1) Which of the following is not true regarding letters of credit?

a. They are issued by banks on behalf of the importer promising to pay the exporter

b. A revocable letter of credit can be cancelled or revoked at any time without prior

notification to the beneficiary

c. They guarantee that the goods shipped are the goods purchased

d. All of the above are true

2) Which of the following is not one of the more common methods used by MNCs to

improve their internal control process?

a. Establishing a centralized database of information

b. Ensuring that all data are reported consistently among subsidiaries

c. Speeding the process by which all departments and all subsidiaries have access to the

data that they need

d. Making executives more accountable for financial statements by personally verifying

their accuracy

e. All of the above are common methods used by MNCs to improve their internal

control process

3) The legal protection of shareholders is the same among countries.

a. True

b. False

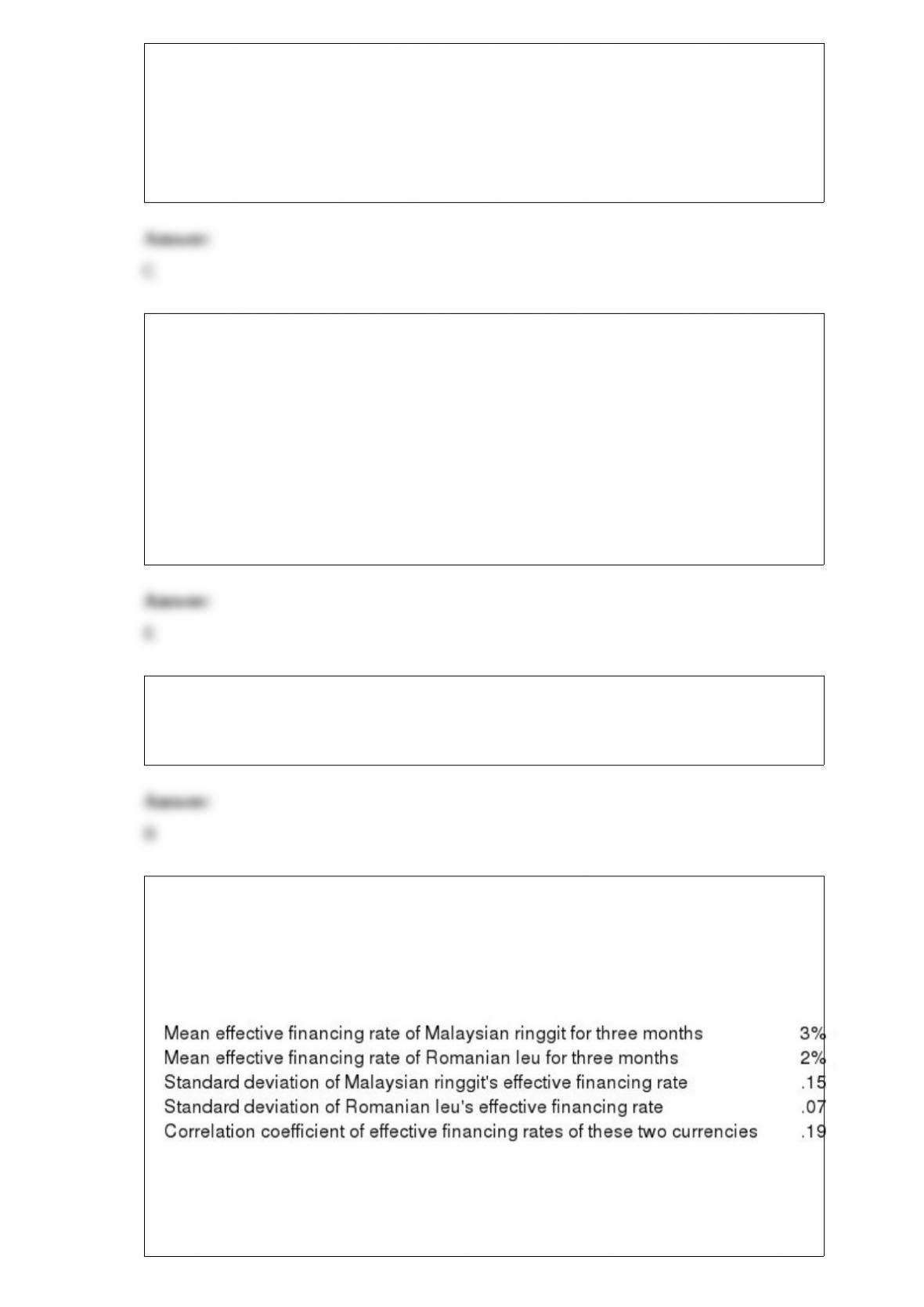

4) Exhibit 21-2

Moore Corporation would like to simultaneously invest in Malaysian ringgit (MYR)

and Romanian leu (ROL) for a three-month period. Moore would like to determine the

expected yield and the variance of a portfolio consisting of 40% ringgit and 60% leu.

Moore has identified the following information:

Refer to Exhibit 21-2. What is the expected effective yield of the portfolio contemplated

by Moore Corporation?

a. 2.50%

b. 2.60%

c. 2.40%

d. none of the above

5) Assume that a yield curve’s shape is caused by liquidity. An MNC may be tempted to

finance with a maturity that is less than the expected life of the project when the yield

curve is:

a. flat

b. inverted

c. upward-sloping

d. downward sloping

6) ____ is not a disadvantage of direct foreign investment.

a. The expense of establishing a foreign subsidiary

b. The uncertainty of inflation and exchange rate movements

c. Political risk

d. All of the above are disadvantages of direct foreign investment

7) According to the text, an MNC’s “global” target capital structure is:

a. always debt-intensive

b. always equity-intensive

c. sometimes different from an MNC’s “local” capital structures (at subsidiaries)

d. none of the above

8) The euro has not been adopted by:

a. Slovenia

b. the U.K

c. Germany

d. France

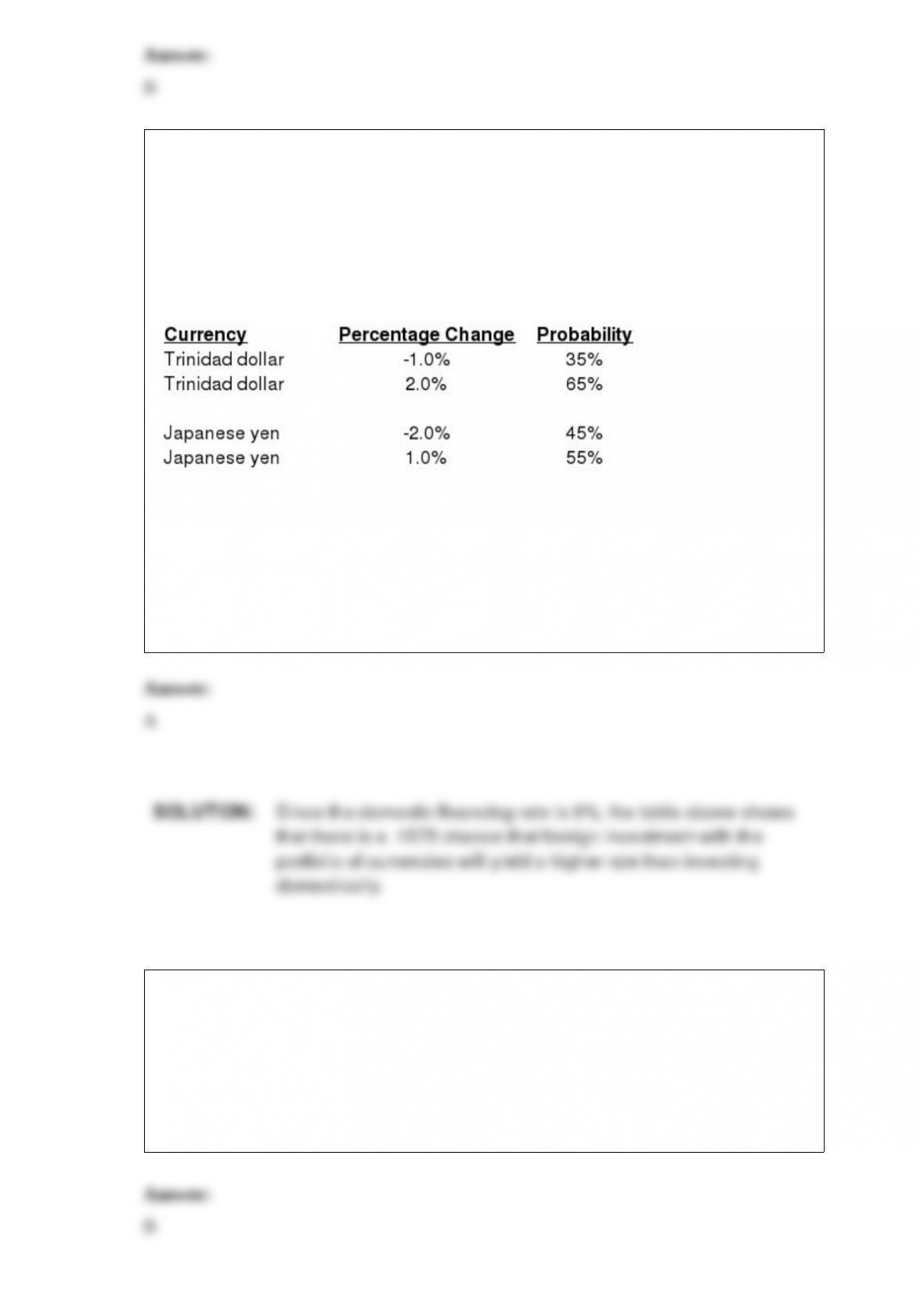

9) Exhibit 21-1

To benefit from the low correlation between the Trinidad dollar and the Japanese yen (),

Sciorra Corporation decides to invest 50% of total funds invested in Trinidad dollars

and the remainder in yen. The domestic yield on a one-year deposit is 8%. The Trinidad

one-year interest rate is 10% and the Japanese one-year interest rate is 7%. Sciorra has

determined the following possible percentage changes in the two individual currencies

as follows:

Refer to Exhibit 21-1. What is the probability that the yield of the two-currency

portfolio is less than the domestic yield?

a. .1575

b. .35

c. .6425

d. 1

e. none of the above

10) An international alliance typically requires a ____ initial outlay than an

international acquisition, and the cash flows to be received will typically be ____ than

the cash flow resulting from an international acquisition.

a. smaller; larger

b. smaller; smaller

c. larger; smaller

d. larger; larger

11) If interest rate parity exists, the attempt to finance with a foreign currency while

covering the position to avoid exchange rate risk will result in an effective financing

rate that is ____ the domestic interest rate.

a. lower than

b. greater than

c. similar to

d. none of the above

12) A U.S. firm could issue bonds denominated in euros and partially hedge against

exchange rate risk by:

a. invoicing its exports in U.S. dollars.

b. requesting that any imports ordered by the firm be invoiced in U.S. dollars.

c. invoicing its exports in euros.

d. requesting that any imports ordered by the firm be invoiced in the currency

denominating the bonds.

13) If the Fed ____ the interest rates when inflationary expectations remain unchanged,

the most likely result is that the value of dollar will ____ and the economy may ____.

a. increases; appreciate; weaken

b. decreases; appreciate; weaken

c. increases; depreciate; strengthen

d. decreases; appreciate; strengthen

14) Futures contracts are standardized with respect to delivery date and the futures price

specified for the settlement date.

a. True

b. False

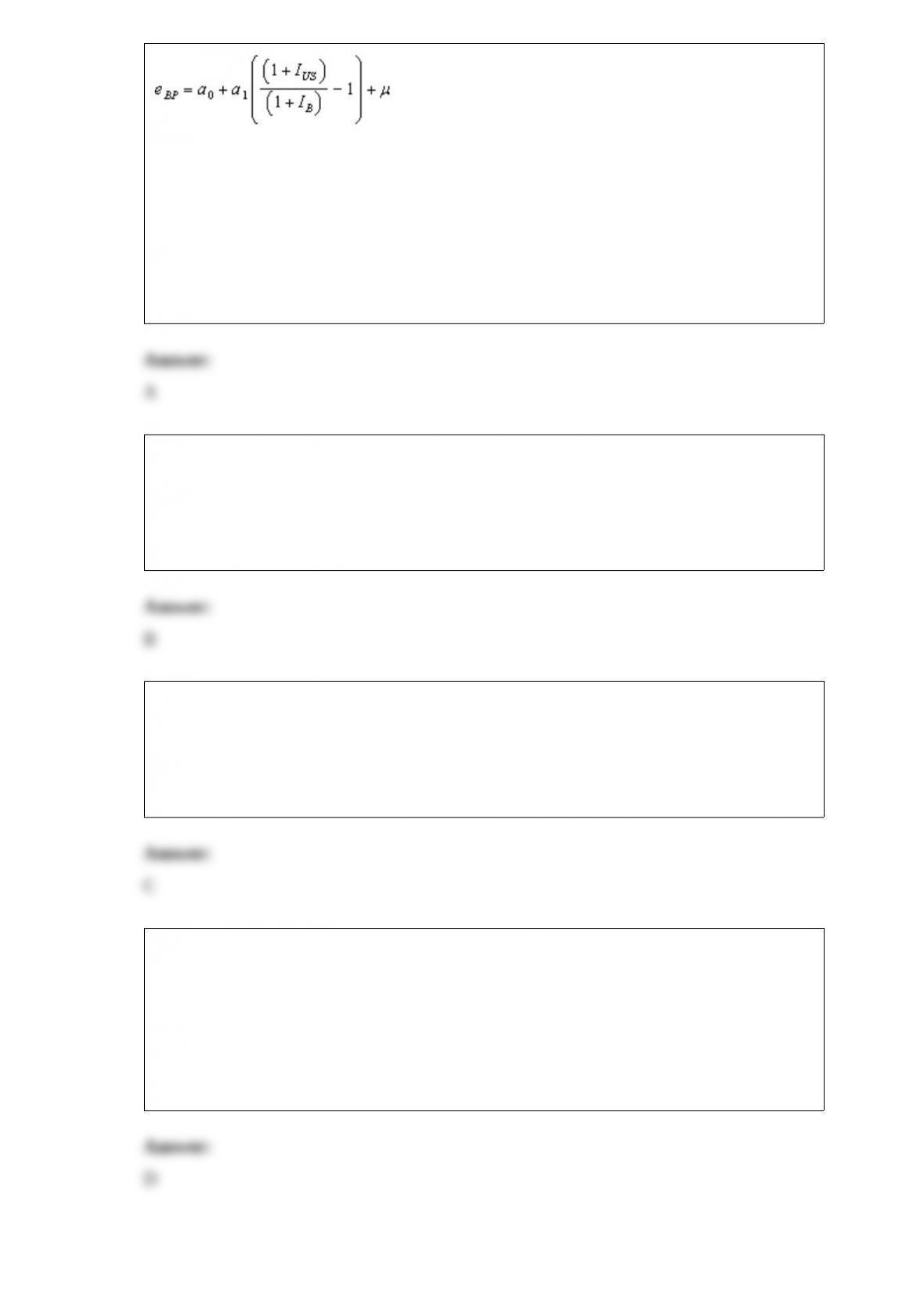

15) The following regression analysis was conducted for the inflation rate information

and exchange rate of the British pound:

Regression results indicate that a0 = 0 and a1 = 1. Therefore:

a. purchasing power parity holds

b. purchasing power parity overestimated the exchange rate change during the period

under examination

c. purchasing power parity underestimated the exchange rate change during the period

under examination

d. purchasing power parity will overestimate the exchange rate change of the British

pound in the future

16) The preferences of corporations and governments to borrow in foreign currencies

and of investors to make short-term investments in foreign currencies resulted in the

creation of the international bond market.

a. True

b. False

17) A ____ provides a summary of freight charges and conveys title to the merchandise.

a. letter of credit

b. banker’s acceptance

c. bill of lading

d. bill of exchange

18) Other things being equal, a blocked funds restriction is more likely to have a

significant adverse effect on a project if the currency of that country is expected to ____

over time, and if the interest rate in that country is relatively ____.

a. appreciate; low

b. appreciate; high

c. depreciate; high

d. depreciate; low

19) If you expect the euro to depreciate, it would be appropriate to ____ for speculative

purposes.

a. buy a euro call and buy a euro put

b. buy a euro call and sell a euro put

c. sell a euro call and sell a euro put

d. sell a euro call and buy a euro put

20) U.S.-based MNCs whose foreign subsidiary generates large earnings may be able to

offset exposure to exchange rate risk by issuing bonds denominated in the subsidiary’s

local currency.

a. True

b. False

21) If movements of two currencies with low interest rates are highly negatively

correlated, then financing in a portfolio of currencies would not be very beneficial. That

is, financing with such a portfolio would not be very different from financing with a

single foreign currency.

a. True

b. False

22) Assume that the U.S. interest rate is 11 percent, while Australia’s one-year interest

rate is 12 percent. Assume interest rate parity holds. If the one-year forward rate of the

Australian dollar was used to forecast the future spot rate, the forecast would reflect an

expectation of:

a. depreciation in the Australian dollar’s value over the next year

b. appreciation in the Australian dollar’s value over the next year

c. no change in the Australian dollar’s value over the next year

d. information on future interest rates is needed to answer this question

23) Assume that a U.S. firm considers investing in British one-year Treasury securities.

The interest rate on these securities is 12%, while the interest rate on the same securities

in the U.S. is 10%. The firm believes that today’s spot rate is an appropriate forecast for

the spot rate of the pound in one year. Based on this information, the effective yield on

British securities from the U.S. firm’s perspective is:

a. equal to the U.S. interest rate

b. equal to the British interest rate

c. lower than the U.S. interest rate

d. higher than the British interest rate

e. lower than the British interest rate, but higher than the U.S. interest rate

24) The degree of volatility of financing with a currency portfolio depends on only the

standard deviations of effective financing rates of the individual currencies within the

portfolio.

a. True

b. False

25) A centralized management style, where major decisions about a foreign subsidiary

are made by the parent company, results in an increase in agency costs.

a. True

b. False

26) Campbell Company has a subsidiary located in Jamaica. The subsidiary has

generated losses for the last five years and is expected to generate losses for the next ten

years. Campbell is reluctant to divest of this subsidiary, however. Given this

information, Campbell would ____ from a(n) ____ of the Jamaican dollar.

a. benefit; appreciation

b. benefit; depreciation

c. not benefit; appreciation

d. not benefit; depreciation

e. B and C

27) Assume Countries A, B, and C produce goods that are substitutes of each other and

that these countries engage in trade with each other. Assume that Country A’s currency

floats against Country B’s currency, and that Country C’s currency is pegged to B’s. If

A’s currency depreciates against B, then A’s exports to C should ____, and A’s imports

from C should ____.

a. decrease; increase

b. decrease; decrease

c. increase; decrease

d. increase; increase

28) If an actual put option premium is less than what is suggested by the put-call parity

relationship, arbitrage can be conducted.

a. True

b. False

29) The lower a project’s beta, the ____ is the project’s ____ risk.

a. lower; systematic

b. lower; unsystematic

c. higher; systematic

d. higher; unsystematic

30) Under prepayment, the exporter will not ship the goods until the buyer has remitted

payment to the exporter.

a. True

b. False

31) If the foreign exchange market is ____ efficient, then historical and current

exchange rate information is not useful for forecasting exchange rate movements.

a. weak-form

b. semistrong-form

c. strong form

d. all of the above

32) If a U.S. firm sets up a plant in Mexico to benefit from low cost labor, it will likely

have a comparative advantage over other firms in Mexico that sell the same product.

a. True

b. False

33) All European countries now use the euro as their currency.

a. True

b. False

34) Which of the following theories suggests that the percentage change in spot

exchange rate of a currency should be equal to the inflation differential between two

countries?

a. purchasing power parity (PPP)

b. triangular arbitrage

c. international Fisher effect (IFE)

d. interest rate parity (IRP)

35) If a country experiences an increase in interest rates relative to U.S. interest rates,

the inflow of U.S. funds to purchase its securities should ____, the outflow of its funds

to purchase U.S. securities should ____, and there is ____ pressure on its currency’s

equilibrium value.

a. increase; decrease; downward

b. decrease; increase; upward

c. increase; decrease; upward

d. decrease; increase; downward

e. increase; increase; upward

36) The existence of imperfect markets has prevented the internationalization of

financial markets.

a. True

b. False

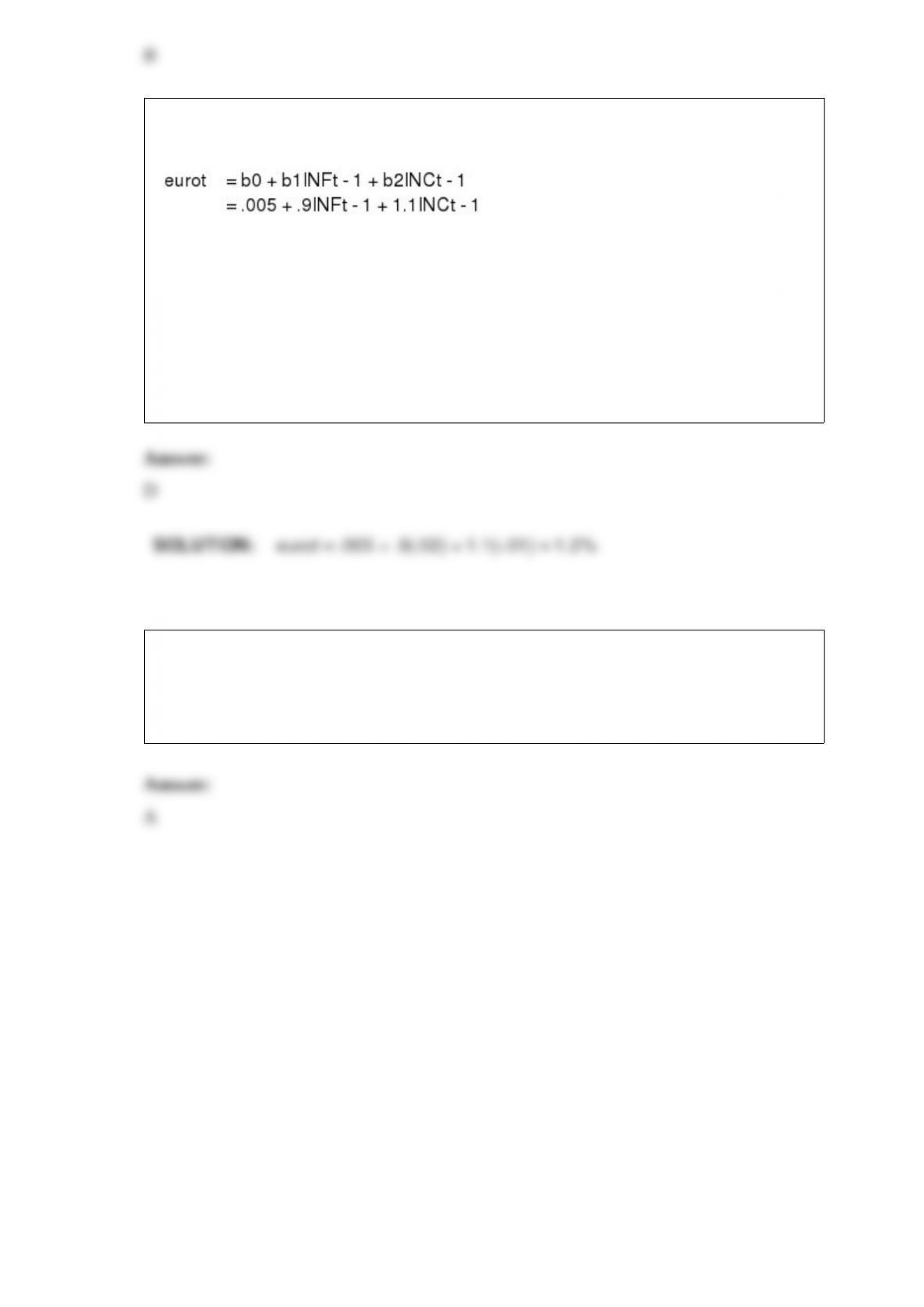

37) Sulsa Inc. uses fundamental forecasting. Using regression analysis, it has

determined the following equation for the euro:

The most recent quarterly percentage change in the inflation differential between the

U.S. and Europe was 2 percent, while the most recent quarterly percentage change in

the income growth differential between the U.S. and Europe was -1 percent. Based on

this information, the forecast for the euro is a(n) ____ of ____%.

a. appreciation; 3.4

b. depreciation; 3.4

c. appreciation; 0.7

d. appreciation; 1.2

38) Country differences, such as differences in the risk-free interest rate and differences

in risk premiums across countries, can cause the cost of capital to vary across countries.

a. True

b. False