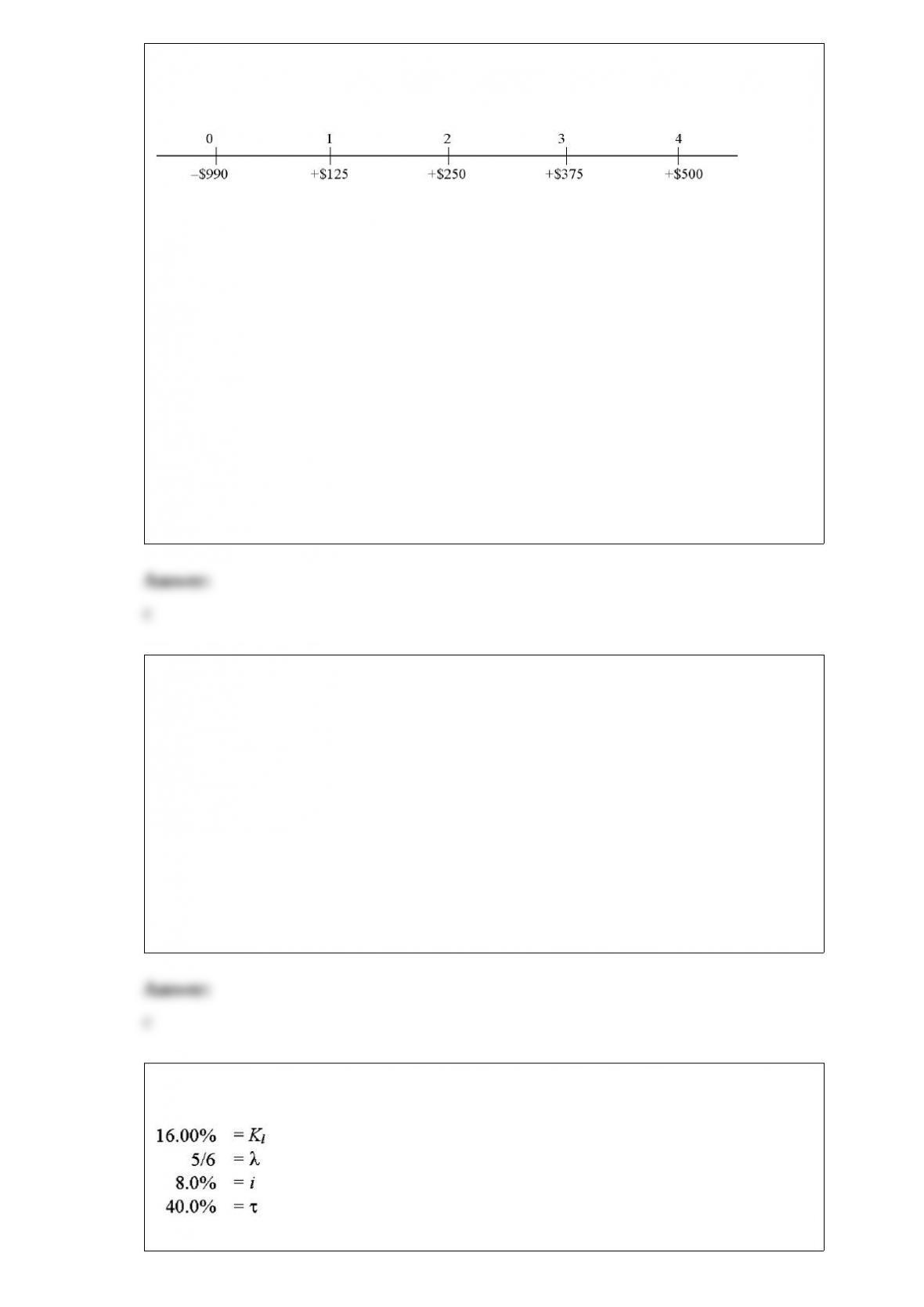

1) consider a project of the cornell haul moving company, the timing and size of the

incremental after-tax cash flows (for an all-equity firm) are shown below in millions:

the firm’s tax rate is 34%; the firm’s bonds trade with a yield to maturity of 8%; the

current and target debt-equity ratio is 2; if the firm were financed entirely with equity,

the required return would be 10%

using the flow to equity methodology, what is the value of the equity claim?

a.-$1,540,000

b.$446,570,866.00

c.$36,580,767.55

d.$470,953,393.70

e.$30,716,236.13

2) during the period between world war i and world war ii,

a.the major european powers and the u.s. returned to the gold standard and fixed

exchange rates

b.while most countries abandoned the gold standard during world war i, international

trade and investment flourished during the interwar period under a coherent

international monetary system

c.the u.s. dollar emerged as the dominant world currency, gradually replacing the british

pound for the role

d.none of the above

3) solve for the weighted average cost of capital:

a.7.00%

b.6.89%

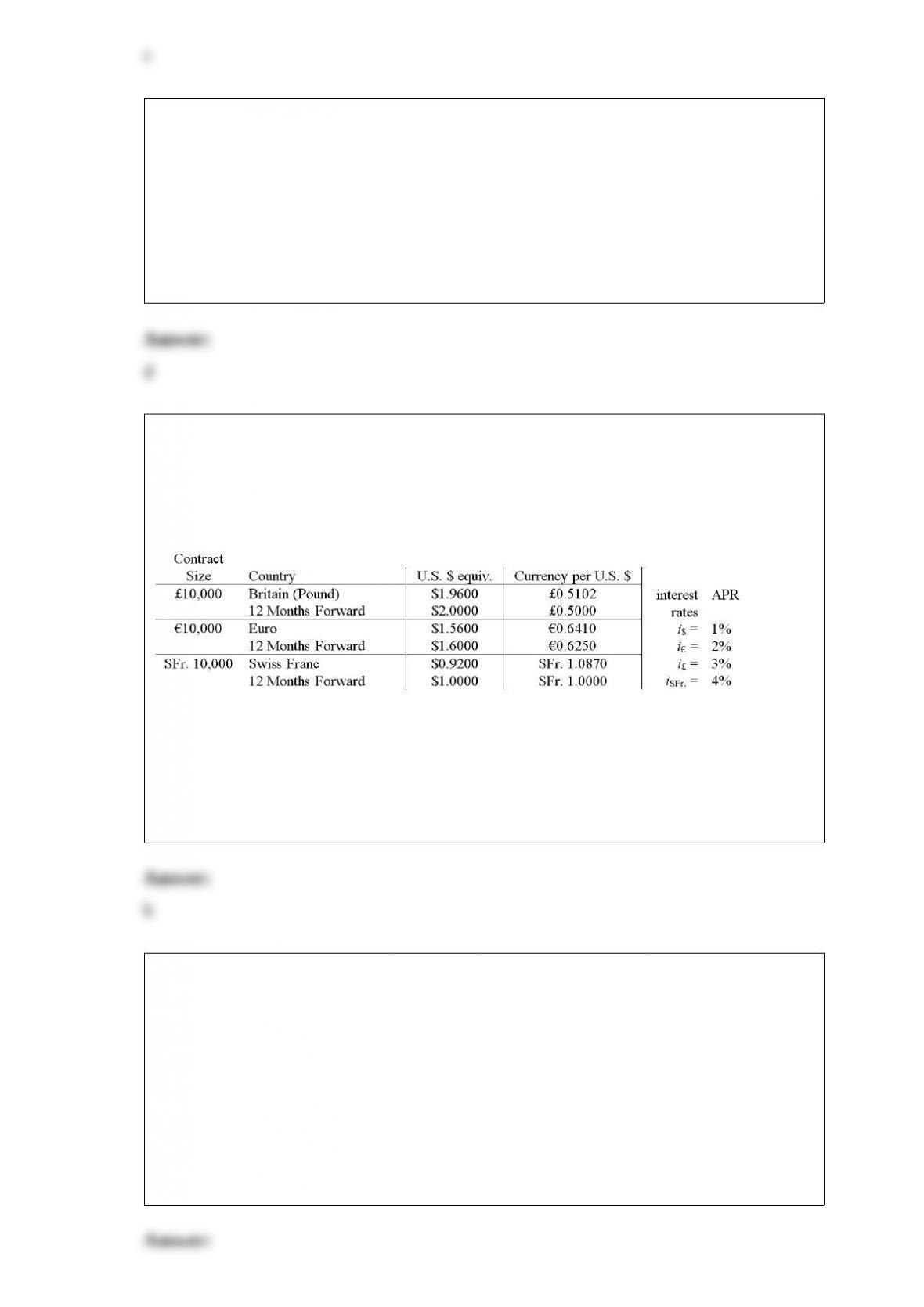

c.6.73%

d.6.67%

e.6.57%

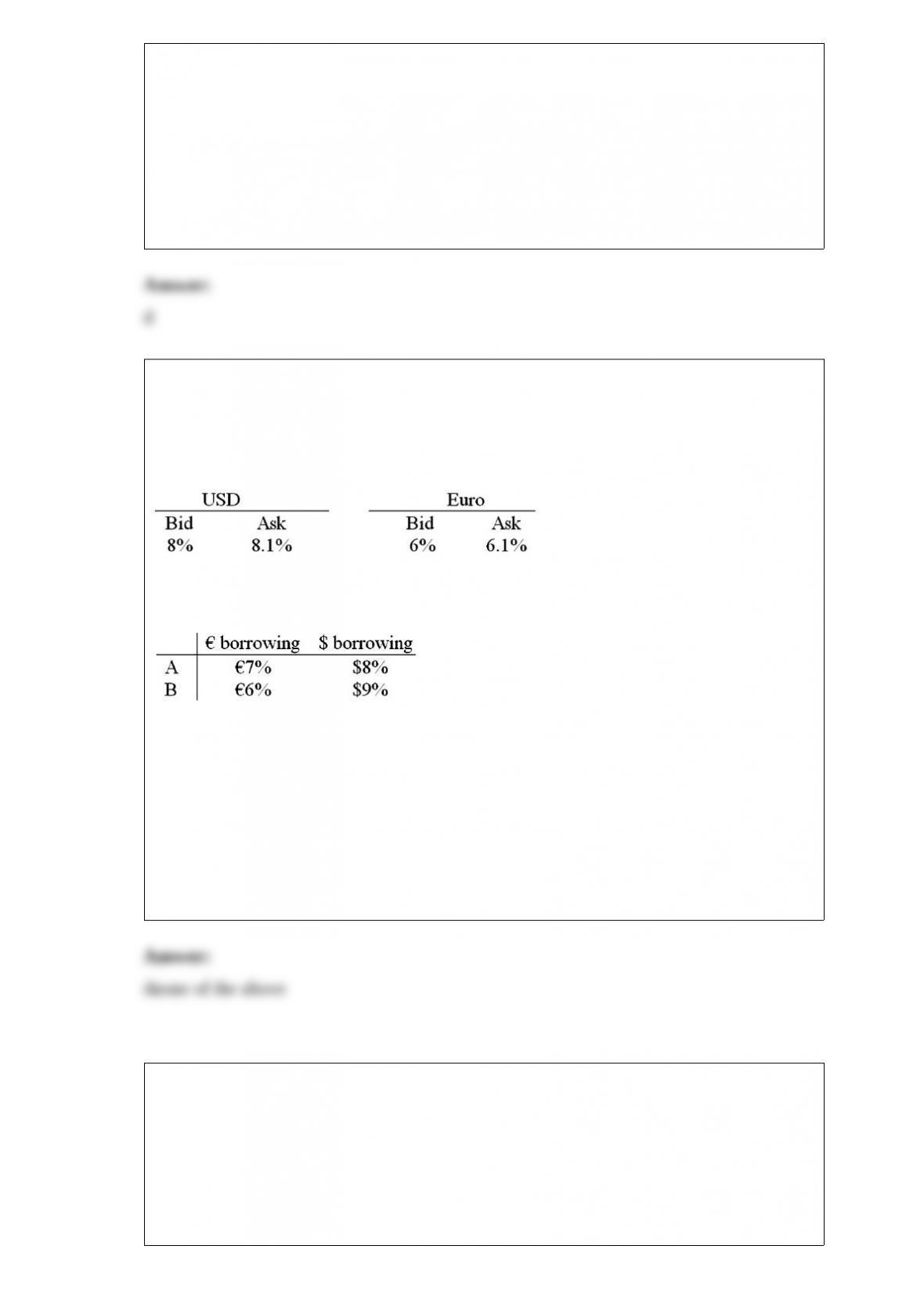

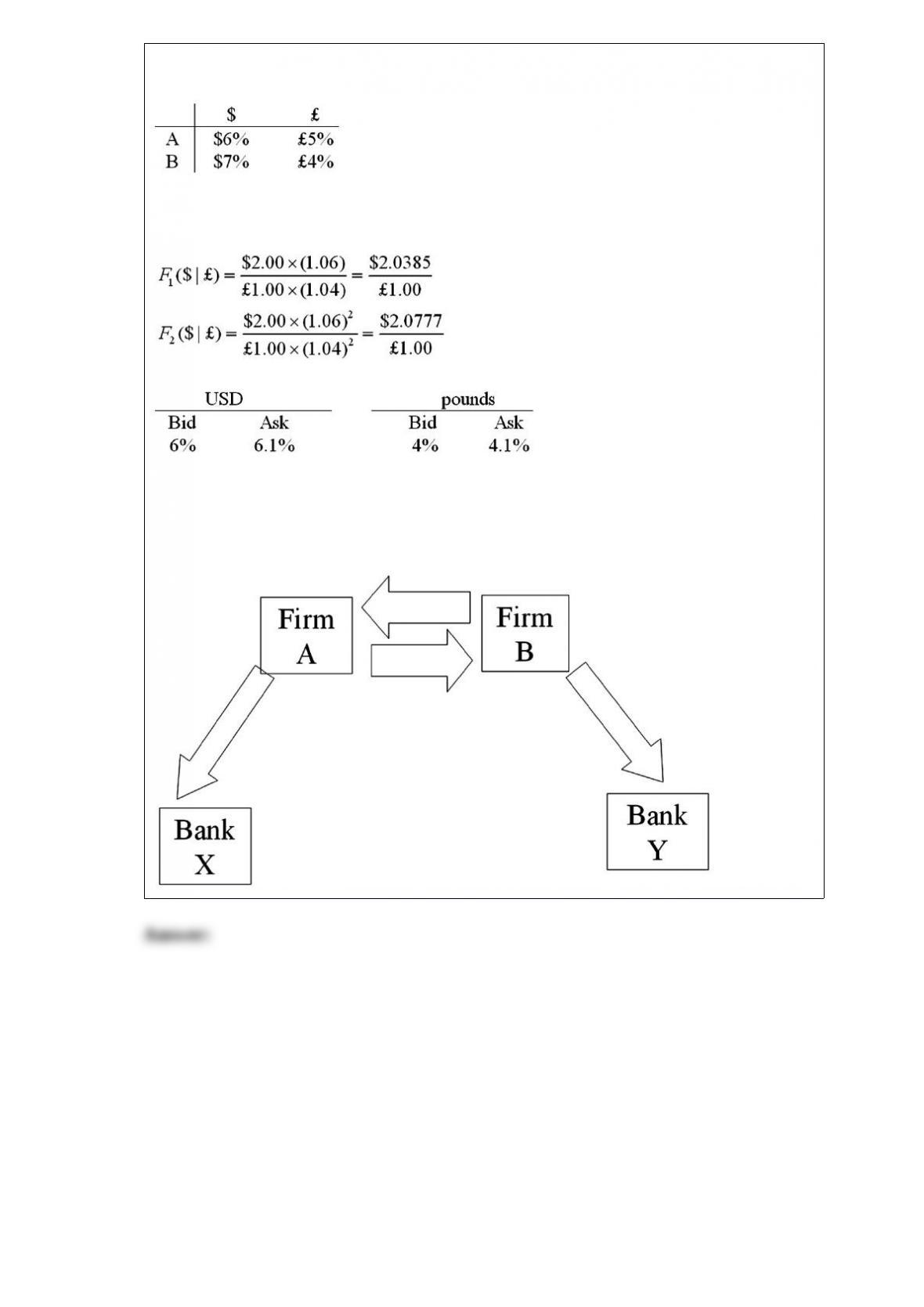

4) a is a u.s.-based mnc with aaa credit; b is an italian firm with aaa credit. firm a wants

to borrow 1,000,000 for one year and b wants to borrow $2,000,000 for one year. the

spot exchange rate is $2.00 = 1.00, a swap bank makes the following quotes for 1-year

swaps and aaa-rated firms against usd libor:

the firms external borrowing opportunities are:

a.firm a does 2 swaps with the swap bank, $ at bid and at ask. firm b does 2 swaps with

the swap bank, $ at ask and at bid. firms a and b would each save 90bp and the swap

bank would earn 20bp

b.there is no mutually beneficial swap at these prices

c.firm a does 2 swaps with the swap bank, $ at ask and at bid. firm b does 2 swaps with

the swap bank, $ at bid and at ask. firms a and b would each save 90bp and the swap

bank would earn 20bp

5) suppose a u.s.-based mnc makes computers with parts from its subsidiary in a

low-tax east asian country. it can reduce its reported u.s. incomeand increase its

subsidiary’s profitsby

a.overpaying for the computer components

b.underpaying for the computer components

c.paying an arm’s length price

d.none of the above

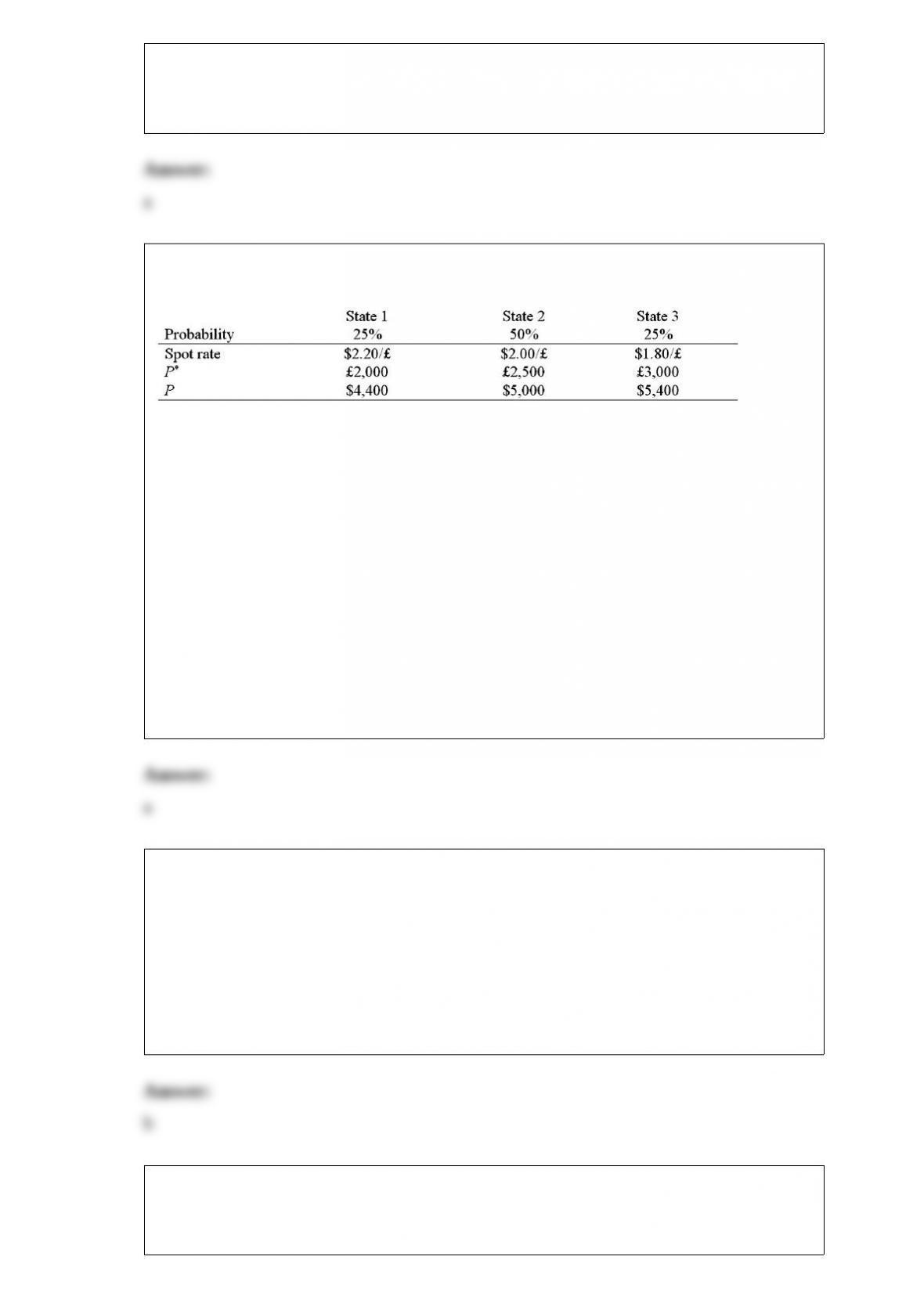

6) a u.s. firm holds an asset in great britain and faces the following scenario:

where,

p* = pound sterling price of the asset held by the u.s. firm

p = dollar price of the same asset

the variance of the exchange rate is:

a.0.0200

b.0.10

c.0.002

d.none of the above

7) the price elasticity of demand for unique products tends to be

a.highly elastic

b.highly inelastic

c.both a and b

d.none of the above

8) the sensitivity of “realized” domestic currency values of the firm’s contractual cash

flows denominated in foreign currency to unexpected changes in the exchange rate is

a.transaction exposure

b.translation exposure

c.economic exposure

d.none of the above

9) according to the research in the accuracy of paid exchange rate forecasters,

a.as a group, they do not do a better job of forecasting the exchange rate than the

forward rate does

b.the average forecaster is better than average at forecasting

c.the forecasters do a better job of predicting the future exchange rate than the market

does

d.none of the above

10) the underlying principle of the temporal method is

a.assets and liabilities should be translated based on their maturity

b.monetary accounts have a similarity because their value represents a sum of money

whose currency equivalent after translation changes each time the exchange rate

changes

c.monetary accounts are translated at the current exchange rate; other accounts are

translated at the current exchange rate if they are carried on the books at current value;

items carried at historical cost are translated at historic exchange rates

d.all balance sheet accounts are translated at the current exchange rate, except for

stockholders’ equity. a “plug” equity account named cumulative translation adjustment

(cta) is used to make the balance sheet balance, since translation gains or losses do not

go through the income statement according to this method

11) there is an intimate relationship between a country’s bca and how the country

finances its domestic investment and pays for government expenditures. given this,

which of the following is a true statement?

a.if (s – i) < 0, it implies that a country’s domestic savings is insufficient to finance

domestic investment

b.if (t – g) < 0, it implies that a country’s tax revenue is insufficient to finance

government spending

c.both a and b are true

d.none of the above

12) corporate governance can be defined as

a.the economic, legal, and institutional framework in which corporate control and cash

flow rights are distributed among shareholders, managers and other stakeholders of the

company

b.the general framework in which company management is selected and monitored

c.the rules and regulations adopted by boards of directors specifying how to manage

companies

d.the government-imposed rules and regulations affecting corporate management

13) a bank sold a 3 9 fra. payment is made when?

a.at the end of 3 months

b.at the end of 6 months

c.at the end of 9 months

d.none of the above

14) financial accounting standards board (fasb) statements 8 and 52 relate to the

translation methods. the following outlines the objectives and descriptions of the two

statements.

(i) – measure in dollars an enterprise’s assets, liabilities, revenues, or expenses that are

denominated in a foreign currency according to generally accepted accounting

principles

(ii) – is essentially the temporal method of translation (with some subtle differences)

(iii) – provide information that is generally compatible with the expected economic

effects of a rate change on an enterprise’s cash flows and equity

(iv) – reflect in consolidated statements the financial results and relationships of the

individual consolidated entities as measured in their functional currencies in conformity

with u.s. generally accepted accounting principles

the currency of the primary economic environment in which the entity operates is

defined in fasb 52 as

a.the “reporting currency”

b.the “functional currency”

c.the “current currency”

d.none of the above

15) some of the factors (with selected explanations) used in calculating the basic “net

present value” and the “incremental” cash flows of a capital project are:

(i) – expected after-tax terminal value, including recapture of working capital

(ii) – net income, which belongs to the equity holders of the firm

(iii) – initial investment at inception

(iv) – depreciation, and the fact that depreciation is a noncash expense (i.e. it is removed

from the calculation of net income, for tax purposes, but added back because it did not

actually flow out of the firm)

(v) – weighted-average cost of capital

(vi) – the firm’s after-tax payment of interest to debtholders

(vii) – economic life of the capital project in years

the “net present value” of a capital project is calculated by using:

a.(i), (ii), and (iii)

b.(ii), (iv), and (vi)

c.(i), (iii), (v), and (vii)

d.(iv), (v), (vi), and (vii)

16) in the u.s., corporate governance has included all of the following except:

a.strengthen the independence of boards of directors

b.enhancing the transparency and disclosure of financial statements

c.energizing the regulatory an monitoring functions of the sec

d.requiring auditors to sit on the boards of directors

17) your firm is a swiss importer of bicycles. you have placed an order with a british

firm for £1,000,000 worth of bicycles. payment (in pounds sterling) is due in 12

months. use a money market hedge to redenominate this one-year pound denominated

payable into a swiss franc-denominated payable with a one-year maturity.

the following were computed without rounding. select the answer closest to yours.

a.sfr. 2,000,000

b.sfr. 2,151,118.62

c.sfr. 2,068,383.28

d.sfr. 1,921,941.75

18) the idea that the tax burden a host country imposes on the foreign subsidiary of a

mnc should be the same regardless of the country in which the mnc is incorporated and

the same as that placed on domestic firms is earned is referred to as

a.capital-export neutrality

b.capital-import neutrality

c.national neutrality

d.none of the above

19) with regard to the oip,

a.the composition of the optimal international portfolio is identical for all investors,

regardless of home country

b.the oip has more return and less risk for all investors, regardless of home country

c.the composition of the optimal international portfolio is identical for all investors,

regardless of home country, if they hedge their risk with currency futures contracts

d.none of the above

20) foreign banks that establish subsidiary and affiliate banks in the u.s.

a.tend to locate in states that are major centers of financial activity

b.tend to locate in the highly populous states of new york, california, illinois, florida,

georgia, and texas

c.can underwrite securities, but not accept dollar-denominated deposits

d.both a and b

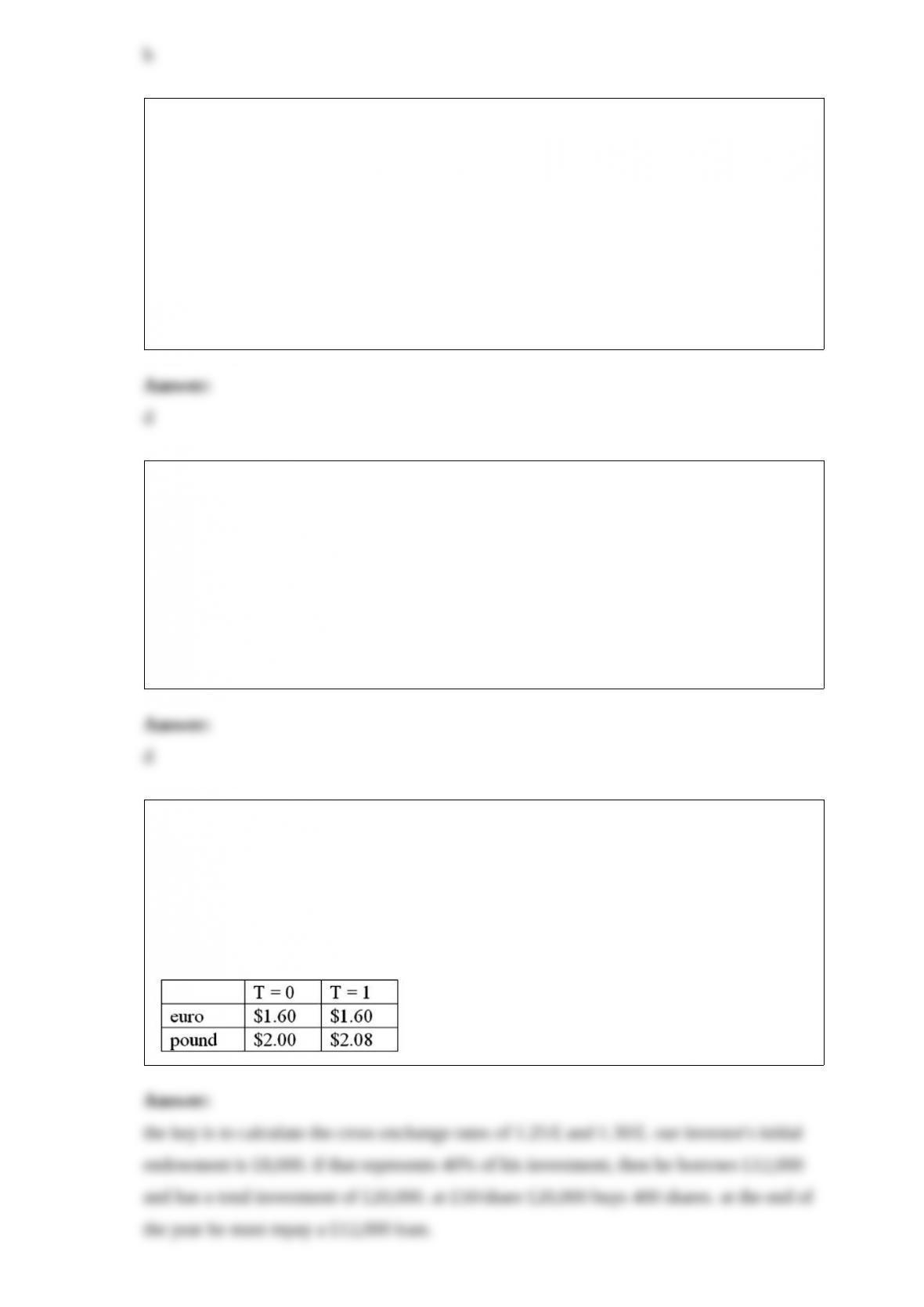

21) calculate the euro-based return an italian investor would have realized by investing

10,000 into a £50 british stock on margin with only 40% down and 60% borrowed.the

stock pays a £0.30 quarterly dividend, and after one year the investment sells for £54.

the interest on the margin loan is 1% per year. the margin loan is denominated in

pounds.

spot exchange rates at the start and end of the year are shown in the table.

22) calculate the euro-based return an italian investor would have realized by investing

10,000 into a £50 british stock on margin with only 40% down and 60% borrowed.the

stock pays a £0.30 quarterly dividend, and after one year the investment sells for £54

the exchange rate has changed from 1.25 per pound to 1.30 per pound. the interest on

the margin loan is 1% per year. the margin loan is denominated in pounds.

our investor’s initial endowment is £8,000. if that represents 40% of his investment,

then he borrows £12,000 and has a total investment of £20,000. at £50/share £20,000

buys 400 shares. at the end of the year he must repay a £12,000 loan.

23)

please note that your answers are worth zero points if they do not include currency

symbols ($, )

there is (at least) one profitable arbitrage at these prices. what is it?

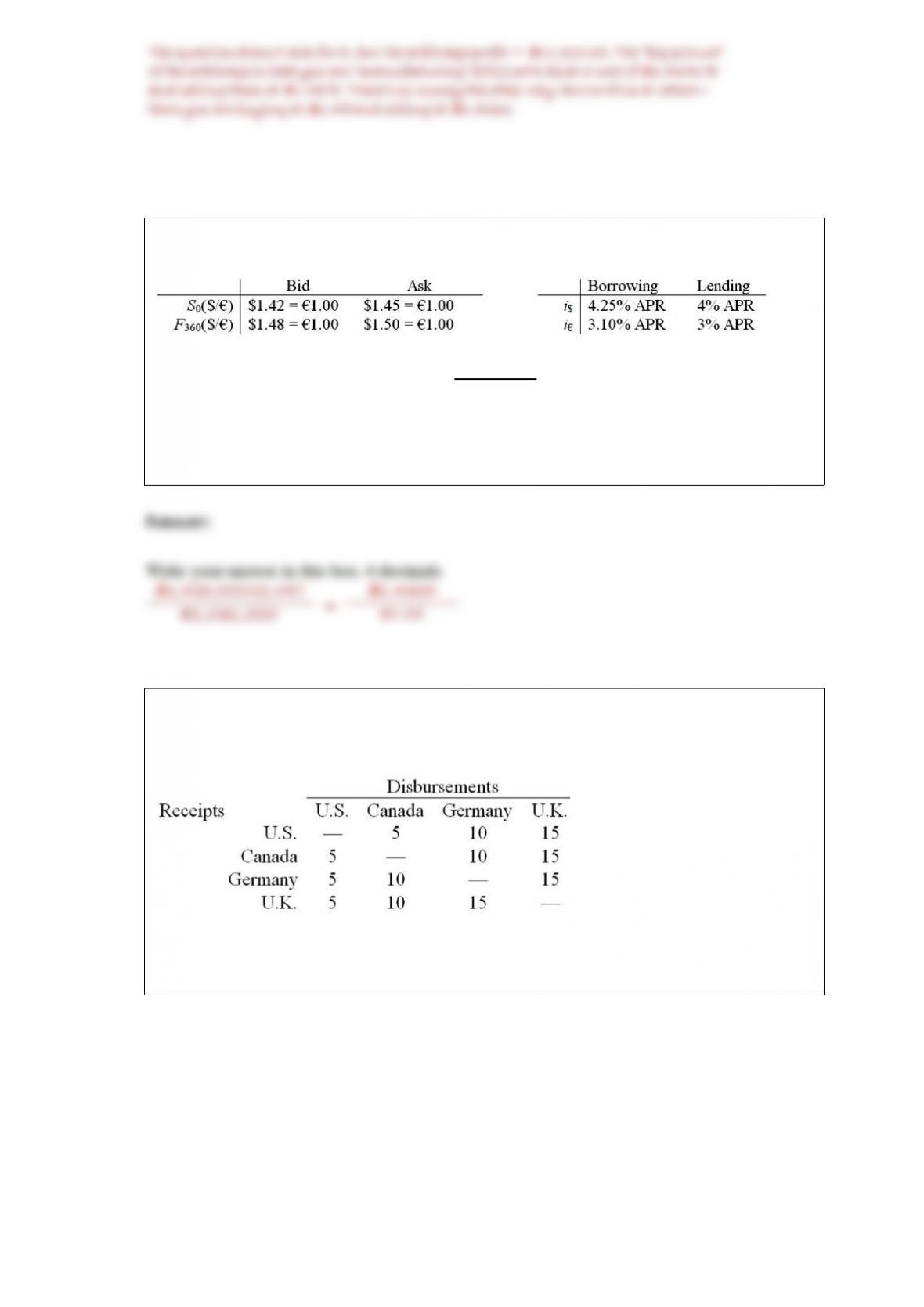

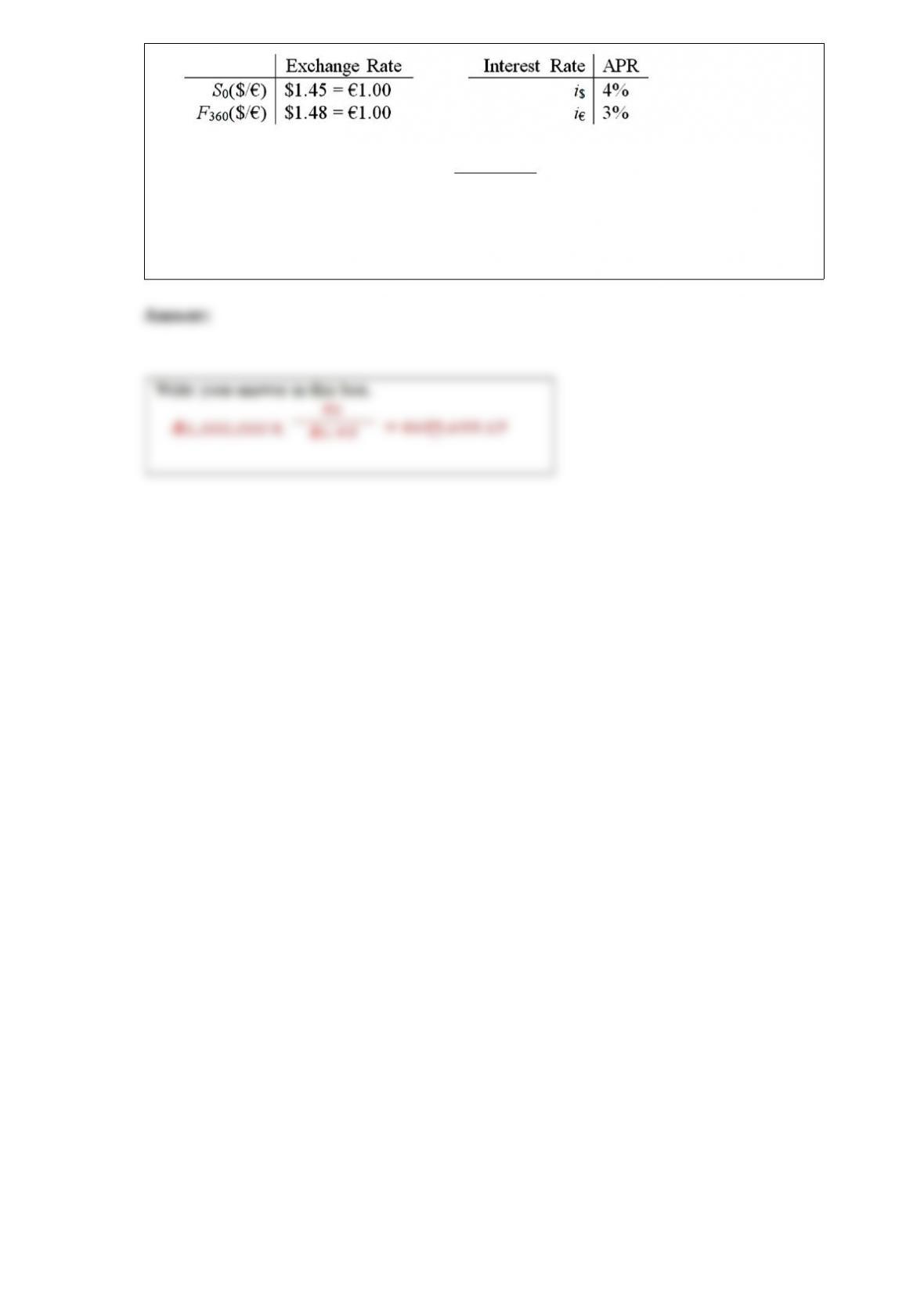

24) assume that you are a retail customer.

please note that your answers are worth zero points if they do not include currency

symbols ($, )

using your previous answers and a bit more work, find the 1-year forward ask exchange

rate in $ per that that satisfies irp from the perspective of a customer.

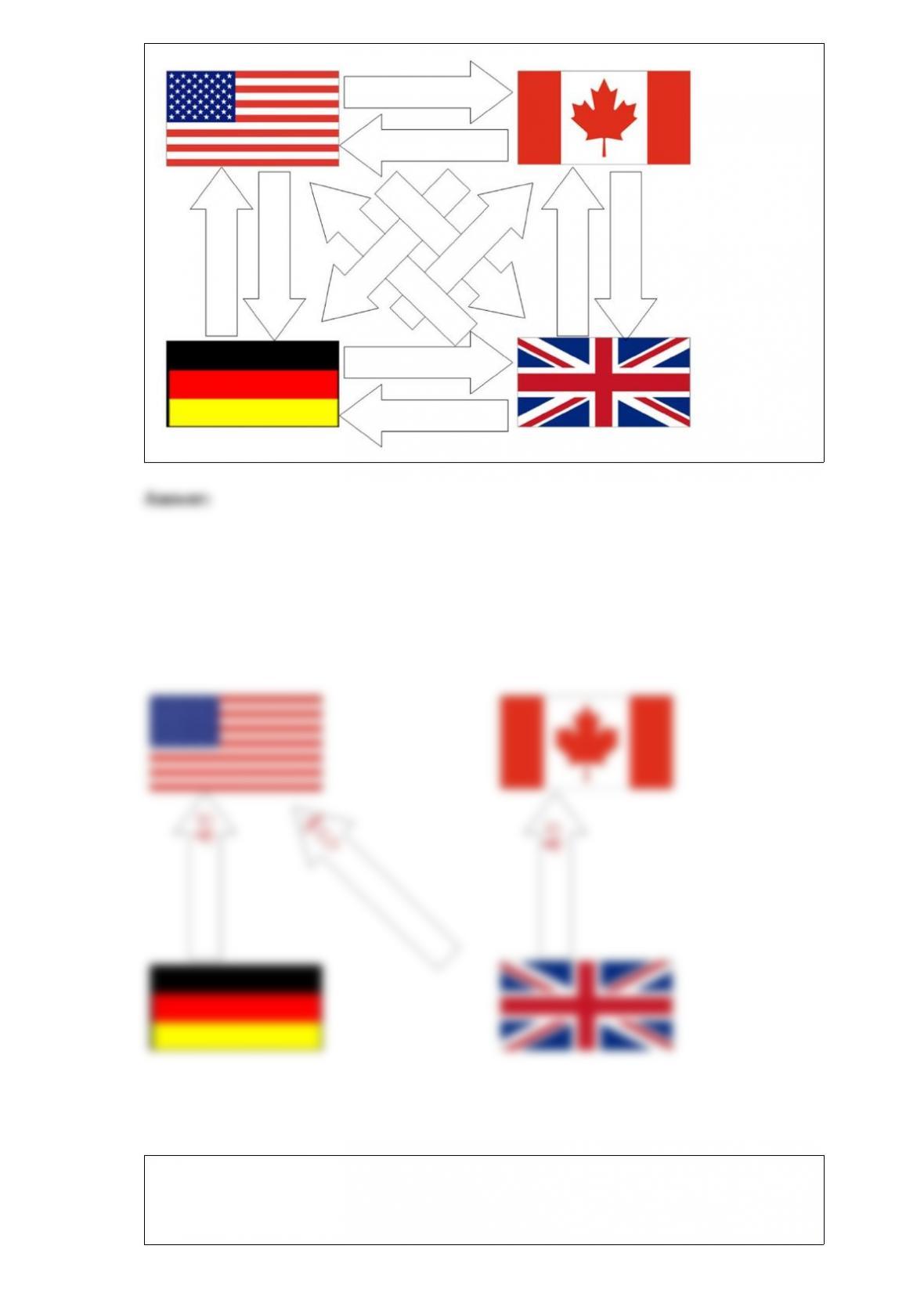

25) your firm’s interaffiliate cash receipts and disbursements matrix is shown below

($000):

using your results to the last question, use bilateral netting.

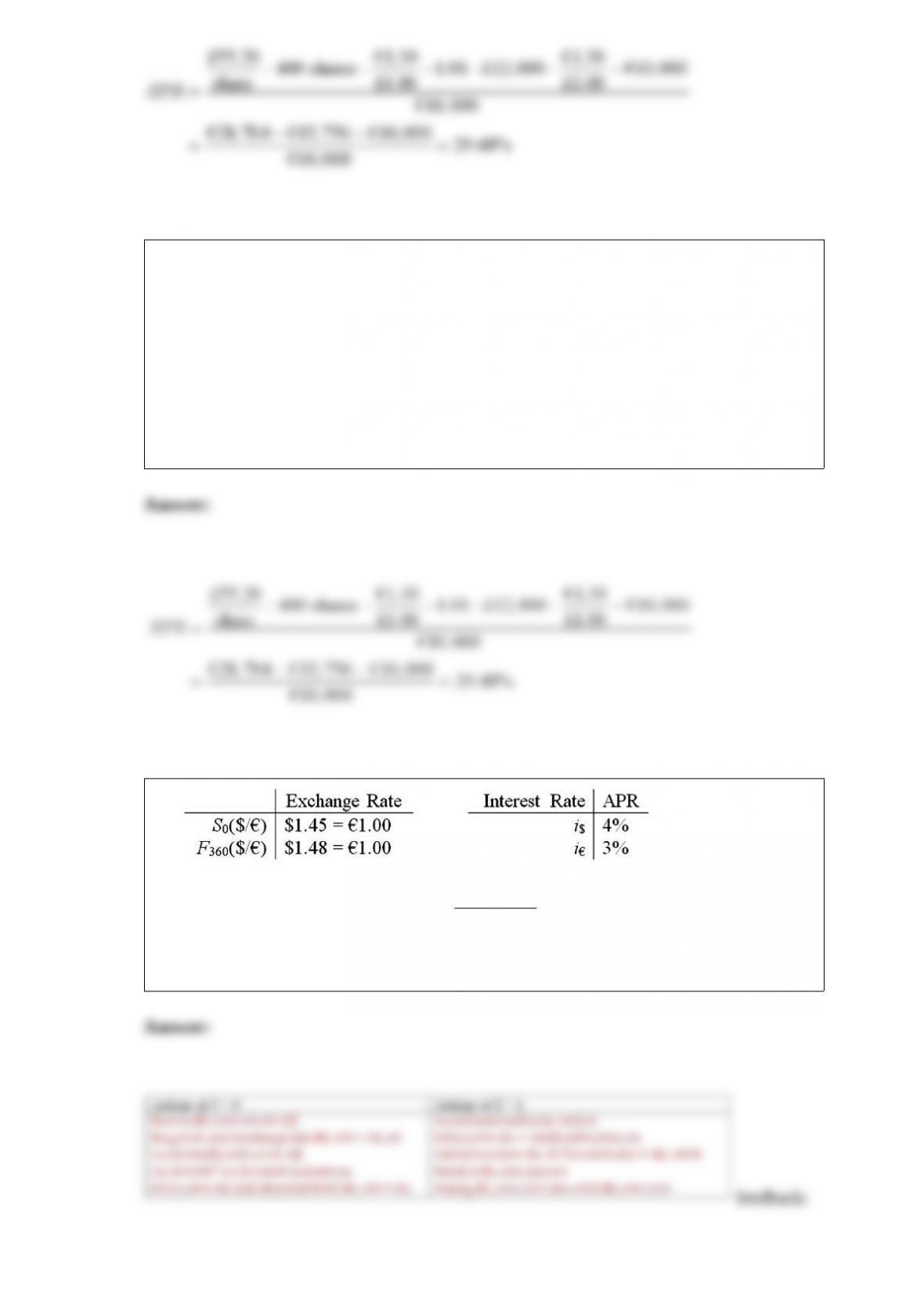

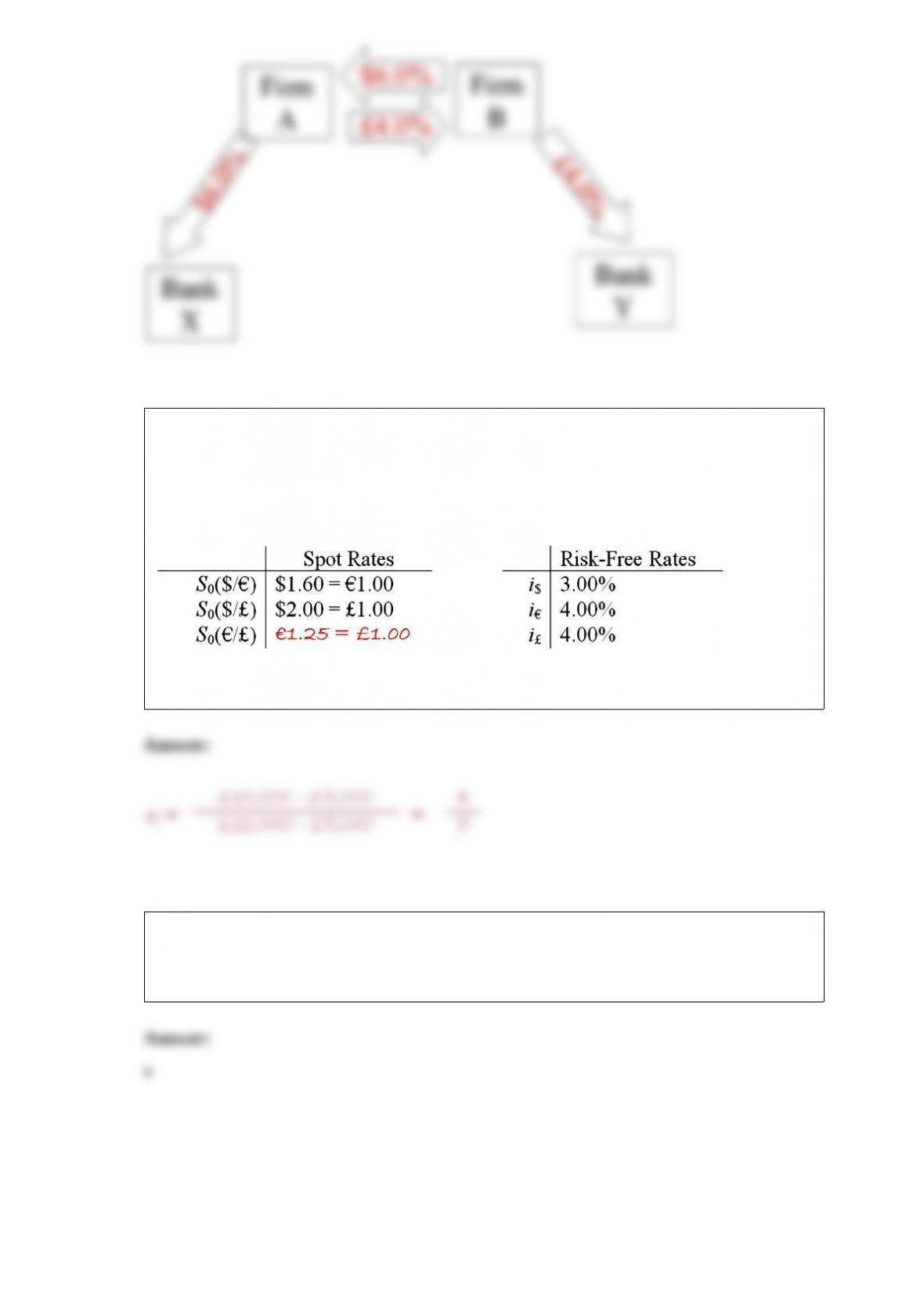

26) consider the situation of firm a and firm b. the current exchange rate is $2.00/£ firm

a is a u.s. mnc and wants to borrow £30 million for 2 years. firm b is a british mnc and

wants to borrow $60 million for 2 years. their borrowing opportunities are as shown,

both firms have aaa credit ratings.

the irp 1-year and 2-year forward exchange rates are

devise a direct swap for a and b that has no swap bank. show their external borrowing.

answer the problem in the template provided.

27) consider an option to buy 12,500 for £10,000. in the next period, the euro can

strengthen against the pound by 25% (i.e. each euro will buy 25% more pounds) or

weaken by 20%.

big hint: don’t round, keep exchange rates out to at least 4 decimal places.

find the risk neutral probability of an “up” move.

28) in the eu, there is a

a. low degree of fiscal integration among eu countries

b. high degree of fiscal integration among eu countries

29)

please note that your answers are worth zero points if they do not include currency

symbols ($, )

if you had borrowed $1,000,000 and traded for euro at the spot rate, how many do you

receive?