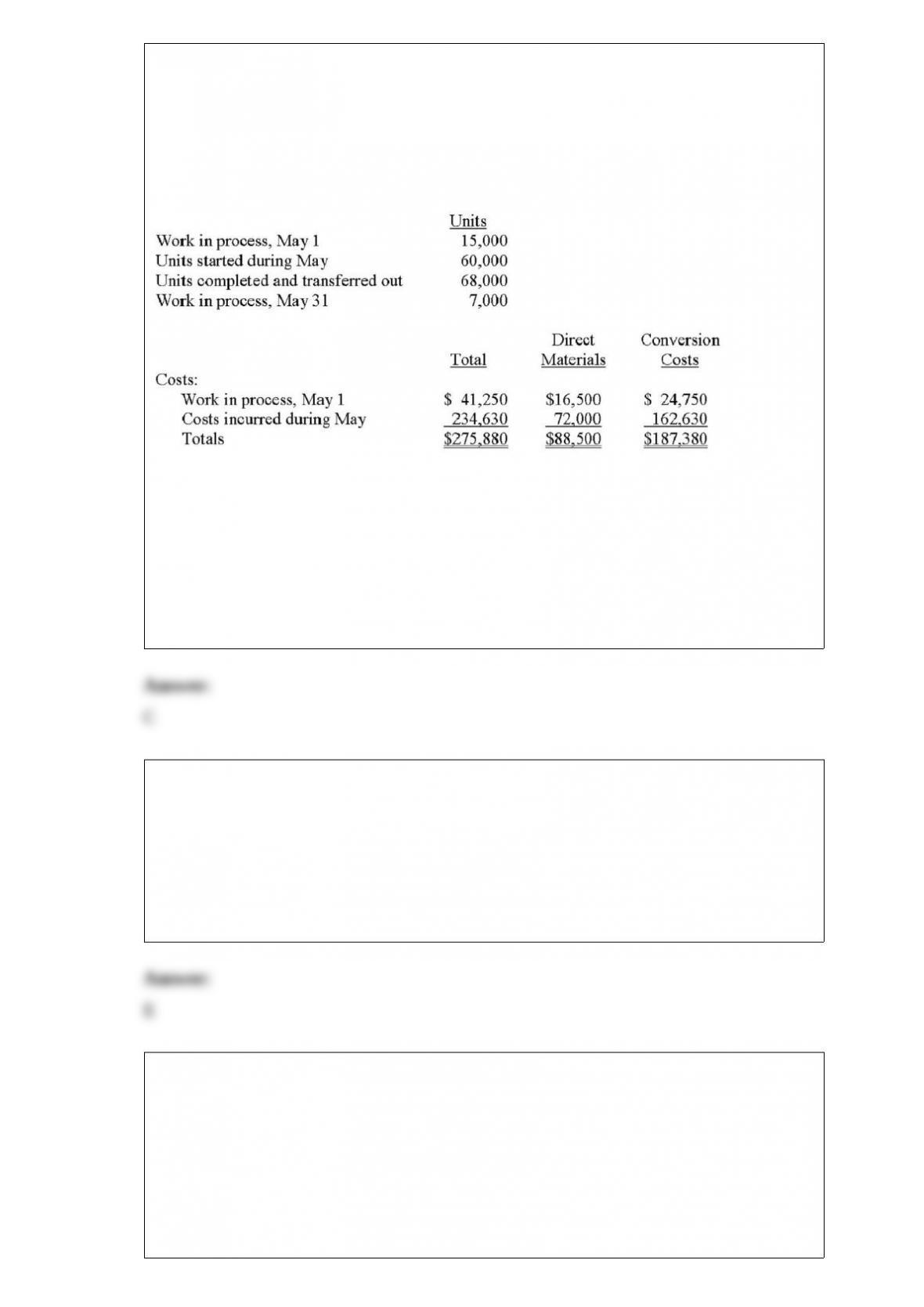

1) Southern Lake Chemical manufactures a product called Zubek. Direct materials are

added at the beginning of the process, and conversion activity occurs uniformly

throughout production. The beginning work-in-process inventory is 60% complete with

respect to conversion; the ending work-in-process inventory is 20% complete. The

following data pertain to May:

Using the weighted-average method of process costing, the cost per unit of conversion

activity is:

A.$2.50

B.$2.53

C.$2.70

D.$2.76

E.None of the answers is correct

2) A hospital administrator is in the process of implementing an activity-based-costing

system. Which of the following tasks would not be part of this process?

A.Identification of cost pools

B.Calculation of pool rates

C.Assignment of cost to services provided

D.Identification of cost drivers

E.None of the other answers is correct

3) Green Company owes White Company money for the purchase of equipment. White

has given Green the following payment options:

I. Immediate payment in full of $38,000.

II. Annual payments of $15,000 made at the end of each of the next three years.

III. A single payment of $48,000 made at the end of three years.

Green uses a 10% annual compound interest rate and will choose the option with the

lowest present value. Which option should Green choose, and what is the present value

of that option?

A.Option I, $34,542

B.Option I, $38,000

C.Option II, $37,305

D.Option III, $34,164

E.Option III, $36,048

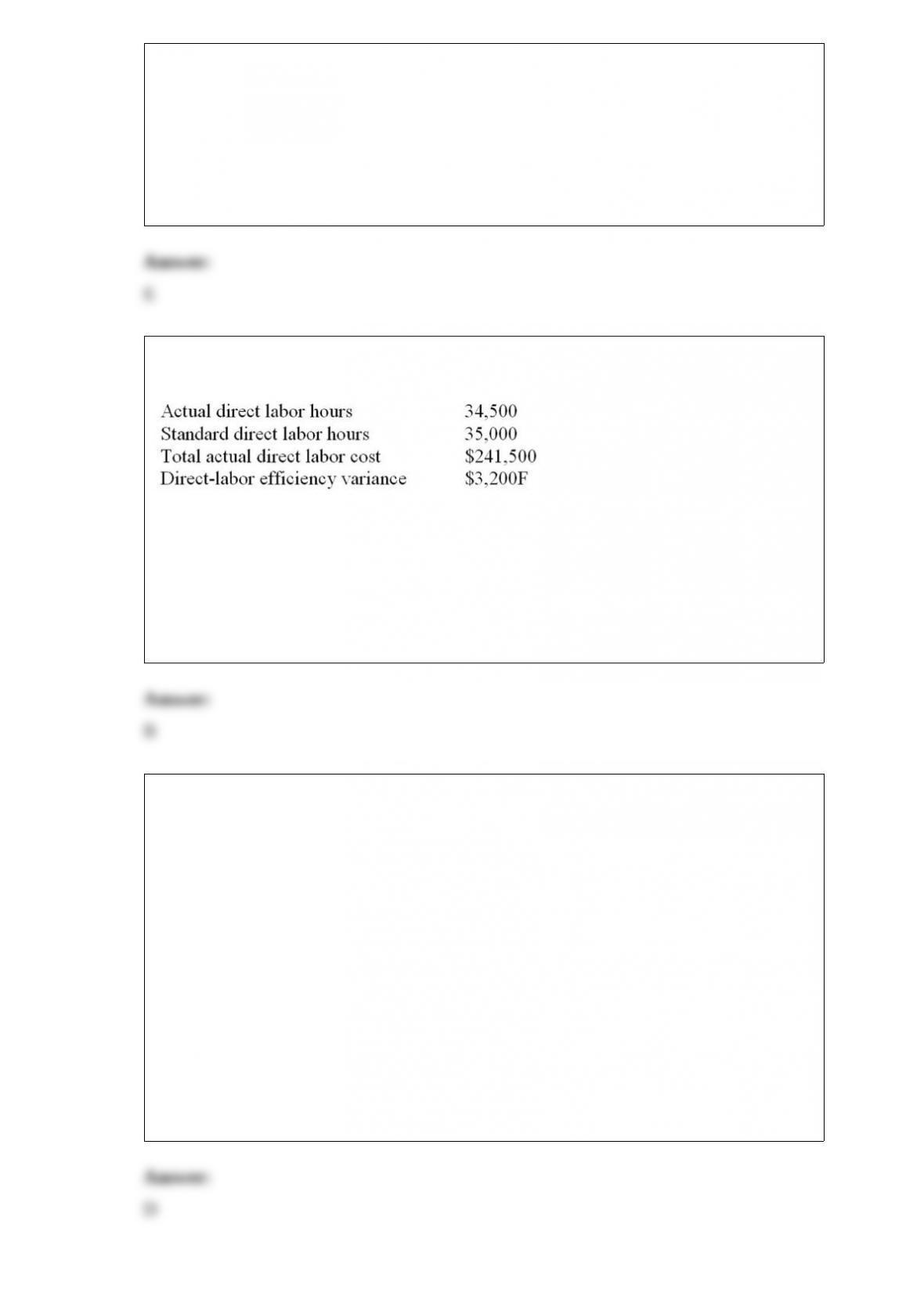

4) Consider the following information:

The direct-labor rate variance is:

A.$17,250U

B.$20,700U

C.$20,700F

D.$21,000F

E.none of the other answers are correct

5) Michaella, Inc. uses a process-costing system. A newly-hired accountant identified

the following procedures that must be performed by the close of business on Friday:

1Calculation of equivalent units

2Analysis of physical flows of units

3Assignment of costs to completed units and units still in process

4Calculation of unit costs

Which of the following choices correctly expresses the proper order of the preceding

tasks?

A.1, 2, 3, 4

B.1, 2, 4, 3

C.1, 4, 3, 2

D.2, 1, 4, 3

E.2, 1, 3, 4

6) The payback method is a popular way to analyze investment proposals.

Required:

A. Explain how the payback period is determined. Generally speaking, from a payback

perspective, which projects are viewed to be the most attractive?

B. Can the payback method take income taxes into consideration? Explain.

C. What are the deficiencies of the payback method?

7) Which of the following is classified as an inventory shortage cost?

A.Purchase order preparation

B.Production disruption

C.Lost sales and lost customers

D.Spoilage

E.Both production disruption and lost sales and lost customers

8) The main idea behind the time value of money is that:

A.cash flows received in the distant future are less valuable than cash flows received in

the near-term future

B.cash received in year 3, say, $80,000, has the same value as $40,000 received in year

3 plus $40,000 received in year 4

C.cash flows received in different years are treated as equal in value

D.cash payments made in the future have the same value as payments made today

E.timing considerations of cash flows have little value in decision making

9) An allocation base for a cost pool should ideally be:

A.machine hours

B.a cost object

C.a common cost

D.a cost driver

E.direct labor, either cost or hours

10) For many years, Orbit Corporation has used a straightforward cost-plus pricing

system, marking its goods up approximately 20% of total cost. The company has been

profitable; however, it has recently lost considerable business to foreign competitors

that have become very aggressive in the marketplace. These firms appear to be using

target costing.

An example of Orbit’s woes is typified by item no. 710, which has the following

unit-cost characteristics: direct materials, $50; direct labor, $90; manufacturing

overhead, $40; and selling and administrative expenses, $20. The going market price

for an identical product of identical quality is $210, which is below what Orbit is

charging.

Required:

A. Contrast cost-plus pricing and target costing.

B. What is Orbit’s current selling price for item no. 710?

C. If Orbit used target costing for item no. 710, what must happen to costs if the

company desired to meet market prices and maintain its current rate of profit on sales?

By how much?

11) Luke, Inc. has a standard variable overhead rate of $5 per machine hour, with each

completed unit expected to take three machine hours to produce. A review of the

company’s accounting records found the following:

Actual production: 19,500 units

Variable-overhead efficiency variance: $9,000U

Variable-overhead spending variance: $21,000F

What was Luke’s actual variable overhead during the period?

A.$262,500

B.$280,500

C.$304,500

D.$322,500

E.None of the other answers are correct

12) Narchie sells a single product for $50. Variable costs are 60% of the selling price,

and the company has fixed costs that amount to $400,000. Current sales total 16,000

units.

Narchie:

A.will break-even by selling 8,000 units

B.will break-even by selling 13,333 units

C.will break-even by selling 20,000 units

D.will break-even by selling 1,000,000 units

E.cannot break-even because it loses money on every unit sold

13) Standard costs rather than actual costs should be used in transfer-pricing methods

because:

A.financial accounting rules (GAAP) require the use of standard costs

B.tax rules require the use of standard costs

C.standard costs are more readily available than actual costs

D.standard costs facilitate a professionally negotiated, amicable settlement between the

buying and selling divisions

E.inefficient producing divisions could pass on their inefficiencies to buying divisions

in the transfer price

14) Dixie Company, which applies overhead at the rate of 190% of direct material cost,

began work on job no. 101 during June. The job was completed in July and sold during

August, having accumulated direct material and labor charges of $27,000 and $15,000,

respectively. On the basis of this information, the total overhead applied to job no. 101

amounted to:

A.$0

B.$28,500

C.$51,300

D.$70,500

E.$79,800

15) The journal entry needed to record $5,000 of advertising for Westwood

Manufacturing would include:

A.a debit to Advertising Expense

B.a credit to Advertising Expense

C.a debit to Manufacturing Overhead

D.a credit to Manufacturing Overhead

E.a debit to Projects-in-Process

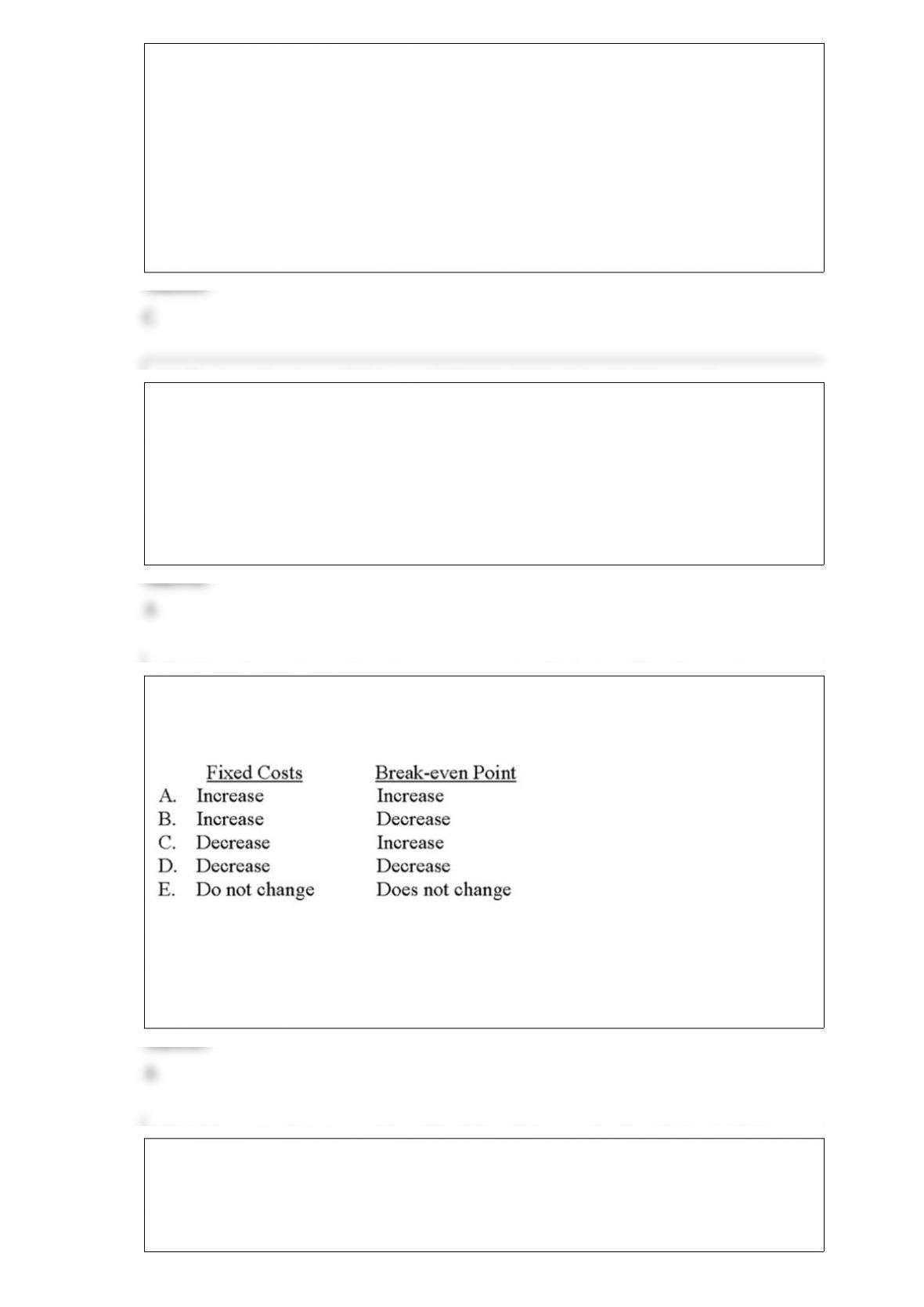

16) When advanced manufacturing systems are installed, what effect does such

installation usually have on fixed costs and the break-even point?

A.Choice A

B.Choice B

C.Choice C

D.Choice D

E.Choice E

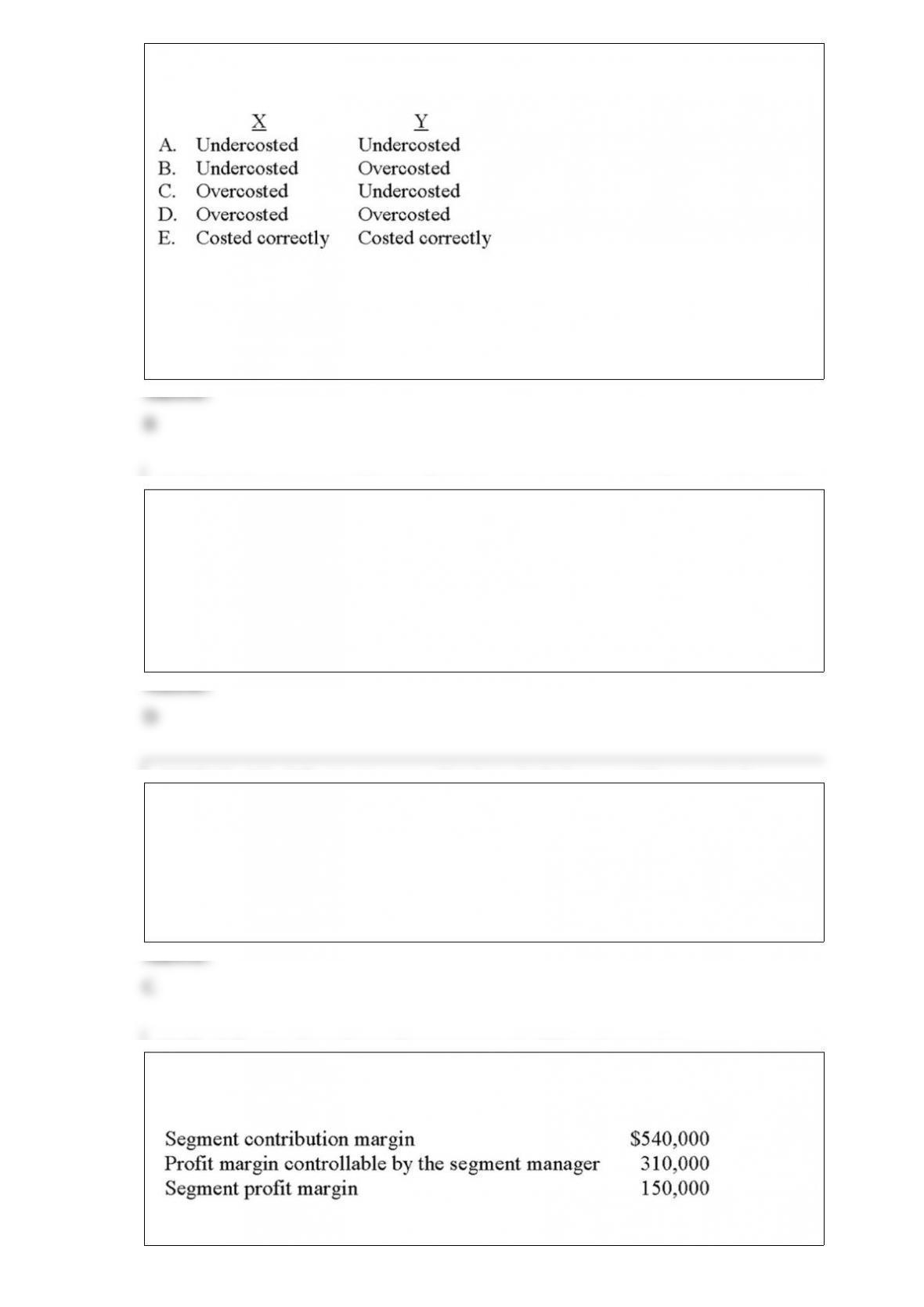

17) Jackson manufactures products X and Y, applying overhead on the basis of labor

hours. X, a low-volume product, requires a variety of complex manufacturing

procedures. Y, on the other hand, is both a high-volume product and relatively

simplistic in nature. What would an activity-based costing system likely disclose about

products X and Y as a result of Jackson’s current accounting procedures?

A.Choice A

B.Choice B

C.Choice C

D.Choice D

E.Choice E

18) Which department would normally begin an investigation regarding an unfavorable

materials quantity variance?

A.Quality control

B.Purchasing

C.Engineering

D.Production

E.Receiving

19) Which of the following is not an ethical standard of managerial accounting?

A.Competence

B.Confidentiality

C.Efficiency

D.Integrity

E.Credibility

20) The following data relate to Department no. 3 of Tsing Corporation:

On the basis of this information, Department no. 3’s variable operating expenses are:

A.$80,000

B.$160,000

C.$230,000

D.$390,000

E.not determinable

21) Which of the following statements is (are) true about non-value-added activities?

I. Non-value-added activities are often unnecessary and dispensable.

II. Non-value-added activities may be necessary but are being performed in an

inefficient and improvable manner.

III. Non-value-added activities can be eliminated without deterioration of product

quality, performance, or perceived value.

A.I only

B.II only

C.III only

D.I and II

E.I, II, and III

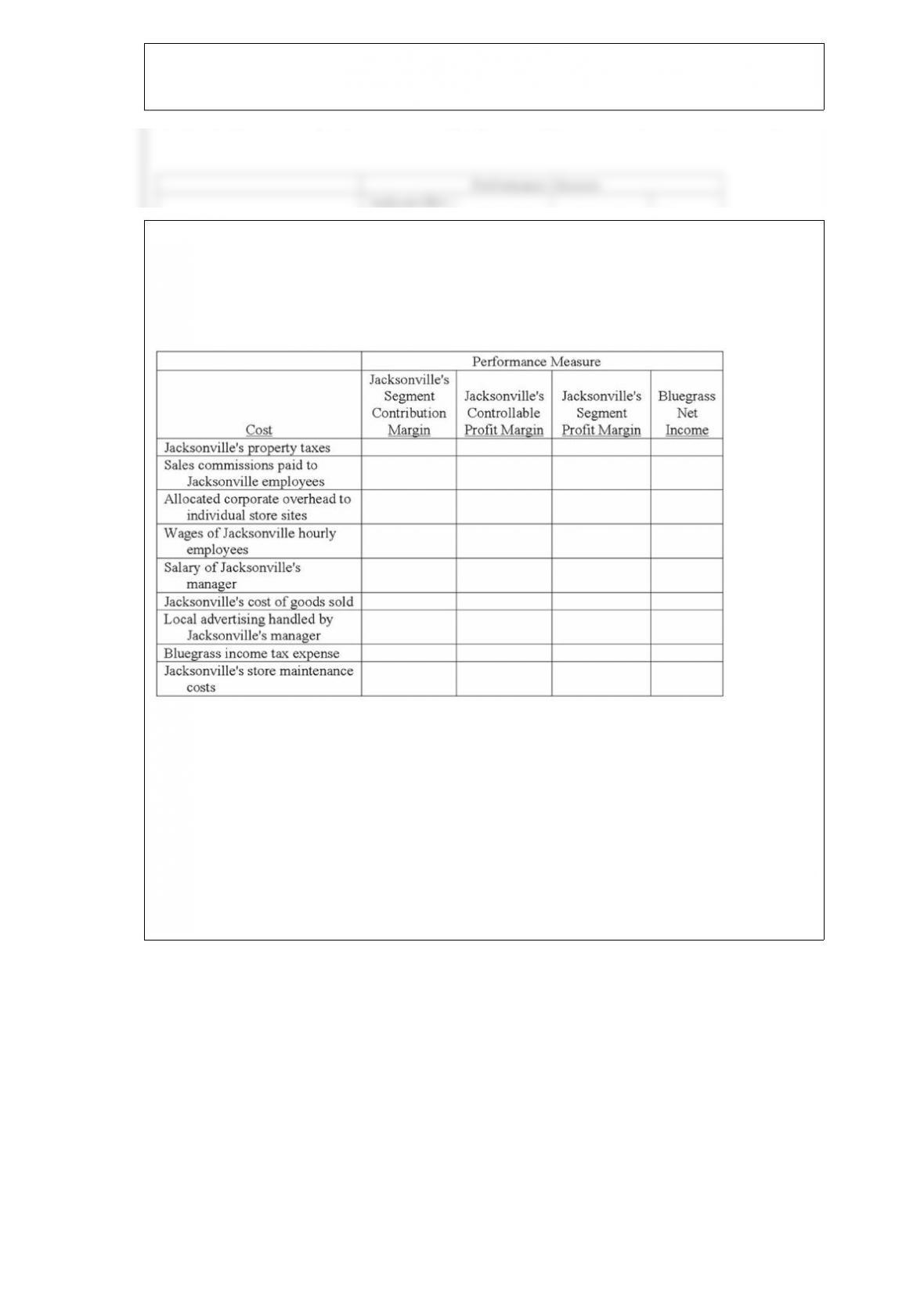

22) HiTech Products manufactures three types of remote-control devices: Economy,

Standard, and Deluxe. The company, which uses activity-based costing, has identified

five activities (and related cost drivers). Each activity, its budgeted cost, and related cost

driver is identified below.

The following information pertains to the three product lines for next year:

What is HiTech’s pool rate for the finishing activity?

A.$5.00 per labor hour

B.$5.00 per machine hour

C.$5.00 per unit

D.$7.50 per unit

E.None of the other answers is correct

23) Consider the following statements regarding the economic pricing model:

I. The economic model is limited in use because a firm’s demand curve is difficult to

determine.

II. The marginal revenue and marginal cost model is valid for all forms of market

organization (perfect competition, oligopoly, and so forth).

III. Cost accounting systems are not designed to measure the marginal changes in cost

incurred as production and sales increase.

Which of the above statements is (are) true?

A.I only

B.III only

C.I and III

D.II and III

E.I, II, and III

24) Hirsch Company has per-unit fixed and variable manufacturing costs of $40 and

$15, respectively. Variable selling and administrative costs are $9 per unit. Consider the

two independent cases that follow for the firm.

Case A: Variable-costing income, $110,000; sales, 6,000 units; production, 6,000 units

Case B: Variable-costing income, $178,000; sales, 7,500 units; production, 7,100 units

Required:

A. From a product-costing perspective, what is the basic difference between absorption

costing and variable costing?

B. Compute Hirsch’s absorption-costing income in Case A.

C. Compute Hirsch’s absorption-costing income in Case B.

25) Consider the following statements about absorption costing and variable costing:

I. Variable costing is consistent with contribution reporting and cost-volume-profit

analysis.

II. Variable costing must be used for external financial reporting.

III. A number of companies use both absorption costing and variable costing.

Which of the above statements is (are) true?

A.I only

B.II only

C.III only

D.I and II

E.I and III

26) SchilleCompany is considering a $5.4 million asset investment that has a four-year

service life and a $400,000 salvage value. The investment is expected to produce annual

savings in cash operating costs of $860,000 and will require a $250,000 overhaul in

year 3, which is fully-deductible for tax purposes.

Schille uses the net-present-value method to analyze investments. Asset investments are

depreciated by the straight-line method, ignoring salvage values in related

computations.

Required:

A. Ignoring income taxes, determine the (pre-discounted) cash-flow amounts that

would be used in a net-present-value analysis for (1) the asset acquisition, (2) annual

savings in cash operating costs, (3) annual straight-line depreciation, (4) the overhaul in

year 3, and (5) disposal of the asset in year 4. Note cash outflows in parentheses.

B. Repeat requirement “A,” assuming the company is subject to a 30% income tax rate.

Assume the company depreciates the asset using the optional straight-line method.

Additionally, it depreciates it over the asset’s service life (not its MACRS life).

27) Garcia’s inventory increased during the year. On the basis of this information,

income reported under absorption costing:

A.will be the same as that reported under variable costing

B.will be higher than that reported under variable costing

C.will be lower than that reported under variable costing

D.will differ from that reported under variable costing, the direction of which cannot be

determined from the information given

E.will be less than that reported in the previous period

28) The individual generally responsible for the direct-material price variance is the:

A.sales manager

B.production supervisor

C.purchasing manager

D.finance manager

E.head of the human resources department

29) Which of the following employees at Starbucks would likely be considered as

holding a staff position?

A.The company’s chief operating officer (COO)

B.The manager of a store located in Kansas City, Missouri

C.The company’s lead, in-house attorney

D.The company’s chief financial officer (CFO)

E.The company’s lead, in-house attorney and the company’s chief financial officer

(CFO)

30) Bluegrass, Inc., which is headquartered in Atlanta, operates a chain of 225 clothing

stores throughout the United States. Consider the costs that appear in the following

table, many of which pertain to the company’s sole operation in Jacksonville, Florida:

Specify store maintenance as a fixed costs. Adopt the following language.”

Jacksonville’s store maintenance costs as agreed upon in yearly maintenance contract

negotiated by Jacksonville’s manager.”

Required:

Analyze each of the costs and determine whether the cost affects Jacksonville’s segment

contribution margin, controllable profit margin, and segment profit margin, and/or the

net income of Bluegrass, Inc. Place an “X” in the appropriate cell(s).

31) The following events occurred at Crescent Manufacturing (CM), an assembler of

engine parts, during May:

1> Because of a stock shortage at its regular supplier, CM had to rely on a new vendor

for two purchases of raw material parts. The vendor required CM to pay air-freight

charges; however, upon arrival, the company found the goods to be above-average in

quality.

2> The local municipality raised its property tax rates by 2%.

3> A flu outbreak on the assembly line forced management to use more experienced,

senior personnel to complete production orders on a timely basis. These workers more

than made up for lost time.

4> A shoddy maintenance program resulted in an abnormally high number of

breakdowns on machine no. 76 and slowed production.

5> The implementation of a new program had positive effects for the company with

respect to material usage and worker productivity.

Required:

Create a table with the following headings: material price variance, material quantity

variance, labor rate variance, and labor efficiency variance. Determine which of these

variances would be affected by the individual events and whether the variance would be

favorable or unfavorable.

32) List several factors that an organization might consider when developing a sales

forecast.

33) Discuss the importance of budgeting and identify five purposes of budgeting

systems.

34) Consider the descriptors that follow.

1> Is heavily involved with the recordkeeping and reporting of assets, liabilities, and

stockholders’ equity.

2> Focuses on planning, decision making, directing, and control.

3> Is heavily regulated.

4> A field that is becoming more “cross-functional” in nature.

5> Much of the field is based on costs and benefits.

6> Is involved almost exclusively with past transactions and events.

7> Much of the information provided is directed toward stockholders, financial

analysts, creditors, and other external parties.

8> Tends to focus more on subunits within an entity rather than the organization as a

whole.

9> May become involved with measures of customer satisfaction, and the amount of

actual cost incurred vs. budgeted targets.

Required:

Determine whether the descriptors are most closely associated with financial

accounting or managerial accounting.

35) Hitchcock Company is studying the impact of the following:

1> An increase in sales price.

2> An increase in the variable cost per unit.

3> An increase in the number of units sold (note: each unit produces a $6 contribution

margin).

4> A decrease in fixed costs.

5> A proposed change in the method of compensation for salespeople, away from

commissions based on gross sales dollars and toward higher monthly salaries.

Required:

Determine the impact of each of these operating changes on Hitchcock’s per-unit

contribution margin and break-even point by completing the chart that follows. Your

responses should be Increase (INC), Decrease (DEC), No Effect (NE), or Insufficient

Information to Judge (II).

36) Briefly describe the stages used in the two-stage allocation process for assigning

overhead costs.

37) Describe the economic characteristics of sunk costs and opportunity costs, and

explain the impact that these costs may have on decisions.

38) The difference in income between absorption and variable costing can be explained

by the change in finished-goods inventory (in units) multiplied by the standard fixed

manufacturing overhead rate.

Required:

Explain why this calculation accounts for the difference noted.