A fixed-income portfolio manager sets a minimum acceptable rate of return on the bond

portfolio at 5% per year over the next 4 years. The portfolio is currently worth $10

million. One year later interest rates are at 6%. What is the portfolio value trigger point

at this time that would require the manager to immunize the portfolio?

A. $12,155,063

B. $10,205,625

C. $9,627,948

D. $10,500,000

Bonds with coupon rates that fall when the general level of interest rates rise are called

_____________.

A. asset-backed bonds

B. convertible bonds

C. inverse floaters

D. index bonds

A call option has an exercise price of $35 and a stock price of $36.50. If the call option

is trading at $2.25, what is the time value embedded in the option?

A. $0

B. $.75

C. $1.50

D. $2.25

The purchase of a futures contract gives the buyer _________.

A. the right to buy an item at a specified price

B. the right to sell an item at a specified price

C. the obligation to buy an item at a specified price

D. the obligation to sell an item at a specified price

The bulk of most initial public offerings (IPOs) of equity securities goes to

___________.

A. institutional investors

B. individual investors

C. the firm’s current shareholders

D. day traders

You believe that the spread between the September T-bond contract and the June T-bond

futures contract is too large and will soon correct. This market exhibits positive cost of

carry for all contracts. To take advantage of this, you should ______________.

A. buy the September contract and sell the June contract

B. sell the September contract and buy the June contract

C. sell the September contract and sell the June contract

D. buy the September contract and buy the June contract

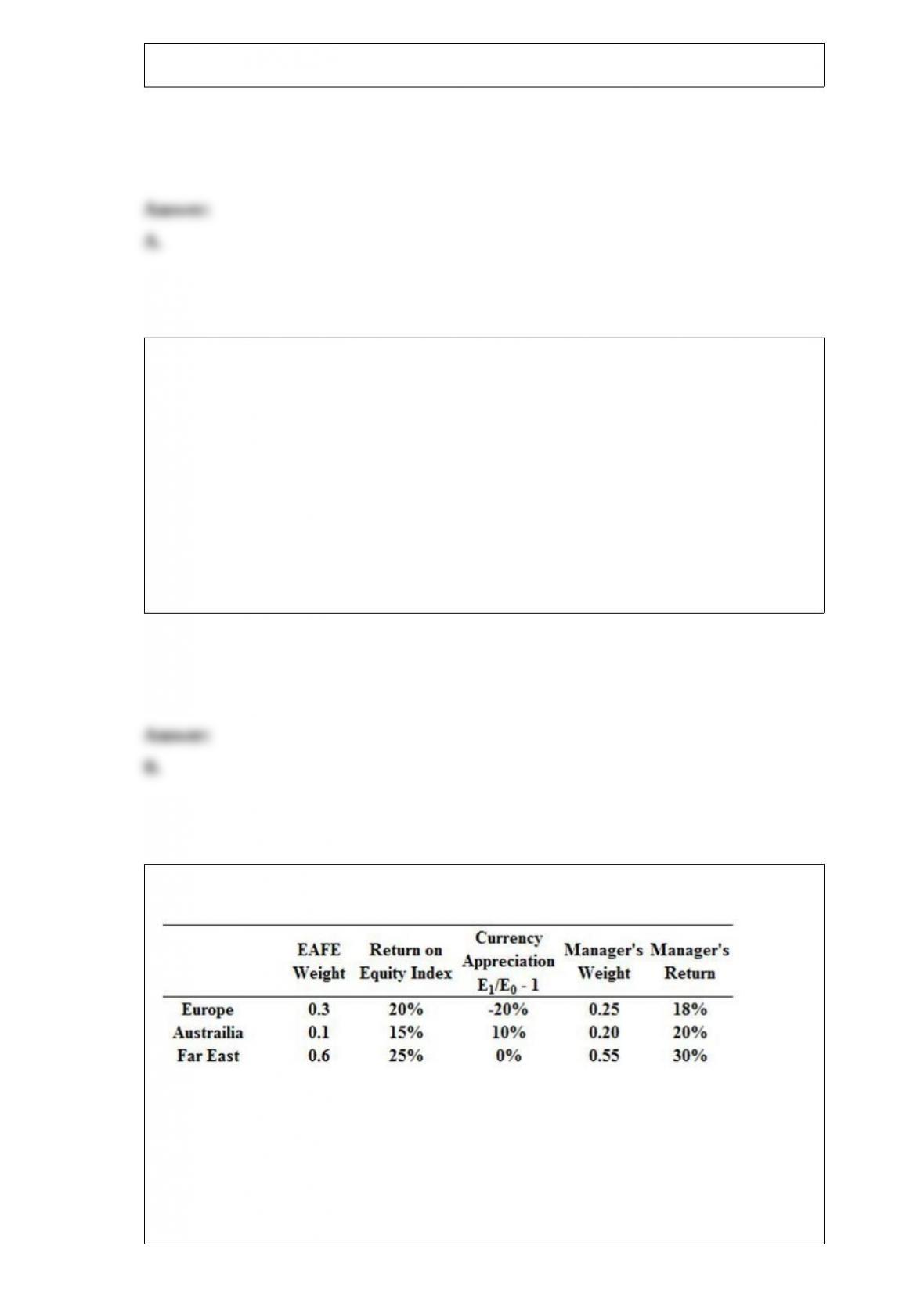

All exchange rates are expressed as units of foreign currency that can be purchased with

one U.S. dollar. Answer the following about decomposing the manager’s performance.

What is the difference in return of the manager’s portfolio due to currency selection?

A. -5%

B. -3%

C. 2%

D. 1%

When a stock price breaks through the moving average from below, this is considered

to be ______.

A. the starting point for a new moving average

B. a bearish signal

C. a bullish signal

D. none of these options