Finance companies have had no significant downturns in economic performance over

the last two decades.

Answer:

Insurance guarantee funds are administered by federal insurance regulators.

Answer:

The cost of insolvency of an FI to the FDIC is offset in part by the deposit insurance

premiums paid by the bank.

Answer:

In most countries, regulators often set minimum liquid reserve requirements on FIs.

Answer:

Most vulture funds are formed by the mutual fund industry as a way around SEC

restrictions from participating in the FI-originated loan sales market.

Answer:

Securities trading and underwriting is a profit generating activity that requires FIs to

hold an inventory of securities they trade.

Answer:

As of 2012, the total investment in long-term mutual funds is less than the total

investment in money market mutual funds.

Answer:

During the most recent financial crisis, life insurance companies with large proportions

of separate accounts business were well-protected from the decline in the debt and

equity markets.

Answer:

International loan contracts that contain cross-default provisions allow the country to

select specific lenders for special default treatment.

Answer:

Under Basel III, OBS contingent guaranty contracts are assigned the same risk weights

as on-balance-sheet principal items to determine their risk-adjusted asset values.

Answer:

An FI with a positive duration gap is exposed to interest rate declines and could hedge

its interest rate risk by buying forward contracts.

Answer:

Because the minimum amount of a negotiable wholesale CD is $100,000, holders of

these CDs are fully covered by FDIC insurance.

Answer:

The Investment Advisors Act of 1940 sets out rules to prevent conflicts of interest,

fraud, and excessive fees or charges for mutual fund shares.

Answer:

A disadvantage of the back simulation approach to estimate market risk exposure is the

limited confidence level based on the number of observations.

Answer:

Currently (2012) J.P. Morgan Chase is the largest bank holding company in the world

and operations in 60 countries.

Answer:

Because bank loans have a shorter maturity than most debt contracts, FIs typically

exercise less monitoring power and control over the borrower.

Answer:

Cross-market selling of financial products requires production of the products within

the same branch or bank office.

Answer:

Both buyers and sellers of LDC debt seem willing to participate in the LDC debt

markets for the purpose of rebalancing the country risk exposure on their balance

sheets.

Answer:

Because of changes in regulatory barriers, technology, and financial innovation, a single

financial service firm may now be able to offer a full set of financial services.

Answer:

Determining the pricing of a swap agreement requires the calculation of expected

one-year rates from the Treasury yield curve that is accomplished by calculating the

spot or zero-coupon discount yield curve.

Answer:

Because cash reserves at the Federal Reserve do not earn interest, DIs do not hold any

excess cash reserves beyond the minimum requirements.

Answer:

Personal credit institutions specialize in making equipment leases to consumers.

Answer:

The traditional interbank loan sale market has been growing rapidly due to an increase

in the number of mergers and acquisitions.

Answer:

Finance companies prefer to outwardly purchase equipment and then lease it to a

business rather than finance the purchase because they receive part of the lease payment

in the form of a down payment from the purchaser.

Answer:

Sovereign country risk exposure is a result of the FI’s inability to be fully diversified.

Answer:

To reduce liquidity risk an FI can efficiently manage the liability structure of its

portfolio.

Answer:

As of March 2012, U.S. banks were net short British pounds.

Answer:

Which of the following observations is TRUE of a no-load fund?A. Purchase is subject

to a sales charge.

B. Sales charges may be as high as 8.5 percent.

C. They market shares of the fund directly to investors.

D. They use sales agents.

E. They have up-front commission charges.

Answer:

Which of the following is TRUE of the market price of an options contract over time?

A. It is set at time 0.

B. It is fixed over the life of the contract.

C. It changes based on the market value of the underlying asset.

D. It increases with time to expiration.

E. It is based on supply and demand.

Answer:

The bank is considering changing its asset mix by moving $100 million of commercial

loans into Treasury securities. If it does change the asset mix and capital remains the

same, the risk-based capital ratio A. will not change because the total assets have not

changed.

B. will decrease because the earnings rate on Treasuries is less than on loans.

C. will increase by 16.67 percent.

D. will increase because the assets will have less risk.

E. will change, but the direction cannot be determined with the information given.

Answer:

An interest rate swapA. involves a swap buyer who agrees to make a number of

variable-rate payments on periodic settlement dates.

B. involves a swap seller who agrees to make a number of fixed-rate payments on

periodic settlement dates.

C. is effectively a succession of forward contracts on interest rates.

D. involves comparative advantage by the fixed-rate side of the swap, but not the

variable-rate side.

E. eliminates credit risk.

Answer:

City bank has six-year zero coupon bonds with a total face value of $20 million. The

current market yield on the bonds is 10 percent.

What is the modified duration of these bonds? A. 5.45 years.

B. 6.00 years.

C. 6.60 years.

D. 10.0 years.

E. 10.9 years.

Answer:

What is the amount of risk-adjusted assets? A. $1,000 million.

B. $720 million.

C. $900 million.

D. $600 million.

E. $700 million.

Answer:

If the relative change in interest rates is a decrease of 1 percent, calculate the impact on

the bank’s market value of equity using the duration approximation.

(That is, ΔR/(1 + R) = -1 percent)A. The bank’s market value of equity increases by

$325,550.

B. The bank’s market value of equity decreases by $325,550.

C. The bank’s market value of equity increases by $336,500.

D. The bank’s market value of equity decreases by $336,500.

E. There is no change in the bank’s market value of equity.

Answer:

Which of the following group of derivative securities had the smallest notational value

among the top 25 FIs as of June 2012? A. Futures and forwards.

B. Caps, floors, and collars.

C. Options.

D. Swaps.

E. Credit derivatives.

Answer:

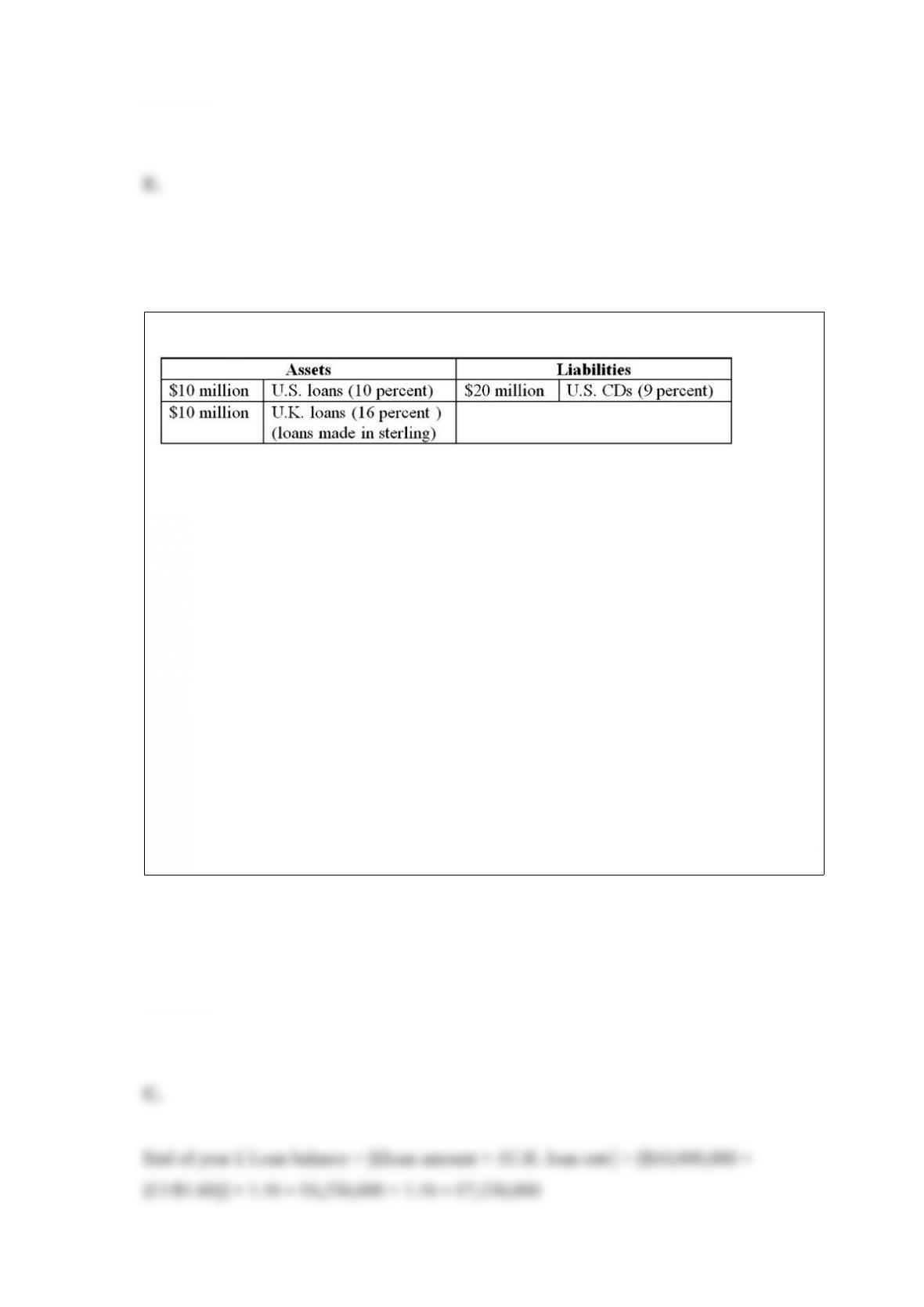

A U.S. FI is raising all of its $20 million liabilities in dollars (one-year CDs) but

investing 50 percent in U.S. dollar assets (one-year maturity loans) and 50 percent in

U.K. pound sterling assets (one-year maturity loans). Suppose the promised one-year

U.S. CD rate is 9 percent, to be paid in dollars at the end of the year, and that one-year,

credit risk-free loans in the United States are yielding only 10 percent. Credit risk-free

one-year loans are yielding 16 percent in the United Kingdom.

What amount, in sterling, will the FI have to repatriate back to the U.S. after one year if

the exchange rate remains constant at $1.60 to ≤1.A. ≤6.25 million.

B. ≤7.875 million.

C. ≤7.25 million.

D. ≤6.625 million.

E. ≤11.26 million.

Answer:

In economic terms, the letters of credit (LCs) and stand-by letters of credit SLCs sold

by an FIA. are contractual commitments to make a loan up to a stated amount at a

given interest rate in the future.

B. are insurance against the frequency or severity of some particular future occurrence.

C. are nonstandard contracts between two parties to deliver and pay for an asset in the

future.

D. are standardized contract guaranteed by organized exchanges to deliver and pay for

an asset in the future.

E. Answers C and D only.

Answer:

Loan assignments make up more than 90 percent of the U.S. domestic loan sale market

because A. they have lower capital requirements than other types of loan sales.

B. they are riskier than are other types of loan sales.

C. monitoring costs are reduced since all rights are transferred upon sale.

D. regulators prefer these transactions to loan participations.

E. there is no secondary market in loan participations.

Answer:

During the 1980s, which of the following was NOT a change in the financial

environment that had an inverse impact on U.S. banks and thrifts? A. The effects of

significant interest rate changes.

B. The failure of the FSLIC.

C. The deterioration of real estate prices.

D. The collapse of the energy industry.

E. Significant deterioration in the agricultural economy.

Answer:

By 2012, there were approximately ________ securities firms and investment banks

operating. A. 9,100

B. 7,600

C. 1,200

D. 480

E. 220

Answer:

A company that specializes in making loans to the customers of a particular retailer or

manufacturer would best be categorized as a A. sales finance institution.

B. personal credit institution.

C. business credit institution.

D. lease finance company.

E. factoring company.

Answer:

A bond is scheduled to mature in five years. Its coupon rate is 9 percent with interest

paid annually. This $1,000 par value bond carries a yield to maturity of 10 percent.

If yields increase by 10 basis points, what is the approximate price change on the

$100,000 Treasury note? Use the duration approximation relationship.A. +$179.39

B. +$16.05

C. -$1,605.05

D. -$16.05

E. +$160.51

Answer:

The cash flows that actually are paid on an interest rate swap depend on A. the market’s

expectations of future short-term interest rates.

B. upfront fee payments.

C. varying notional values underlying the swap.

D. special interest rate terms and indexes.

E. actual market rates that materialize over the life of the swap contract.

Answer:

Loan sales by foreign banks A. are forbidden in the U.S. domestic market.

B. must be of a certain size to be purchased by a domestic FI.

C. are allowed to be purchased by domestic FIs if the loan is to a highly-rated

company.

D. must be of a certain duration, and be sold without recourse in order to be purchased

by a domestic FI.

E. have no restrictions placed on them.

Answer:

Under Basel III, Globally Systematically Important Banks (G-SIBs) were identified by

the Bank for International Settlements (BIS) by all of the following indicators except:

A. Size.

B. Lack of substitutes for the institution’s services.

C. Cross-jurisdictional activity.

D. Interconnectedness with other institutions.

E. Ability to obtain insurance or other guarantees on deposits.

Answer:

Loan commitments are classified as A. on-balance-sheet assets.

B. off-balance-sheet assets.

C. off-balance-sheet liabilities.

D. on-balance-sheet liabilities.

E. equity capital.

Answer:

Commercial banks have expanded their activities in each of the following ways

EXCEPT A. opening nonbank banks.

B. grandfathering previously permitted activities.

C. expanding off shore.

D. petitioning regulators for enhanced powers.

E. acquiring nonfinancial firms.

Answer:

Which of the following refers to the term “maturity intermediation”? A. Creation of a

secondary market mature enough to withstand volatility.

B. Overcoming constraints to buying assets imposed by large minimum denomination

size.

C. Mismatching the maturities of assets and liabilities.

D. Reducing information costs or imperfections between households and corporations.

E. The transfer of wealth from one generation to the next.

Answer:

Consider a one-year maturity, $100,000 face value bond that pays a 6 percent fixed

coupon annually.

What is the price of the bond if market interest rates are 7 percent?A. $99,050.15.

B. $99,457.94.

C. $99,249.62.

D. $100,000.00.

E. $99,065.42.

Answer:

A mortgage loan officer is found to have provided false documentation that resulted in a

lower interest rate on a loan approved for one of her friends. The loan was subsequently

added to a loan pool, securitized and sold. Which of the following risks applies to the

false documentation by the employee? A. Market risk.

B. Credit risk.

C. Operational risk.

D. Technological risk.

E. Sovereign risk.

Answer:

What is a difference between a forward contract and a future contract? A. The

settlement price of a forward contract is fixed over the life of the contract but in a

futures contract is marked to market daily.

B. Forward contracts are normally arranged through an organized exchange, while

most futures contracts are OTC contracts.

C. Both are essentially the same, except for trading volumes which are higher for

futures contracts.

D. Both are essentially the same, except for the fact that the terms of a forward contract

is set by the exchange, subject to the approval of the Commodity Futures Trading

Commission (CFTC).

E. Delivery of the underlying asset almost always occurs on a futures contract but

almost never occurs on a forward contract.

Answer:

What is the average daily reserve required to be held by the bank for their demand

deposits during the maintenance period? Suppose that the rules require no reserves for

the first $11.5 million, 3 percent for amounts between $11.5 million and $71.0 million,

and 10 percent thereafter. A. $24.285 million.

B. $28.862 million.

C. $29.555 million.

D. $31.561 million.

E. $32.069 million.

Answer:

If the insured depositor transfer resolution method is utilized, what is the cost to the

FDIC of bank failure resolution?A. $0.

B. -$200 million.

C. $67 million.

D. $133 million.

E. $200 million.

Answer:

Overseas bank is pooling 50 similar and fully amortized mortgages into a pass-through

security. The face value of each mortgage is $100,000 paying 180 monthly interest and

principal payments at a fixed rate of 9 percent per annum.

What is the monthly payment on the mortgage pass-through? A. $37,500.

B. $45,231.

C. $45,309.

D. $50,713.

E. $55,256.

Answer:

Which of the following is a drawback of charging flat deposit insurance premiums?A.

The FDIC acts more like a private property-casualty insurer when charging flat

premiums.

B. It discourages banks from taking risks.

C. Both high risk and low risk banks are charged the same premium rate.

D. High risk banks will be charged an unreasonably high premium rate.

E. Premiums reflect the expected private costs or losses to the insurer from the

provision of deposit insurance.

Answer:

Bank of the Atlantic has liabilities of $4 million with an average maturity of two years

paying interest rates of 4.0 percent annually. It has assets of $5 million with an average

maturity of 5 years earning interest rates of 6.0 percent annually.

To what risk is the bank exposed? A. Reinvestment risk.

B. Refinancing risk.

C. Interest rate risk.

D. Answers A and C only.

E. Answers B and C only.

Answer:

A U.S. bank has €40 million in assets and €50 million in CDs. All other assets and

liabilities are in U.S. dollars. This bank is A. net long €10 million.

B. net short €10 million.

C. neither short nor long in €.

D. net long -€10 million.

E. net short -€10 million.

Answer:

HLT loans typically have all of the following characteristics except which of the

following? A. They have a short maturity of less than three months.

B. They are secured by assets of the borrowing firm.

C. They have floating rates tied to LIBOR or some other short-term index.

D. They have strong covenant protection.

E. They are term loans.

Answer:

Over the past 500 days, the 25th worst day for adverse exchange rate changes saw a

change in the exchange rates of 0.78 percent for the Yen and 0.30 percent for the Swiss

Franc. What is the expected VAR exposure on December 31?A. -$96,332.

B. -$2,157,088.

C. -$26,375,899.

D. -$109,233.

E. -$314,848.

Answer:

How would regulators characterize this FI based on the Standardized Approach

leverage ratio zones of Basel III? A. Well capitalized.

B. Undercapitalized.

C. Severely undercapitalized.

D. Overcapitalized.

E. Insolvent.

Answer:

For small change in interest rates, market prices of bonds move in an inversely

proportional manner according to the size of theA. equity.

B. asset value.

C. liability value.

D. duration value.

E. Answers A and B only.

Answer:

Which of the following is used as collateral when an insurance company issues policy

loans? A. Expected premium payments.

B. Existing policies.

C. Unearned premiums.

D. Guarantee funds.

E. U.S. Treasury Bills.

Answer:

Which of the following is a source of loan volume data?A. Commercial bank call

reports.

B. Data on shared national credits.

C. Commercial databases.

D. All of the above.

E. Only the Federal Reserve has this data.

Answer:

Consider a six-year maturity, $100,000 face value bond that pays a 5 percent fixed

coupon annually.

What is the price of the bond if market interest rates are 6 percent?A. $95,082.68.

B. $95,769.55.

C. $95,023.00.

D. $100,000.00.

E. $96,557.87.

Answer: