Which of the following observations about the repricing model is correct? A. Its

information value is limited.

B. It accounts for the problem of rate-insensitive asset and liability runoffs and

prepayments.

C. It accommodates cash flows from off-balance-sheet activities.

D. It helps to determine an FI’s profit exposure to interest rate changes.

E. It considers market value effects of interest rate changes.

Answer:

An investment banker agrees to underwrite an issue of 10 million shares of stock for

Rochester Industries on a best-efforts basis. The investment banker is able to sell 8

million shares for $10.50 per share, and it charges Rochester Industries $0.225 per share

sold.

What is the profit to the investment banker it sells 8 million shares for $9.75 per share?

A. Profit of $1,000,000.

B. Loss of $7,500,000.

C. Profit of $7,000,000.

D. Loss of $7,000,000.

E. Profit of $1,800,000.

Answer:

What should be the one-year forward rate in order to prevent any arbitrage? A.

$0.1944/€.

B. $0.1975/€.

C. $0.2000/€.

D. $0.2025/€.

E. $0.2031/€.

Answer:

Loan participationsA. are riskier than loan assignments.

B. are less risky than loan assignments.

C. are always sold without recourse.

D. are always sold with partial recourse.

E. are made in smaller denominations than are loan assignments.

Answer:

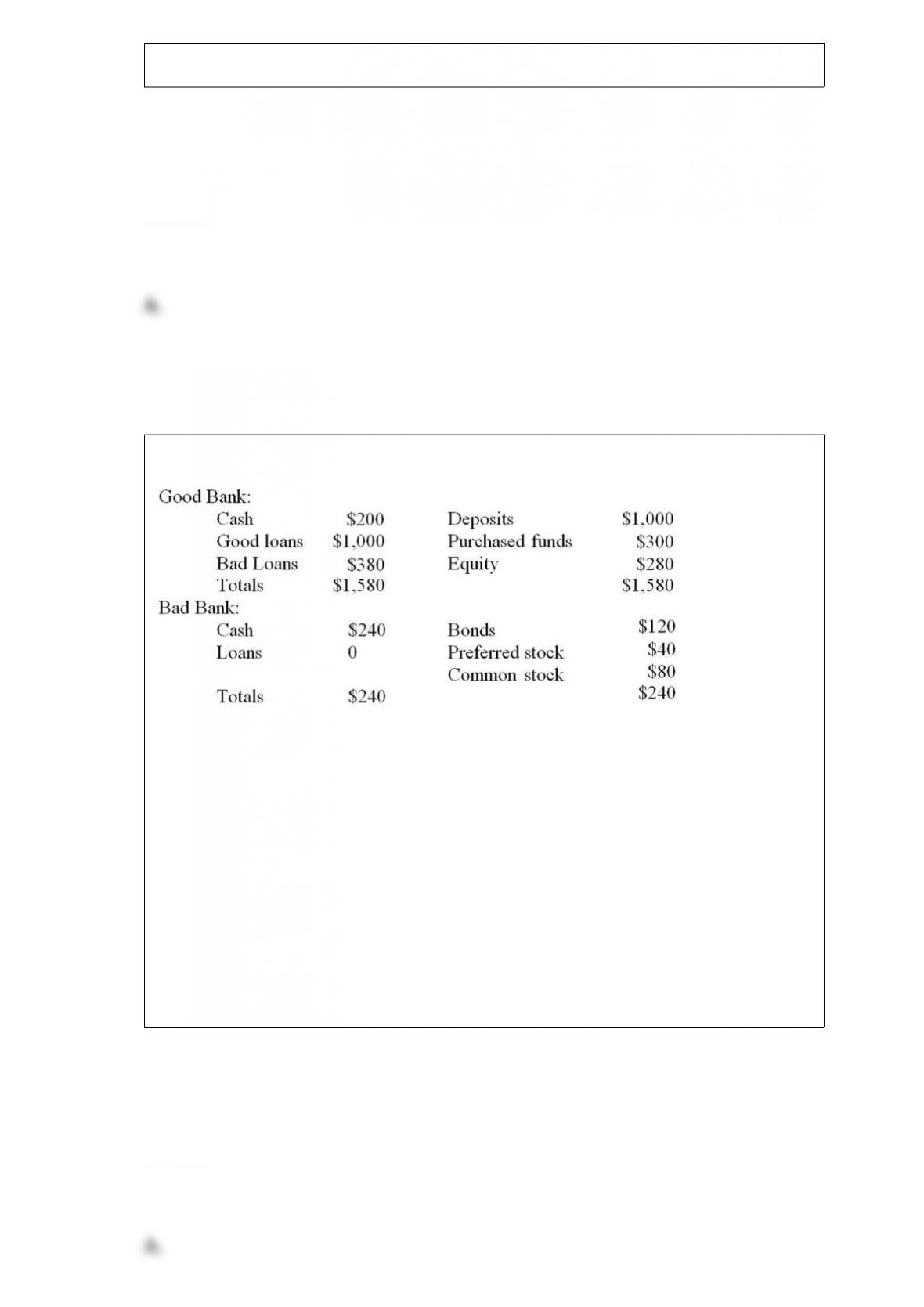

Bad Bank buys the bad loans for $232. The proceeds of the loan sale are used by Good

Bank to pay off purchased funds.

What will be the total assets of Good Bank after the sale of the loans? A. $1,200.

B. $232.

C. $132.

D. $68.

E. $0.

Answer:

State-chartered commercial banks may be regulated by A. the FDIC only.

B. the FDIC and the Federal Reserve System.

C. the Federal Reserve System only.

D. the FDIC, the Federal Reserve System, and the Comptroller of the Currency.

E. the FDIC, the Federal Reserve System, the Comptroller of the Currency, and state

banking commissions.

Answer:

Which of the following is an outcome of a decrease in the reserve requirement ratio? A.

DIs must hold more reserves against the transaction accounts on their balance sheets.

B. DIs are able to lend a smaller percentage of their deposits.

C. Decreased credit availability in the economy.

D. A multiple contraction in deposits and a decrease in the money supply.

E. A multiplier effect on the supply of DI deposits and thus, the money supply.

Answer:

Which of the following refers to mandatory actions that have to be taken by regulators

as a DI’s capital ratio falls. A. Capital forbearance.

B. Prompt corrective action.

C. Risk-based deposit insurance.

D. Too-big-to-fail.

E. Regulatory oversight.

Answer:

Higher uncertainty of losses forces property-casualty firms to A. invest in more

short-term assets than life insurance firms.

B. invest in more long-term assets than life insurance firms.

C. hold a lower percentage of capital and reserves than life insurance firms.

D. invest in riskier equity securities than life insurance firms.

E. conduct more separate accounts business than life insurance firms.

Answer:

Which of the following is an example of a negative duration asset that is valuable as a

portfolio-hedging device for an FI manager when included with regular bonds whose

price-yield curves show the normal inverse relationship. A. PO strip.

B. IO strip.

C. Class B bonds

D. Class Z bonds

E. Class A bonds

Answer:

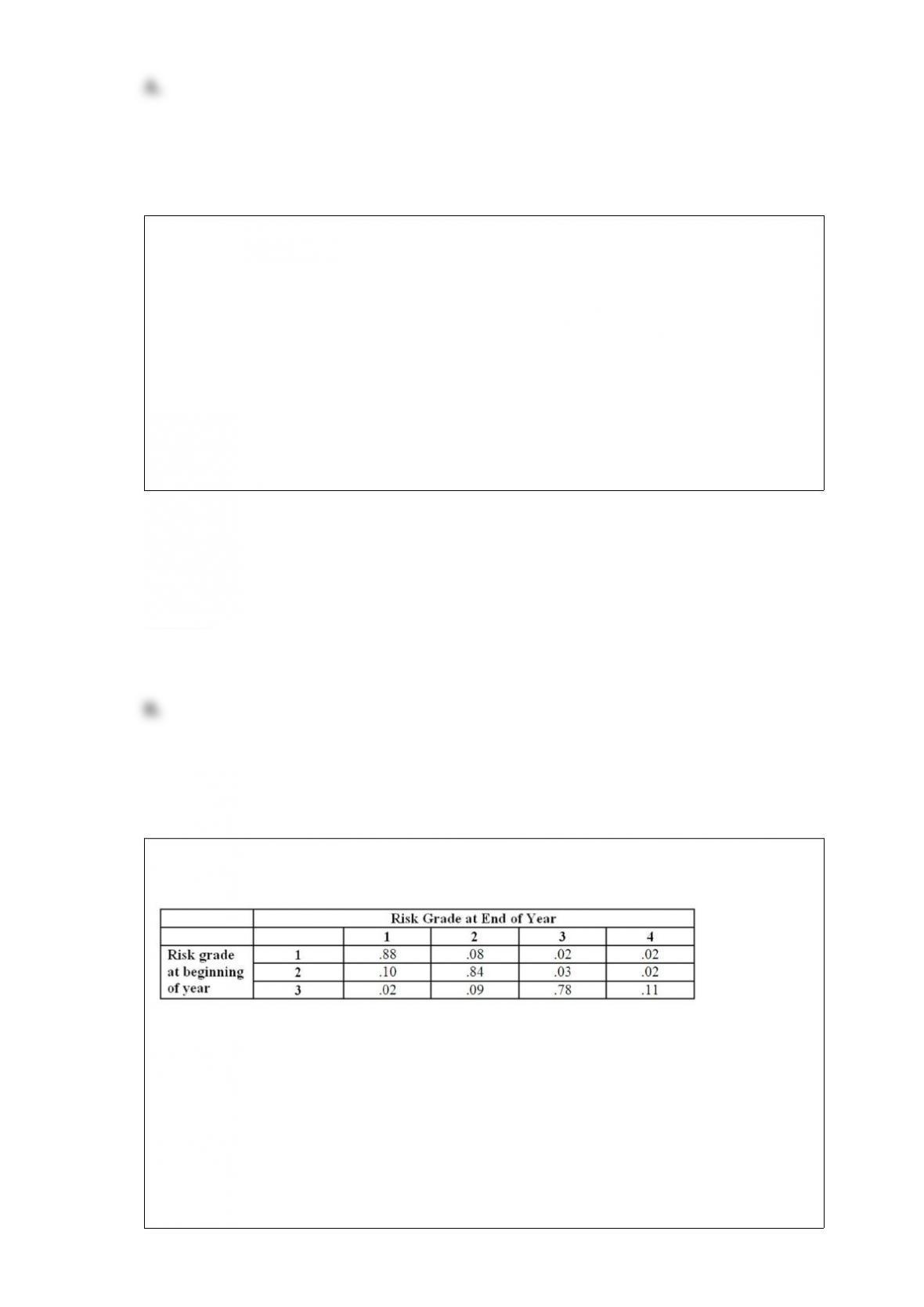

Matrix Bank has compiled the following migration matrix on consumer loans. Which of

the following statements accurately summarizes this data?

A. Ten

percent of grade two loans were upgraded during the year.

B. Grade one loans have a higher probability of downgrade than grades two or three.

C. Grade three loans have a higher probability of upgrade than grade two loans.

D. Grade three loans have a higher probability of downgrade than grade two loans.

E. All of the above.

Answer:

If in one year there is no change in either interest rates or exchange rates, what is the

end-of-year profit or loss of your bank’s cash position? Assume that annual interest is

paid on both the CD and the Canadian bonds on the date of liquidation in exactly one

year. A. Profit of US $20,000.

B. Loss of C $224,000

C. Profit of US $50,000.

D. Profit of C $63,000.

E. Profit of US $313,000.

Answer:

Bank of the Atlantic has liabilities of $4 million with an average maturity of two years

paying interest rates of 4.0 percent annually. It has assets of $5 million with an average

maturity of 5 years earning interest rates of 6.0 percent annually.

What is the bank’s net interest income in dollars in year 3, if it refinances all of its

liabilities at a rate of 8.0 percent? A. -$20,000.

B. -$10,000.

C. -$15,000.

D. +$20,000.

E. +$10,000.

Answer:

High rates of domestic inflation impact the credit scoring model of sovereign country

risk exposure through which of the following variables? A. The debt service ratio.

B. The import ratio.

C. The variance of export revenue.

D. The investment ratio.

E. Domestic money supply growth.

Answer:

If Bank A’s average return on its loan portfolio is lower than that of Bank B’s,A. its

risk-adjusted return is higher than Bank B’s.

B. its risk-adjusted return is lower than Bank B’s.

C. its standard deviation is lower than Bank B’s.

D. its standard deviation is higher than Bank B’s.

E. Answers b and d

Answer:

To be deemed “accredited” and able to invest in a hedge fund, an investor must have A.

a net worth of over $2 million.

B. an annual income of at least $200,000.

C. an annual income of at least $500,000 if married.

D. a net worth of over $4 million.

E. a retirement savings plan and over $1 million in net worth.

Answer:

Choose among the following major banking laws.

A. The McFadden Act of 1927

B. The Glass-Steagall Act of 1933

C. The Depository Institutions Deregulation and Monetary Control Act (DIDMCA) of

1980

D. The Garn-St Germain Depository Institutions Act of 1982

E. The Competitive Equality in Banking Act of 1987

F. The Financial Institutions Reform, Recovery, and Enforcement Act of 1989

G. The Federal Deposit Insurance Corporation Improvement Act (FDICIA) of 1991

H. The Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994

I. Financial Services Modernization Act of 1999

Eliminated restrictions on banks, insurance companies, and securities firms from

entering into each other’s areas of business.

Answer:

The Institutional Investor Index is based onA. spread of the required interest rate on a

country’s debt over LIBOR.

B. a number of economic and political factors weighted according to their relative

importance in determining country risk problems.

C. surveys of the loan officers of major multinational banks.

D. combined economic and political risk on a 10-point (maximum) scale.

E. key economic ratios for each regional grouping.

Answer:

Which function of an FI involves buying primary securities and issuing secondary

securities? A. Brokerage.

B. Asset transformation.

C. Investment research.

D. Self-regulator.

E. Trading.

Answer:

The largest liability on credit unions’ balance sheet as of September 30, 2012 was A.

small time and savings deposits.

B. open-market paper.

C. repurchase agreements.

D. ownership shares.

E. share advances.

Answer:

The risk that many depositors withdraw their funds from an FI at once is A. credit risk.

B. sovereign risk.

C. currency risk.

D. liquidity risk.

E. interest rate risk.

Answer:

Regarding the relative asset size and asset growth rate of mutual fund sectors, A.

long-term funds had more assets at the end of 2012, but short-term funds had grown at a

faster rate since 1980.

B. long-term funds had more assets at the end of 2012, and long-term funds had grown

at a faster rate since 1980.

C. short-term funds had more assets at the end of 2012, but long-term funds had grown

at a faster rate since 1980.

D. short-term funds had more assets at the end of 2012, and short-term funds had

grown at a faster rate since 1980.

E. More than one of the above is correct.

Answer:

National full-line investment and brokerage firmsA. may specialize in providing

service to both retail and corporate customers.

B. usually serve only as discount brokers without offering investment advice.

C. may specialize more in corporate finance with high activity in trading securities.

D. All of the above.

E. Answers A and C only.

Answer:

Swap contracts are actively traded on the A. NYSE.

B. AMEX.

C. CBOE.

D. CFTC.

E. Swaps are not actively traded.

Answer:

These types of funds mix hedge funds and other pooled investment vehicles. A.

Distressed securities funds.

B. Macro funds.

C. Value funds.

D. Opportunistic funds.

E. Fund of funds.

Answer:

When a bank enters into a fixed-floating currency swap, it is exposed to A. both

interest rate and currency exposures.

B. only interest rate exposures.

C. only exchange rate exposure.

D. zero interest rate exposure over the life of the swap.

E. zero interest rate and currency exposure over the life of the swap.

Answer:

What is the reserve to be maintained with fed? A. $38.247 million.

B. $34.419 million.

C. $36.971 million.

D. $35.087 million.

E. $35.695 million.

Answer:

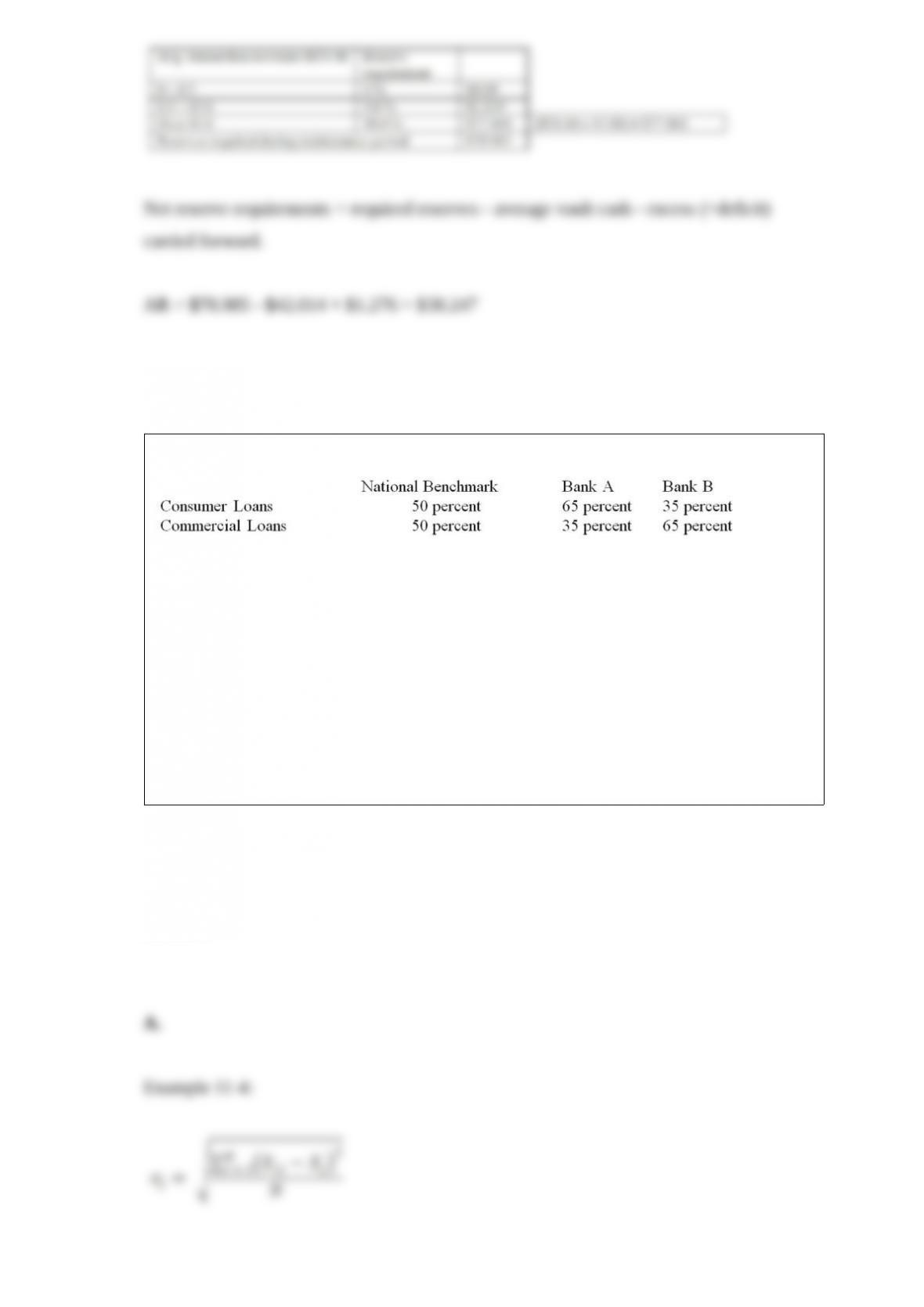

Estimate the standard deviation of Bank A’s asset allocation proportions relative to the

national benchmark. A. 15.00 percent.

B. 21.21 percent.

C. 29.89 percent.

D. 34.32 percent.

E. 40.44 percent.

Answer:

The relationship of this variable with the probability of rescheduling is often disputed.

A. The debt service ratio.

B. The import ratio.

C. The variance of export revenue.

D. The investment ratio.

E. Domestic money supply growth.

Answer:

What is the value of delta for the respective positions of the two currencies in dollars?

A. -$200,000,000 and -$50,000,000.

B. -$21,524 and -$261,930.

C. -$21,524 and -$50,000,000.

D. -$200,000,000 and -$261,640.

E. -$21,524 and -$317,642.

Answer:

Which of the following is NOT a potential causes of liquidity risk for a DI? A. A

decrease in the DI’s stock price caused by market factors.

B. An increase in requests to fund large amounts of loan commitments.

C. A decrease in the availability of short-term borrowed funds.

D. An increase in requests by depositors to withdrawal large amounts of deposits.

E. A decrease in asset prices of securities held in the investment portfolio.

Answer:

Assume that instead of investing in Euro bonds at a fixed rate of 6.5 percent, the FI

invests them in variable rates of LIBOR + 1.5 percent, reset every six months. The

current LIBOR rate is 5 percent. Assume both interest and principal will be reinvested

in six months. Assume the exchange rate remains at €1.75/$ at the end of the year. What

should be the LIBOR rates in six months in order for the bank to earn a 1 percent

spread? A. 5.25 percent.

B. 5.48 percent.

C. 5.76 percent.

D. 5.86 percent.

E. 5.94 percent.

Answer:

Nondepository financial institutions are represented by all of the following EXCEPT

A. insurance companies.

B. mutual funds.

C. finance companies.

D. credit unions.

E. securities firms.

Answer: