Identify the residual class of a CMO that gives the owner the right to any remaining

collateral in the trust after all other bond classes have been retired plus any

reinvestment income earned by the trust. A. Class A bonds.

B. Class B bonds.

C. Class C bonds.

D. Class Z bonds.

E. Class R bonds.

Answer:

Which of the following is a major source of debt capital for a captive finance company?

A. Premiums.

B. Deposits.

C. Equity.

D. Bank loans.

E. Parent company.

Answer:

One of the problems with estimating expected default rates is that the analysis is based

on historic data.

Answer:

Match the following pieces of legislation with the function achieved by each regulation

as stated in question

A. Securities Act of 1933

B. Securities Exchange Act of 1934

C. Investment Advisers Act

D. Investment Company Act

E. Insider Trading and Securities Fraud Enforcement Act of 1988

F. Market Reform Act of 1990

G. National Securities Markets Improvement Act of 1996

Requires a mutual fund to file a registration statement with the SEC.

Answer:

Which of the following identifies the largest group of derivative contracts as of June

2012? A. Futures.

B. Forwards.

C. Options.

D. Swaps.

E. Credit derivatives.

Answer:

If problem loans reduce the market value of the loan portfolio by 25 percent, what is the

market value of capital? A. $35 million.

B. -$155 million.

C. $7 million.

D. -$7 million.

E. $0.

Answer:

If 25 percent of the commitment is taken down, the total fees areA. $250,000.

B. $4,000,000.

C. $400,000.

D. $775,000.

E. $375,000.

Answer:

Calculate the modified duration of a two-year corporate loan paying 6 percent interest

annually. The $40,000,000 loan is 100 percent amortizing, and the current yield is 9

percent annually. A. 2 years.

B. 1.91 years.

C. 1.94 years.

D. 1.49 years.

E. 1.36 years.

Answer:

A claim to the present value of the interest payments made by the mortgage holders in a

GNMA pool is A. a CARS.

B. an IO strip.

C. a CARD.

D. a PO strip.

E. a prepayment claim.

Answer:

Over the past 30 years in the DI industry A. the loan portfolio has become more liquid

because of increased securitization.

B. lower amounts of very liquid assets need to be held to manage withdrawal risk.

C. more opportunities exist for raising funds that are not deposit related.

D. DIs have intentionally managed liabilities to reduce withdrawal risk.

E. All of the above.

Answer:

Why do households prefer to use FIs as intermediaries to invest their surplus funds? A.

Transaction costs are low to the household since FIs are more efficient in monitoring

and gathering investment information.

B. To receive the benefits of diversification that households may not be able to achieve

on their own.

C. The FI has can benefit from combining funds and negotiating lower asset prices and

transactions costs.

D. The FI can provide insurance at relatively low cost that will protect funds under

management.

E. All of the above.

Answer:

If the minimum RAROC acceptable to the bank is 8 percent, what should be its

expected percentage fee income in order for it to approve the loan? A. .157 percent.

B. .331 percent.

C. .471 percent.

D. .531 percent.

E. .571 percent.

Answer:

What is Bank B’s standard deviation of its asset allocation proportions relative to the

national banks average? Use the formula in the textbook.A. 14.16 percent.

B. 33.33 percent.

C. 5.66 percent.

D. 3.00 percent.

E. 1.50 percent.

Answer:

The operating ratio for a PC insurer equals A. loss ratio plus the ratios of loss

adjustment expenses to premiums earned.

B. loss ratio plus expense ratio plus dividend ratio.

C. combined ratio minus dividends paid to policyholders.

D. acquisition costs plus dividends paid as a proportion of premiums earned.

E. combined ratio after dividends minus the investment yield.

Answer:

If interest rates increase by 20 basis points (i.e., ΔR = 20 basis points), use the duration

approximation to determine the approximate price change for the Treasury note.A.

$0.000.

B. $0.2775 per $100 face value.

C. $2.775 per $100 face value.

D. $0.2672 per $100 face value.

Answer:

What does a hurdle rate specified by a hedge fund indicate?A. The maximum number

of investors possible in the fund that would allow it to avoid regulations.

B. The minimum amount required to be invested in the fund.

C. The net worth criterion for an individual to be deemed an “accredited investor.”

D. The highest net asset value that the fund has previously achieved, above which the

manager receives a performance fee.

E. The minimum annualized performance benchmark that must be realized before a

performance fee can be assessed.

Answer:

The numbers provided are in millions of dollars and reflect market values:

The

short-term debt consists of 4-year bonds paying an annual coupon of 4 percent and

selling at par. What is the duration of the short-term debt?A. 3.28 years.

B. 3.53 years.

C. 3.78 years.

D. 4.03 years.

E. 4.28 years.

Answer:

In which of the following situations would an FI be considered net long in foreign

assets if it has ¥100 million in loans? A. ¥120 million in liabilities.

B. ¥80 million in liabilities.

C. ¥100 million in liabilities.

D. ¥110 million in liabilities.

E. Answers A and D only.

Answer:

Calculate the annual cash flows of a $2 million, 10-year fixed-payment deferred annuity

earning a guaranteed 8 percent per year if annual payments are to begin at the end of the

sixth (6th) year. A. $218,973.21.

B. $202,752.97.

C. $343,321.86.

D. $405,505.95.

E. $437,946.42.

Answer:

Which of the following is NOT a wholesale banking service? A. Controlled

disbursement accounts.

B. Account reconciliation.

C. Electronic funds transfer.

D. Electronic initiation of letters of credit.

E. Automated teller machines.

Answer:

At what one-year forward rate will the bank earn a 1 percent spread? A. €1.7344/$.

B. €1.7418/$.

C. €1.7478/$.

D. €1.7750/$.

E. €1.7842/$.

Answer:

Mortgage-backed bonds (MBB) differ from pass-throughs and CMOs in which of the

following ways?A. The MBB bondholders have a junior claim to assets of the FI.

B. There is no direct link between the cash flow on the mortgages backing the bond

and the interest and principal payments on the MBB.

C. The assets backing a MBB issue are normally removed from the balance sheet of the

FI.

D. Tranches of a MBB are treated equally with respect to prepayments on mortgages

backing the bond issue.

E. None of the above.

Answer:

Broker-dealers must calculate a market value for their net worth on a day-to-day basis

and ensure that their net worth-assets ratio A. exceeds 1 percent.

B. is at least 2 percent.

C. exceeds 5 percent.

D. is less than 1 percent.

E. is greater than or equal to 1 percent.

Answer:

Using the proceeds from the simultaneous sale of a floor to finance the purchase of a

cap is to open a position called a A. open interest.

B. pull-to-par.

C. cap.

D. floor.

E. collar.

Answer:

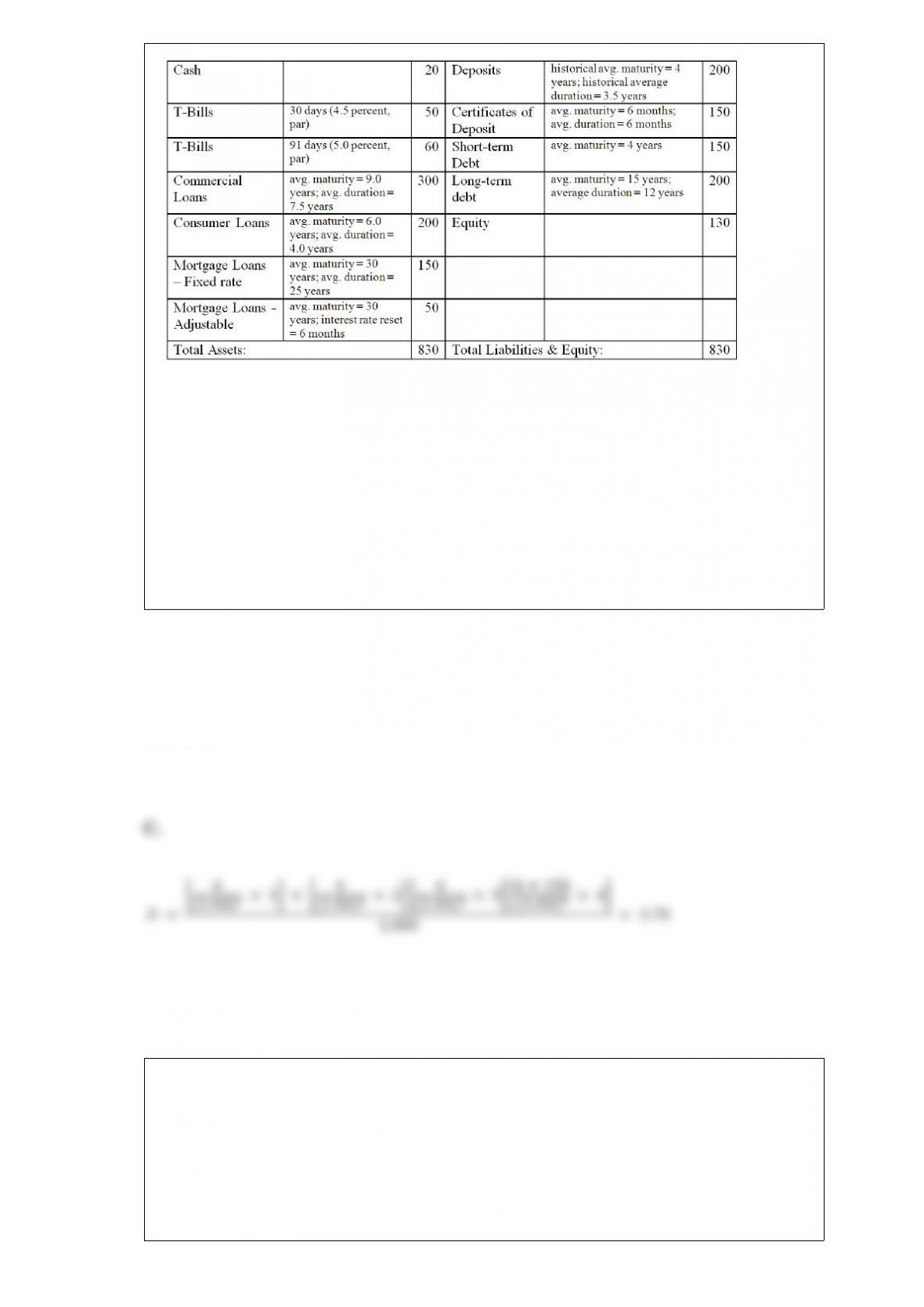

Third Duration Investments has the following assets and liabilities on its balance sheet.

The two-year Treasury notes are zero coupon assets. Interest payments on all other

assets and liabilities occur at maturity. Assume 360 days in a year.

What is

the duration of the assets? A. 0.708 years.

B. 0.354 years.

C. 0.350 years.

D. 0.955 years.

E. 0.519 years.

Answer:

What is the cash spread earned by the FI if at the end of the year the ≤ is trading at

$1.63/≤ in the cash market? Again adjust for all exchange rate changes. A. $1,610,000

gain.

B. $1,610,000 loss.

C. $2,670,000 loss.

D. $2,670,000 gain.

E. $2,390,000 loss.

Answer:

What will be the cost of using a strategy of reducing its asset base to meet the expected

decline in deposits? Assume that the bank intends to keep $2 million in cash as a

liquidity precaution. A. $10,000.

B. $15,000.

C. $30,000.

D. $40,000.

E. $50,000.

Answer:

Credit rationing by an FI A. involves restricting the quantity of loans made available to

individual borrowers.

B. results from a positive linear relationship between interest rates and expected loan

returns.

C. is not used by FIs at the retail level.

D. involves rationing consumer loans using price or interest rate differences.

E. is only relevant to banks.

Answer:

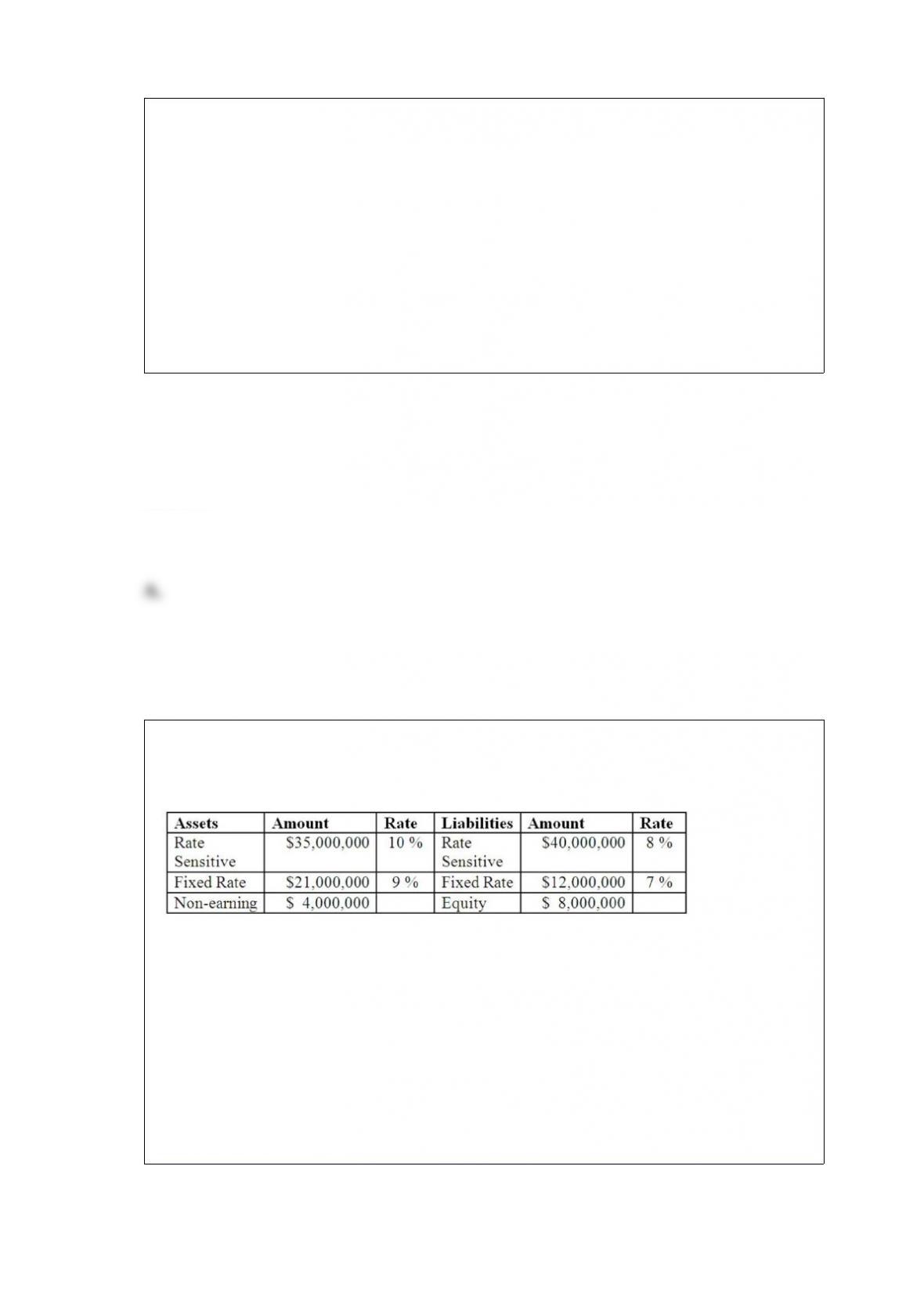

The balance sheet of ARGH Insurance shows the following fixed and rate sensitive

assets and liabilities.

Suppose

short-term interest rates increase by 1 percent. Calculate the change in net interest

income after the interest rate increase.A. $50,000.

B. $18,900.

C. $40,400.

D. $53,900.

E. $32,000.

Answer:

The U.S.A. Patriot Act requires financial services firms toA. verify the identity of any

person seeking to open an account.

B. maintain records of the information used to verify a person’s identity.

C. determine whether a person opening an account is on a list of suspected terrorists.

D. All of the above.

E. Answers A and C only.

Answer:

Which of the following are contracts that give the holder the right, but not the

obligation, to buy or sell an underlying asset at a pre-specified price for a specified time

period? A. Options.

B. Futures.

C. Forwards.

D. Swaps.

E. All of the above.

Answer:

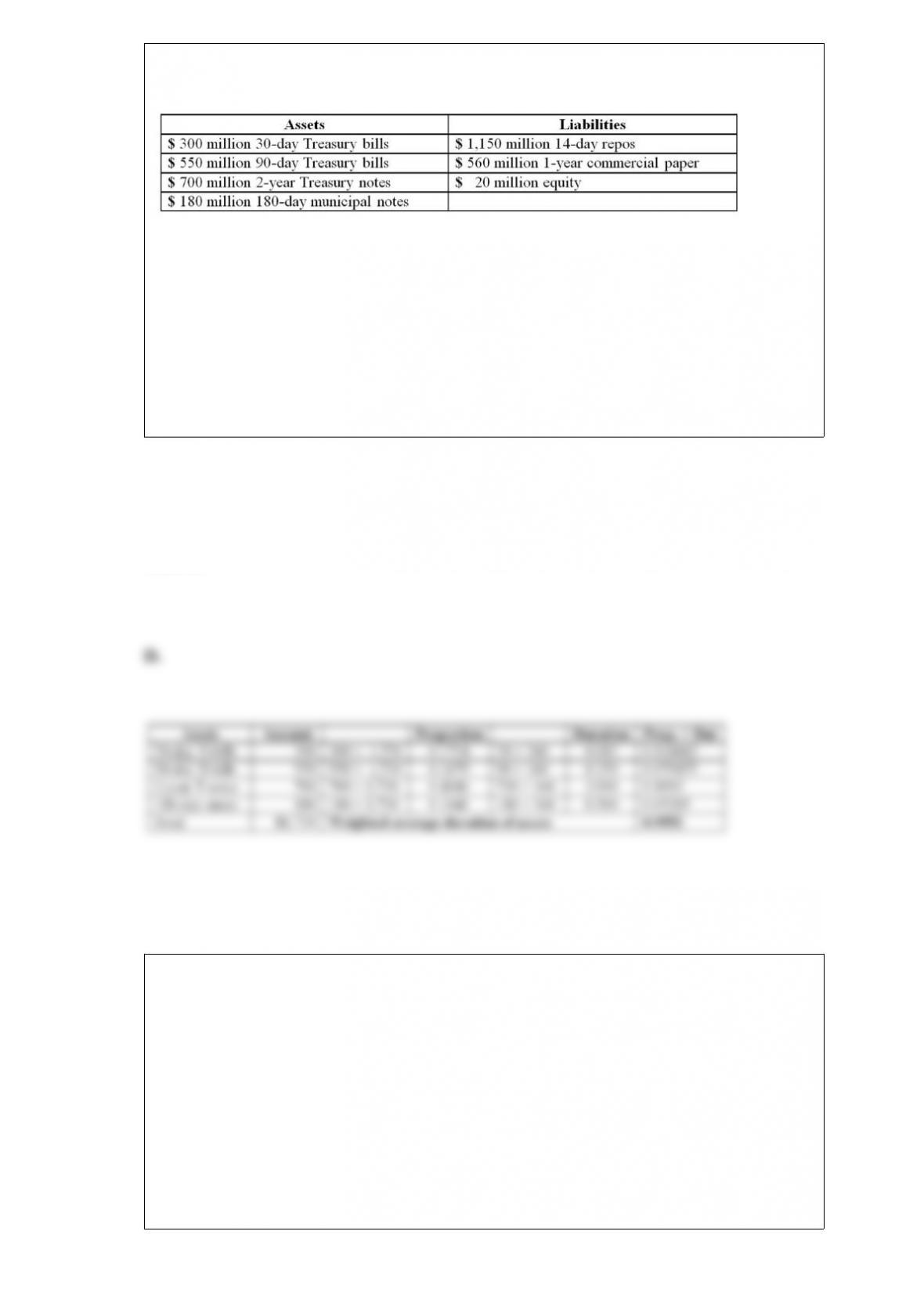

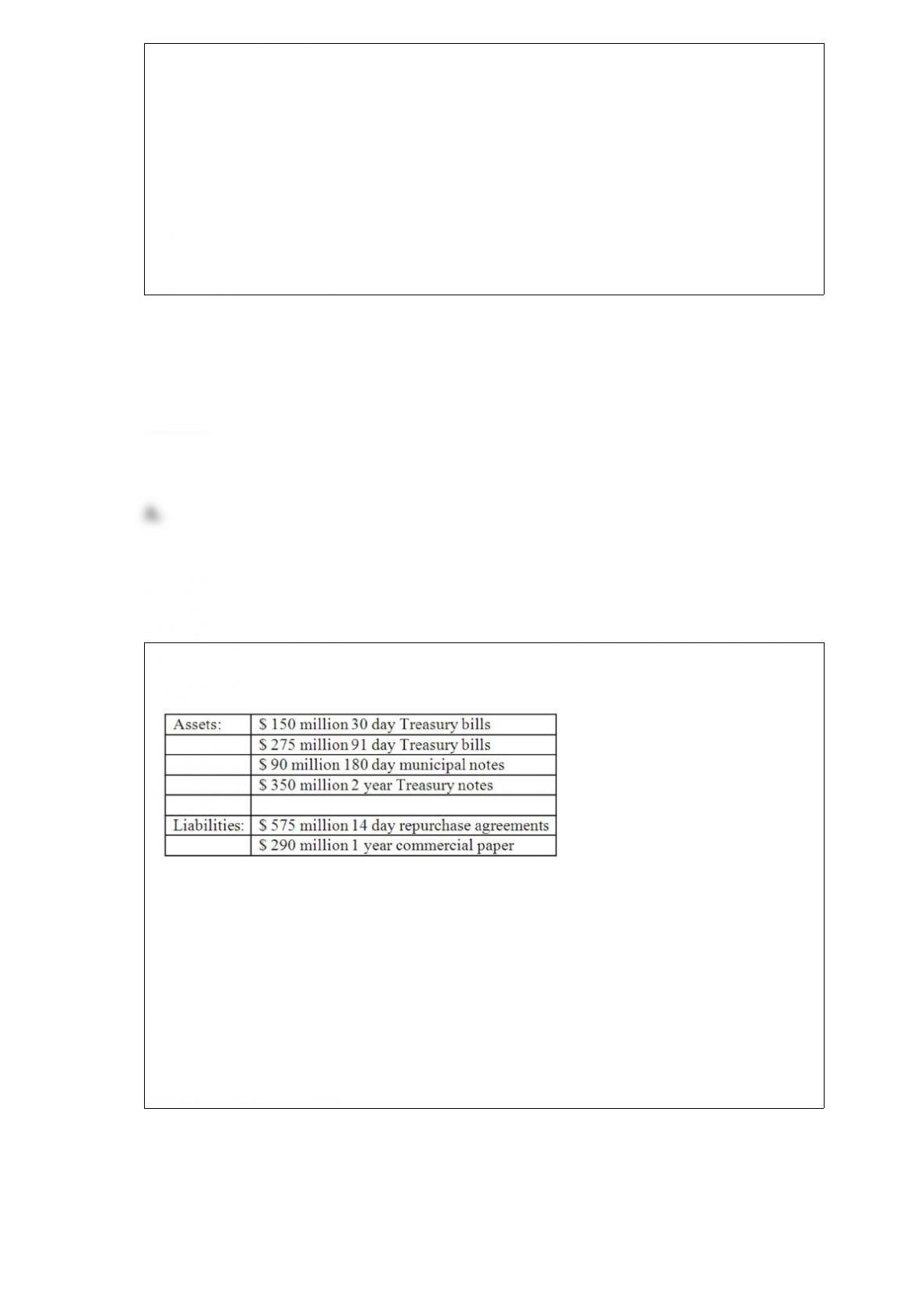

The following are the assets and liabilities of a government security dealer.

What is the impact over the next

30 days on the dealer’s net interest income if all interest rates increase by 50 basis

points?A. Net interest income will decrease by $50,000.

B. Net interest income will decrease by $2.125 million.

C. Net interest income will decrease by $475,000.

D. Net interest income will decrease by $2.375 million.

E. Net interest income will increase by $750,000.

Answer:

Factoring involves A. making loans to customers that depository institutions find too

risky to lend.

B. providing financing for the purchase of products manufactured by the parent

company.

C. approving of collateral that depository institutions do not find acceptable.

D. providing financing through equipment leasing.

E. purchasing of accounts receivable by finance company from corporate customers.

Answer:

As of 2012, commercial banks with over $10 billion in assets constituted approximately

____ percent of the industry assets and numbered approximately _____. A. 50; 310

B. 60; 165

C. 70; 525

D. 80; 90

E. 90; 440

Answer: