You purchased shares of a mutual fund at a price of $20 per share at the beginning of

the year and paid a front-end load of 5.75%. If the securities in which the fund invested

increased in value by 11% during the year, and the fund’s expense ratio was 1.25%,

your return if you sold the fund at the end of the year would be

A. 4.33%.

B. 3.44%.

C. 2.45%.

D. 6.87%.

The potential loss for a writer of a naked call option on a stock is

A. limited.

B.unlimited.

C. increasing when the stock price is decreasing.

D. equal to the call premium.

E. None of the options are correct.

An example of a liquidity ratio is

A. fixed asset turnover.

B. current ratio.

C. acid test or quick ratio.

D. fixed asset turnover and acid test or quick ratio.

E. current ratio and acid test or quick ratio.

A zero-coupon bond has a yield to maturity of 12% and a par value of $1,000. If the

bond matures in 18 years, the bond should sell for a price of _______ today.

A. $422.41

B. $501.87

C. $513.16

D. $130.04

Which one of the following terms best describes Eurodollars?

A. Dollar-denominated deposits only in European banks.

B. Dollar-denominated deposits at branches of foreign banks in the U.S.

C. Dollar-denominated deposits at foreign banks and branches of American banks

outside the U.S.

D. Dollar-denominated deposits at American banks in the U.S.

E. Dollars that have been exchanged for European currency.

A rapidly growing GDP indicates a(n) ______ economy with ______ opportunity for a

firm to increase sales.

A. stagnant; little

B. stagnant; ample

C. expanding; little

D.-expanding; ample

E. stable; no

A Treasury bond due in one year has a yield of 6.2%; a Treasury bond due in five years

has a yield of 6.7%. A bond issued by Xerox due in five years has a yield of 7.9%; a

bond issued by Exxon due in one year has a yield of 7.2%. The default risk premiums

on the bonds issued by Exxon and Xerox, respectively, are

A. 1.0% and 1.2%.

B. 0.5% and .7%.

C. 1.2% and 1.0%.

D. 0.7% and 0.5%.

E. None of the options are correct.

SIVs raise funds by ______ and then use the proceeds to ______.

A. issuing short-term commercial paper; retire other forms of their debt

B. issuing short-term commercial paper; buy other forms of debt such as mortgages

C. issuing long-term bonds; retire other forms of their debt

D. issuing long-term bonds; buy other forms of debt such as mortgages

The industry with the lowest return in 2016 was

A.-asset management.

B. telecom services.

C. health care.

D. business software.

E. money center banks.

According to proponents of the efficient-market hypothesis, the best strategy for a small

investor with a portfolio worth $40,000 is probably to

A. perform fundamental analysis.

B. exploit market anomalies.

C. invest in Treasury securities.

D. invest in derivative securities.

E. invest in mutual funds.

In 2016, ____________ was the least significant financial asset of U.S. households in

terms of total value.

A. real estate

B. mutual fund shares

C. debt securities

D. life insurance reserves

E. pension reserves

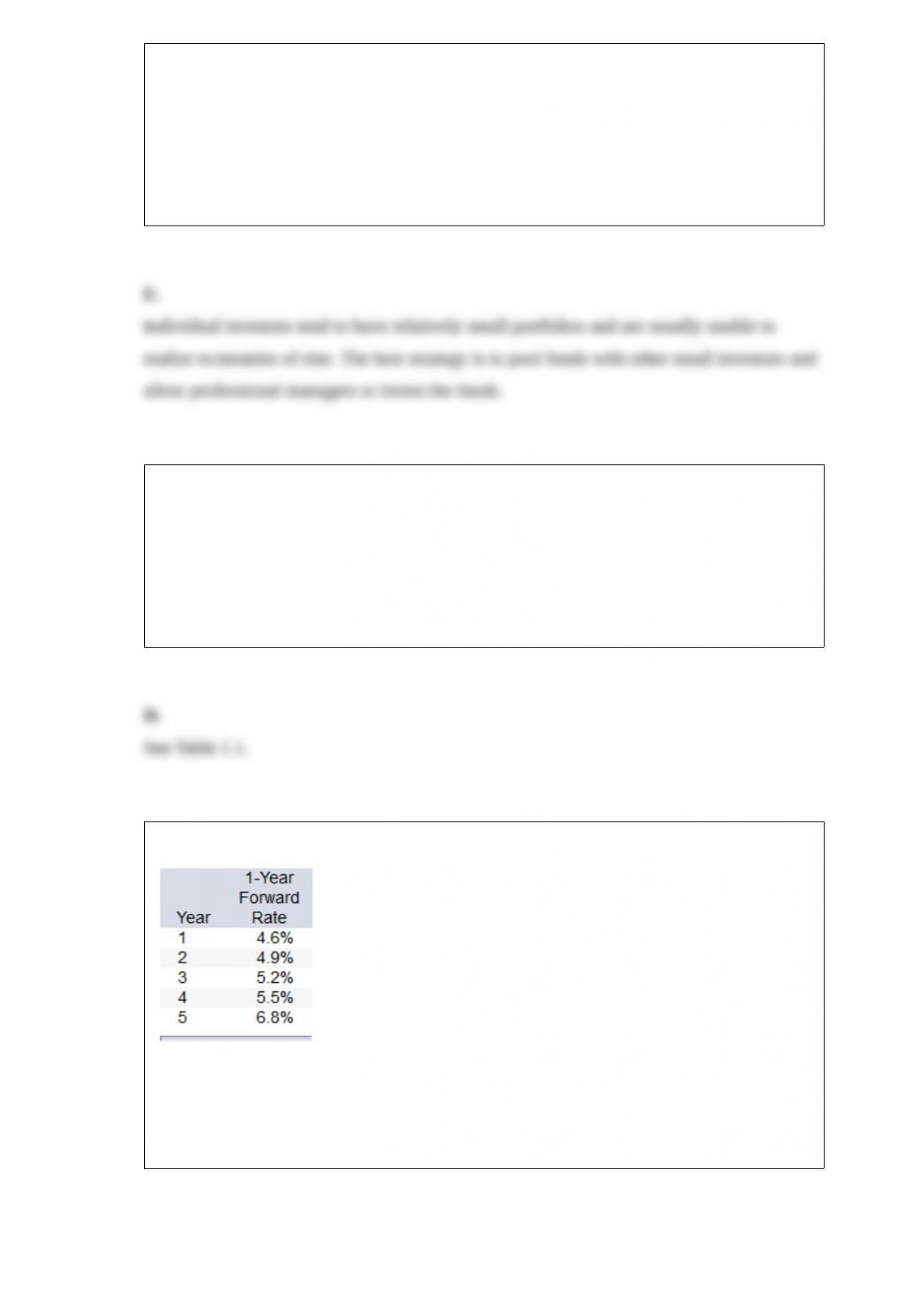

What is the yield to maturity of a 5-year bond?

A. 4.6%

B. 4.9%

C. 5.2%

D. 5.5%

E. 5.8%

Consider the one-factor APT. The variance of returns on the factor portfolio is 9%. The

beta of a well-diversified portfolio on the factor is 1.25. The variance of returns on the

well-diversified portfolio is approximately

A. 3.6%.

B. 6.0%.

C. 7.3%.

D. 14.1%.

Which of the following are possible explanations for the term structure of interest rates?

A. The expectations theory

B. The liquidity preference theory

C. Modern portfolio theory

D. The expectations theory and the liquidity preference theory

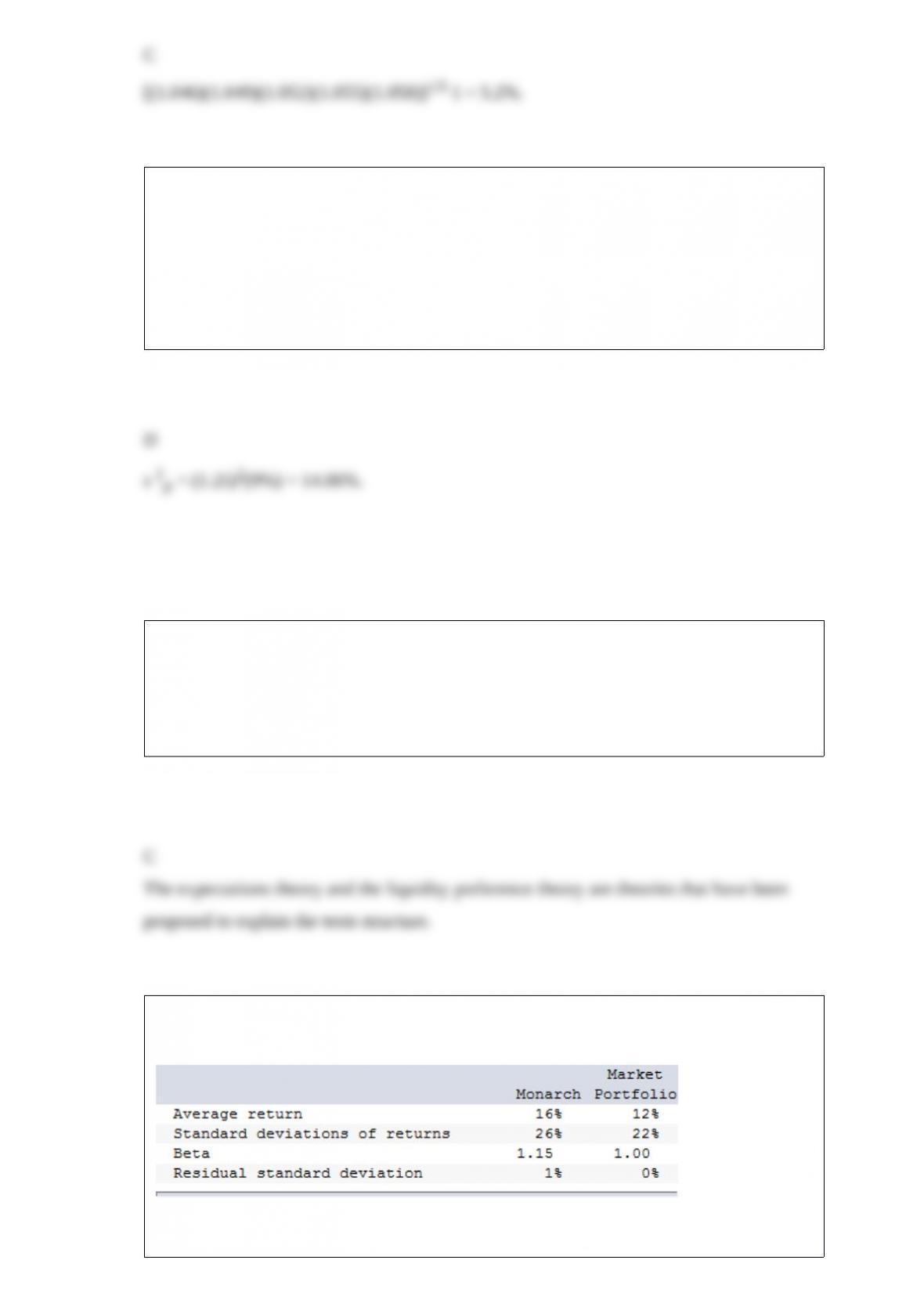

The following data are available relating to the performance of Monarch Stock Fund

and the market portfolio:

The risk-free return during the sample period was 4%.

Calculate Treynor’s measure of performance for Monarch Stock Fund.

A. 10.40%

B. 8.80%

C. 44.00%

D. 50.00%

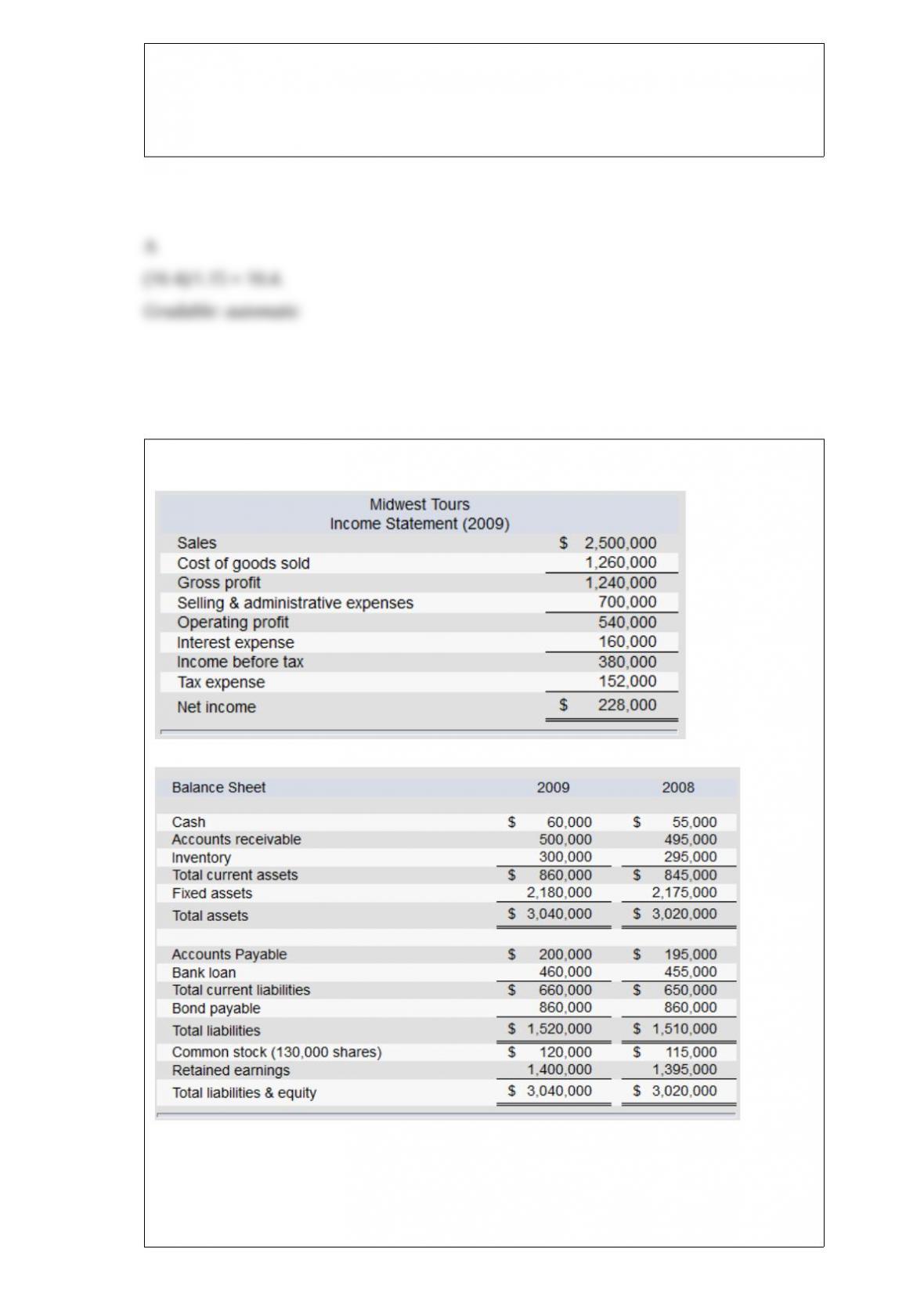

The financial statements of Midwest Tours are given below.

Note: The common shares are trading in the stock market for $36 each.

Refer to the financial statements of Midwest Tours. The firm’s asset turnover ratio for

2009 is

A. 1.86.

B. 0.63.

C. 0.83.

D. 1.63.

If a firm’s beta was calculated as 1.35 in a regression equation, a commonly-used

adjustment technique would provide an adjusted beta of

A. equal to 1.35.

B. between 0.0 and 1.0.

C. between 1.0 and 1.35.

D. greater than 1.35.

E. zero or less.

The maximum loss a buyer of a stock call option can suffer is equal to

A. the striking price minus the stock price.

B. the stock price minus the value of the call.

C.the call premium.

D. the stock price.

E. None of the options are correct.

The utility score an investor assigns to a particular portfolio, other things equal,

A. will decrease as the rate of return increases.

B. will decrease as the standard deviation decreases.

C. will decrease as the variance decreases.

D. will increase as the variance increases.

E. will increase as the rate of return increases.

Regarding hedge fund incentive fees, hedge fund managers ______ if the portfolio

return is very large and ______ if the portfolio return is negative.

A. get nothing; get nothing

B. refund the fee; get the fee

C. get the fee; lose nothing except the incentive fee

D. get the fee; lose the management fee

E. None of the options are correct.

A mutual fund had NAV per share of $26.25 on January 1, 2016. On December 31 of

the same year, the fund’s rate of return for the year was 16.4%. Income distributions

were $1.27, and the fund had capital gain distributions of $1.85. Without considering

taxes and transactions costs, what ending NAV would you calculate?

A. $27.44

B. $33.88

C. $24.69

D. $42.03

E. $16.62

Workers who change jobs may wind up with lower pension benefits at retirement than

otherwise identical workers who stay with the same employer, even if the employers

have defined benefit plans with the same finalpay benefit formula. This is referred to as

A. an accumulated benefit obligation.

B. an unfunded liability.

C. immunization.

D. indexation.

E. the portability problem.

In the APT model, what is the nonsystematic standard deviation of an equally-weighted

portfolio that has an

average value of σ(ei ) equal to 18% and 250 securities?

A. 1.14%

B. 625%

C. 0.5%

D. 3.54%

E. 3.16%

With regard to a futures contract, the long position is held by

A. the trader who bought the contract at the largest discount.

B. the trader who has to travel the farthest distance to deliver the commodity.

C. the trader who plans to hold the contract open for the lengthiest time period.

D. the trader who commits to purchasing the commodity on the delivery date.

E. the trader who commits to delivering the commodity on the delivery date.

At issue, coupon bonds typically sell

A. above par value.

B. below par value.

C. at or near par value.

D. at a value unrelated to par.

E. None of the options are correct.

An overpriced security will plot

A. on the security market line.

B. below the security market line.

C. above the security market line.

D. either above or below the security market line depending on its covariance with the

market.

E. either above or below the security-market line depending on its standard deviation.

At expiration, the time value of an in-the-money call option is always

A. equal to zero.

B. positive.

C. negative.

D. equal to the stock price minus the exercise price.

E. None of the options are correct.

A coupon bond that pays interest semi-annually has a par value of $1,000, matures in

six years, and has a yield to maturity of 9%. The intrinsic value of the bond today will

be __________ if the coupon rate is 9%.

A. $922.78

B. $924.16

C. $1,075.80

D. $1,000.00

E. None of the options are correct.

The factor F in the APT model represents

A. firm-specific risk.

B. the sensitivity of the firm to that factor.

C. a factor that affects all security returns.

D. the deviation from its expected value of a factor that affects all security returns.

E. a random amount of return attributable to firm events.

A decrease in the basis will __________ a long hedger and __________ a short hedger.

A. hurt; benefit

B. hurt; hurt

C. benefit; hurt

D. benefit; benefit

E. benefit; have no effect upon

Consider the following probability distribution for stocks C and D:

The coefficient of correlation between C and D is

A. 0.67.

B. 0.50.

C. –0.50.

D. –0.67.

E. None of the options are correct.

__________ can lead investors to misestimate the true probabilities of possible events

or associated rates of return.

A. Information processing errors

B. Framing errors

C. Mental accounting errors

D. Regret avoidance