Both parties in an interest rate swap normally are fully hedged against interest rate risk

on the notional amount of the swap.

Answer:

One way to minimize contingent credit risk is to use derivative products sold on

organized exchanges.

Answer:

Which of the following observations concerning loan default provisions is NOT TRUE?

A. They ensure that if a country defaults on just one of its loans, all its other

outstanding loans would automatically be put into default as well.

B. They prevent a country from selecting a group of weak lenders for special default

treatment.

C. They make the outcome of any individual loan default decision potentially very

costly for the borrower.

D. They protect strong lenders in any loan default by guaranteeing the repayment of

such defaulted loans.

E. None of the above.

Answer:

The typical customer of a payday lender has income of between $25,000 and $50,000

per year.

Answer:

The book value of bonds and loans reflects the market value of those assets when they

were placed on the books of an FI.

Answer:

Standby letters of credit perform an insurance function similar to that of commercial

and trade letters of credit.

Answer:

A contagious run, or bank panic, differs from a run on a bank in that a contagious run

involves loss of faith in the entire banking system as opposed to just one bank.

Answer:

Microhedging uses futures or forward contracts to hedge the entire balance sheet

duration gap.

Answer:

The real interest rate reflects the underlying real sector demand and supply for funds

denominated in the domestic currency.

Answer:

The European Community Second Banking Directive has aided the international

competitive position of European banks by creating a single banking market in Europe.

Answer:

The use of an up-front fee by a bank eliminates the contingent risk on a loan

commitment.

Answer:

The use of the option pricing model to determine the actuarially fair premium is

difficult to apply in practice because the asset values and risks are difficult to

determine.

Answer:

Selective hedging that results in an over-hedged position may be regarded as

speculative by regulators.

Answer:

In duration analysis, the times at which cash flows are received are weighted by the

relative importance in present value terms of the cash flows arriving at each point in

time.

Answer:

The buyer of an interest rate swap is likely to have a negative duration gap that they

would like to reduce.

Answer:

Deposit insurance is the only deterrent to bank runs, contagious runs, and bank panics.

Answer:

Interest rates charged to healthy banks that use the Federal Reserve discount window

are typically set one percent below the fed funds target interest rate.

Answer:

The value of assets is the traditional measure of size in the securities brokerage and

investment banking industry.

Answer:

The objective of technological expansion is to achieve economies of scale at the

expense of diseconomies of scope.

Answer:

The Securities Exchange Act of 1934 requires a mutual fund to file a registration

statement with the SEC.

Answer:

Basis risk occurs when the underlying security in the futures contract is not the same

asset as the cash asset on the balance sheet.

Answer:

Reliance on purchased or borrowed funds will largely eliminate the liquidity risk faced

by a bank.

Answer:

As FIs consolidate and expand their range of financial services, customer relationships

with commercial entities are likely to become more important.

Answer:

The larger the import ratio of a country; the higher is the probability that the country

will have to schedule its debt payments.

Answer:

CRA statistical credit scoring models have difficulty measuring political risk events.

Answer:

If regulators provide more protection against bank runs, the incidence of moral hazard

is likely to increase.

Answer:

Because of the large amounts of policy reserves that life insurance companies carry as

liabilities, they are rarely surprised by unexpected fluctuations in expected future

payouts.

Answer:

As an asset transformer, the FI issues financial claims that are more attractive to

household savers than the claims directly issued by corporations.

Answer:

Banks began selling short-term loans only since the passage of the Financial Services

Modernization Act in 1999.

Answer:

Under contemporaneous reserve accounting, there is a seven day reserve maintenance

period.

Answer:

The use of risk-based capital measures under Basel I (1993) effectively mark-to-market

the bank’s on- and off-balance-sheet for the purpose of reflecting credit and market

risk.

Answer:

The concentration limit method of managing credit risk concentration involves

estimating the minimum loan amount to a single customer as a percent of capital.

Answer:

Electronic brokerage allows an investor to have direct access to the trading floor.

Answer:

In recent years, the number of commercial banks in the U.S. has been increasing.

Answer:

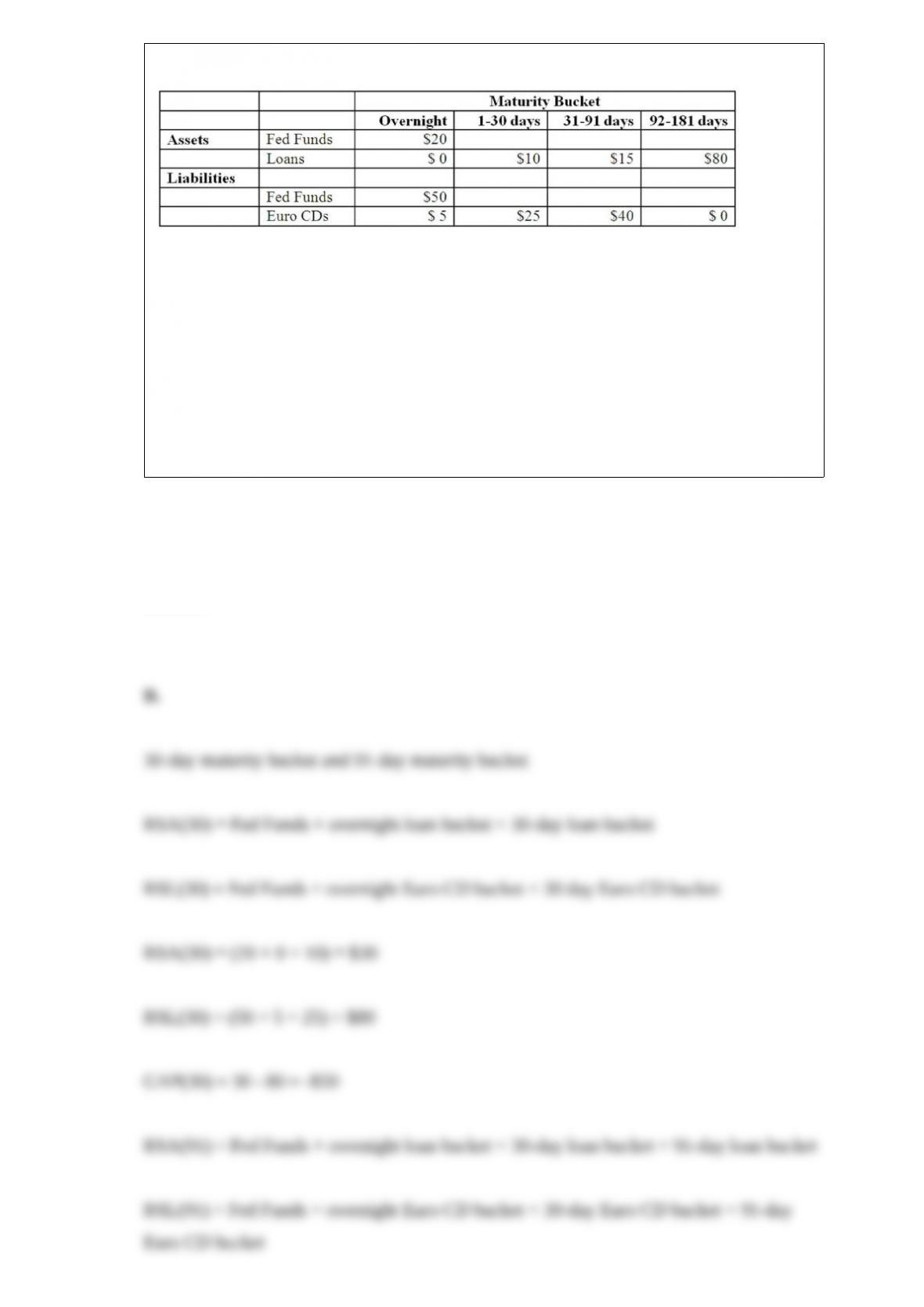

The following information details the current rate sensitivity report for Gotbucks Bank,

Inc. ($million).

Calculate the funding gap for Gotbucks Bank using (a) a 30 day maturity period and (b)

a 91 day maturity period? A. -$25 and +$80.

B. -$50 and -$75.

C. -$75 and +$5.

D. +$55 and -$40.

E. 0 and 0.

Answer:

Calculate the annual cash flows of a $2 million, 10-year fixed-payment annuity earning

a guaranteed 8 percent annually if the payments are to start at the end of this year. A.

$137,990.27.

B. $275,980.53.

C. $298,058.98.

D. $149,029.49.

E. $220,000.00.

Answer:

Assume that instead of investing in Euro bonds at a fixed rate of 6.5 percent, the FI

invests them in variable rates of LIBOR + 1.5 percent, reset every six months. The

current LIBOR rate is 5 percent. LIBOR at the end of six months is 5.5 percent. Assume

both interest and principal will be reinvested in six months. Assume the spot exchange

rate is €1.75/$. What should be the one-year forward rate in order for the bank to earn a

spread of 1 percent?A. €1.7344/$.

B. €1.7418/$.

C. €1.7478/$.

D. €1.7750/$.

E. €1.7842/$.

Answer:

Which of the following aided in allowing Federal Government Agencies (such as the

FDIC) to sell loans of institutions for which the agency has become responsible? A.

National Banking Act.

B. Financial Services Modernization Act.

C. Savings Institutions Reform Act.

D. Glass-Steagall Act.

E. Federal Debt Collection Improvement Act.

Answer:

In terms of liquidity risk measurement, the financing gap is defined as A. total deposits

minus core deposits.

B. financing requirement plus liquid assets.

C. rate sensitive assets minus rate sensitive liabilities.

D. total assets minus total liabilities.

E. average loans minus average deposits.

Answer:

Legislation designed to improve corporate governance practices, especially as they

relate to accounting practices, is the A. National Securities Markets Improvement Act

of 1996.

B. Sarbanes-Oxley Act.

C. U.S.A. Patriot Act.

D. Financial Services Modernization Act of 1999.

E. Bank Holding Company Act.

Answer:

Which of the following investment banks is no longer in business as a result of the most

recent financial crisis? A. Morgan Stanley.

B. Bear Stearns.

C. Lehman Brothers.

D. Goldman Sachs.

E. Merrill Lynch.

Answer:

The risk that borrowers are unable to repay their loans on time is A. credit risk.

B. sovereign risk.

C. currency risk.

D. liquidity risk.

E. interest rate risk.

Answer:

The statistical results of the country risk analysis models A. may have limited

usefulness if parameters are unstable.

B. are not subject to estimation error.

C. cannot be extrapolated to influence financial decision making.

D. are theoretical depictions of underlying relationships.

E. should not change over time.

Answer:

If the portfolio manager wants to shorten the bank’s asset maturity, what type of risk is

she concerned about? A. Credit risk.

B. Foreign exchange rate risk.

C. The risk of rising interest rates.

D. The risk of falling interest rates.

E. Default risk.

Answer:

The following is an example of a credit scoring model to estimate the probability of

debt rescheduling for country I:

Pi= 0.25DSRi+ 0.17IRi– 0.03 INVRi+ 0.84VAREXi+ 0.93 MGi

Where Pi is the probability of rescheduling country I’s debt; DSR is the country’s debt

service ratio; IR is the country’s import ratio; INVR is the country’s investment ratio;

VAREX is the country’s variance of export revenue; and MG is the country’s rate of

growth of the domestic money supply.

What is an important determinant of rescheduling probability if inflation is a prime

concern?A. The debt service ratio.

B. The import ratio.

C. The investment ratio.

D. The variance of export revenue.

E. The rate of growth of the domestic money supply.

Answer:

What reflects the degree to which the rate on the option’s underlying asset moves

relative to the spot rate on the asset or liability that is being hedged? A. Credit risk.

B. Basis risk.

C. Hedge risk.

D. Volatility.

E. Open interest.

Answer:

Overseas bank is pooling 50 similar and fully amortized mortgages into a pass-through

security. The face value of each mortgage is $100,000 paying 180 monthly interest and

principal payments at a fixed rate of 9 percent per annum.

If the entire mortgage pool is repaid after the second month, what is the second month’s

interest and principal payments? A. $37,441 interest and $13,275 principal.

