1) the price-to-sales ratio is probably most useful for firms in which phase of the

industry life cycle?

a.start-up phase

b.consolidation

c.maturity

d.relative decline

2) the strong form of the emh states that ________ must be reflected in the current

stock price.

a.all security price and volume data

b.all publicly available information

c.all information, including inside information

d.all costless information

3) suppose a u.s. investor wants to invest in a british firm currently selling for 50 per

share. the investor has $7,000 to invest, and the current exchange rate is $1.40/.

after 1 year, the exchange rate is $1.60/ and the share price is 55. what is the

dollar-denominated return?

a.25.7%

b.16%

c.14.3%

d.9.3%

4) the tendency of poorly performing stocks and well-performing stocks in one period

to continue their performance into the next period is called the ________________.

a.fad effect

b.martingale effect

c.momentum effect

d.reversal effect

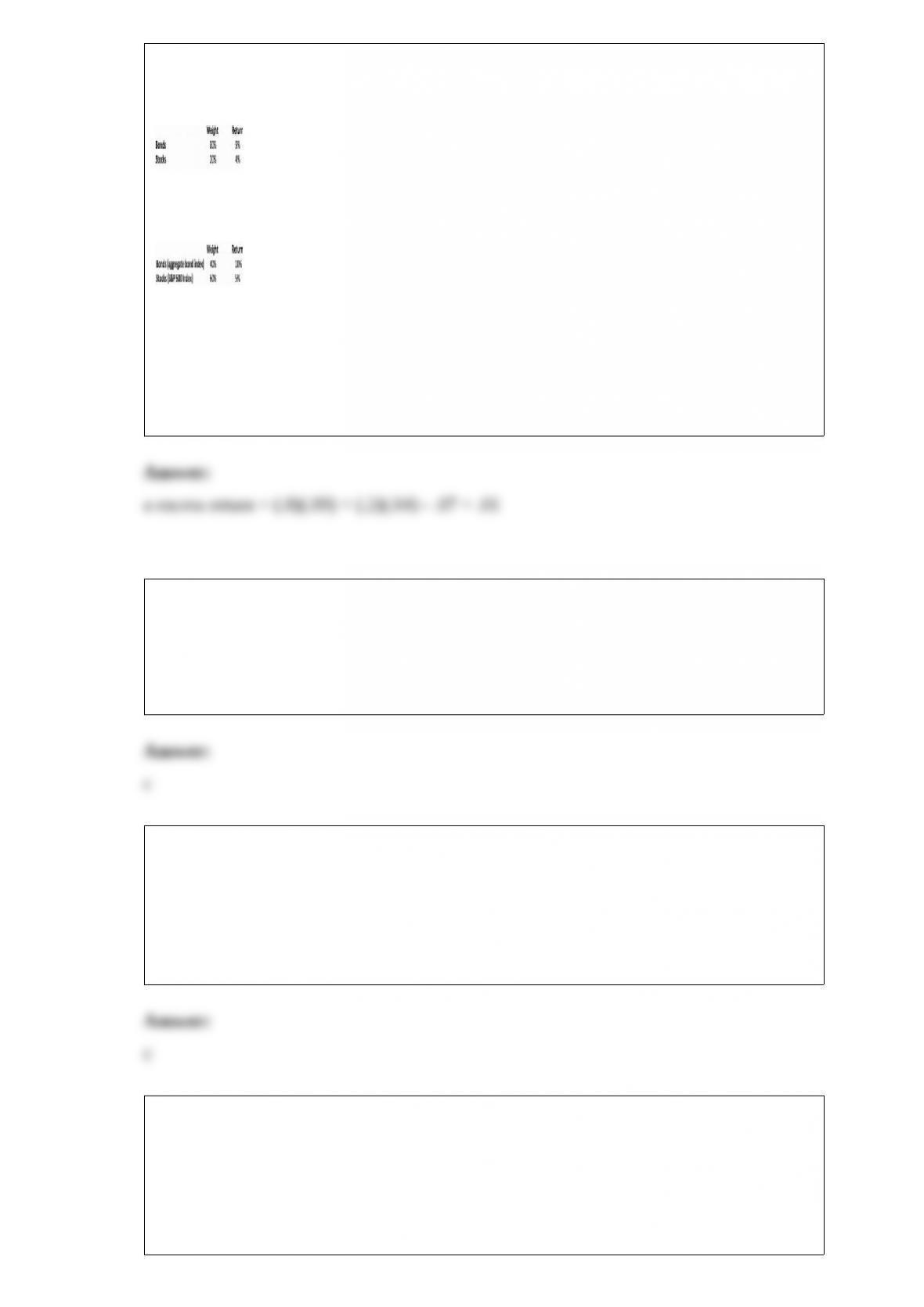

5) in a particular year, lost hope mutual fund made the following investments in asset

classes:

the return on a bogey portfolio was 12%, based on the following:

the total extra return on the managed portfolio was __________.

a.1%

b.2%

c.3%

d.4%

6) the complete portfolio refers to the investment in _________.

a.the risk-free asset

b.the risky portfolio

c.the risk-free asset and the risky portfolio combined

d.the risky portfolio and the index

7) investor portfolios are notoriously overweighted in home-country stocks. this is

commonly called ________.

a.local fat

b.nativism

c.home-country bias

d.misleading representation

8) an investor can design a risky portfolio based on two stocks, a and b. the standard

deviation of return on stock a is 24%, while the standard deviation on stock b is 14%.

the correlation coefficient between the returns on a and b is .35. the expected return on

stock a is 25%, while on stock b it is 11%. the proportion of the minimum-variance

portfolio that would be invested in stock b is approximately _________.

a.45%

b.67%

c.85%

d.92%

9) price volatility is greatest on which one of the following investments?

a.commercial paper

b.20-year zero-coupon bonds

c.treasury notes

d.treasury bills

10) a collateral trust bond is _______.

a.secured by other securities held by the firm

b.secured by equipment owned by the firm

c.secured by property owned by the firm

d.unsecured

11) when issued, most convertible bonds are issued _____________.

a.deep in the money

b.deep out of the money

c.slightly out of the money

d.slightly in the money

12) sinking funds are commonly viewed as protecting the _______ of the bond.

a.issuer

b.underwriter

c.holder

d.dealer

13) which one of the following is a true statement regarding corporate bonds?

a.a corporate callable bond gives its holder the right to exchange it for a specified

number of the company’s common shares.

b.a corporate debenture is a secured bond.

c.a corporate convertible bond gives its holder the right to exchange it for a specified

number of the company’s common shares.

d.holders of corporate bonds have voting rights in the company.

14) under firm-commitment underwriting, the ______ assumes the full risk that the

shares cannot be sold to the public at the stipulated offering price.

a.red herring

b.issuing company

c.initial stockholder

d.underwriter

15) tips are ______.

a.treasury bonds that pay no interest and are sold at a discount

b.u.k. bonds that protect investors from default risk

c.securities that trade on the toronto stock index

d.treasury bonds that protect investors from inflation

16) in an era of particularly low interest rates, which of the following bonds is most

likely to be called?

a.zero-coupon bonds

b.coupon bonds selling at a discount

c.coupon bonds selling at a premium

d.floating-rate bonds

17) a 1-year oil futures contract is selling for $74.50. spot oil prices are $68, and the

1-year risk-free rate is 3.25%.

based on the above data, which of the following sets of transactions will yield positive

riskless arbitrage profits?

a.buy oil in the spot market with borrowed money, and sell the futures contract.

b.buy the futures contract, and sell the oil spot and invest the money earned.

c.buy the oil spot with borrowed money, and buy the futures contract.

d.buy the futures contract, and buy the oil spot using borrowed money.

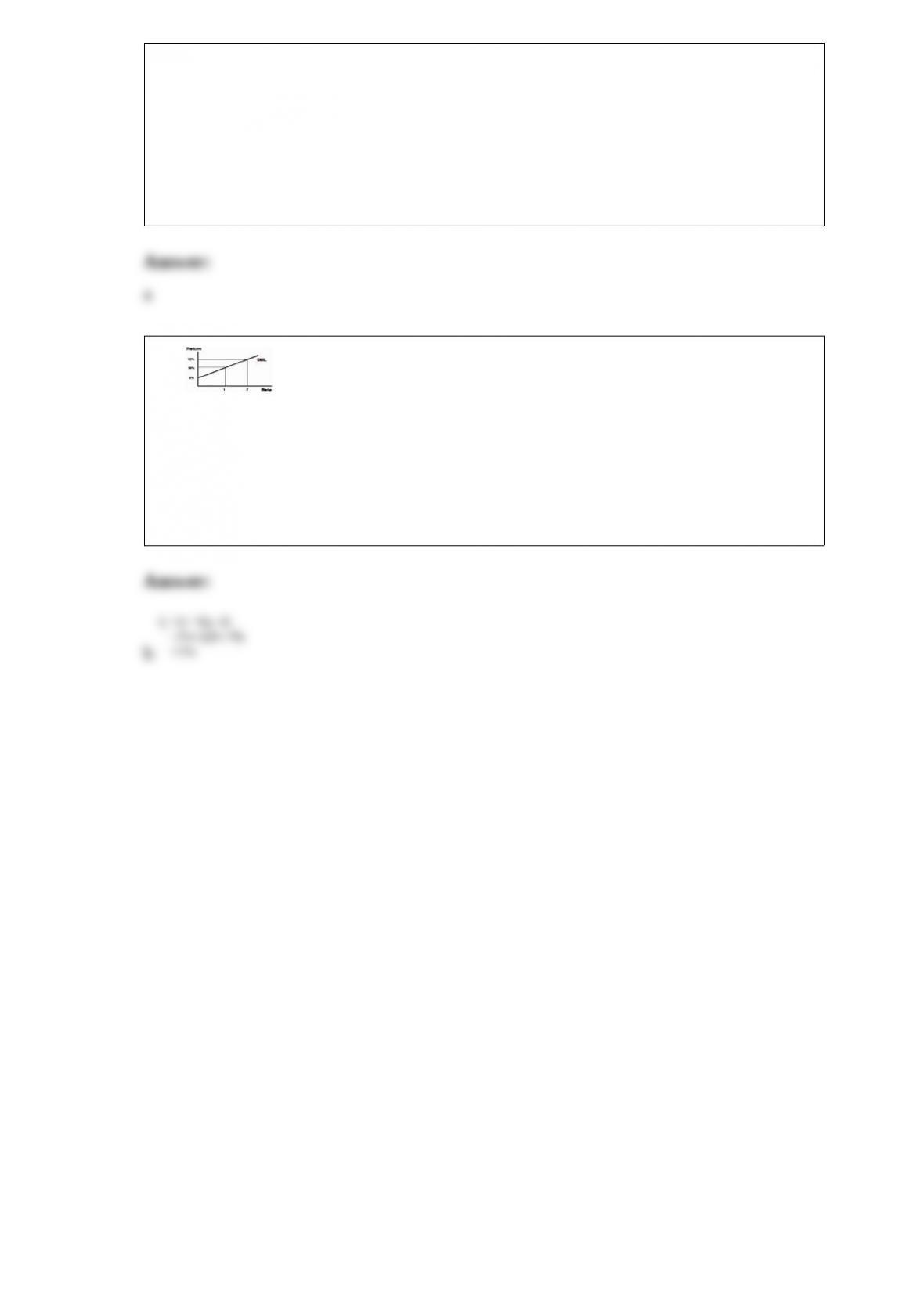

18)

what is the expected return for a portfolio with a beta of .5?

a.5%

b.7.5%

c.12.5%

d.15%