__________ are examples of financial intermediaries.

A. Commercial banks

B. Insurance companies

C. Investment companies

D. All of the options

______ are mutual funds that vary the proportions of funds invested in particular

market sectors according to the fund manager’s forecast of the performance of that

market sector.

A. Asset allocation funds

B. Balanced funds

C. Index funds

D. Income funds

The value of a listed call option on a stock is lower when:

I. The exercise price is higher.

II. The contract approaches maturity.

III. The stock decreases in value.

IV. A stock split occurs.

A. II, III, and IV only

B. I, III, and IV only

C. I, II, and III only

D. I, II, III, and IV

A perpetuity pays $100 each and every year forever. The duration of this perpetuity will

be __________ if its yield is 9%.

A. 7

B. 9

C. 9.39

D. 12.11

What would be the profit or loss per share of stock to an investor who bought an

October expiration Apple call option with an exercise price of $130 if Apple closed on

the expiration date at $120? Assume the option premium was $3.00.

A. $0

B. $3.00 gain

C. $3.00 loss

D. $7.00 gain

A country has a PRS political risk rating of 75, a financial score of 40, and an economic

score of 35. The country’s composite rating is _________.

A. 75

B. 50

C. 40

D. 35

The fact that the exchange is the counterparty to every futures contract issued is

important because it eliminates _________ risk.

A. market

B. credit

C. interest rate

D. basis

Assuming positive basis and negligible borrowing cost, which of the following

transactions could yield positive arbitrage profits if pursued by a hedge fund?

A. Buy gold in the spot market, and sell the futures contract.

B. Buy the futures contract, and sell the gold spot and invest the money earned.

C. Buy gold spot with borrowed money, and buy the futures contract.

D. Buy the futures contract, and buy the gold spot using borrowed money.

An underpriced stock provides an expected return that is ____________ the required

return based on the capital asset pricing model (CAPM).

A. less than

B. equal to

C. greater than

D. greater than or equal to

Fama and French claim that after controlling for firm size and the ratio of the firm’s

book value to market value, beta is:

I. Highly significant in predicting future stock returns

II. Relatively useless in predicting future stock returns

III. A good predictor of the firm’s specific risk

A. I only

B. II only

C. I and III only

D. I, II, and III

Consider the CAPM. The risk-free rate is 6%, and the expected return on the market is

18%. What is the expected return on a stock with a beta of 1.3?

A. 6%

B. 15.6%

C. 18%

D. 21.6%

You are convinced that a stock’s price will move by at least 15% over the next 3

months. You are not sure which way the price will move, but you believe that the results

of a patent hearing are definitely going to have a major effect on the stock price. You

are somewhat more bullish than bearish however. Which one of the following options

strategies best fits this scenario?

A. buy a strip.

B. buy a strap.

C. buy a straddle.

D. write a straddle.

Which one of the following is a false statement regarding NYSE specialists?

A. On a stock exchange most buy or sell orders are executed via an electronic system

rather than through specialists.

B. Specialists cannot trade for their own accounts.

C. Specialists maintain limit order books, which contain the outstanding unexecuted

limit orders.

D. Specialists stand ready to trade at narrower bid-ask spreads in cases where the spread

has become too wide.

The Stone Harbor Fund is a closed-end investment company with a portfolio currently

worth $300 million. It has liabilities of $5 million and 9 million shares outstanding. If

the fund sells for $30 a share, what is its premium or discount as a percent of NAV?

A. 9.26% premium

B. 8.47% premium

C. 9.26% discount

D. 8.47% discount

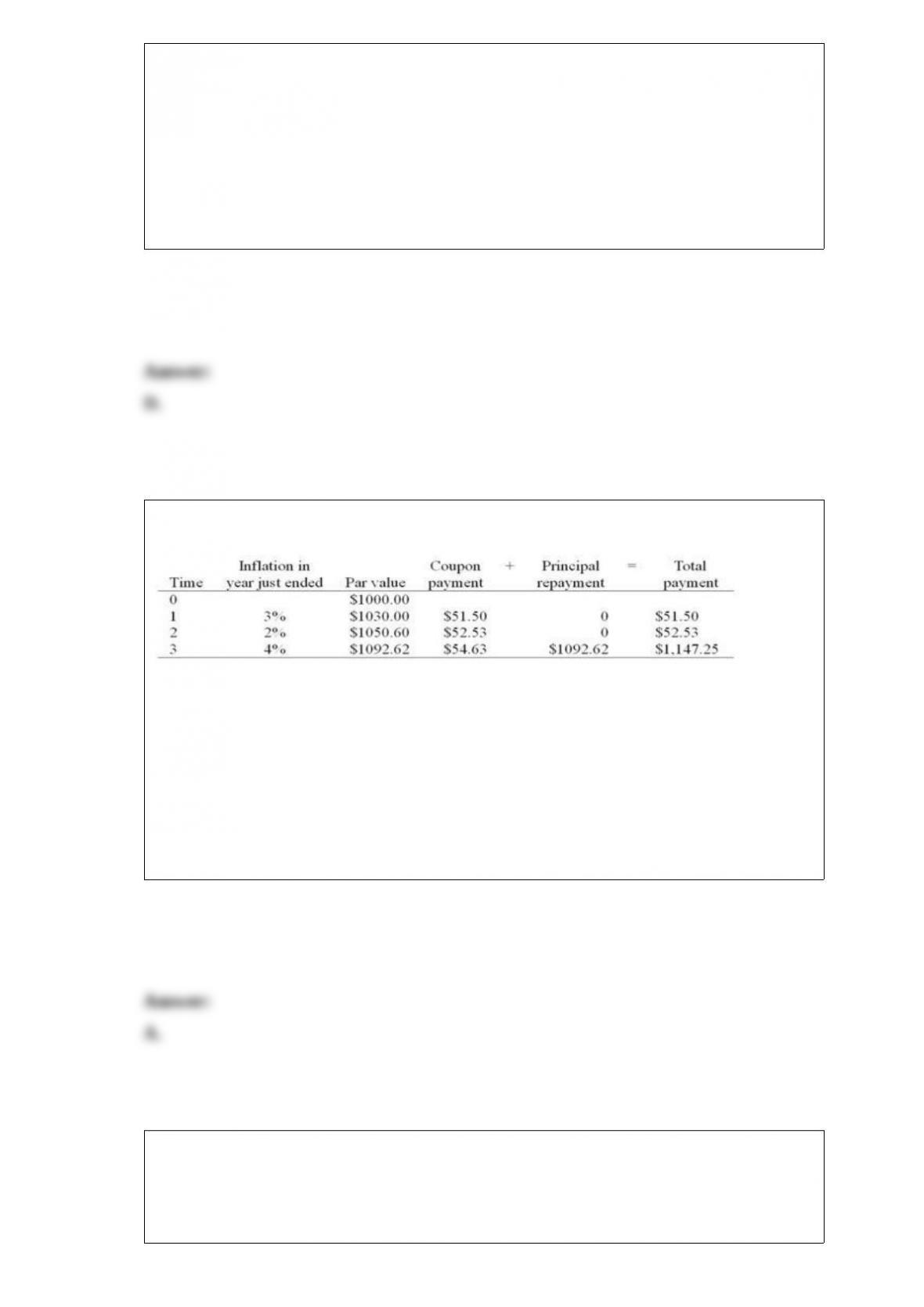

Consider a newly issued TIPS bond with a 3-year maturity, par value of $1,000, and

coupon rate of 5%. Assume annual coupon payments.

What is the real rate of return on the TIPS bond in the first year?

A. 5%

B. 8.15%

C. .15%

D. 4%

Life insurance companies try to hedge the risks inherent in whole-life insurance policies

by investing in __________.

A. long-term bonds

B. money market mutual funds

C. savings accounts

D. short-term commercial paper

If you anticipatea dramatic decline in stock prices, which naked strategy will make you

the most profit?

A. long call

B. long put

C. short call

D. short put

The graph of the relationship between expected return and beta in the CAPM context is

called the _________.

A. CML

B. CAL

C. SML

D. SCL

The expected return of a portfolio is 8.9%, and the risk-free rate is 3.5%. If the portfolio

standard deviation is 12%, what is the reward-to-variability ratio of the portfolio?

A. 0

B. .45

C. .74

D. 1.35

An expanding economy puts stress on the manufacturing ability of a company. When a

firm turns business down during periods of economic expansion, a problem exists in the

area of ____________.

A. asset allocation

B. capacity utilization

C. employment management

D. strategic planning

Warrants differ from listed options in that:

I. Exercise of warrants results in dilution of a firm’s earnings per share.

II. When warrants are exercised, new shares of stock must be created.

III. Warrant exercise results in cash flows to the firm, whereas exercise of listed options

does not.

A. I only

B. I and II only

C. II and III only

D. I, II, and III

If the S&P 500 Index futures contract is overpriced relative to the spot S&P 500 Index,

you should __________.

A. buy all the stocks in the S&P 500 and write put options on the S&P 500 Index

B. sell all the stocks in the S&P 500 and buy call options on S&P 500 Index

C. sell S&P 500 Index futures and buy all the stocks in the S&P 500

D. sell short all the stocks in the S&P 500 and buy S&P 500 Index futures

An investor who is hedging a corporate bond portfolio using a T-bond futures contract

is said to have _______.

A. an arbitrage

B. a cross-hedge

C. an over hedge

D. a spread hedge

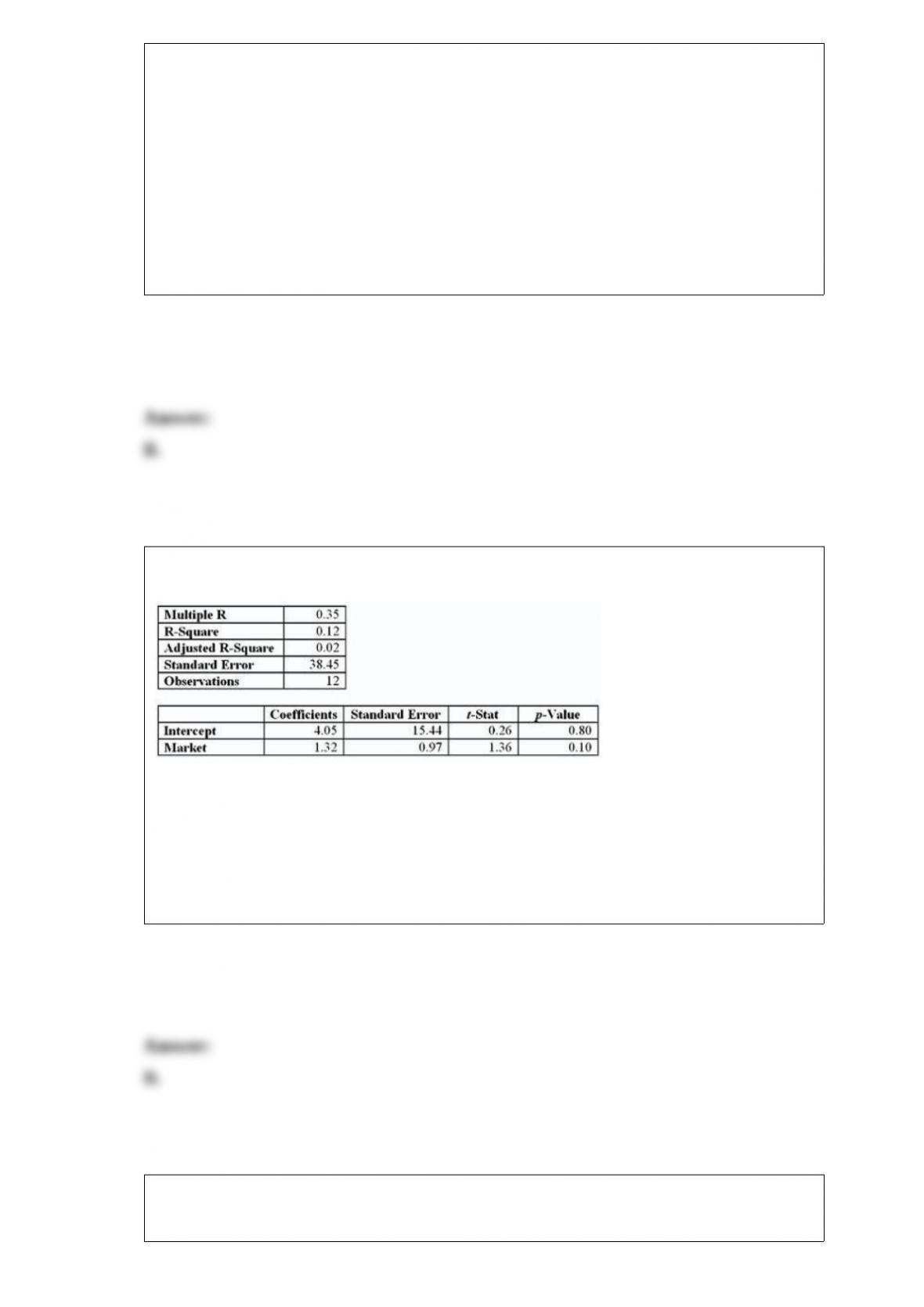

The characteristic

line for this stock

is Rstock = ___ +

___ Rmarket.

A. .35; .12

B. 4.05; 1.32

C. 15.44; .97

D. 26; 1.36

Consider a hedge fund with $200 million at the start of the year. The benchmark S&P

500 Index was up 16.5% during the same period. The gross return on assets is 21%, and

the expense ratio is 2%. For each 1% above the benchmark return, the fund managers

receive a .1% incentive bonus.

What was the annual return on this fund?

A. 16.5%

B. 18.04%

C. 18.55%

D. 21%

The 2002 law designed to improve corporate governance is titled the _____ .

A. Pension Reform Act

B. ERISA

C. Financial Services Modernization Act

D. Sarbanes-Oxley Act

Market signals will help to allocate capital efficiently only if investors are acting

_____ .

A. on the basis of their individual hunches

B. as directed by financial experts

C. as dominant forces in the economy

D. on accurate information

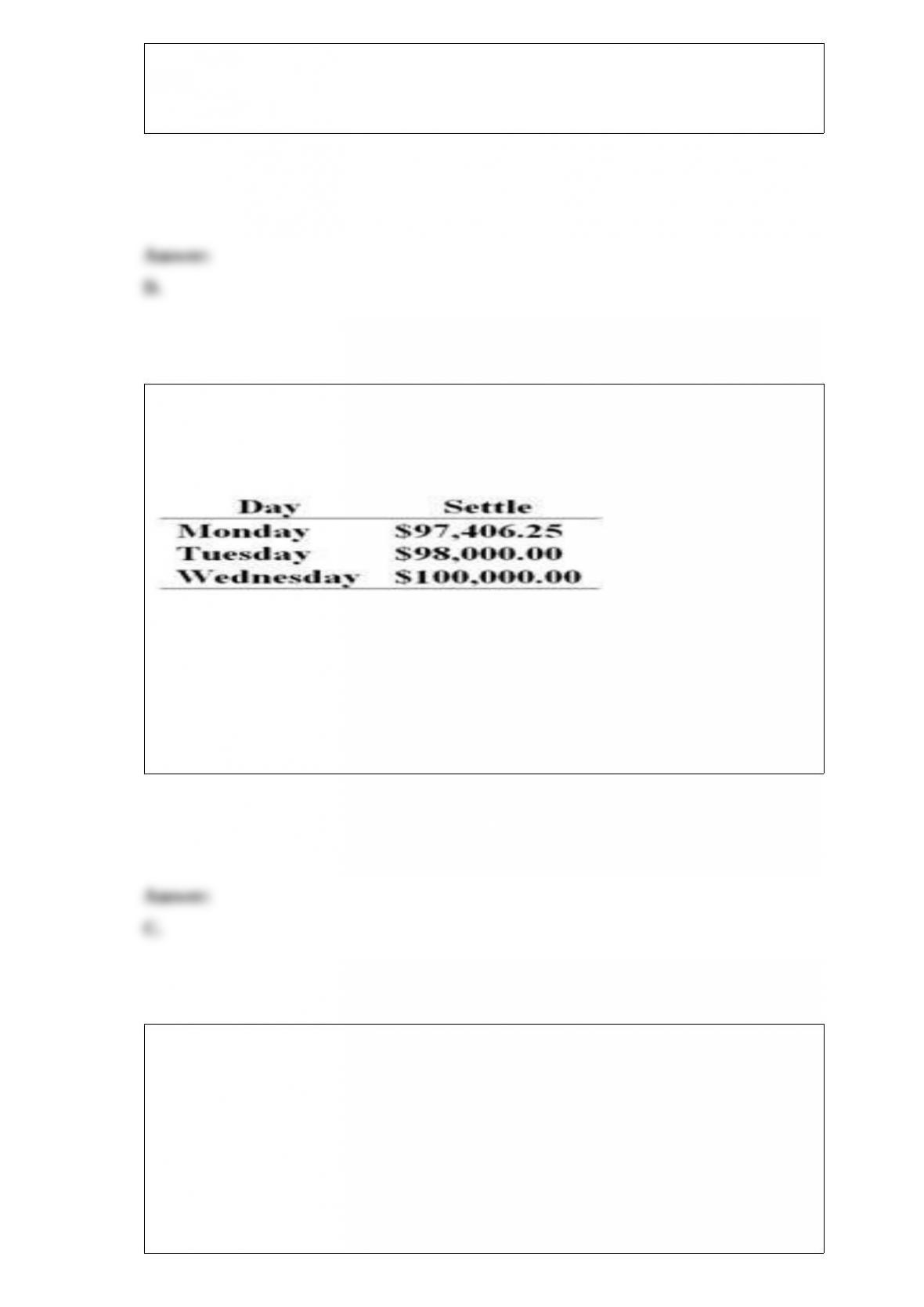

On Monday morning you sell one June T-bond futures contract at 97:27, that is, for

$97,843.75. The contract’s face value is $100,000. The initial margin requirement is

$2,700, and the maintenance margin requirement is $2,000 per contract. Use the

following price data to answer the following questions.

On which of the

given days do

you get a

margin call?

A. Monday

B. Tuesday

C. Wednesday

D. none of these options

The percentage change in the call option price divided by the percentage change in the

stock price is the __________ of the option.

A. delta

B. elasticity

C. gamma

D. theta

What happened to the effective spread on trades when the SEC allowed the minimum

tick size to move from one-eighth of a dollar to one-sixteenth of a dollar in 1997 and

from one-sixteenth of a dollar to one cent in 2001?

A. The effective spread increased in 1997 but decreased in 2001.

B. The effective spread increased in both cases.

C. The effective spread decreased in 1997 but increased in 2001.

D. The effective spread decreased in both cases.

The most common measure of __________ is the spread between the number of stocks

that advance in price and the number of stocks that decline in price.

A. market breadth

B. market volume

C. odd-lot trading

D. short interest

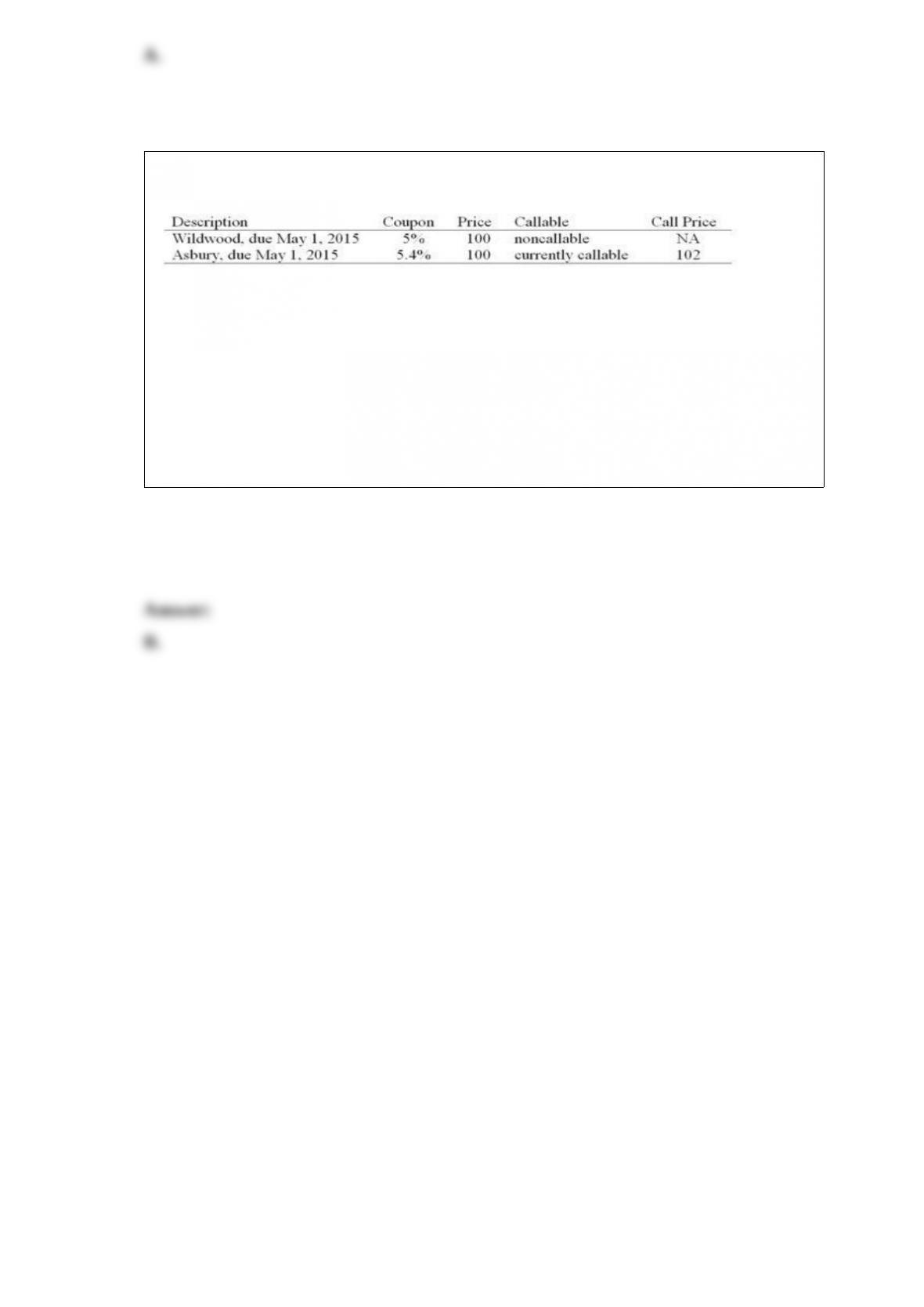

On May 1, 200, Joe Hill is considering one of the following newly issued 10-year AAA

corporate bonds.

If interest rates are expected to rise, then Joe Hill should ____.

A. prefer the Wildwood bond to the Asbury bond

B. prefer the Asbury bond to the Wildwood bond

C. be indifferent between the Wildwood bond and the Asbury bond

D. The answer cannot be determined from the information given.