1) xyz corporation, located in the united states, has an accounts payable obligation of

¥750 million payable in one year to a bank in tokyo. which of the following is not part

of a money market hedge?

a.buy the ¥750 million at the forward exchange rate

b.find the present value of ¥750 million at the japanese interest rate

c.buy that much yen at the spot exchange rate

d.invest in risk-free japanese securities with the same maturity as the accounts payable

obligation

2) your u.s. firm has a £100,000 payable with a 3-month maturity. which of the

following will hedge your liability?

a.buy a call option on £100,000 with a strike price in euro

b.buy a put option on £100,000 with a strike price in dollars

c.buy a call option on £100,000 with a strike price in dollars

d.none of the above

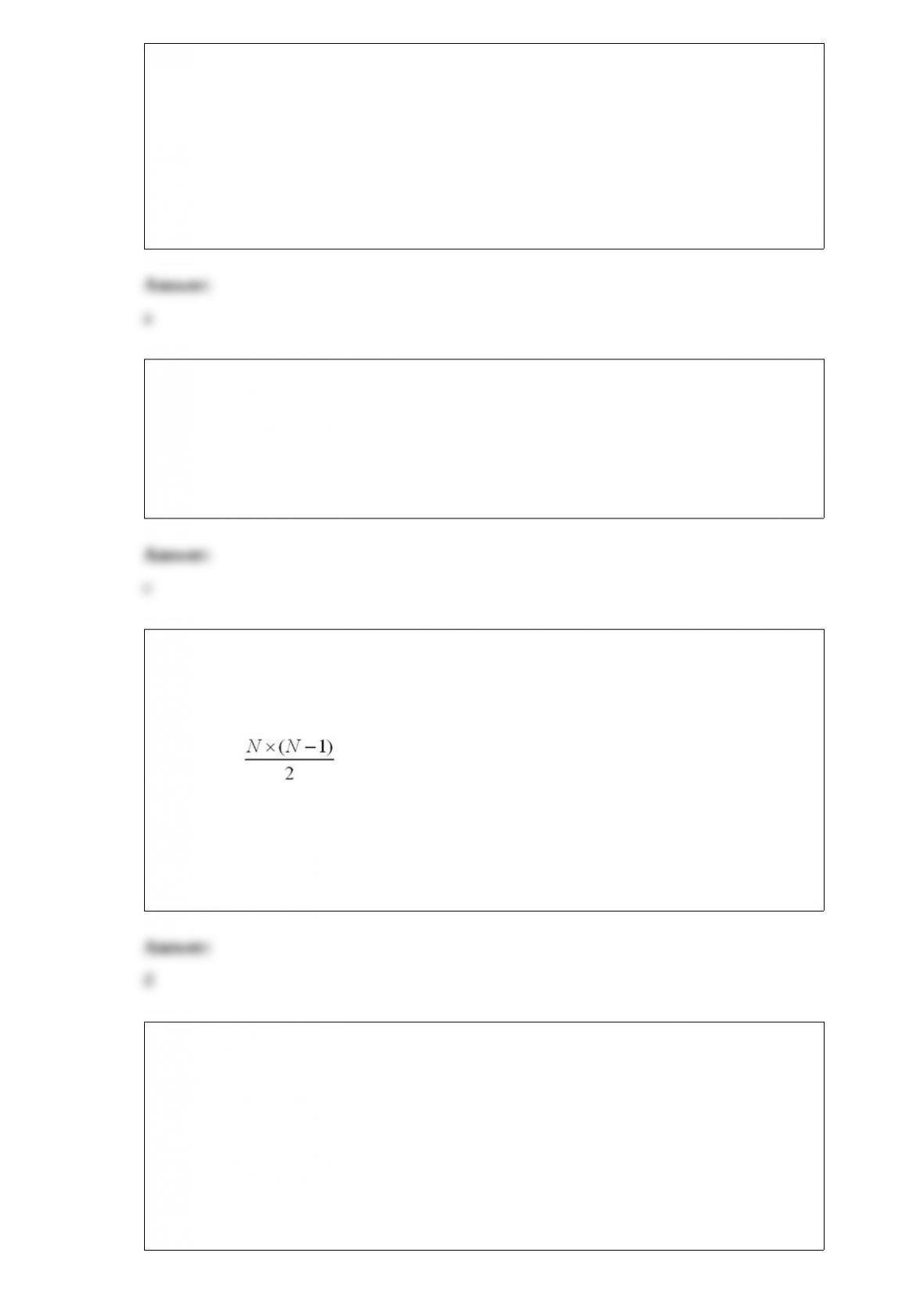

3) when engaged in bilateral netting

a.total interaffiliate receipts will always equal total interaffiliate disbursements

b.we can reduce the number of foreign exchange transactions among a mnc with n

affiliates to or less

c.each affiliate nets all its interaffiliate receipts against all its disbursements. it then

transfers or receives the balance, respectively, if it is a net payer or receiver

d.all of the above

4) libor

a.is the london interbank offered rate

b.is the reference rate in london for eurodollar deposits

c.one of several reference rates in london: there is a libor for eurodollars, euroyen,

eurocanadian dollars, and even euro

d.all of the above

5) a firm that is committed to keeping manufacturing facilities in only the home country

(and not developing multiple production sites in a variety of countries) can

a.not mitigate the effects of exchange rate changes

b.lessen the effect of exchange rate changes by sourcing from where input costs are low

c.focus on selling commodity products with product differentiation

d.pursue a strategy of increasing its products price elasticity of demand

6) the emergence of global financial markets is due in no small part to

a.advances in computer and telecommunications technology

b.enforcement of the soviet system of state ownership of resources of production

c.government regulation and protection of infant industries

d.none of the above

7) price discovery in the secondary stock markets

a.occurs due to the competitive trading between buyers and sellers, just like on ebay

b.is set once a day at the close

c.is set by the investment bankers at the ipo

d.all of the above

8) suppose mexico is a major export market for your u.s.-based company and the

mexican peso appreciates drastically against the u.s. dollar. this means

a.your company’s products can be priced out of the mexican market, as the peso price of

american imports will rise following the peso’s fall

b.your firm will be able to charge more in dollar terms while keeping peso prices stable

c.your domestic competitors will enjoy a period of facing lessened price competition

from mexican imports

d.both b and c are correct

9) the shorter length of time in bringing a eurodollar bond issue to market, coupled with

the lower rate of interest that borrowers pay for eurodollar bond financing in

comparison to yankee bond financing, are two major reasons why the eurobond

segment of the international bond market is roughly ________ the size of the foreign

bond segment.

a.four times

b.two times

c.ten times

d.one hundred times

10) the underlying principle of the current/noncurrent method is

a.assets and liabilities should be translated based on their maturity

b.monetary accounts have a similarity because their value represents a sum of money

whose currency equivalent after translation changes each time the exchange rate

changes

c.monetary accounts are translated at the current exchange rate; other accounts are

translated at the current exchange rate if they are carried on the books at current value;

items carried at historical cost are translated at historic exchange rates

d.all balance sheet accounts are translated at the current exchange rate, except for

stockholders’ equity. a “plug” equity account named cumulative translation adjustment

(cta) is used to make the balance sheet balance, since translation gains or losses do not

go through the income statement according to this method

11) suppose your firm invests $100,000 in a project in italy. at the time the exchange

rate is $1.25 = 1.00. one year later the exchange rate is the same, but the italian

government has expropriated your firm’s assets paying only 80,000 in compensation.

this is an example of

a.exchange rate risk

b.political risk

c.market imperfections

d.none of the above, since $100,000 = 80,000 $1.25/1.00

12) your firm is a swiss importer of bicycles. you have placed an order with an italian

firm for 1,000,000 worth of bicycles. payment (in euro) is due in 12 months. use a

money market hedge to redenominate this one-year receivable into a swiss

franc-denominated receivable with a one-year maturity.

the following were computed without rounding. select the answer closest to yours.

a.sfr. 1,728,900.26

b.sfr. 1,600,000

c.sfr. 1,544,705.88

d.sfr. 800,000

13) a buy-back transaction

a.is also called a bilateral clearing agreement

b.involves a technology transfer via the sale of a manufacturing plant: as part of the

terms, the seller of the plant agrees to purchase a certain portion of the plant output

c.involves two parties agreeing to buy a specified amount of goods or services from one

another

d.all of the above

14) the most popular reserve currency is now the

a.u.s. dollar

b.euro

c.japanese yen

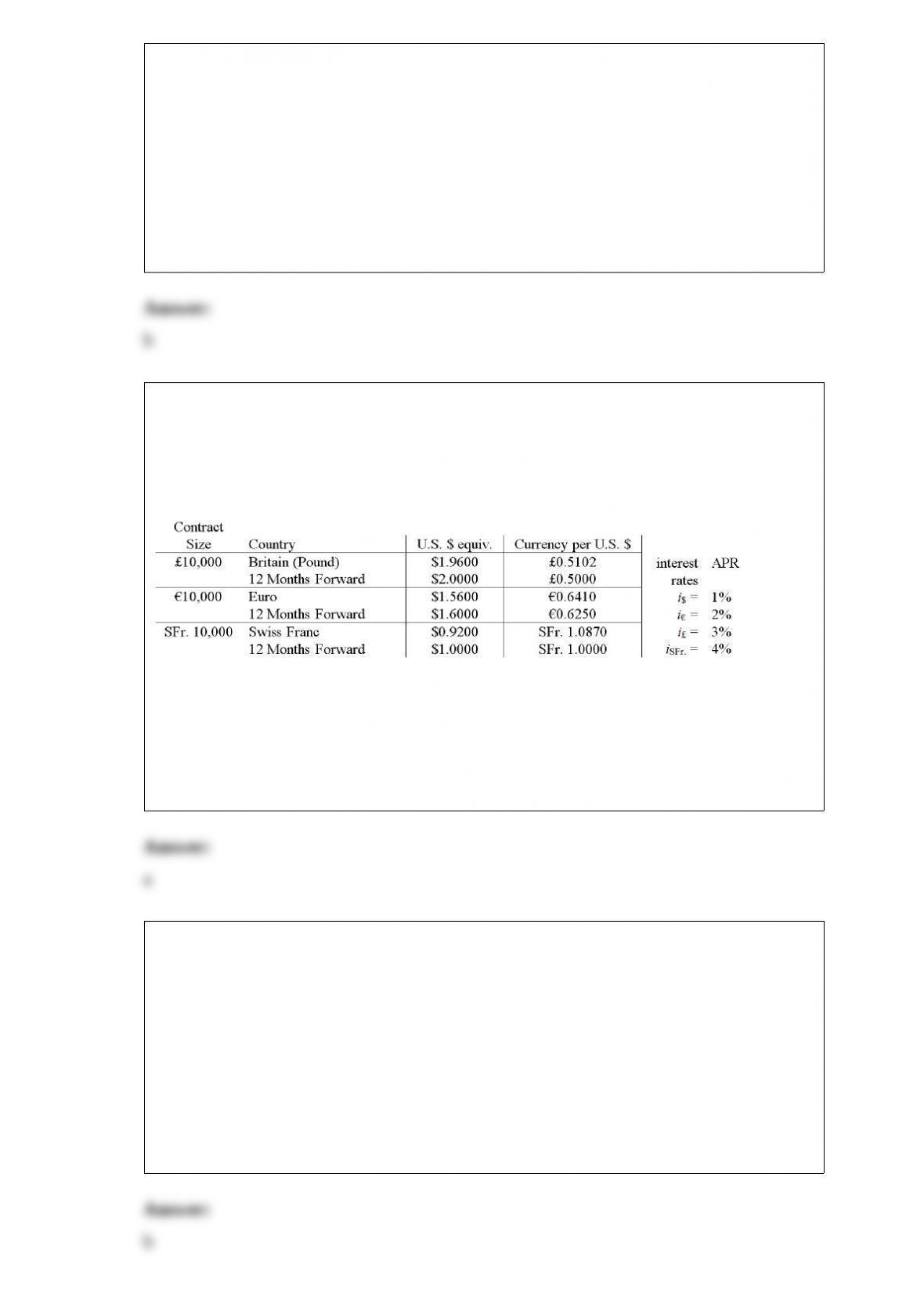

15) a currency dealer has good credit and can borrow either $1,000,000 or 800,000 for

one year. the one-year interest rate in the u.s. is i$ = 2% and in the euro zone the

one-year interest rate is i = 6%. the spot exchange rate is $1.25 = 1.00 and the one-year

forward exchange rate is $1.20 = 1.00. show how to realize a certain profit via covered

interest arbitrage.

a.borrow $1,000,000 at 2%. trade $1,000,000 for 800,000; invest at i = 6%; translate

proceeds back at forward rate of $1.20 = 1.00, gross proceeds = $1,017,600

b.borrow 800,000 at i = 6%; translate to dollars at the spot, invest in the u.s. at i$ = 2%

for one year; translate 848,000 back into euro at the forward rate of $1.20 = 1.00. net

profit $2,400

c.borrow 800,000 at i = 6%; translate to dollars at the spot, invest in the u.s. at i$ = 2%

for one year; translate 850,000 back into euro at the forward rate of $1.20 = 1.00. net

profit 2,000

d.both c and b

16) with regard to estimates of “world beta” measures of the sensitivity of a national

market to world market movements,

a.the japanese stock market is the most sensitive to world market movements

b.the u.s. stock market is the least sensitive to world market movements

c.both a and b

d.none of the above

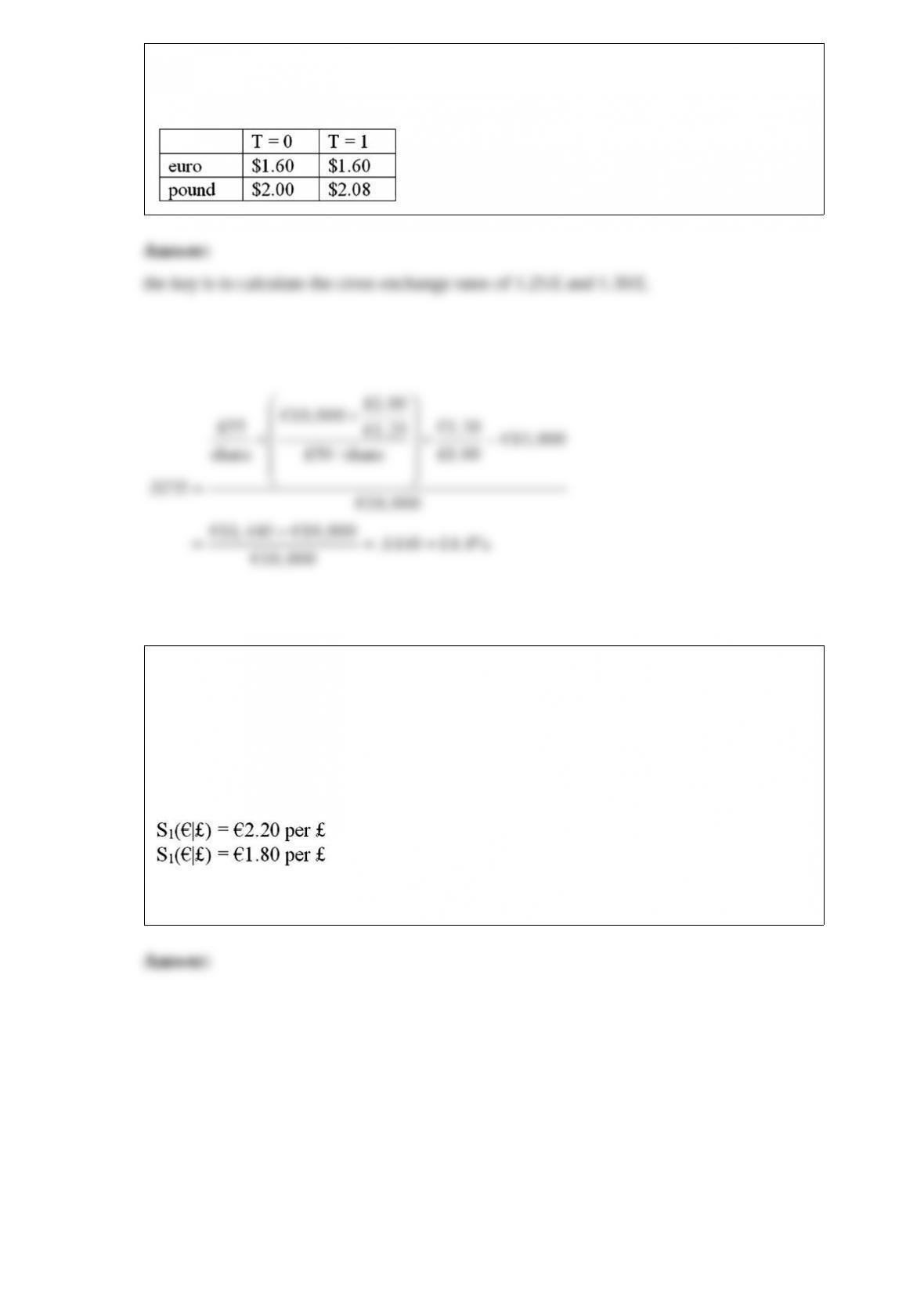

17) calculate the euro-based return an italian investor would have realized by investing

10,000 into a £50 british stock. one year after investment, the stock pays a £1 dividend,

and sells for £54. spot exchange rates at the start and end of the year are shown in the

table.

18) a french firm is considering a one-year investment in the united kingdom with a

pound-denominated rate of return of i£ = 15%. the firm’s local cost of capital is i = 10%

the project costs £1,000 and will return £1,150 at the end of one year.

the current exchange rate is 2.00 = £1.00

suppose that the bank of england is considering either tightening or loosening its

monetary policy. it is widely believed that in one year there are only two possibilities:

using the notion of a hedge ratio, make a recommendation vis–vis how to undertake the

project today without “buying” the option.

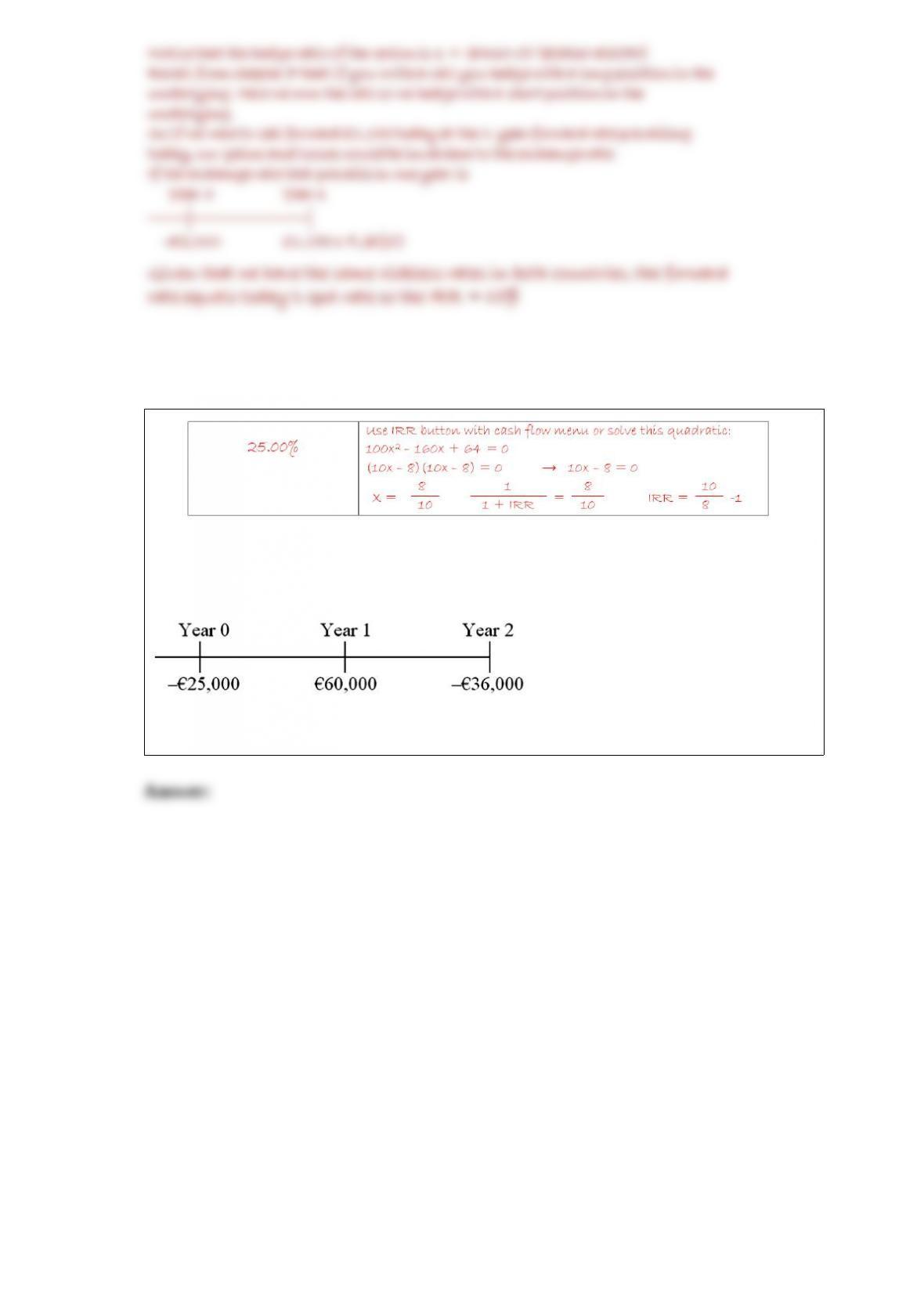

19)

consider the following international investment opportunity. it involves a gold mine that

can be opened at a cost, then produces a positive cash flow, but then requires

environmental clean-up:

find the euro-zone cost of capital to compute is the dollar-denominated npv of this

project.

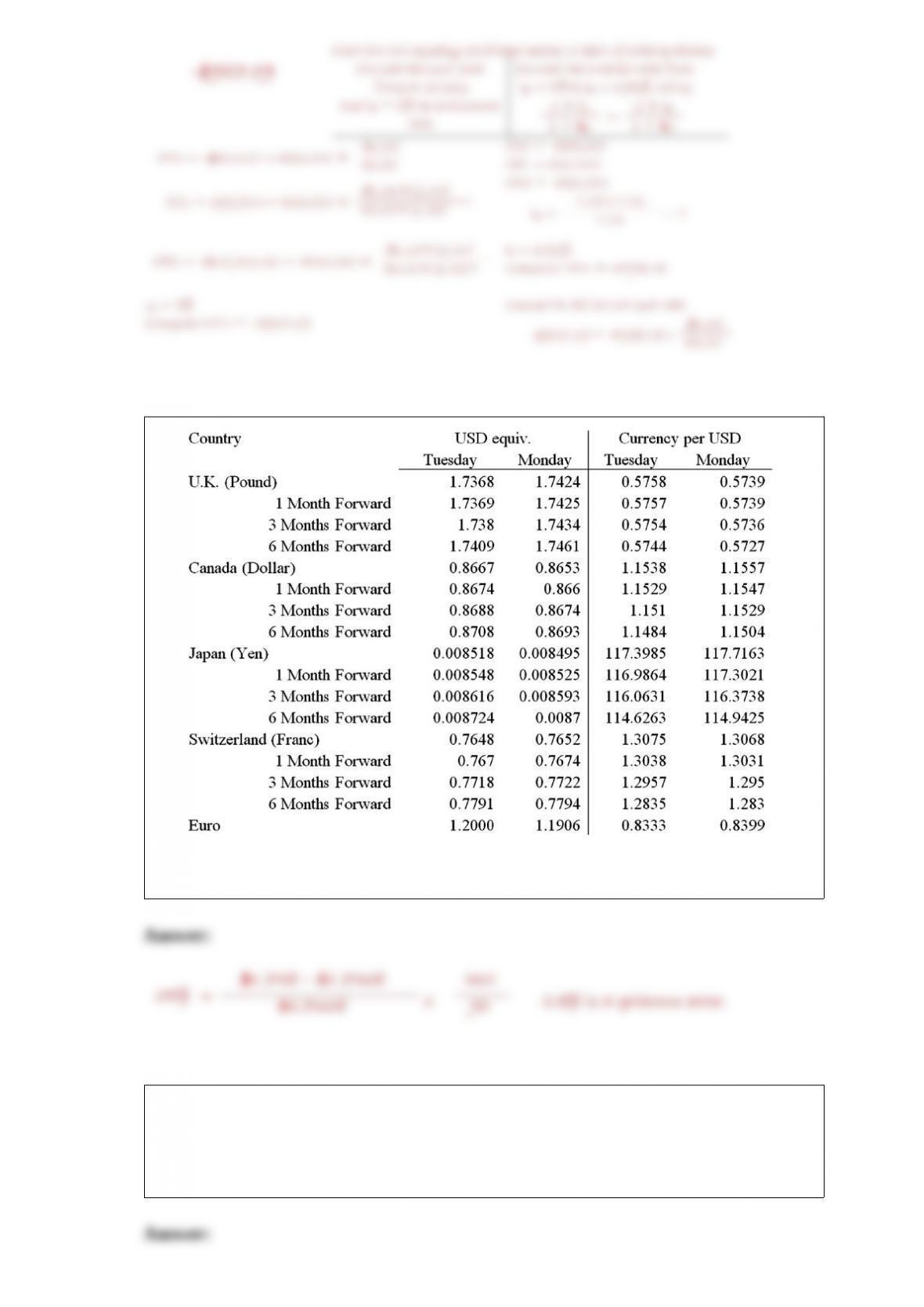

20)

using the table, what is 3-month forward premium or discount (expressed as an annual

percentage rate) for the british pound in terms of u.s. dollars?

21) calculate the euro-based return an italian investor would have realized by investing

10,000 into a £50 british stock. the stock pays a £0.30 quarterly dividend, and after one

year the investment sells for £54 the exchange rate has changed from 1.25 per pound to

1.30 per pound.

22) the time from acceptance to maturity on a $2,000,000 banker’s acceptance is 90

days.

the importing bank’s acceptance commission is 1.25 percent and that the market rate for

90-day b/as is 6 percent.

calculate the amount the banker will receive if the exporter discounts the b/a with the

importer’s bank.

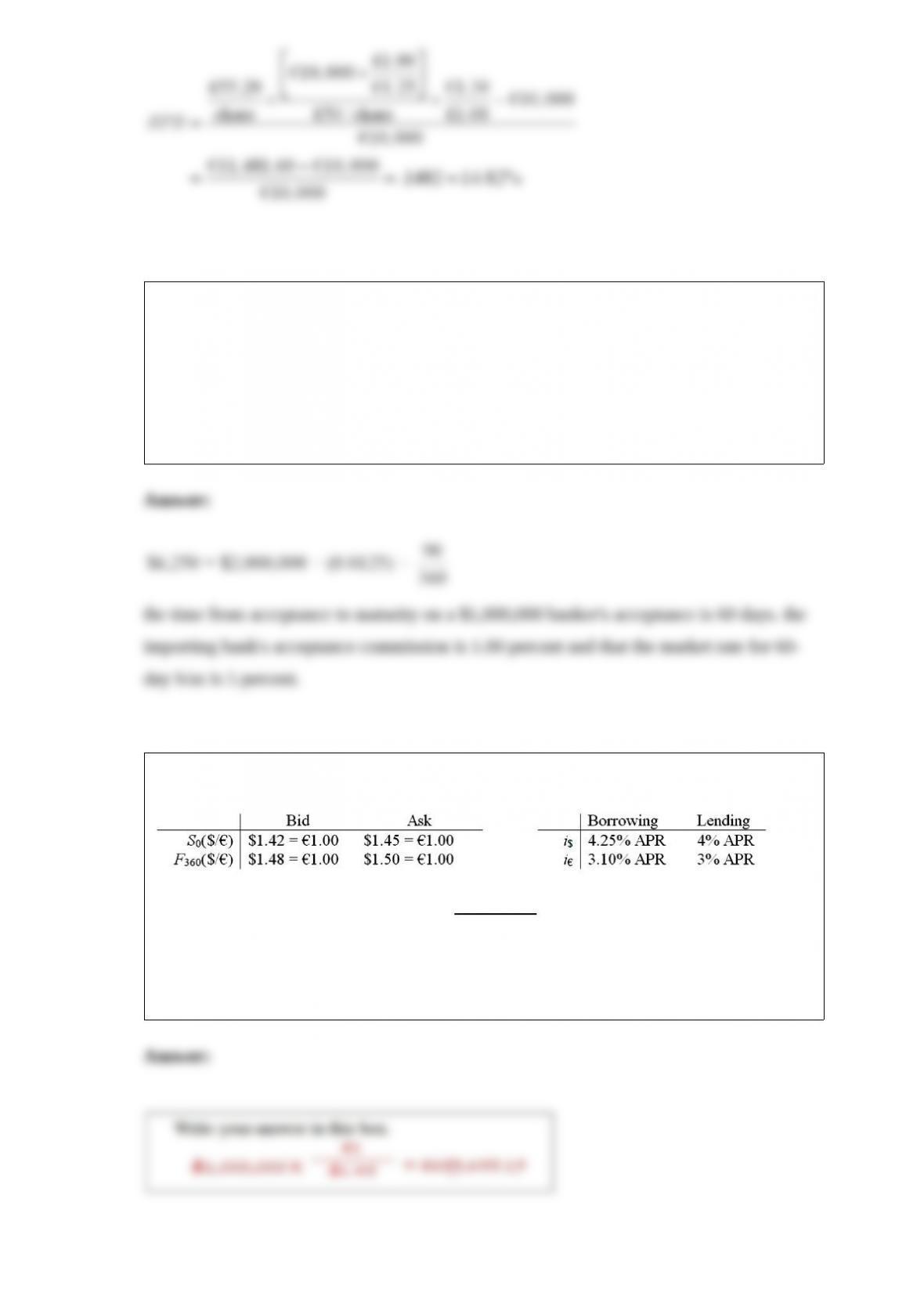

23) assume that you are a retail customer.

please note that your answers are worth zero points if they do not include currency

symbols ($, )

if you had borrowed $1,000,000 and traded for euro at the spot rate, how many do you

receive?

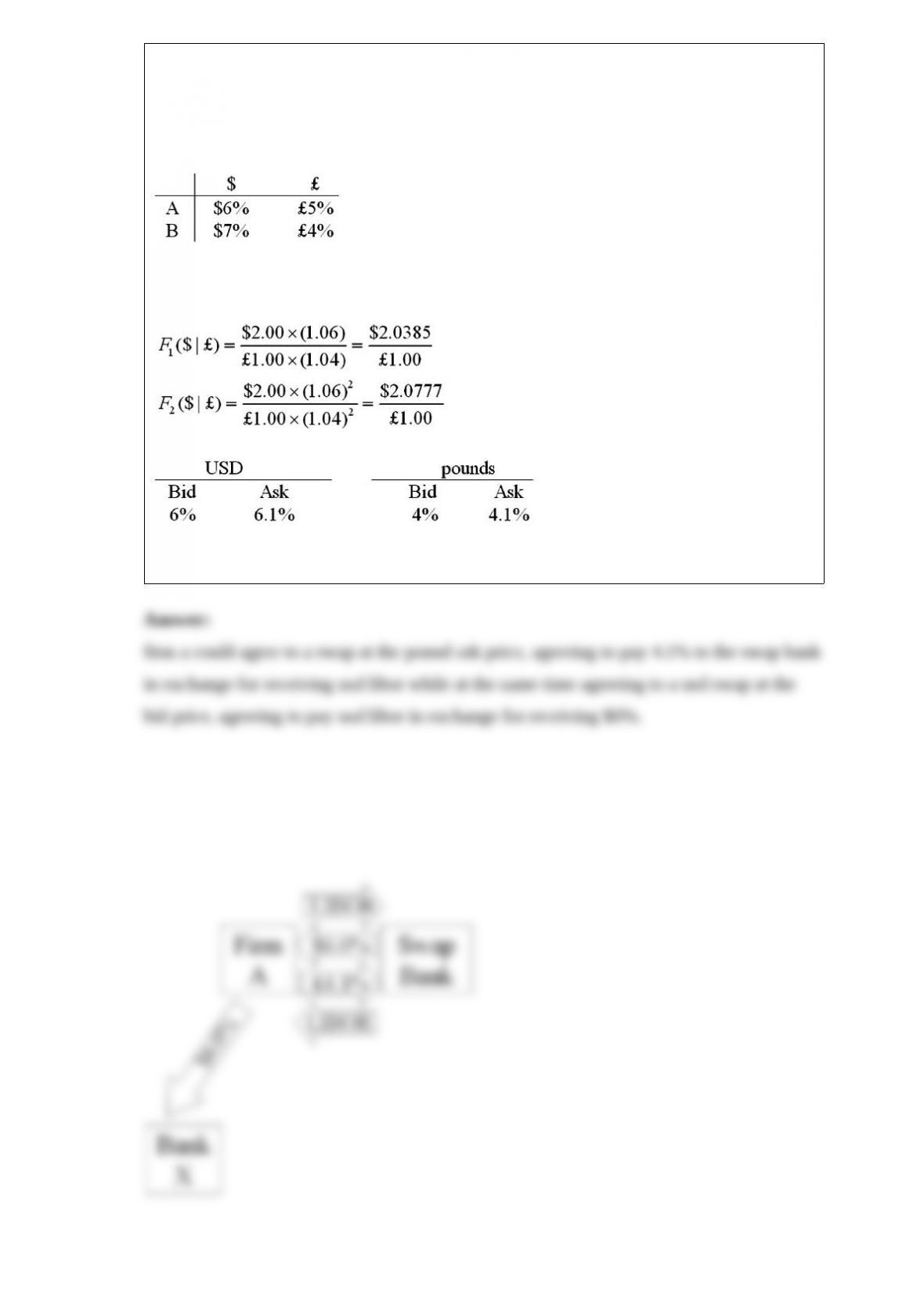

24) consider the situation of firm a and firm b. the current exchange rate is $2.00/£ firm

a is a u.s. mnc and wants to borrow £30 million for 2 years. firm b is a british mnc and

wants to borrow $60 million for 2 years. their borrowing opportunities are as shown,

both firms have aaa credit ratings.

the irp 1-year and 2-year forward exchange rates are

explain how firm a could use two of the swaps offered above to hedge its exchange rate

risk.