1) the fisher effect states that

a.any forward premium or discount is equal to the expected change in the exchange rate

b.any forward premium or discount is equal to the actual change in the exchange rate

c.the nominal interest rate differential reflects the expected change in the exchange rate

d.an increase (decrease) in the expected inflation rate in a country will cause a

proportionate increase (decrease) in the interest rate in the country

2) after a hostile takeover

a.the existing management team is usually fired

b.the existing management team is usually retained at a higher wage

c.the target company usually mounts a takeover defense

3) in mutual funds, investment in emerging foreign equity markets

a.represents less than one percent of investments in u.s.-based mutual funds

b.represents about five percent of investments in u.s.-based mutual funds

c.represents more than twenty percent of investments in u.s.-based mutual funds

d.declined during the 1990s

4) suppose the u.s. dollar substantially depreciates against the japanese yen. the change

in exchange rate

a.will tend to weaken the competitive position of import-competing u.s. car makers

b.will tend to strengthen the competitive position of import-competing u.s. car makers

c.will tend to strengthen the competitive position of japanese car makers at the expense

of u.s. makers

d.none of the above

5) a pyramidal ownership structure is one in which

a.a shareholder controls a holding company that owns a controlling block of another

company, which in turn owns controlling interests in yet another company, and so on

b.equity cross-holdings among a group of companies, such as keiretsu and chaebols can

be used to concentrate and leverage voting rights to acquire control

c.a combination of these schemes may also be used to leverage control in a pyramidal

ownership structure

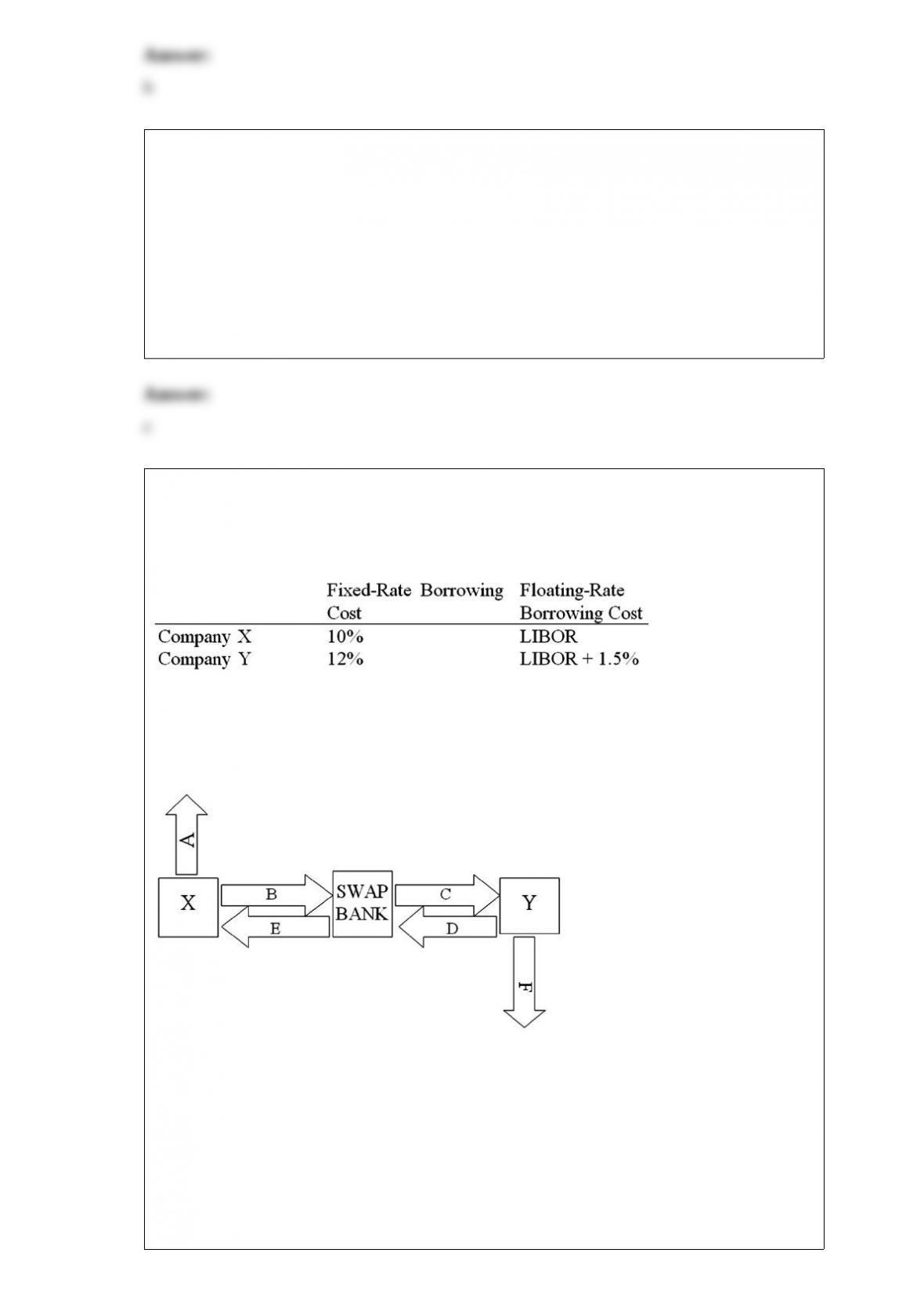

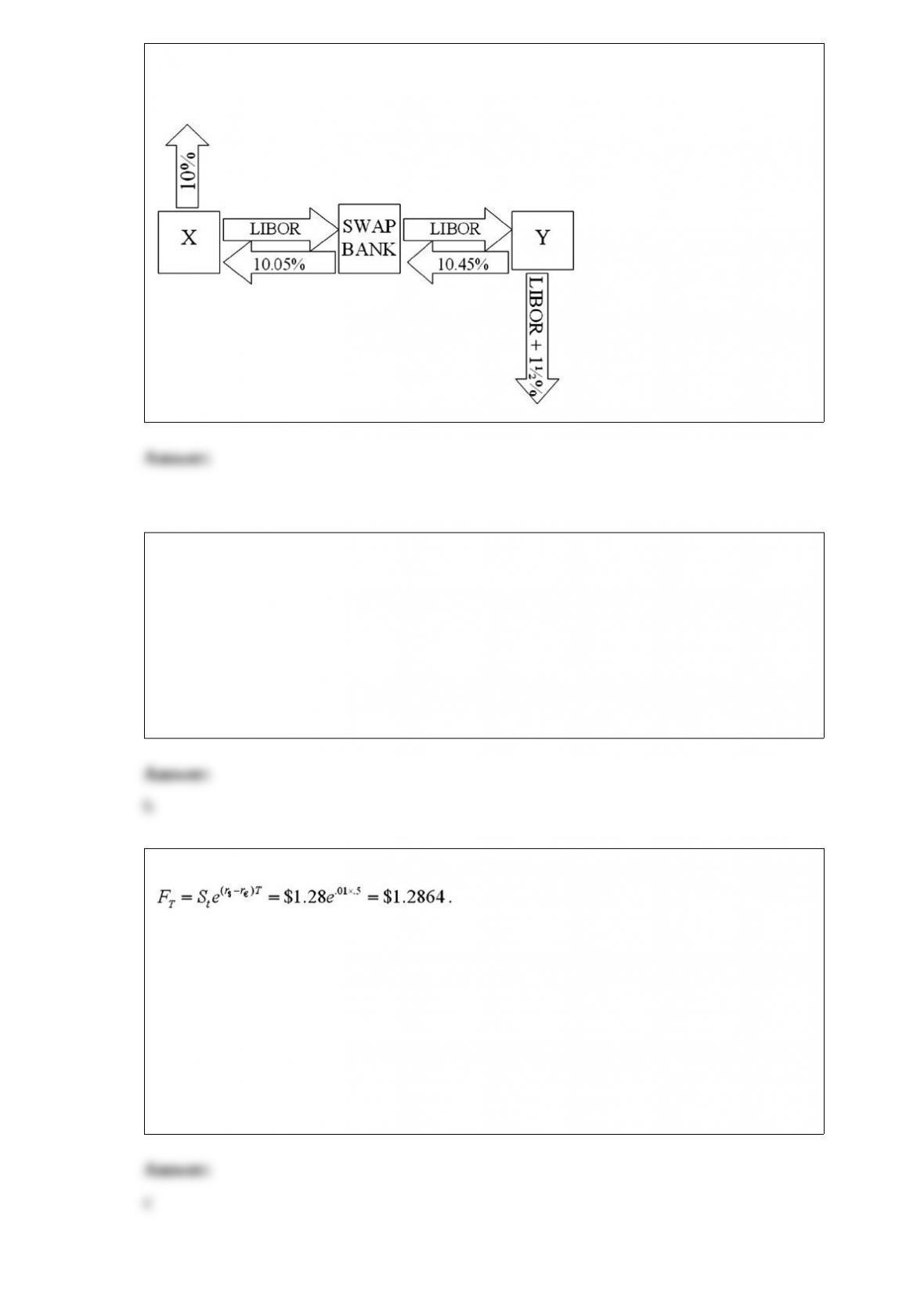

6) company x wants to borrow $10,000,000 floating for 5 years; company y wants to

borrow $10,000,000 fixed for 5 years. their external borrowing opportunities are shown

below:

a swap bank is involved and quotes the following rates five-year dollar interest rate

swaps at 10.05%-10.45% against libor flat.

assume both x and y agree to the swap bank’s terms.

fill in the values for a, b, c, d, e, & f on the diagram.

a.a = libor; b = 10.45%; c = 10.05%; d = libor; e = libor; f = 12%

b.a = 10%; b = 10.45%; c = 10.05%; d = libor; e = libor; f = libor + 1%

c.a = 10%; b = 10.45%; c = libor; d = libor; e = 10.05%; f = libor + 1%

d.a = 10%; b = libor; c = libor; d = 10.45%; e = 10.05%; f = libor + 1%

7) systematic risk refers to

a.the diversifiable (company specific) risk of an asset

b.the nondiversifiable (market) risk of an asset

c.economic and political risk

d.the risk that can be hedged

8) assume that the dollar-euro spot rate is $1.28 and the six-month forward rate is

the six-month u.s. dollar rate is 5% and the

eurodollar rate is 4%. the minimum price that a six-month american call option with a

striking price of $1.25 should sell for in a rational market is

a.0 cents

b.3.47 cents

c.3.55 cents

d.3 cents

9) the majority of countries got off the gold standard in 1914 when

a.the american civil war ended

b.world war i broke out

c.world war ii started

d.none of the above

10) intangible assets are often hard to package and sell to foreigners

a.because they usually default on the contracts that they sign

b.as a result, there is more fdi than there might otherwise be

c.because property rights in intangible assets are difficult to establish and protect,

especially in foreign countries where legal recourse may not be readily available

d.both b and c

11) shareholders of u.s. bidders (acquiring firms in m&a) experience significant positive

abnormal returns when firms expand into new industries and geographic markets.

12) suppose that the pound is pegged to gold at £20 per ounce and the dollar is pegged

to gold at $35 per ounce. this implies an exchange rate of $1.75 per pound. if the

current market exchange rate is $1.60 per pound, how would you take advantage of this

situation? hint: assume that you have $350 available for investment.

a.start with $350. buy 10 ounces of gold with dollars at $35 per ounce. convert the gold

to £200 at £20 per ounce. exchange the £200 for dollars at the current rate of $1.80 per

pound to get $360

b.start with $350. exchange the dollars for pounds at the current rate of $1.60 per

pound. buy gold with pounds at £20 per ounce. convert the gold to dollars at $35 per

ounce

c.a and b both work

d.none of the above

13) a japanese importer has a 1,000,000 payable due in one year.

the one-year risk free rates are i$ = 4.03%; i = 6.05%; and i¥ = 1%. detail a strategy

using forward contracts that will hedge his exchange rate risk. have an estimate of how

many contracts of what type.

a.go short in 12 yen forward contracts. go long in 16 euro contracts

b.go long in 12 yen forward contracts. go short in 16 euro contracts

c.go short in 16 yen forward contracts. go long in 12 euro contracts

d.none of the above

14) which of the following is correct?

a. the value (in dollars) of a call option on £5,000 with a strike price of $10,000 is equal

to the value (in dollars) of a put option on $10,000 with a strike price of £5,000 only

when the spot exchange rate is $2 = £1

b. the value (in dollars) of a call option on £5,000 with a strike price of $10,000 is equal

to the value (in dollars) of a put option on $10,000 with a strike price of £5,000

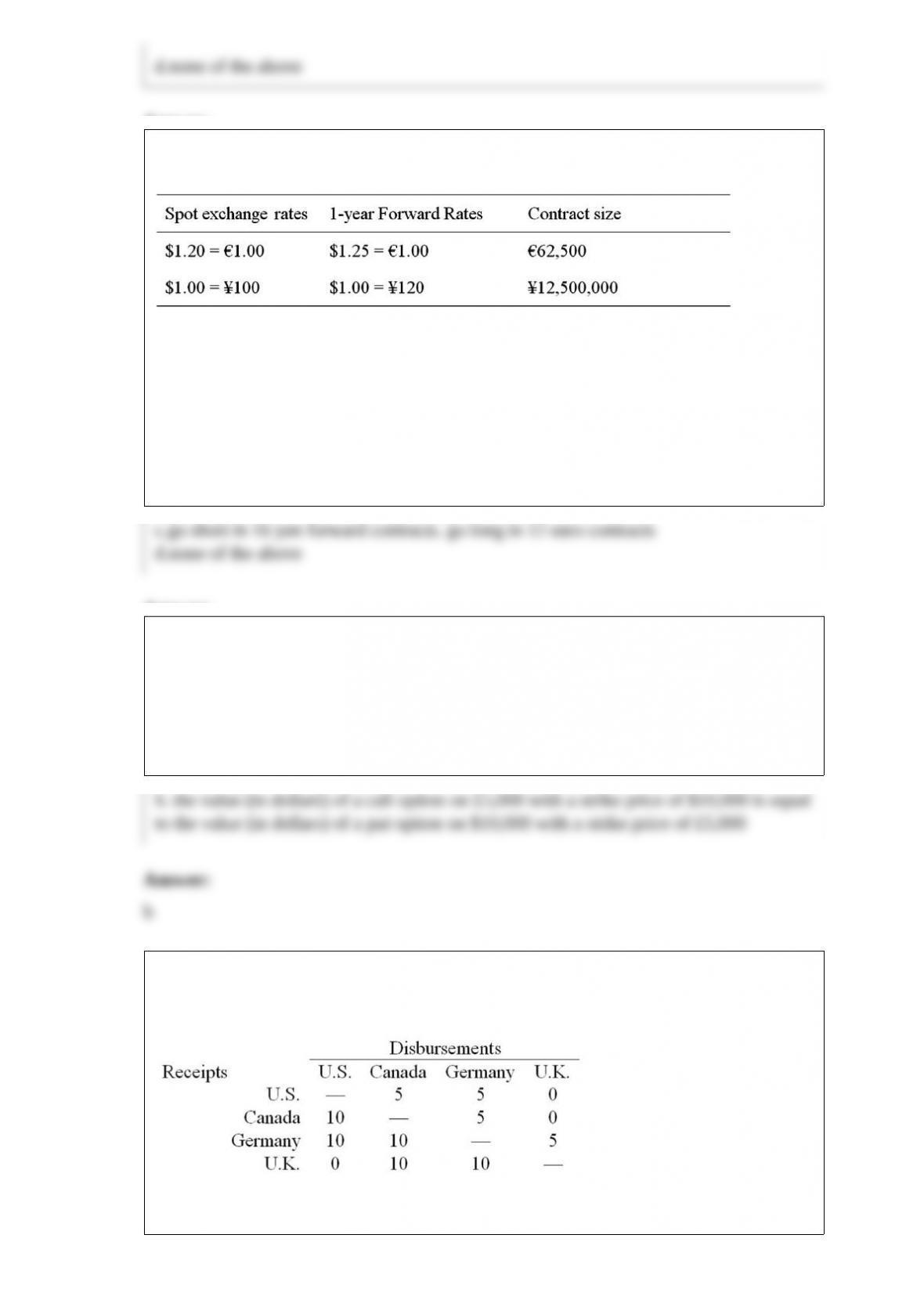

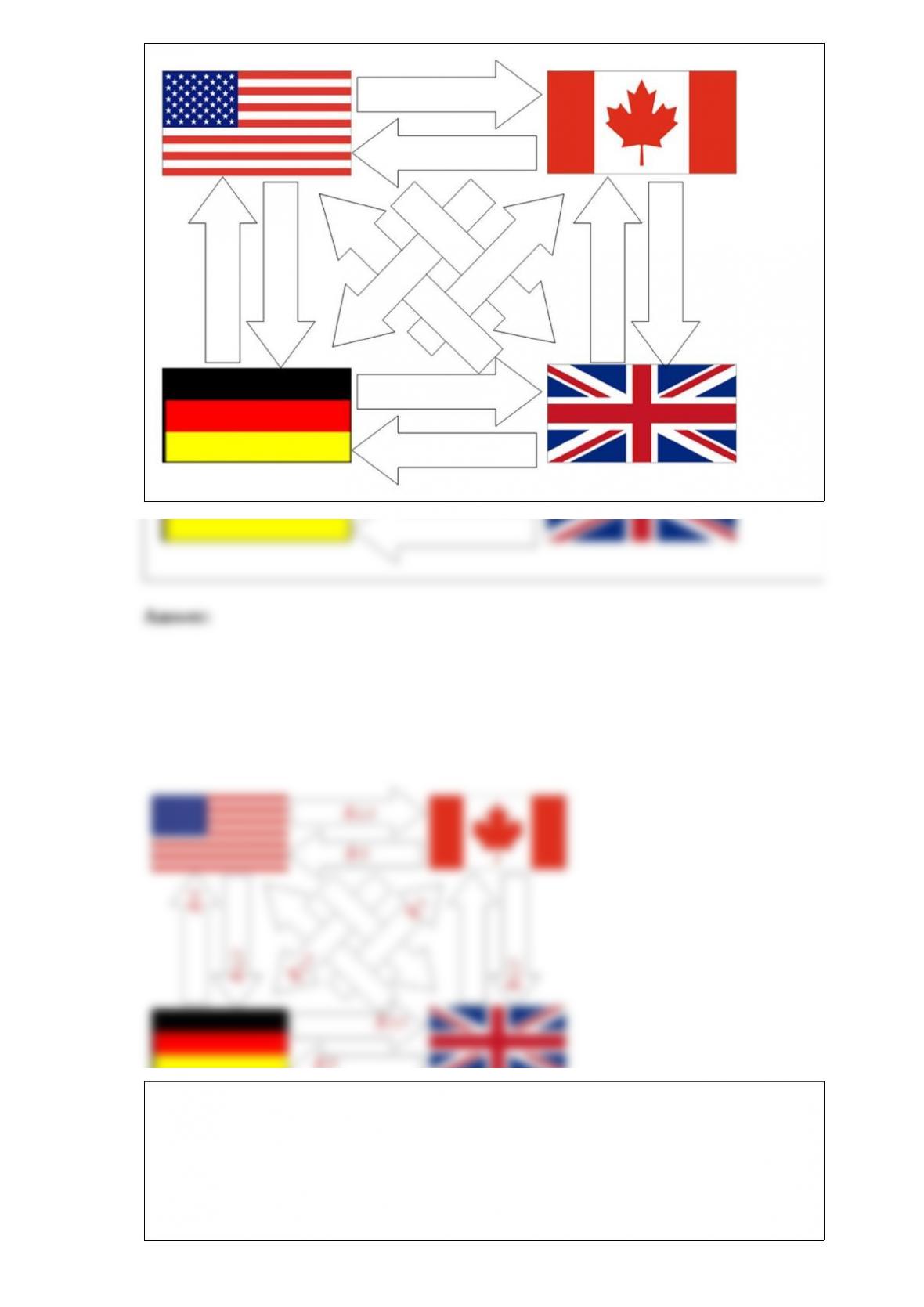

15) your firm’s interaffiliate cash receipts and disbursements matrix is shown below

($000):

fill out the following figure with the initial situation shown in the table.

16) the stock market of country a has an expected return of 5%, and standard deviation

of expected return of 8%. the stock market of country b has an expected return of 15%

and standard deviation of expected return of 10%.

assume that the correlation of expected return between a and b is negative 1. calculate

the standard deviation of expected return of the portfolio in the last question.

17) the time from acceptance to maturity on a $1,000,000 banker’s acceptance is 90

days.

the importing bank’s acceptance commission is 3 percent and that the market rate for

90-day b/as is 5 percent.

calculate the amount the banker will receive if the exporter discounts the b/a with the

importer’s bank.

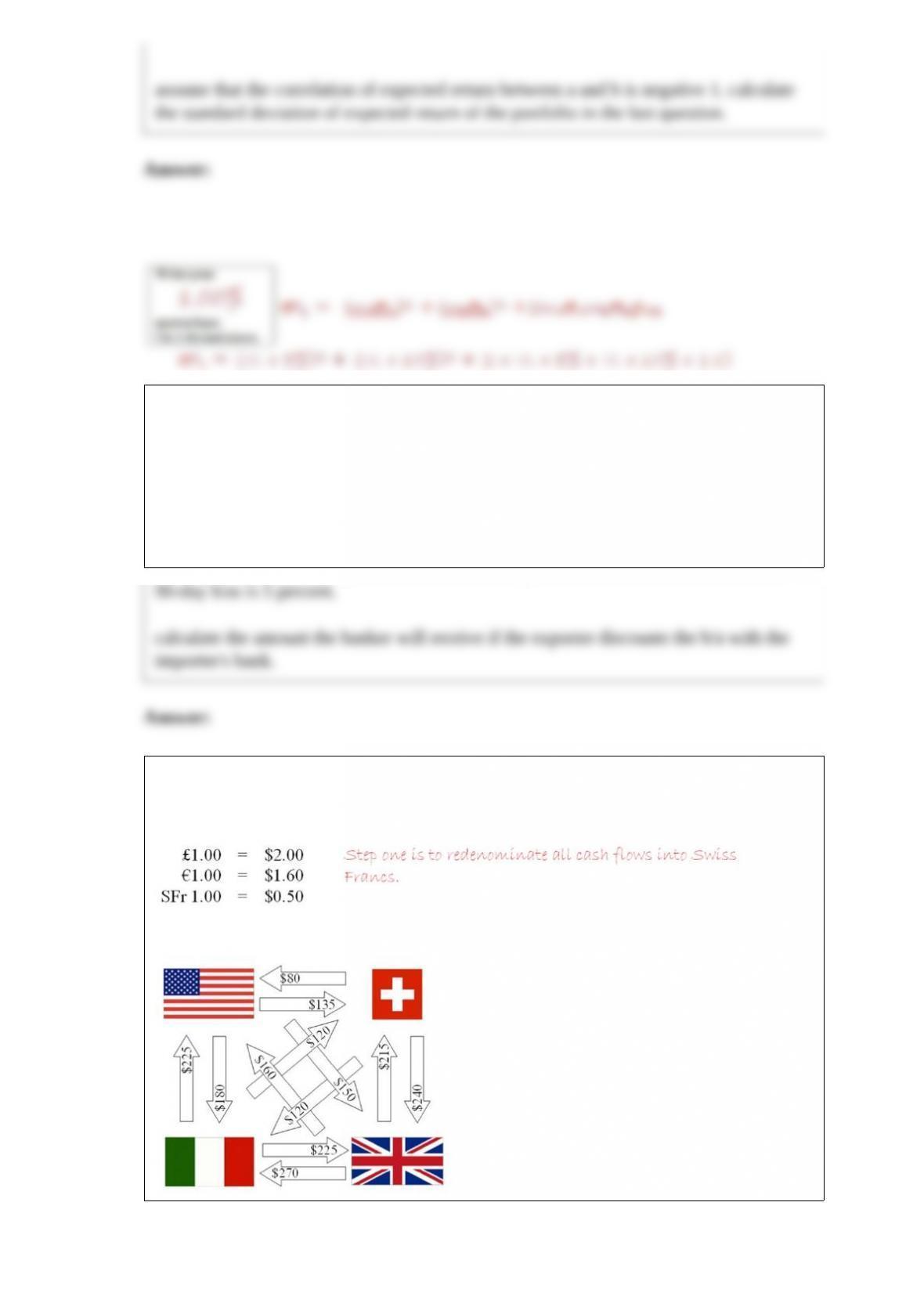

18) simplify the following set of intra company cash flows for this swiss firm

consider the following exchange rates.