?

Overcosted?

20) Consumption ratios are useful in determining:

A.the existence of product-line diversity

B.overhead that is incurred at the unit level

C.if overhead-producing activities are being utilized effectively

D.if overhead costs are being applied to products

E.if overhead-producing activities are being utilized efficiently

21) Package Express, Inc. operates a small package delivery service in the Jacksonville

suburbs. If the company uses a regression equation to forecast total operating costs, the

coefficient of the equation’s independent variable would correspond to the:

A.variable operating cost per delivery

B.fixed operating costs

C.number of deliveries

D.total variable operating costs

E.total operating costs

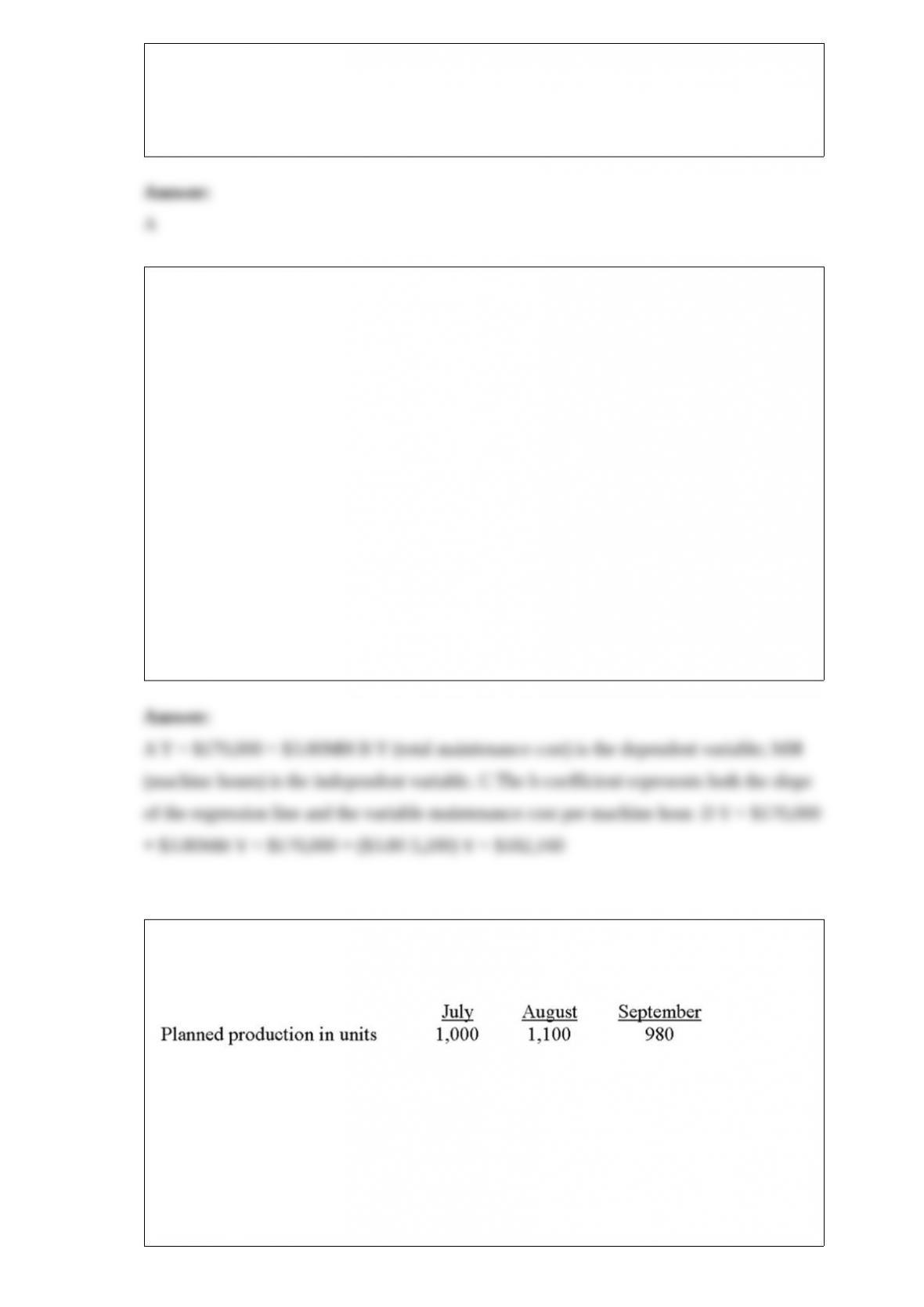

22) Ellington Corporation uses least-squares regression to analyze a variety of operating

costs. A staff assistant determined that monthly machine hours (MH) have a strong

cause-and-effect relationship with total maintenance costs, and generated the following

statistics:

