1) a bank agrees to buy from a customer a “three against six” fra at the market rate for

such instruments. how can the bank hedge this obligation?

a.go long a 6-month eurodollar deposit in the amount of the fra at the current 6-month

rate financed by going short a 3-month eurodollar deposit in the amount of the fra at the

current 3-month rate

b.go short a 6-month eurodollar deposit in the amount of the fra at the current 6-month

rate; go long a 3-month eurodollar deposit in the amount of the fra at the current

3-month rate

c.borrow a 3-month eurodollar deposit in the amount of the fra at the current 3-month

rate

d.none of the above

2) most interbank trades are

a.speculative or arbitrage transactions

b.simple order processing for the retail client

c.overnight loans from one bank to another

d.brokered by dealers

3) the u.s. irs allows transfer prices to be set using the arms-length price.

a.this is a very straight-forward method to use in practicejust use the ebay price

b.this method is difficult to apply in practice because many factors enter into the pricing

of goods and services. examples include: differences in the terms of sale, differences in

quantity and or quality sold, even differences in location or date of sale

c.all of the above

d.none of the above

4) a typical foreign trade transaction requires three basic documents

a.letter of credit, bill of lading, and shipping documents

b.time draft, banker’s acceptance, and bill of lading

c.letter of credit, time draft, and bill of lading

d.letter of credit, banker’s acceptance, and bill of lading

5) most governments at least try to make it difficult for people to cross their borders

illegally. this barrier to the free movement of labor is an example of

a.information asymmetry

b.excessive transactions costs

c.racial discrimination

d.a market imperfection

6) a foreign country could provide low cost production sites

a.because the factors of production are underpriced

b.because the currency is undervalued

c.because the locals like to give away their land labor and capital to foreigners

d.both a and b

7) the current spot exchange rate is $1.55/ and the three-month forward rate is $1.50/.

based on your analysis of the exchange rate, you are confident that the spot exchange

rate will be $1.52/ in three months. assume that you would like to buy or sell 1,000,000.

what actions do you need to take to speculate in the forward market?

a.take a long position in a forward contract on 1,000,000 at $1.50/

b.take a short position in a forward contract on 1,000,000 at $1.50/

c.buy euro today at the spot rate, sell them forward

d.sell euro today at the spot rate, buy them forward

8) the sarbanes-oxley act of 2002

a.applies to all u.s. firms

b.applies to listed companies

c.applies to issuers whose securities are traded on an over-the-counter bulletin board

d.all of the above

9) several studies document the empirical link between

a.weak investor protection and gdp growth

b.financial development and economic growth

c.growth in gdp and concentrated ownership

d.none of the above

10) in may 1995 when the exchange rate was 80 yen per dollar, japan life insurance

company invested ¥800,000,000 (i.e., $10,000,000) in pure-discount u.s. bonds. the

investment was liquidated one year later when the exchange rate was 110 yen per dollar.

if the rate of return earned on this investment was 46% in terms of yen, calculate the

dollar amount that the bonds were sold at.

a.$10,618,000

b.$10,720,000

c.$14,600,000

d.none of the above

11) a 1-year, 4 percent euro denominated bond sells at par. a comparable risk 1-year, 5.5

percent euro/dollar dual-currency bond pays $1,500 at maturity per 1,000 of face value.

it sells for 1,250. what is the implied $/ exchange rate at maturity?

a.0.8300/$1.00

b.$1.2048/1.00

c.$1.25/1.00

d.$1.50/1.00

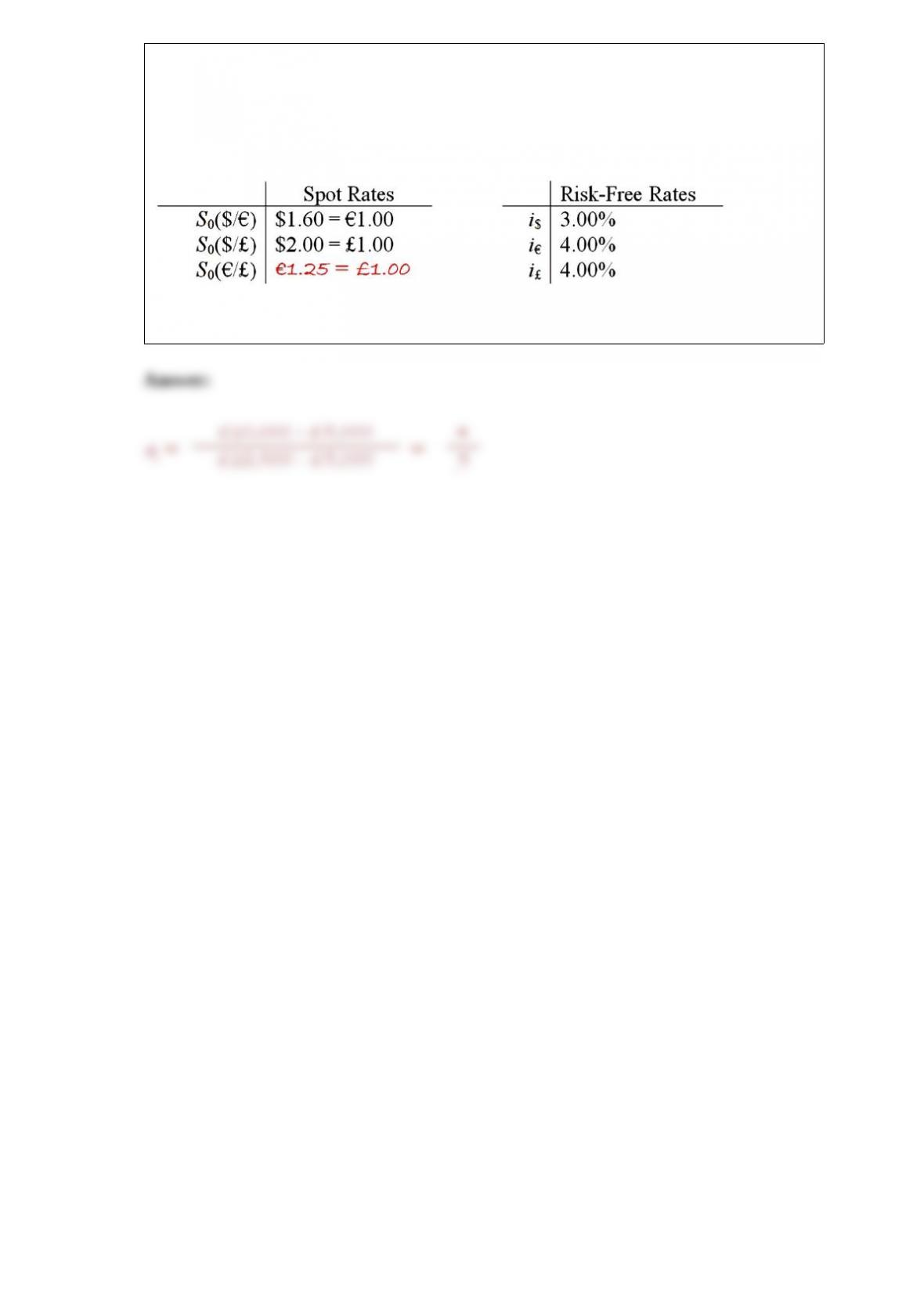

12) an italian currency dealer has good credit and can borrow 800,000 for one year. the

one-year interest rate in the u.s. is i$ = 2% and in the euro zone the one-year interest

rate is i = 6%. the spot exchange rate is $1.25 = 1.00 and the one-year forward

exchange rate is $1.20 = 1.00. show how to realize a certain euro-denominated profit

via covered interest arbitrage.

a.borrow $1,000,000 at 2%. trade $1,000,000 for 800,000; invest at i = 6%; translate

proceeds back at forward rate of $1.20 = 1.00, gross proceeds = $1,017,600

b.borrow 800,000 at i = 6%; translate to dollars at the spot, invest in the u.s. at i$ = 2%

for one year; translate 848,000 back into euro at the forward rate of $1.20 = 1.00. net

profit $2,400

c.borrow 800,000 at i = 6%; translate to dollars at the spot, invest in the u.s. at i$ = 2%

for one year; translate 850,000 back into euro at the forward rate of $1.20 = 1.00. net

profit 2,000

d.both c and b

13) the world’s largest foreign exchange trading center is

a.new york

b.tokyo

c.london

d.hong kong

14) suppose that britain pegs the pound to gold at the market price of £6 per ounce, and

the united states pegs the dollar to gold at the market price of $36 per ounce. if the

official exchange rate between pounds and u.s. dollars is $5 = £1. which of the

following trades is profitable?

a.start with £100 and trade for $500 at the official exchange rate. redeem the $500 for

13.89 ounces of gold. trade the gold for £83.33

b.start with $100 and buy gold. sell the gold for £16.67. sell the pounds at the official

exchange rate

c.start with £100 and buy gold. sell the gold for $600

d.start with $500 and trade for £100 at the official exchange rate. redeem the £100 for

16 2/3 ounces of gold. trade the gold for $600

15) a booming economy with a fixed or stable nominal exchange rate

a.inevitably brings about an appreciation of the real exchange rate

b.inevitably brings about a depreciation of the real exchange rate

c.inevitably brings about a stabilization of the real exchange rate

d.inevitably brings about increased volatility of the real exchange rate

16) a french firm is considering a one-year investment in the united kingdom with a

pound-denominated rate of return of i£ = 15%. the firm’s local cost of capital is i = 10%

the project costs £1,000 and will return £1,150 at the end of one year.

the current exchange rate is 2.00 = £1.00

suppose that the bank of england is considering either tightening or loosening its

monetary policy. it is widely believed that in one year there are only two possibilities:

using your results to the last question, make a recommendation vis–vis when to

undertake the project.

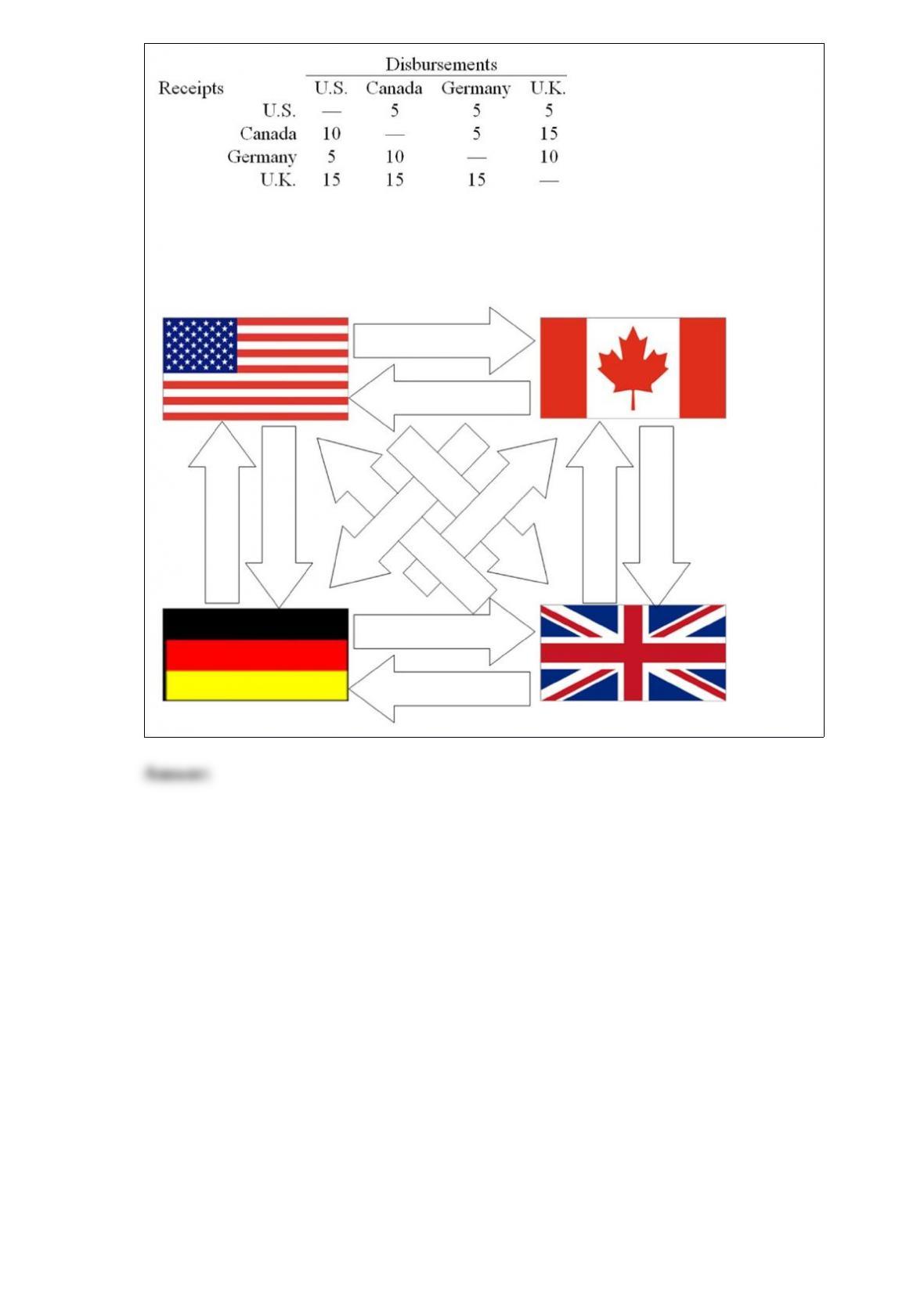

17) your firm’s interaffiliate cash receipts and disbursements matrix is shown below

($000):

fill out the following figure with the initial situation shown in the table.

18) the time from acceptance to maturity on a $500,000 banker’s acceptance is 270

days.

the importing bank’s acceptance commission is 0.75 percent and that the market rate for

270-day b/as is 4 percent.

determine the bond equivalent yield the importer’s bank will earn from discounting the

b/a with the exporter.

19) indirect exchange rate quotations from the u.s. perspective are

a. the price of one unit of the foreign currency in terms of the u.s. dollar

b. the price of one u.s. dollar in the foreign currency

20) a withholding tax is

21) a french firm is considering a one-year investment in the united kingdom with a

pound-denominated rate of return of i£ = 15%. the firm’s local cost of capital is i = 10%

the project costs £1,000 and will return £1,150 at the end of one year.

the current exchange rate is 2.00 = £1.00

suppose that the bank of england is considering either tightening or loosening its

monetary policy. it is widely believed that in one year there are only two possibilities:

find the expost irr in euro for the french firm if they undertake the project today and

then the exchange rate rises to s1(|£) = 2.20 per £.

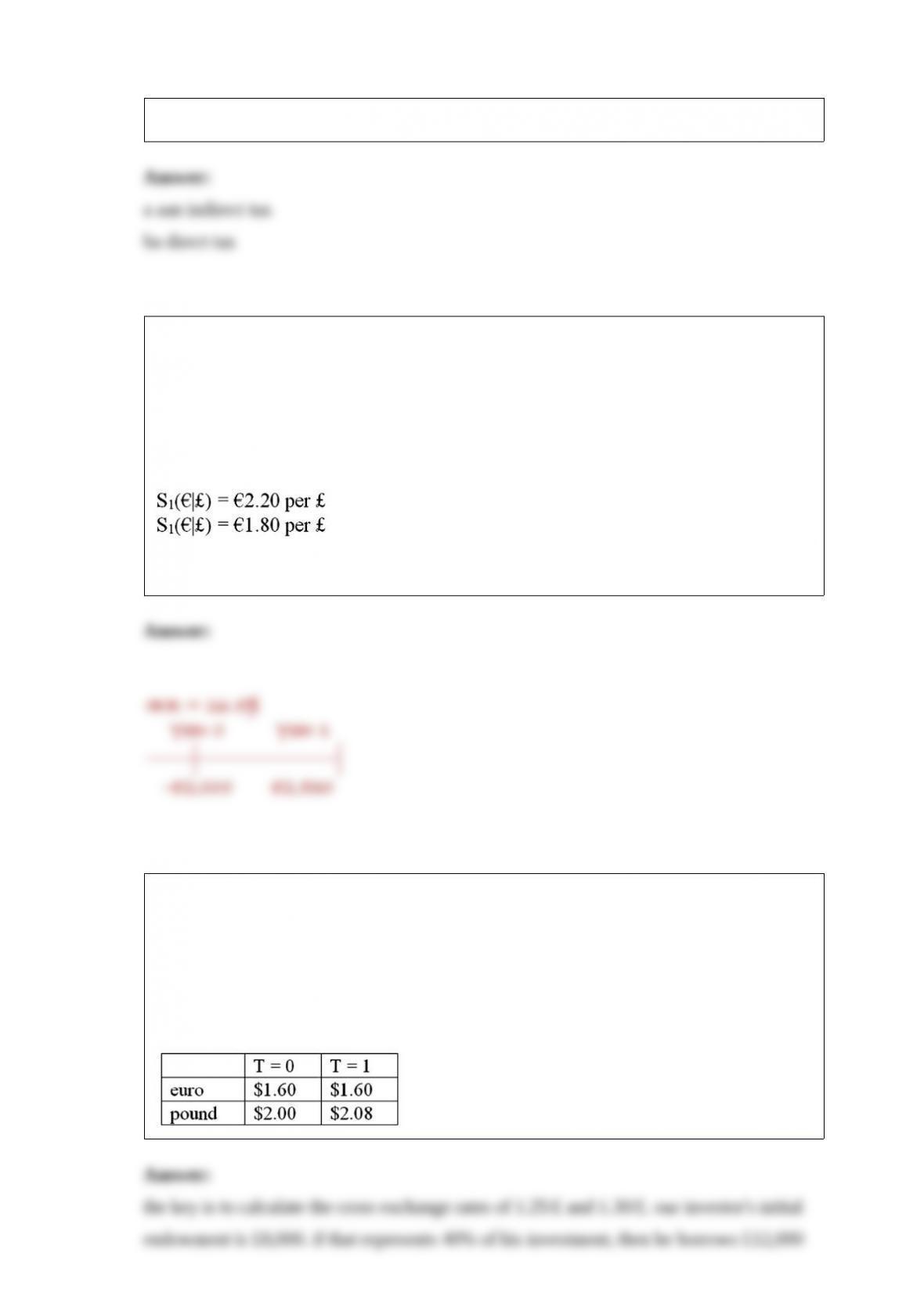

22) calculate the euro-based return an italian investor would have realized by investing

10,000 into a £50 british stock on margin with only 40% down and 60% borrowed.the

stock pays a £0.30 quarterly dividend, and after one year the investment sells for £54.

the interest on the margin loan is 1% per year. the margin loan is denominated in

pounds.

spot exchange rates at the start and end of the year are shown in the table.

23) your firm is based in southern ireland (and thereby operates in euro, not pounds)

and is considering an investment in the united states.

the project involves selling widgets: you project a sales volume of 50,000 widgets per

year, sales price of $20 per widget with a contribution margin of $15 per widget.

the project will last for 5 years, require an investment of $1,000,000 at time zero (which

will be depreciated straight-line to $10,000 over the 5 years). salvage value for the

equipment is projected to be $10,000. the project will operate in rented quarters:

$300,000 rent is due at the start of each year.

the corporate tax rate is 12% in ireland and 40% in the u.s.

for simplicity, assume that taxes are paid like sales taxes: immediately.

the spot exchange rate is $1.50 = 1.00. the cost of capital to the irish firm for a domestic

project of this risk is 8%. the u.s. risk-free rate is 3%; the irish risk-free rate is 2%.

find the break-even price (in dollars) and break-even quantity for the u.s. project.

24) consider an option to buy 12,500 for £10,000. in the next period, the euro can

strengthen against the pound by 25% (i.e. each euro will buy 25% more pounds) or

weaken by 20%.

big hint: don’t round, keep exchange rates out to at least 4 decimal places.

find the risk neutral probability of an “up” move.