The buyer must pay the shipping costs.

Match the terms with the descriptions related to merchandise sales and purchases.

a. Transportation-in e. Cost of goods available for sale

b. Perpetual inventory system f. Periodic inventory system

c. Net purchases g. FOB shipping point

d. FOB destination h. Delivery expense

If a corporation repurchases 500 shares of its previously-issued common stock for

$5,000 and then reissues it for $4,000, which of the following statements is true

regarding the difference in the amounts of the repurchase and reissuance?

a. It is reported as a loss on the sale of treasury stock.

b. It is reported as a gain on the sale of treasury stock.

c. It is a decrease in stockholders’ equity.

d. It is an increase in stockholders’ equity.

Current Assets / Current Liabilities Match each of the ratios named with the proper

formula for computation.

a. Current Ratio

b. Quick Ratio

c. Cash Ratio

d. Operating Cash Flow Ratio

The bookkeeper made the following errors while recording transactions for the period:

A) A purchase of equipment for $450 cash was recorded as a debit to Equipment for

$540 and a credit to Cash for $540.

B) The sale of services for cash in the amount of $4,134 was recorded as a debit to Cash

for $4,134 and a credit to Service Revenue for $4,314.

C) A purchase of supplies for $200 cash was recorded correctly in the journal but was

omitted from the general ledger.

D) The sale of services for credit in the amount of $3,800 was recorded correctly in the

journal but was posted twice to the general ledger.

E) $5,500 cash paid for salaries was recorded in the journal as a $5,500 debit to Cash

and a $5,500 credit to Salaries Expense. Indicate whether or not the debit and credit

columns of the trial balance will be equal after recording each of these erroneous

entries. Then identify the account(s) that will be misstated as a result of these errors and

the direction of the misstatement (i.e., understatement or overstatement).

On January 1, 2013, Kaiser Permanente issued $2,000,000 of 8% bonds at par. These

bonds are due in 10 years with interest payable semi-annually on June 30 and

December 31. What is the amount of the interest expense in 2013 assuming the use of

the effective interest amortization method?

a. $16,000

b. $160,000

c. $1,600,000

d. $2,000,000

A transaction that brings together two or more previously separate entities to form a

single legal entity is called

a. stock acquisition.

b. debt acquisition.

c. asset acquisition.

d. business acquisition.

The practice of adjusting the market value of securities that are accounted for using the

fair value method is referred to as

a. consolidation.

b. marking-to-market.

c. passive investing.

d. segregation of investments.

A credit means

a. the event had a favorable impact on the entity’s financial statements.

b. the event had an unfavorable impact on the entity’s financial statements.

c. the event had an effect on the right side of the T-account.

d. the event had the effect of increasing the account balance.

A company rented office space to a tenant on January 1 and received a total of $90,000

for the first nine months of rent. The amount was recorded as Rent Collected in

Advance when received. Adjustments are recorded only at the end of every quarter.

What effect does the adjustment at March 31 have on the company’s net income for the

quarter ending March 31?

a. Increase by $90,000

b. Decrease by $60,000

c. Decrease by $30,000

d. Increase by $30,000

The company’s labor rate agree to the last contract.

Provided is a list of important users of accounting information. Also provided are

descriptions of a major need for accounting information that may be experienced by the

various users. Identify the one user group that is most likely to have the need described.

(Choices may be used more than once.)

a. Investors

b. Management

c. Supplier

d. Banker

e. Government

f. Employees

g. Labor Union

h. Investors and Banker

i. Supplier and Banker

This debt, evidenced by a formal agreement or contract to repay, is frequently issued in

exchange for a noncash asset such as equipment. Match these terms with their

definitions.

a. Callable bonds f. Mortgage bonds

b. Capital lease g. Notes payable

c. Convertible bonds h. Operating lease

d. Debenture bonds i. Secured bonds

e. Junk bonds

A company whose fiscal year ends December 31, has a weekly payroll of $100,000.

Employees work 5 days per week, Monday through Friday and payday is every Friday.

How much wages expense will be recorded on the Friday, January 3 payday?

a. $0

b. $40,000

c. $60,000

d. $100,000

Each of the following documents is used in the control of cash receipts except

a. NSF checks.

b. outstanding checks.

c. bank deposit slips.

d. bank credit memos.

Which one of the following is not a proper method of recognizing assets as expenses in

a particular accounting period?

a. Customers’ account balances in accounts receivable are assigned to expense in the

period in which each customer pays.

b. Prepaid insurance is assigned to expense as the insurance expires.

c. A building is depreciated and its cost is assigned to the current and future accounting

periods in which the building is expected to be used.

d. Merchandise inventory is assigned to cost of goods sold in the period the goods are

sold.

For a merchandising company, the cost of goods sold is subtracted from net sales to

arrive at gross profit.

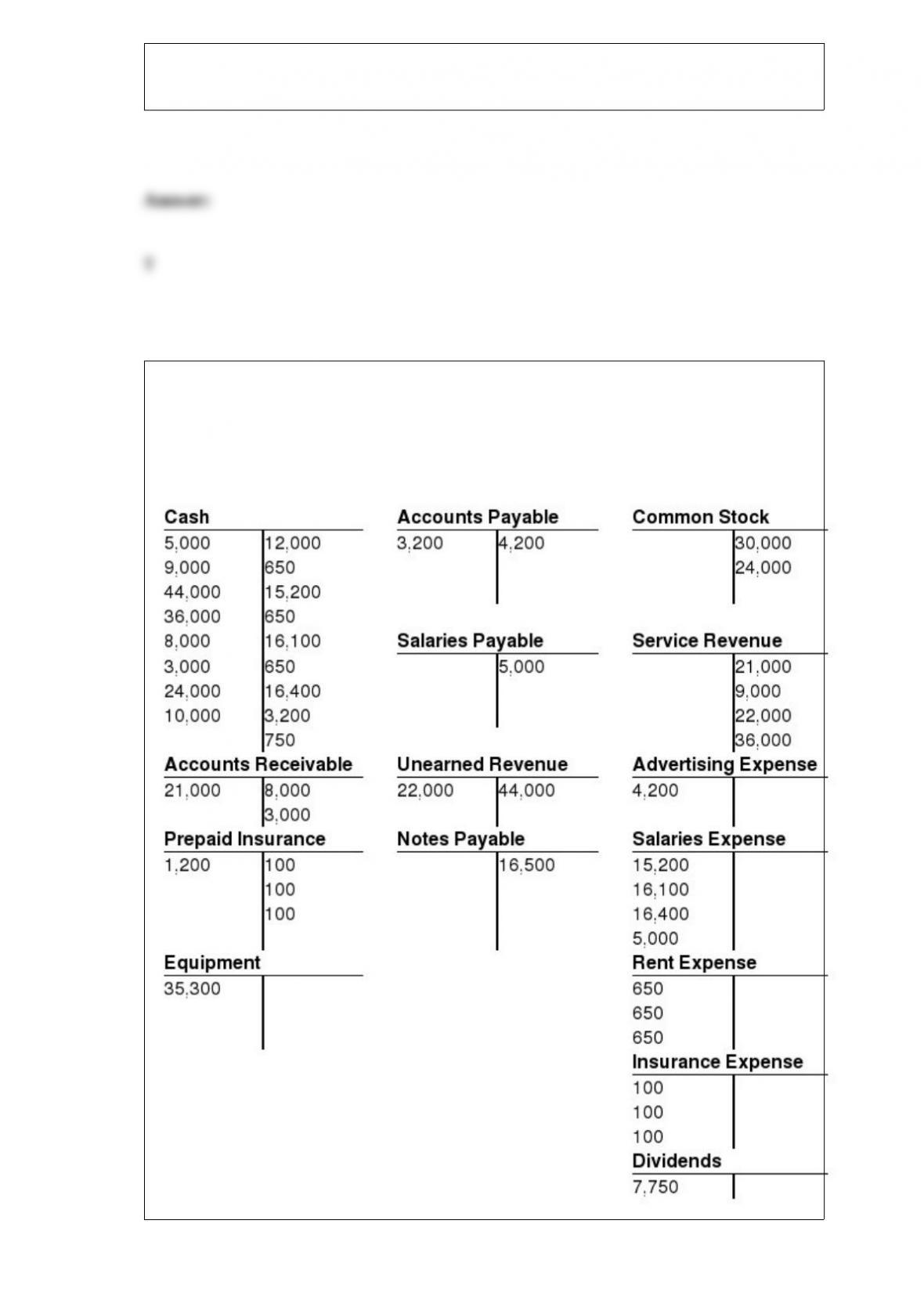

The T-accounts presented below are taken from the general ledger of Health Force

Corporation on March 31, 2013. Determine the balance of each account and present

them in proper trial balance format.

When making lending decisions, lenders generally are not interested in the company’s

operating assets.

Income statement accounts have normal credit balances.