Intercept: $170,000

b coefficient: $3.80

Total machine hours for the year: 36,500

Required:

A. Construct the company’s regression equation.

B. Based on your answer in part “A,” identify Ellington’s dependent variable and

independent variable.

C. What does the b coefficient really represent?

D. Predict the company’s maintenance cost in a month when 3,200 machine hours are

worked.

23) Northcutt’s production data for a new deluxe product were taken from the most

recent quarterly production budget:

In addition, Northcutt produces 5,000 units a month of its standard product. It takes two

direct labor hours to produce each standard unit and 2.25 direct labor hours to produce

each deluxe unit. Northwest’s cost per labor hour is $15. Direct labor cost for

September would be budgeted at:

A.$187,125

B.$183,075

C.$194,750

D.$197,075

E.None of the other answers are correct

24) Wesley Enterprises has determined that three variables play a key role in

determining company revenues. To arrive at an objective forecast of revenues for the

next accounting period, Wesley should use:

A.simple regression

B.multiple regression

C.a scatter diagram

D.complex regression

E.the high-low method

25) Many traditional costing systems:

A.trace manufacturing overhead to individual activities and require the development of

numerous activity-costing rates

B.write off manufacturing overhead as an expense of the current period

C.combine widely varying elements of overhead into a single cost pool

D.use a host of different cost drivers (e.g., number of production setups, inspection

hours, orders processed) to improve the accuracy of product costing

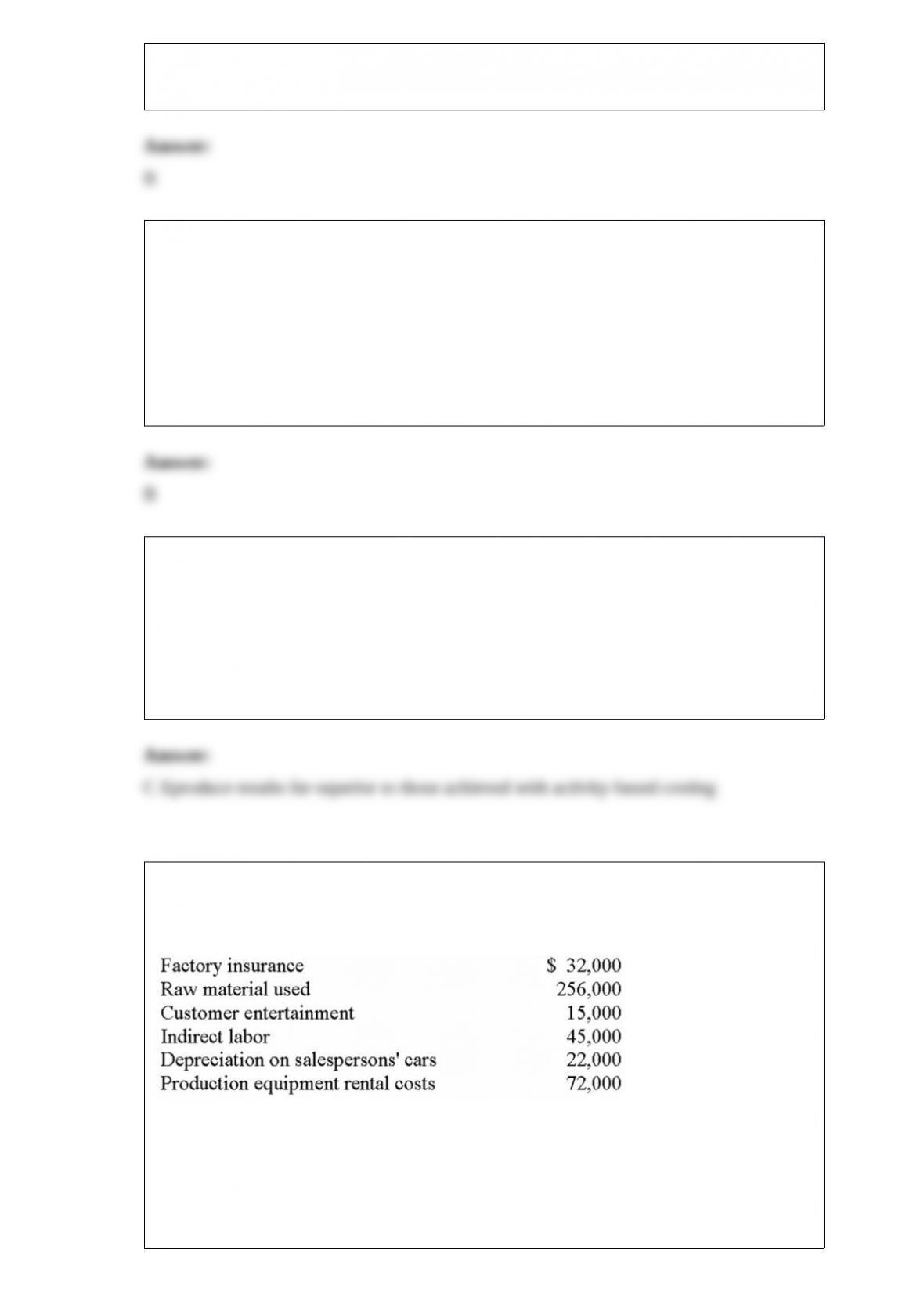

26) The accounting records of Diego Company revealed the following costs, among

others:

Costs that would be considered in the calculation of manufacturing overhead total:

A.$149,000

B.$171,000

C.$186,000

D.$442,000

E.None of the other answers are correct

27) A division’s return on investment may be improved by increasing:

A.cost of goods sold and expenses

B.sales margin and cost of capital

C.sales revenue and cost of capital

D.capital turnover or sales margin

E.capital turnover or cost of capital

28) On a graph where the horizontal axis represents quantity sold and the vertical axis

represents selling price, the basic demand curve in a competitive market can be

graphed:

A.as a horizontal line

B.as a vertical line

C.as a downward sloping line to the right

D.as an upward sloping line to the right

E.in the same manner as the total revenue curve

29) Courtney purchased and consumed 50,000 gallons of direct material that was used

in the production of 11,000 finished units of product. According to engineering

specifications, each finished unit had a manufacturing standard of five gallons. If a

review of Courtney’s accounting records at the end of the period disclosed a material

price variance of $5,000U and a material quantity variance of $3,000F, what is the

actual price paid for a gallon of direct material?

A.$0.50

B.$0.60

C.$0.70

D.None of the other answers are correct

E.Not enough information to judge

30) Which of the following statements about the visual-fit method is (are) true?

I. The method results in the creation of a scatter diagram.

II. The method is not totally objective because of the manner in which the cost line is

determined.

III. The method is especially helpful in the determination of outliers.

A.I only

B.II only

C.I and II

D.I and III

E.I, II, and III

31) When calculating unit costs under the weighted-average process-costing method,

the unit cost is based on:

A.only the current period’s manufacturing costs

B.only costs in the period’s beginning work-in-process inventory

C.a summation of the costs in the beginning work-in-process inventory plus costs

incurred in the current period

D.only costs incurred in previous accounting periods

E.a summation of the costs in the beginning work-in-process inventory plus costs to be

incurred in the upcoming period

32) An organization’s budgets will often be prepared to cover:

A.one month

B.one quarter

C.one year

D.periods longer than one year

E.all of the other answers are correct

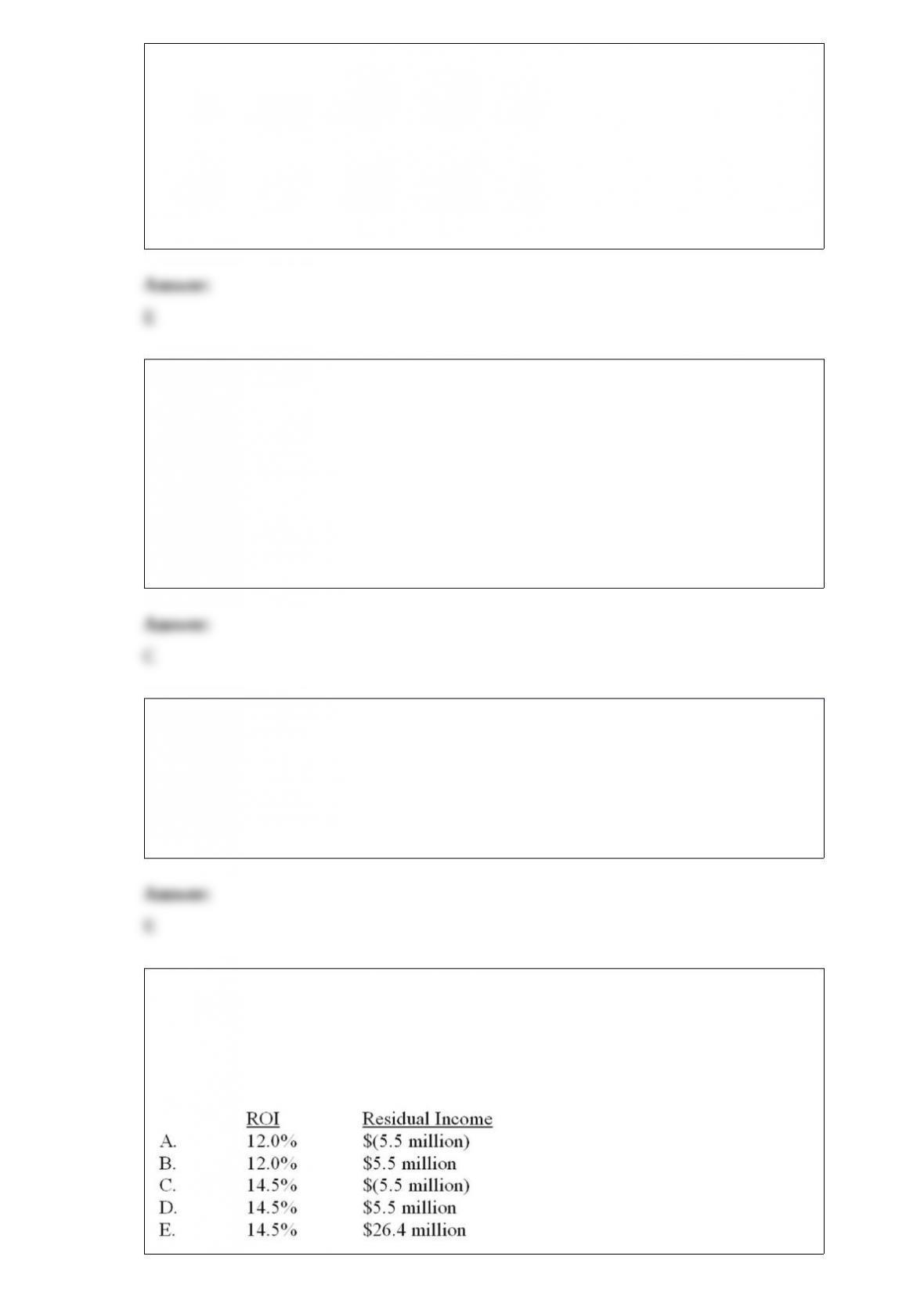

33) For the period just ended, United Corporation’s Delta Division reported profit of

$31.9 million and invested capital of $220 million. Assuming an imputed interest rate of

12%, which of the following choices correctly denotes Delta’s return on investment

(ROI) and residual income?

A.Choice A

B.Choice B

C.Choice C

D.Choice D

E.Choice E

34) Consider the following statements about the payback period:

I. As shown in your text, the payback period considers the time value of money.

II. The payback period can only be used if net cash inflows are uniform throughout a

project’s life.

III. The payback period ignores cash inflows that occur after the payback period is

reached.

Which of the above statements is (are) correct?

A.I only

B.II only

C.III only

D.I and II

E.I, II, and III

35) Which of the following statements about the use of direct labor as a cost driver is

false?

A.Direct labor is the most commonly used cost driver when calculating a predetermined

overhead rate

B.Direct labor is gaining importance in many manufacturing applications with respect

to being a significant cost driver

C.Direct labor is an inappropriate cost driver to use if a company is highly automated

D.If direct labor is a good cost driver, increases in direct labor are matched with

increases in manufacturing overhead

E.Companies can use either direct labor cost or direct labor hours as a cost driver