B. $13,275 principal and $37,441 interest.

C. $13,312 interest and $4,986,786 principal.

D. $4,986,786 interest and $37401 interest.

E. $37,401 interest and $4,986,786 principal.

Answer:

Why do garbage class bonds often have a negative duration?A. The value of the returns

in this bond class increases when interest rates increase.

B. It gives the rights to collateralization.

C. Bond values fall with interest rate increases.

D. It gives rights to reinvestment income on the cash flows in the CMO trust.

E. Significant risk premium required by the uninsured depositors.

Answer:

Making a lending decision to a party residing in a foreign country is a two-step

decision. What are the two steps involved in such a decision? A. Assessing credit

quality of the borrower and sovereign risk quality of the borrower’s country.

B. Assessing political economy risk and exogenous risks.

C. Assessing sovereign risk quality of the borrower’s country and other country risks.

D. Rescheduling of existing loans and deciding on the terms for new loans.

E. Assessing the foreign exchange risk involved and the security that can be provided

by the borrower.

Answer:

An FI has purchased an agency security that is an inverse floater at 9 percent minus

LIBOR. Which of the following characteristics reflect this type of asset? A. If LIBOR

is 4 percent, the asset will pay 5 percent to the investor.

B. As LIBOR increases, the investor will receive a lower return on the security.

C. The agency issuing this security may convert it into a LIBOR liability by entering

into a swap agreement.

D. If the FI funded the asset at LIBOR, and LIBOR reaches 10 percent, the FI will

have a negative 10 percent spread on the asset.

E. All of the above.

Answer:

Bank USA has fixed-rate assets of $50 million funded by fixed-rate liabilities of 75

million Euros paying an interest rate of 10 percent annually. Bank Dresdner has

fixed-rate assets of €75 million funded by fixed-rate liabilities of $50 million paying an

interest rate of 10 percent annually. The current exchange rate is €1.50/$. They agree to

swap interest payments on their liabilities to hedge against currency risk exposure for

two years.

The transaction each year consists of A. Bank USA swaps a payment of $5 million per

year for Bank Dresdner’s payment of €7.5 million to make interest payments on each

other’s debt.

B. Bank USA swaps a payment of €6 million per year for Bank Dresdner’s payment of

$4 million to make interest payments on each other’s debt.

C. Bank USA swaps a payment of $6 million per year for Bank Dresdner’s payment of

€6 million to make interest payments on each other’s debt.

D. Bank USA swaps a payment of €6 million per year for Bank Dresdner’s payment of

$6 million to make interest payments on each other’s debt.

E. Bank USA swaps a payment of $4 million per year for Bank Dresdner’s payment of

€4 million to make interest payments on each other’s debt.

Answer:

How have the innovations of global financial networks and computerized money and

information transfer systems changed financial intermediation?A. Financial

intermediation has become riskier because it is more difficult to stay informed about

worldwide events.

B. Financial intermediation has become more costly because it is necessary to invest in

high cost technology.

C. Financial intermediation has been unaffected.

D. Financial intermediation has become more costly as global firms exploit economies

of scale and scope.

E. Financial intermediation has become less risky as firms become adept at

maintaining zero gap positions.

Answer:

Which of the following is an example of interest rate parity? A. The Japanese yen

trades at the same exchange rate as the Swiss franc.

B. U.S. dollar rates on one year U.S. Treasury securities equal 1 year Japanese

government bond rates.

C. U.S. dollar rates on one year U.S. Treasury securities equal 1 year Japanese

government bond rates, restated in dollars.

D. British pound 2 year forward rates equal 2 year Swiss franc forward rates.

E. All currency exchange rates and interest rates move in unison.

Answer:

XYZ Bank lends $20,000,000 to ABC Corporation which has a credit rating of BB. The

spread of a BB rated benchmark bond is 2.5 percent over the U.S. Treasury bond of

similar maturity. XYZ Bank sells a $20,000,000 one-year credit forward contract to

IWILL Insurance Company. At maturity, the spread of the benchmark bond against the

Treasury bond is 2.1 percent, and the benchmark bond has a modified duration of 4

years. What is the amount of payment paid by whom to whom at the maturity of the

credit forward contract? A. The seller pays the buyer $320,000.

B. The buyer pays the seller $320,000.

C. The seller pays the buyer $80,000.

D. The buyer pays the seller $80,000.

E. The borrower receives $240,000.

Answer:

Which of the following is an advantage to an FI of expanding globally? A. Exposure to

nationalization or expropriation.

B. Economies of scale.

C. High fixed costs.

D. Costs of complying with different regulatory requirements.

E. Information and monitoring costs.

Answer:

What is the primary function of finance companies? A. Protect individuals and

corporations from adverse events.

B. Make loans to both individuals and corporations.

C. Extend loans to banks and other financial institutions.

D. Pool the financial resources of individuals and companies and invest in diversified

portfolios of assets.

E. Assist in the trading of securities in the secondary markets.

Answer:

At the end of year 3, LIBOR rates are 6 percent and the exchange rate is $1.10/£. What

is the net payment paid or received in dollars by the U.S. bank? A. The U.S. bank paid

$12 million and received $16.5 million for a net receipt of $4.5 million.

B. The U.S. bank paid $12 million and received $11 million for a net payment of $1

million.

C. The U.S. bank paid $12 million and received $12 million for a net payment of $0

million.

D. The U.S. bank paid $9 million and received $11 million for a net receipt of $2

million.

E. The U.S. bank paid $9 million and received $12 million for a net receipt of $3

million.

Answer:

Which of the following occur when managers undertake growth-oriented investments to

increase an FI’s size that may be inconsistent with stockholders’ value-maximizing

objectives?A. Technology risk.

B. Operational efficiency.

C. Agency conflicts.

D. Diseconomies of scale.

E. Diseconomies of scope.

Answer:

Giving the purchaser the right to sell the underlying security at a prespecified price is a

A. put option.

B. call option.

C. naked option.

D. futures option.

E. credit spread call option.

Answer:

What is the impact on economic capital of a 25 basis point decrease in interest rates if

the FI is holding a 20-year, fixed-rate, 11 percent annual coupon bond selling at a par

value of $100,000? A. A decrease of $250.

B. An increase of $250.

C. An increase of $2,024.

D. A decrease of $1,959.

E. No impact on capital since the book value is unchanged.

Answer:

The largest category of liabilities of broker-dealers as of the beginning of 2012 was A.

bank loans payable.

B. securities sold under repurchase agreements.

C. payables to customers.

D. short positions in securities and commodities.

E. payables to non-customers.

Answer:

This type of finance company competes directly with depository institutions for

consumer loans because they can frequently process loans faster and more

conveniently. A. Sales finance institution.

B. Personal credit institution.

C. Business credit institution.

D. Lease finance company.

E. Factoring company.

Answer:

The FI is acting as a hedger when it A. buys or sells currency to balance the FI’s net

exposure.

B. takes a nonzero net position in a particular currency.

C. processes an exporter’s transaction in a foreign currency.

D. makes a market in a currency.

E. advises customers on their international business.

Answer:

Each of the variables in the credit scoring model of sovereign country risk A. cannot be

measured independently.

B. has a systematic and unsystematic component.

C. has a predictable and an unpredictable component.

D. is determined by a weighted risk index.

E. has a high systematic risk element.

Answer:

Which of the following is NOT a factor that may tend to increase loan sales in the

future? A. There is an increased trend to apply credit ratings to loans offered for sale,

increasing the attractiveness to secondary market purchasers.

B. The federal government takeover of Fannie Mae and Freddie Mac means that the

loans held by these agencies can never be sold to other entities.

C. Because of their special credit monitoring skills, FIs have a comparative advantage

in making loans to below-investment grade companies and then selling the loan.

D. The trend toward marked-to-market accounting for assets makes bank loans more

like securities so they may be easier to sell.

E. The risk-based capital requirements of the Bank for International Settlements give

banks a strong incentive to sell commercial loans to decrease their amount of risky

assets.

Answer:

The charter values of FIs will be higher if regulators A. increase the cost of entry by

requiring more capital.

B. restrict the number of activities permitted by FIs, thereby increasing potential

profits.

C. restrict the number of FIs that can operate in a given market.

D. Answers A and B.

E. Answers A and C.

Answer: