Kahneman and Tversky (1973) reported that __________ give too much weight to

recent experience compared to prior beliefs when making forecasts.

A. young men

B. young women

C. people

D. older men

E. older women

In the mean-standard deviation graph, which one of the following statements is true

regarding the indifference

curve of a risk-averse investor?

A. It is the locus of portfolios that have the same expected rates of return and different

standard deviations.

B. It is the locus of portfolios that have the same standard deviations and different rates

of return.

C. It is the locus of portfolios that offer the same utility according to returns and

standard deviations.

D. It connects portfolios that offer increasing utilities according to returns and standard

deviations.

E. None of the options are correct.

A coupon bond pays annual interest, has a par value of $1,000, matures in four years,

has a coupon rate of 10%, and has a yield to maturity of 12%. The current yield on this

bond is

A. 10.65%.

B. 10.45%.

C. 10.95%.

D. 10.52%.

E. None of the options are correct.

As a financial analyst, you are tasked with evaluating a capital-budgeting project. You

were instructed to use

the IRR method, and you need to determine an appropriate hurdle rate. The risk-free

rate is 4%, and the

expected market rate of return is 11%. Your company has a beta of 1.4, and the project

that you are evaluating

is considered to have risk equal to the average project that the company has accepted in

the past. According to

CAPM, the appropriate hurdle rate would be

A. 13.8%.

B. 7%.

C. 15%.

D. 4%.

E. 1.4%.

A ___________ bond is a bond where the bondholder has the right to cash in the bond

before maturity at a specified price after a specific date.

A. callable

B. coupon

C. put

D. Treasury

E. zero-coupon

Trading in “exotic options” takes place primarily

A. on the New York Stock Exchange.

B.in the over-the-counter market.

C. on the American Stock Exchange.

D. in the primary marketplace.

E. None of the options.

The most common measure of loss associated with extremely negative returns is

A. lower partial standard deviation.

B. value at risk.

C. expected shortfall.

D. standard deviation.

A year ago, you invested $12,000 in an investment that produced a return of 18%. What

is your approximate

annual real rate of return if the rate of inflation was 2% over the year?

A. 18%

B. 2%

C. 16%

D. 15%

Metals and energy currency futures contracts are actively traded on

A. gold.

B. silver.

C. propane.

D. gold and silver.

E. All of the options are correct.

Options sellers who are delta-hedging would most likely

A. sell when markets are falling.

B. buy when markets are rising.

C. sell when markets are falling and buy when markets are rising.

D. sell whether markets are falling or rising.

E. buy whether markets are falling or rising.

Capital asset pricing theory asserts that portfolio returns are best explained by

A. reinvestment risk.

B. specific risk.

C. systematic risk.

D. diversification.

You are considering investing $1,000 in a T-bill that pays 0.05 and a risky portfolio, P,

constructed with two

risky securities, X and Y. The weights of X and Y in P are 0.60 and 0.40, respectively. X

has an expected rate

of return of 0.14 and variance of 0.01, and Y has an expected rate of return of 0.10 and a

variance of 0.0081.

If you want to form a portfolio with an expected rate of return of 0.10, what percentages

of your money must

you invest in the T-bill, X, and Y, respectively, if you keep X and Y in the same

proportions to each other as in

portfolio P?

A. 0.25; 0.45; 0.30

B. 0.19; 0.49; 0.32

C. 0.32; 0.41; 0.27

D. 0.50; 0.30; 0.20

E. Cannot be determined.

The duration of a perpetuity with a yield of 6% is

A. 13.50 years.

B. 12.11 years.

C. 17.67 years.

D. Cannot be determined

A convertible bond has a par value of $1,000 and a current market value of $950. The

current price of the issuing firm’s stock is $22, and the conversion ratio is 40 shares.

The bond’s conversion premium is

A. $40.

B. $70.

C. $190.

D. $200.

To the option holder, put options are worth ______ when the exercise price is higher;

call options are worth______ when the exercise price is higher.

A. more; more

B.more; less

C. less; more

D. less; less

E. It doesn’t matter— they are too risky to be included in a reasonable person’s

portfolio.

Vega is defined as

A. the change in the value of an option for a dollar change in the price of the underlying

asset.

B. the change in the value of the underlying asset for a dollar change in the call price.

C. the percentage change in the value of an option for a 1% change in the value of the

underlying asset.

D. the change in the volatility of the underlying stock price.

E. the sensitivity of an option’s price to changes in volatility.

Basu (1977, 1983) found that firms with high P/E ratios

A. earned higher average returns than firms with low P/E ratios.

B. earned the same average returns as firms with low P/E ratios.

C. earned lower average returns than firms with low P/E ratios.

D. had higher dividend yields than firms with low P/E ratios.

The intrinsic value of an out-of-the-money call option is equal to

A. the call premium.

B. zero.

C. the stock price minus the exercise price.

D. the striking price.

Empirical results regarding betas estimated from historical data indicate that betas

A. are constant over time.

B. are always greater than one.

C. are always near zero.

D. appear to regress toward one over time.

E. are always positive.

If interest rates increase, business investment expenditures are likely to ______, and

consumer durable expenditures are likely to _________.

A. increase; increase

B. increase; decrease

C. decrease; increase

D.-decrease; decrease

E. be unaffected; be unaffected

A call option allows the buyer to

A. sell the underlying asset at the exercise price on or before the expiration date.

B. buy the underlying asset at the exercise price on or before the expiration date.

C. sell the option in the open market prior to expiration.

D. sell the underlying asset at the exercise price on or before the expiration date and sell

the option in the open market prior to expiration.

E. buy the underlying asset at the exercise price on or before the expiration date and sell

the option in the open market prior to expiration.

Which of the following is not a characteristic of a money market instrument?

A. Liquidity

B. Marketability

C. Long maturity

D. Liquidity premium

E. Long maturity and liquidity premium

A coupon bond that pays interest annually has a par value of $1,000, matures in seven

years, and has a yield to maturity of 9.3%. The intrinsic value of the bond today will be

______ if the coupon rate is 8.5%.

A. $712.99

B. $960.14

C. $1,123.01

D. $886.28

E. $1,000.00

Henriksson (1984) found that, on average, betas of funds __________ during market

advances.

A. increased very significantly

B. increased slightly

C. decreased slightly

D. decreased very significantly

E. did not change

If an investment provides a 0.78% return monthly, its effective annual rate is

A. 9.36%.

B. 9.63%.

C. 10.02%.

D. 9.77%.

What happens to an option if the underlying stock has a 2-for-1 split?

A. There is no change in either the exercise price or in the number of options held.

B. The exercise price will adjust through normal market movements; the number of

options will remain the same.

C.The exercise price would become one-half of what it was, and the number of options

held would double.

D. The exercise price would double, and the number of options held would double.

E. There is no standard rule— each corporation has its own policy.

Conventional theories presume that investors ____________, and behavioral finance

presumes that they ____________.

A. are irrational; are irrational

B. are rational; may not be rational

C. are rational; are rational

D. may not be rational; may not be rational

E. may not be rational; are rational

Consider two perfectly negatively correlated risky securities A and B. A has an expected

rate of return of 10%

and a standard deviation of 16%. B has an expected rate of return of 8% and a standard

deviation of 12%.

The risk-free portfolio that can be formed with the two securities will earn a(n) _____

rate of return.

A. 8.5%

B. 9.0%

C. 8.9%

D. 9.9%

Floating-rate bonds are designed to ___________, while convertible bonds are designed

to __________.

A. minimize the holders’interest rate risk; give the investor the ability to share in the

price appreciation of the company’s stock

B. maximize the holders’interest rate risk; give the investor the ability to share in the

price appreciation of the company’s stock

C. minimize the holders’interest rate risk; give the investor the ability to benefit from

interest rate changes

D. maximize the holders’interest rate risk; give investor the ability to share in the profits

of the issuing company

E. None of the options are correct.

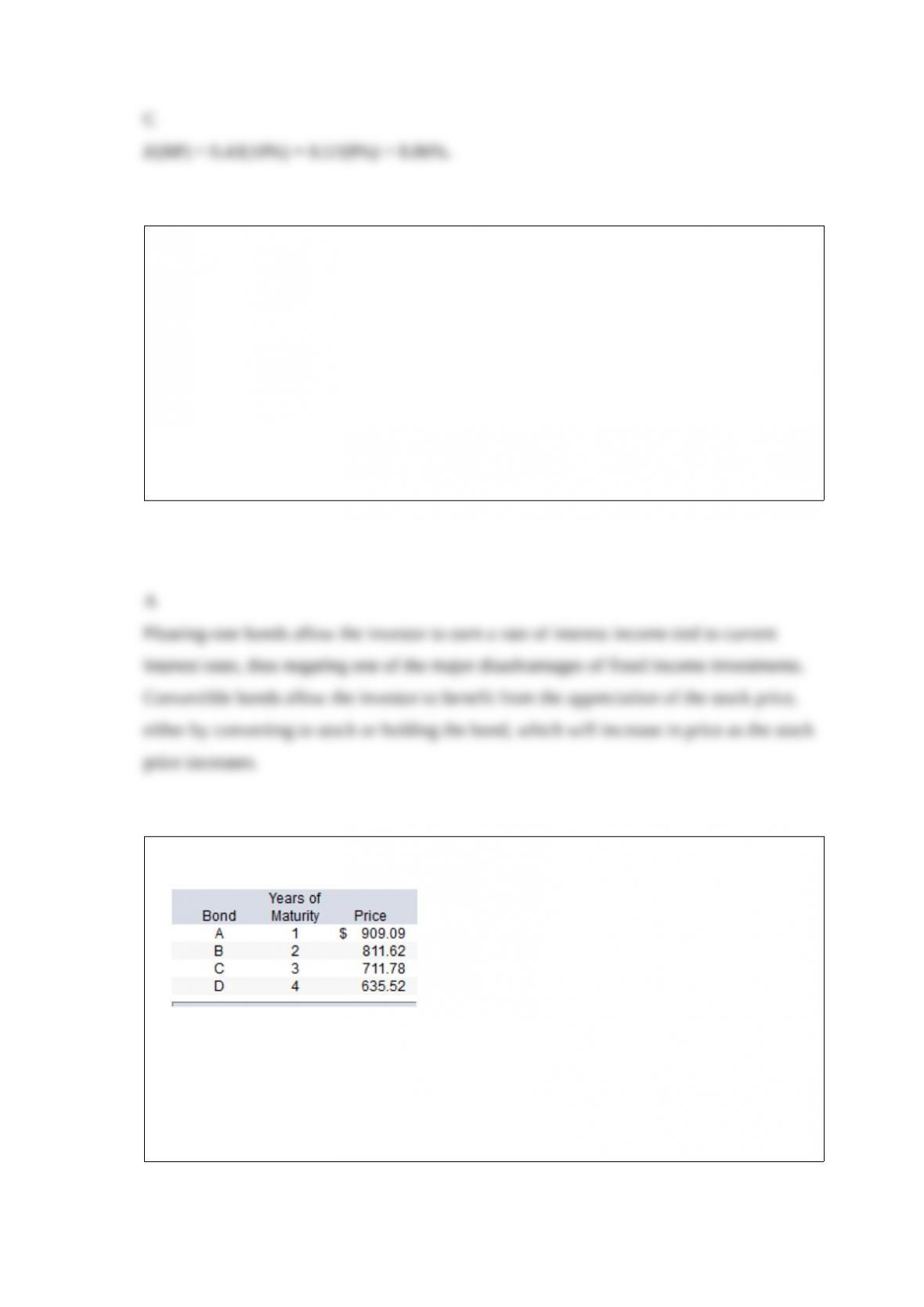

Consider the following $1,000-par-value zero-coupon bonds:

The yield to maturity on bond B is

A. 10%.

B. 11%.

C. 12%.

D. 14%.

E. None of the options are correct.

Economic value added (EVA) is also known as

A. excess capacity.

B. excess income.

C. value of assets.

D. accounting value added.

E. residual income.

Passive portfolio management consists of

A. market timing.

B. security analysis.

C.indexing.

D. market timing and security analysis.

E. None of the options are correct.

Institutional investors will rarely invest in which of these asset classes?

A. Bonds

B. Stocks

C. Cash

D. Real estate

E. Precious metals

When Maurice Kendall examined the patterns of stock returns in 1953, he concluded

that the stock market was __________. Now, these random price movements are

believed to be _________.

A. inefficient; the effect of a well-functioning market

B. efficient; the effect of an inefficient market

C. inefficient; the effect of an inefficient market

D. efficient; the effect of a well-functioning market

E. irrational; even more irrational than before

The Treynor-Black model does not assume that

A. the objective of security analysis is to form an active portfolio of a limited number of

mispriced securities.

B. the cost of less than full diversification comes from the nonsystematic risk of the

mispriced stock.

C.the optimal weight of a mispriced security in the active portfolio is a function of the

degree of mispricing, the

market sensitivity of the security, and its degree of nonsystematic risk.

D. indexing is always optimal.