________ is a risk measure that indicates vulnerability to extreme negative returns.

A. Value at risk

B. Lower partial standard deviation

C. Expected shortfall

D. None of the options

E. None of the options are correct.

The spread between the LIBOR and the Treasury-bill rate is called the

A. term spread.

B. T-bill spread.

C. LIBOR spread.

D. TED spread.

The Dow Jones Industrial Average (DJIA) is computed by

A. adding the prices of 30 large “blue-chip” stocks and dividing by 30.

B. calculating the total market value of the 30 firms in the index and dividing by 30.

C. adding the prices of the 30 stocks in the index and dividing by a divisor.

D. adding the prices of the 500 stocks in the index and dividing by a divisor.

E. adding the prices of the 30 stocks in the index and dividing by the value of these

stocks as of some base

date period.

Which of the following are investment superstars who have consistently shown superior

performance? I) Warren Buffet

II) Phoebe Buffet

III) Peter Lynch

IV) Merrill Lynch

V) Jimmy Buffet

A. I, III, and IV

B. II, III, and IV

C. I and III

D. III and IV

E. I, III, IV, and V

Chartists practice

A. technical analysis.

B. fundamental analysis.

C. regression analysis.

D. insider analysis.

E. psychoanalysis.

You have just purchased a 7-year zero-coupon bond with a yield to maturity of 11% and

a par value of $1,000. What would your rate of return at the end of the year be if you

sell the bond? Assume the yield to maturity on the bond is 9% at the time you sell.

A. 10.00%

B. 23.8%

C. 13.8%

D. 1.4%

Debt securities are often called fixed-income securities because

A. the government fixes the maximum rate that can be paid on bonds.

B. they are held predominantly by older people who are living on fixed incomes.

C. they pay a fixed amount at maturity.

D. they promise either a fixed stream of income or a stream of income determined by a

specific formula.

E. they were the first type of investment offered to the public which allowed them to

“fix” their income at a higher level by investing in bonds.

Ceteris paribus, the duration of a bond is positively correlated with the bond’s

A. time to maturity.

B. coupon rate.

C. yield to maturity.

D. All of the options are correct.

E. None of the options are correct.

If you believe in the ________ form of the EMH, you believe that stock prices reflect

all relevant information, including historical stock prices and current public information

about the firm, but not information that is available only to insiders.

A. semistrong

B. strong

C. weak

D. All of the options are correct.

E. None of the options are correct.

______ are the dominant form of investing in securities markets for most individuals,

but ______ have enjoyed a far greater growth rate in the last decade.

A. Hedge Funds; hedge funds

B. Mutual funds; hedge funds

C. Hedge Funds; mutual funds

D. Mutual funds; mutual funds

E. None of the options are correct.

The gamma of an option is

A. the volatility level for the stock that the option price implies.

B. the continued updating of the hedge ratio as time passes.

C. the percentage change in the stock call-option price divided by the percentage

change in the stock price.

D. the sensitivity of the delta to the stock price.

A mutual fund had average daily assets of $2.0 billion in 2016. The fund sold $500

million worth of stock and purchased $600 million worth of stock during the year. The

fund’s turnover ratio is

A. 27.5%.

B. 12%.

C. 15%.

D. 25%.

E. 20%.

Consider the single-factor APT. Stocks A and B have expected returns of 15% and 18%,

respectively. The risk-free rate of return is 6%. Stock B has a beta of 1.0. If arbitrage

opportunities are ruled out, stock A has a beta of

A. 0.67.

B. 1.00.

C. 1.30.

D. 1.69.

E. 0.75.

A mutual fund had year-end assets of $750,000,000 and liabilities of $7,500,000. There

were 40,000,000 shares in the fund at year end. What was the mutual fund’s net asset

value?

A. $9.63

B. $18.56

C. $16.42

D. $17.87

E. $17.26

Which of the following orders instructs the broker to sell at or above a specified price?

A. Limit-buy order

B. Discretionary order

C. Limit-sell order

D. Stop-buy order

E. Market order

If the market prices of each of the 30 stocks in the Dow Jones Industrial Average

(DJIA) all change by the same percentage amount during a given day, which stock will

have the greatest impact on the DJIA?

A. The stock trading at the highest dollar price per share

B. The stock having the greatest amount of debt in its capital structure

C. The stock having the greatest amount of equity in its capital structure

D.

The stock having the lowest volatility

An American-style call option with six months to maturity has a strike price of $35. The

underlying stock now sells for $43. The call premium is $12. What is the intrinsic value

of the call?

A. $12

B. $8

C. $0

D. $23

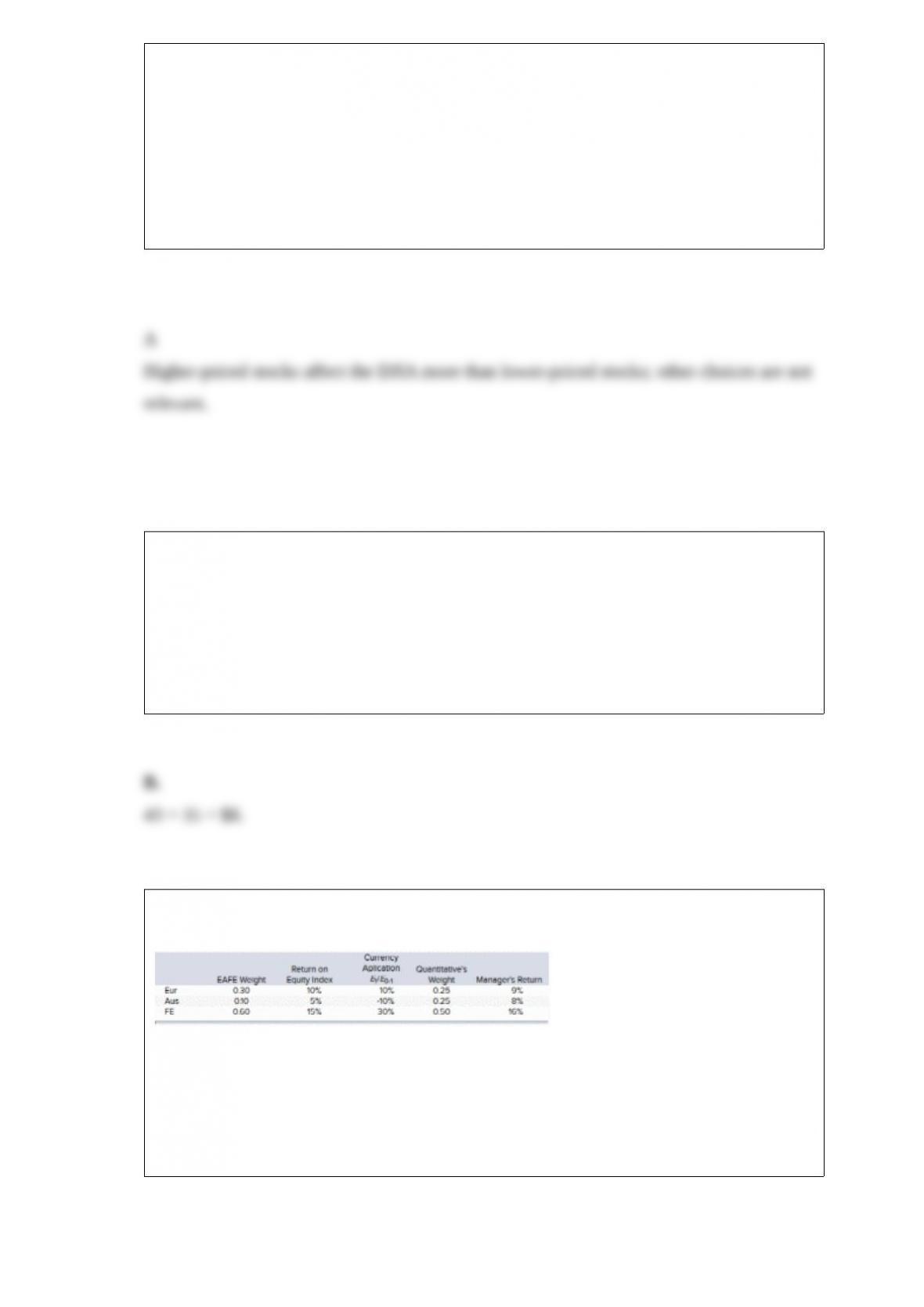

The manager of Quantitative International Fund uses EAFE as a benchmark. Last year’s

performance for the fund and the benchmark were as follows:

Calculate Quantitative’s country selection return contribution.

A. 12.5%

B. 12.5%

C. 11.25%

D. 1.25%

E. 1.25%

Which equity index had the lowest volatility in terms of U.S. dollar-denominated

returns for the period of five years ending in October 2016?

A. Korea

B. U.S.

C. Toronto

D. Nikkei

Pools of money invested in a portfolio that is fixed for the life of the fund are called

A. closed-end funds.

B. open-end funds.

C. unit investment trusts.

D. REITS.

E. redeemable trust certificates.

At issue, offering prices of open-end funds will often be

A. less than NAV due to loads.

B. greater than NAV due to loads.

C. less than NAV due to limited demand.

D. greater than NAV due to excess demand.

E. less than or greater than NAV with no apparent pattern.

In the dividend discount model, which of the following are not incorporated into the

discount rate?

A. Real risk-free rate

B. Risk premium for stocks

C. Return on assets

D. Expected inflation rate

DeBondt and Thaler (1990) argue that the P/E effect can be explained by

A. forecasting errors.

B. earnings expectations that are too extreme.

C. earnings expectations that are not extreme enough.

D. regret avoidance.

E. forecasting errors and earnings expectations that are too extreme.

The sale of a mortgage portfolio by setting up mortgage pass-through securities is an

example of

A. credit enhancement.

B. credit swap.

C. unbundling.

D. derivatives.

According to Peter Lynch, a rough rule of thumb for security analysis is that

A. the growth rate should be equal to the plowback rate.

B. the growth rate should be equal to the dividend-payout rate.

C. the growth rate should be low for emerging industries.

D. the growth rate should be equal to the P/E ratio.

E. None of the options are correct.

Suppose the following equation best describes the evolution of β over time:

βt = 0.31 + 0.82βt– 1.

If a stock had a β of 0.88 last year, you would forecast the β to be _______ in the

coming year.

A. 0.88

B. 0.82

C. 0.31

D. 1.03

_______ are real assets.

A. Land

B. Machines

C. Stocks and bonds

D. Knowledge

E. Land, machines, and knowledge

You purchased a share of stock for $120. One year later, you received $1.82 as a

dividend and sold the share

for $136. What was your holding-period return?

A. 15.67%

B. 22.12%

C. 18.85%

D. 13.24%

E. None of the options are correct.

In the APT model, what is the nonsystematic standard deviation of an equally-weighted

portfolio that has an

average value of (ei ) equal to 20% and 20 securities?

A. 12.5%

B. 625%

C. 4.47%

D. 3.54%

E. 14.59%

If a bond portfolio manager believes

I) in market efficiency, he or she is likely to be a passive portfolio manager.

II) that he or she can accurately predict interest-rate changes, he or she is likely to be an

active portfolio manager.

III) that he or she can identify bond-market anomalies, he or she is likely to be a passive

portfolio manager.

A. I only

B. II only

C. III only

D. I and II

E. I, II, and III

Shares for short transactions

A. are usually borrowed from other brokers.

B. are typically shares held by the short seller’s broker in street name.

C. are borrowed from commercial banks.

D. are typically shares held by the short seller’s broker in street name and are borrowed

from commercial banks.

A.An investor invests 70% of his wealth in a risky asset with an expected rate of return

of 0.15 and a variance of

0.04 and 30% in a T-bill that pays 5%. His portfolio’s expected return and standard

deviation are __________

and __________, respectively.

0.114; 0.128

B. 0.087; 0.063

C. 0.295; 0.125

D. 0.081; 0.052

You purchase a share of CAT stock for $90. One year later, after receiving a dividend of

$4, you sell the stock

for $97. What was your holding-period return?

A. 14.44%

B. 12.22%

C. 13.33%

D. 5.56%

You purchase one IBM March 200 put contract for a put premium of $6. What is the

maximum profit that you could gain from this strategy?

A. $20,000

B. $20,600

C.$19,400

D. $19,000

Agricultural futures contracts are actively traded on

A. soybeans.

B. oats.

C. wheat.

D. soybeans and oats.

E. All of the options are correct.