You own $75,000 worth of stock, and you are worried the price may fall by year-end in

6 months. You are considering using either puts or calls to hedge this position. Given

this, which of the following statements is (are) correct?

I. One way to hedge your position would be to buy puts.

II. One way to hedge your position would be to write calls.

III. If major stock price declines are likely, hedging with puts is probably better than

hedging with short calls.

A. I only

B. II only

C. I and III only

D. I, II, and III

All other things equal, a bond’s duration is _________.

A. higher when the yield to maturity is higher

B. lower when the yield to maturity is higher

C. the same at all yield rates

D. indeterminable when the yield to maturity is high

Harry Markowitz is best known for his Nobel Prize-winning work on _____________.

A. strategies for active securities trading

B. techniques used to identify efficient portfolios of risky assets

C. techniques used to measure the systematic risk of securities

D. techniques used in valuing securities options

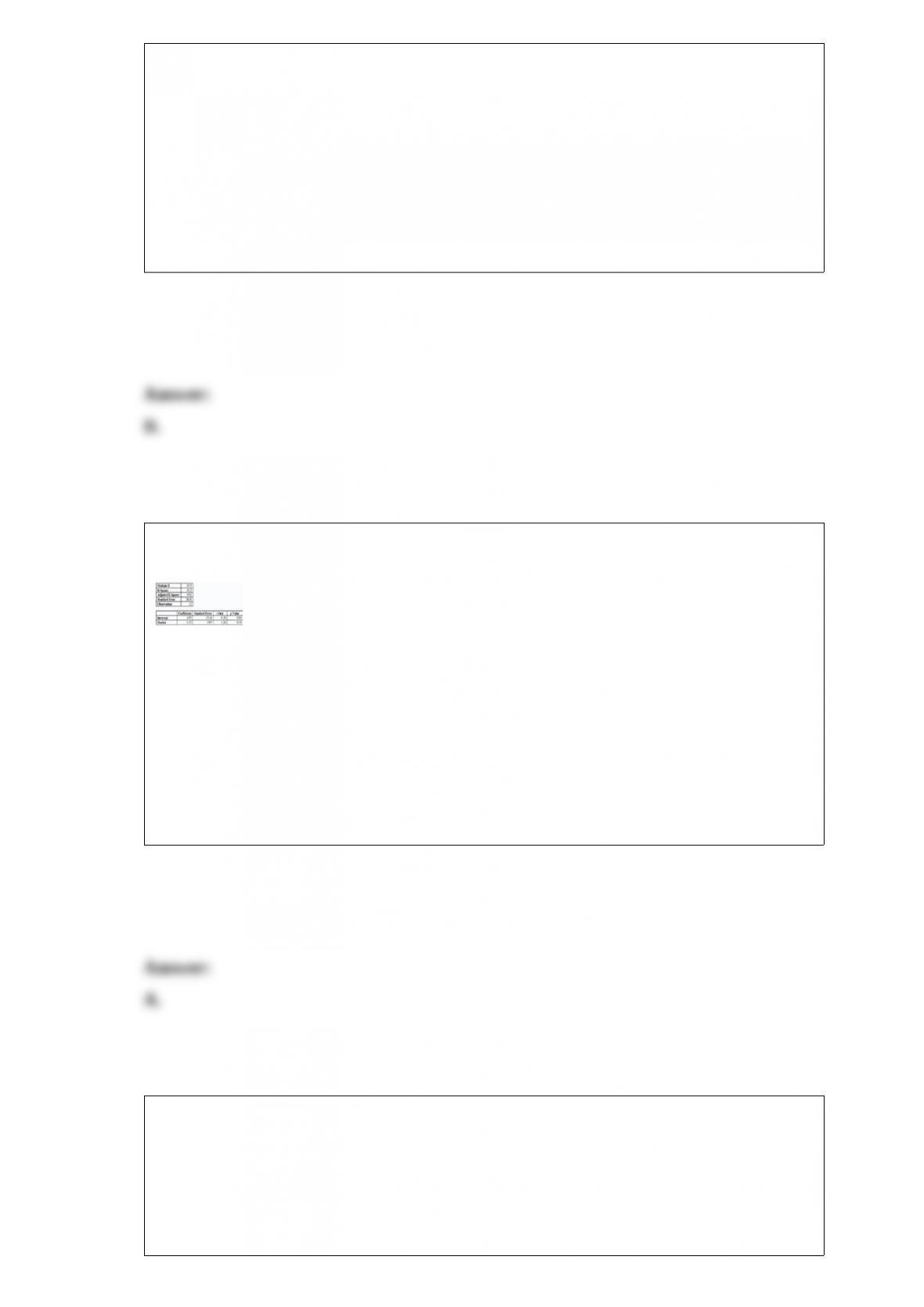

_______________ % of the variance is explained by this regression.

A. 12

B. 35

C. 4.05

D. 80

All else the same, an American-style option will be ______ valuable than a ______

style option.

A. more; European-

B. less; European-

C. more; Canadian-

D. less; Canadian-

When computing the bank discount yield, you would use ____ days in the year.

A. 260

B. 360

C. 365

D. 366

On January 1, you sold one April S&P 500 Index futures contract at a futures price of

1,300. If the April futures price is 1,250 on February 1, your profit would be

__________ if you close your position. (The contract multiplier is 250.)

A. -$12,500

B. -$15,000

C. $15,000

D. $12,500

The stock price of Bravo Corp. is currently $100. The stock price a year from now will

be either $160 or $60 with equal probabilities. The interest rate at which investors

invest in riskless assets is 6%. Using the binomial OPM, the value of a put option with

an exercise price of $135 and an expiration date 1 year from now should be worth

__________ today.

A. $34.09

B. $37.50

C. $38.21

D. $45.45

The goal of supply-side policies is to _______.

A. increase government involvement in the economy

B. create an environment where workers and owners of capital have the maximum

incentive and ability to produce and develop goods

C. maximize tax revenues of the government

D. focus more on wealth redistribution policies

Which of the following is a correct expression concerning the formula for the standard

deviation of returns of a two-asset portfolio where the correlation coefficient is

positive?

A. σ2rp < (W1

2σ1

2 + W2

2σ2

2)

B. σ2rp = (W1

2σ1

2 + W2

2σ2

2)

C. σ2rp = (W1

2σ1

2 – W2

2σ2

2)

D. σ2rp > (W1

2σ1

2 + W2

2σ2

2)

The yield to maturity of a 10-year zero-coupon bond with a par value of $1,000 and a

market price of $625 is _____.

A. 4.8%

B. 6.1%

C. .%

D. 10.4%

The possibility that you are too conservative and your money doesn’t grow fast enough

to keep pace with inflation is called ________.

A. purchasing power risk

B. liquidity risk

C. timing risk

D. market risk

A bond with a 9-year duration is worth $1,080, and its yield to maturity is 8%. If the

yield to maturity falls to 7.84%, you would predict that the new value of the bond will

be approximately _________.

A. $1,035

B. $1,036

C. $1,094

D. $1,124

Which of the following statements is false?

A. Bond prices and yields are inversely related.

B. An increase in a bond’s YTM results in a smaller price change than a decrease in

yield of equal magnitude.

C. Prices of short-term bonds tend to be more sensitive to interest rate changes than

prices of long-term bonds.

D. Interest rate risk is inversely related to the bond’s coupon rate.

Which of the following is not a true statement regarding municipal bonds?

A. A municipal bond is a debt obligation issued by state or local governments.

B. A municipal bond is a debt obligation issued by the federal government.

C. The interest income from a municipal bond is exempt from federal income taxation.

D. The interest income from a municipal bond is exempt from state and local taxation in

the issuing state.

A 1-year gold futures contract is selling for $1,645. Spot gold prices are $1,592 and the

1-year risk-free rate is 3%. Based on the above data, which of the following set of

transactions will yield positive riskless arbitrage profits?

A. Buy gold in the spot with borrowed money, and sell the futures contract.

B. Buy the futures contract, and sell the gold spot and invest the money earned.

C. Buy gold spot with borrowed money, and buy the futures contract.

D. Buy the futures contract, and buy the gold spot using borrowed money.

Assume that the Federal Reserve increases the money supply. This will cause:

I. Interest rates to decrease

II. Consumption and investment to decrease

III. Inflation to fall

A. I only

B. I and II only

C. II and III only

D. I, II, and III

Bill and Shelly are friends. Bill invests in a portfolio of hot stocks that almost all his

friends are invested in. Shelly invests in a portfolio that is totally different from the

portfolios of all her friends. Both Bill’s and Shelly’s stocks fall 15%. According to regret

theory,

_________________________________________.

A. Bill will have more regret over the loss than Shelly

B. Shelly will have more regret over the loss than Bill

C. Bill and Shelly will have equal regret over their losses

D. Bill’s and Shelly’s risk aversion will increase in the future

If the interest rate on debt is higher than the ROA, then a firm’s ROE will _________.

A. decrease

B. increase

C. not change

D. change but in an indeterminable manner

An investor pays $989.40 for a bond. The bond has an annual coupon rate of 4.8%.

What is the current yield on this bond?

A. 4.8%

B. 4.85%

C. 9.6%

D. 9.%

_______ is a life insurance policy that will provide a death benefit only and has no

savings plan.

A. Term life

B. Whole life

C. Variable life

D. Universal life

You buy an 8-year $1,000 par value bond today that has a 6% yield and a 6% annual

payment coupon. In 1 year promised yields have risen to %. Your 1-year holding-period

return was ___.

A. .61%

B. -5.39%

C. 1.28%

D. -3.25%

Which one of the following is not likely to be subject to adverse selection?

A. Health insurance providers

B. Lifetime annuity providers

C. Life insurance providers

D.

Cost of goods sold refers to ___________.

A. direct costs attributable to producing the product sold by the firm

B. salaries, advertising, and selling expenses

C. payments to the firm’s creditors

D. payments to federal and local governments

The market share held by the NYSE Arca system in February 2011 was approximately

____.

A. 65%

B. 45%

C. 25%

D. 10%

An example of a real asset is:

I. A college education

II. Customer goodwill

III. A patent

A. I only

B. II only

C. I and III only

D. I, II, and III

Which one of the following is probably the most direct and immediate way to stimulate

or slow the economy, although it is not very useful for fine-tuning economic

performance?

A. fiscal policy

B. monetary policy

C. supply-side policy

D. rising minimum wages

In the Black-Scholes model, as the stock’s price increases, the values of N(d1) and N(d2)

will _______ for a call and

_______ for a put option.

A. increase; decrease

B. increase; increase

C. decrease; increase

D. decrease; decrease

The price of a stock is $38 at the beginning of the year and $41 at the end of the year. If

the stock paid a $2.50 dividend, what is the holding-period return for the year?

A. 6.58%

B. 8.86%

C. 14.47%

D. 18.66%

One can profit from an arbitrage opportunity by

A. taking a long position in the cheaper market and a short position in the expensive

market.

B. taking a short position in the cheaper market and a long position in the expensive

market.

C. taking a long position in both markets.

D. taking a short position in both markets .

A put option with several months until expiration has a strike price of $55 when the

stock price is $50. The option has _____

intrinsic value and _____ time value.

A. negative; positive

B. positive; positive

C. zero; zero

D. zero; positive

The Black-Scholes option-pricing formula was developed for __________.

A. American options

B. European options

C. Tokyo options

D. out-of-the-money options

An investor can design a risky portfolio based on two stocks, A and B. Stock A has an

expected return of 18% and a standard deviation of return of 20%. Stock B has an

expected return of 14% and a standard deviation of return of 5%. The correlation

coefficient between the returns of A and B is .50. The risk-free rate of return is 10%.

The proportion of the optimal risky portfolio that should be invested in stock A is

_________.

A. 0%

B. 40%

C. 60%

D. 100%