As of December 2012, the number of nationally chartered banks was greater than the

number of state chartered banks.

Answer:

Although life insurance companies also provide health and accident insurance, they

underwrite less than 35% of all health insurance policies.

Answer:

Off-balance-sheet activities are an important source of fee income for many FIs.

Answer:

Which of the following statements is NOT TRUE?A. The Federal Reserve operates the

Fedwire electronic payments system while CHIPS is a private network.

B. Fedwire is used to transfer funds from the Fed to the banking system while CHIPS

is used to make interbank funds transfers.

C. The Fed guarantees all payments on Fedwire while CHIPS transfers are provisional

until settlement.

D. Large daylight overdrafts are incurred on both Fedwire and CHIPS.

E. Fedwire has a fee for daylight overdrafts but CHIPS does not.

Answer:

The passage of legislation to ensure that FIs are meeting the needs of their local

communities is an example of entry regulation.

Answer:

One reason to include demand deposits when estimating a bank’s repricing gap is

because rising interest rates could lead to high withdrawals.

Answer:

In general, money center banks are exposed to less liquidity risk than smaller, regional

banks.

Answer:

The Volker Rule is intended to reduce market risk at depository institutions.

Answer:

Research has shown that current-year income for an FI is rarely affected by the decision

to sell loans from their balance sheet.

Answer:

Included in the Moody’s Analytics model are recovery rates on defaulted loans.

Answer:

Book value accounting systems recognize the impact of interest rate problems sooner

than credit risk problems.

Answer:

A lower level of equity capital increases the risk of insolvency to a financial institution.

Answer:

Unanticipated withdrawals by liability holders are a major part of liquidity risk.

Answer:

The use of LCs and SLCs may result in an FI having a higher concentration ratio than

desired for a particular industry.

Answer:

Research shows that there is a significant reduction in risk achieved by investing in as

few as 8 different securities.

Answer:

A mortgage pass-through strip security is a special type of collateralized mortgage

obligation (CMO).

Answer:

Because the increased level of financial market integration has increased the speed with

which interest rate changes are transmitted among countries, control of U.S. interest

rates by the Federal Reserve is more difficult and less certain.

Answer:

Market value accounting often is said to be difficult to implement because of the

amounts of nontraded assets.

Answer:

Export revenue may be highly variable due to the quantity of exports and the prices that

may be realized on the exported products.

Answer:

Simultaneously buying a bond and a put option on a bond produces the same payoff as

buying a call option on a bond.

Answer:

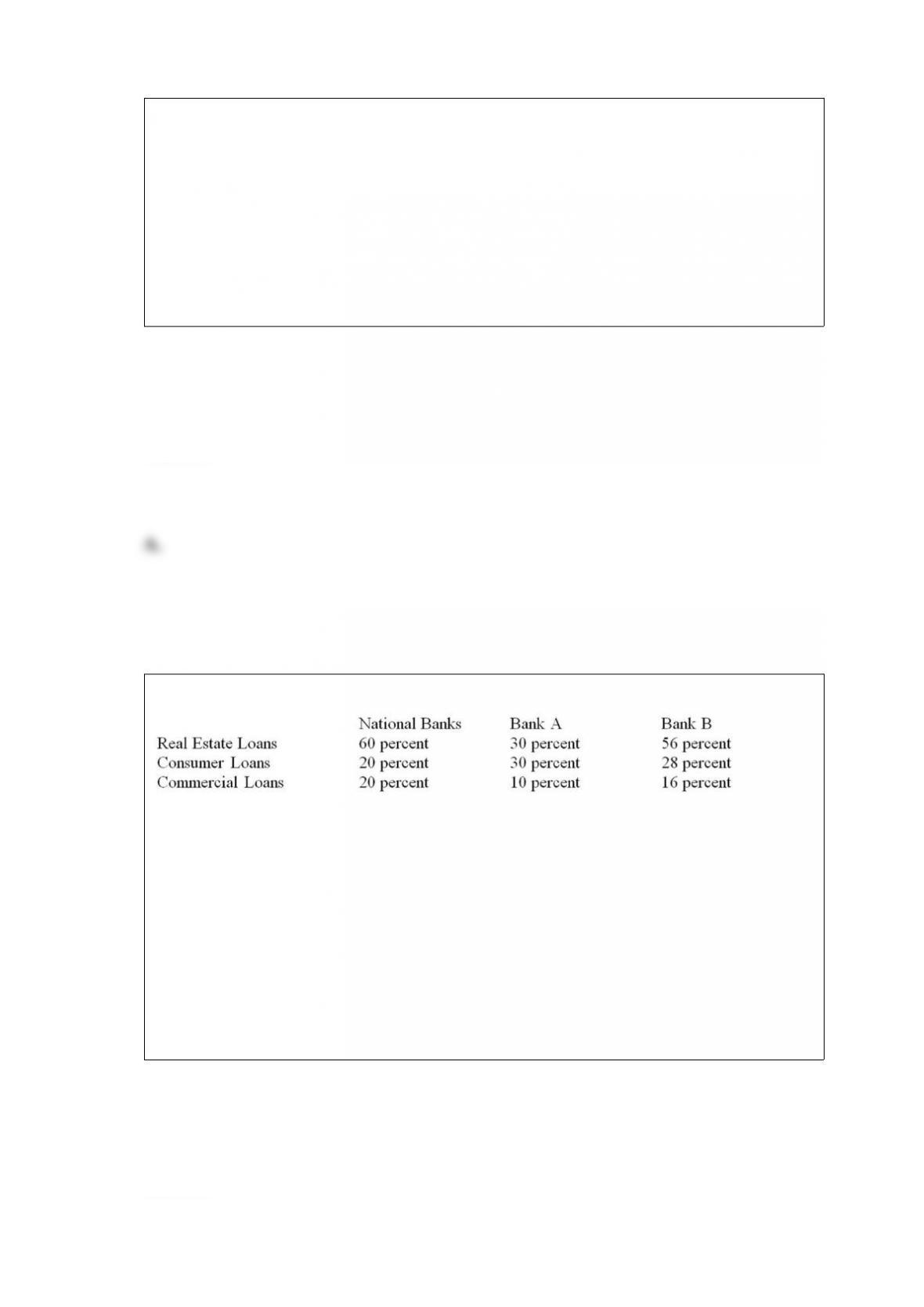

Comparing the loan mix of an individual FI to a national benchmark loan mix is useful

in determining the extent that the individual FI may differ from an efficient portfolio

composition.

Answer:

A major reason for the deterioration of the deposit insurance funds in the 1980s was the

downturn in the technology, manufacturing, and real estate industries.

Answer:

Most mortgage-backed bond issues conducted by depository institutions are

under-collateralized.

Answer:

The liquidity index should be a number that is either greater than one or less than zero.

Answer:

In the U.S., the Glass-Steagall Act limited the integration of commercial banking and

securities activities.

Answer:

At market rates substantially below the mortgage coupon rate of an interest-only (IO)

mortgage-backed strip, the prepayment effect will dominate the discount effect resulting

in a decrease in the price of the IO strip.

Answer:

Forward contracts are individually negotiated and, therefore, can be unique.

Answer:

Funds transferred on CHIPS are settled at the end of the day.

Answer:

Tie-ins and third-party loans are prohibited by current bank regulations.

Answer:

Purchasing power parity is based on the difference in productive output (GDP) that

exists between two countries.

Answer:

Excessive illiquidity can result in an FI’s inability to meet required payments on liability

claims and, at the extreme, in insolvency.

Answer:

MMDAs are considered to be more liquid than demand deposits and NOW accounts.

Answer:

The primary objective of the Reigle-Neal Act (1994) was to ease branching across state

lines by banks.

Answer:

As of 2012, there were over 4,900 securities firms in operation.

Answer:

Direct foreign investment and foreign portfolio investment both can be beneficial to an

FI because of imperfectly correlated returns with domestic investments.

Answer:

Because MMDAs are in direct competition with MMMFs, the withdrawal rate is

affected by the relative amount of explicit interest paid on these accounts.

Answer:

Financial intermediaries are A. funds surplus units, because they exist to make money.

B. funds deficit units, because they must pay heavy regulatory fees and taxes.

C. funds surplus units, because they hold large portfolios of financial securities.

D. funds deficit units, because they must comply with minimum capital requirements.

E. neither funds surplus nor deficit units.

Answer:

What is the leverage-adjusted duration gap?A. 0.605 years.

B. 0.956 years.

C. 0.360 years.

D. 0.436 years.

E. 0.189 years.

Answer:

Bank of the Atlantic has liabilities of $4 million with an average maturity of two years

paying interest rates of 4.0 percent annually. It has assets of $5 million with an average

maturity of 5 years earning interest rates of 6.0 percent annually.

What is the maximum interest rate that it can refinance its $4 million liability and still

break even on its net interest income in dollars?A. 6.5 percent.

B. 7.0 percent.

C. 7.5 percent.

D. 8.0 percent.

E. 8.5 percent.

Answer:

Can the FI immunize itself from interest rate risk exposure by setting the maturity gap

equal to zero?A. Yes, because with a maturity gap of zero the change in the market

value of assets exactly offsets the change in the market value of liabilities.

B. No, because with a maturity gap of zero, the change in the market value of assets

exactly offsets the change in the market value of liabilities.

C. No, because the maturity model does not consider the timing of cash flows.

D. Yes, because the timing of cash flows is not relevant to immunization against

interest rate risk exposure.

E. No, because a representative bank will always have a positive maturity gap.

Answer:

Which of the following is one of the characteristics of household mutual fund owners as

of 2012? A. The typical fund-owning household has $120,000 invested.

B. 52 percent of the families are headed by someone without a college degree.

C. The median age of mutual fund holders is 51.

D. 21 percent of investors that conducted equity fund transactions used the internet.

E. All of the above.

Answer:

The weekend game is A. a strategy to reduce bank interest rate risk exposure.

B. a strategy to reduce bank liquidity risk exposure.

C. a strategy to reduce the cost of meeting reserve requirements.

D. the buying and selling of Fed funds late Friday afternoon.

E. the triple witching effect on the third Friday of the month.

Answer:

The concept of constrained optimization facing an FI manager involving the minimum

amount of liquid reserve assets required by regulators may A. penalize the FI if the

minimum amount is less than the amount warranted by the actual withdrawal risk.

B. benefit the FI if the minimum amount is more than is warranted by actual

withdrawal risk.

C. lead to increased withdrawals by depositors that do not meet the minimum

requirement.

D. assist the FI manager by providing an optimal target amount of reserves that will

exactly match withdrawal expectations.

E. None of the above.

Answer:

What is the end-of-year profit or loss to the bank if in one year Canadian bond rates

increase to 7.538 percent? (Assume no change in either current U.S. interest rates or

current exchange rates, US $0.78493/C $1.) A. Loss of US $5,000.

B. Profit of US $15,000.

C. Loss of C $119,000.

D. Profit of C $50,000.

E. Loss of C $50,000.

Answer:

What does Gotbucks Bank’s 91-day gap positions reveal about the bank management’s

interest rate forecasts and the bank’s interest rate risk exposure?A. The bank is exposed

to interest rate decreases and positioned to gain when interest rates decline.

B. The bank is exposed to interest rate increases and positioned to gain when interest

rates decline.

C. The bank is exposed to interest rate increases and positioned to gain when interest

rates increase.

D. The bank is exposed to interest rate decreases and positioned to gain when interest

rates increase.

E. Insufficient information.

Answer:

Assume that the T-Bills can only be sold at a 10 percent discount, what is the net

liquidity of the bank given this information? A. $6.5 million.

B. $11.5 million.

C. $16.5 million.

D. $20.5 million.

E. $21.5 million.

Answer:

What is the market share of Bank 2? A. 12.5 percent.

B. 37.5 percent.

C. 25.0 percent.

D. 62.5 percent.

E. 50.0 percent.

Answer:

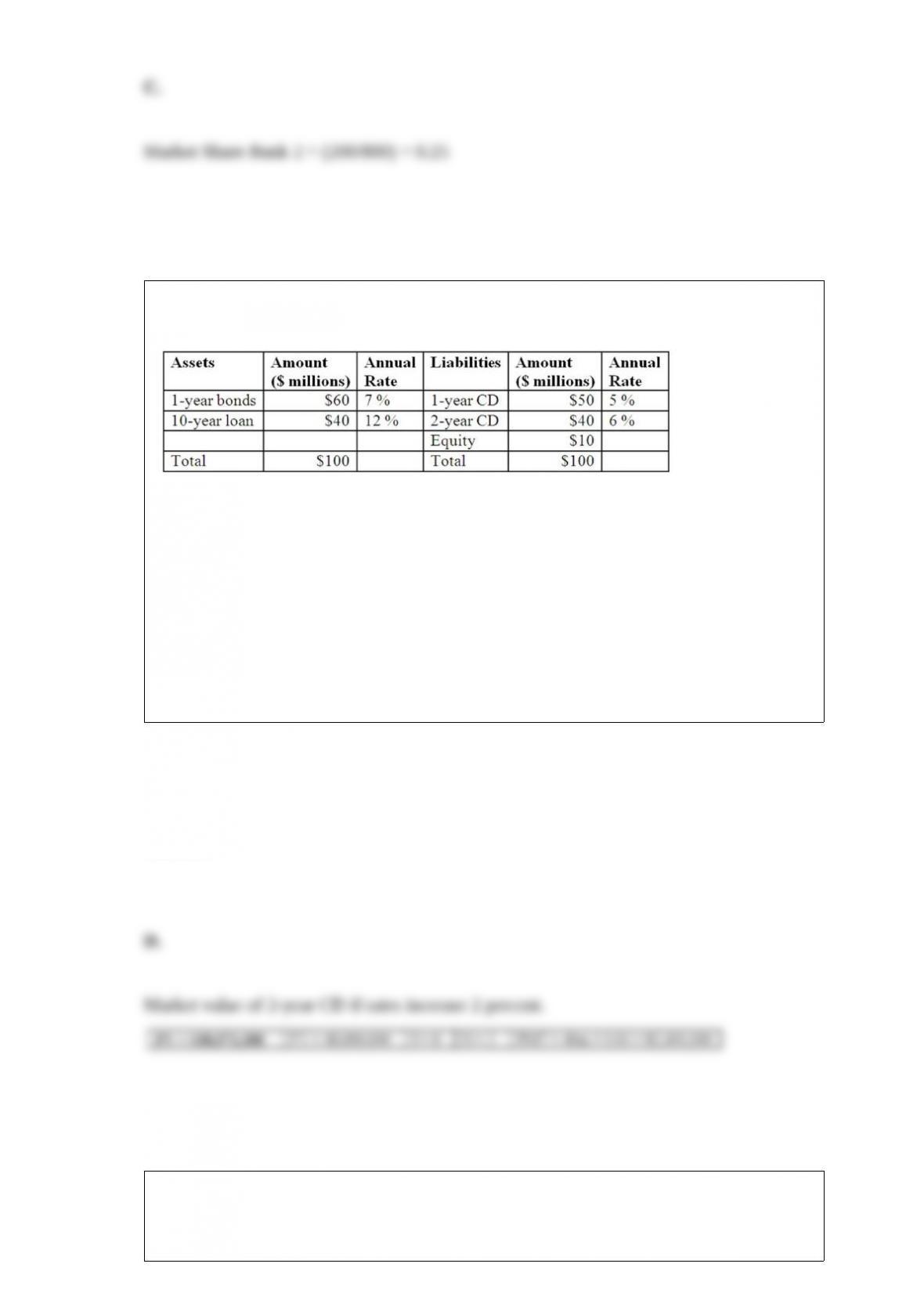

Hadbucks National Bank current balance sheet appears below. All assets and liabilities

are currently priced at par and pay interest annually.

What is market

value of the two-year CD if all market interest rates increase by 2 percent? A. $40.381

million.

B. $39.626 million.

C. $40.000 million.

D. $38.573 million.

E. $40.769 million.

Answer:

The Herfindahl-Hirschman Index (HHI) is a measure of A. market concentration.

B. profitability.

C. market performance.

D. annual sector growth.

E. investor reaction.

Answer:

When are the standby letters of credit used in swap agreements?A. When the

counterparty is perceived to be of significantly lower credit quality than the other party.

B. Where the swap agreement is made between parties of equal credit standing.

C. Where the swap agreement is made between high-quality counterparties.

D. When one party posts collateral in lieu of default.

E. When the no-arbitrage condition does not hold good.

Answer:

Which of the following is NOT a type of finance company? A. Sales finance

institutions.

B. Personal credit institutions.

C. Business credit institutions.

D. Captive finance company.

E. All of the above are types of finance companies.

Answer:

As banks and other FIs increase the use of technology, an unintended consequence may

be thatA. cost savings are seldom realized.

B. customers are driven away because they still want to interact with a person for

certain transactions.

C. innovation of new products tends to take longer periods of time to attract new

customers.

D. the marginal cost of adding new customers tends to increase at an increasing rate.

E. None of the above.

Answer:

What is the total DEAR of Sumitomo’s trading portfolio if the correlation among assets

is assumed to be 1.0? A. -$100,000.

B. -$291,548.

C. -$350,000.

D. -$380,789.

E. -$400,000.

Answer:

The U.S.A. Patriot Act requires firms to implement processes to deter money

laundering.

Answer:

Which of the following is NOT a retail banking service?A. Check deposit services.

B. Point of sale/debit cards.

C. Telephone bill paying services.

D. Pre-authorized debits/credits.

E. Automated teller machines.

Answer:

What is Bank A’s standard deviation of its asset allocation proportions relative to the

national banks average? Use the formula in the textbook.A. 7.23 percent.

B. 10.89 percent.

C. 18.71 percent.

D. 19.15 percent.

E. 27.36 percent.

Answer:

What is the duration of a 5-year par value zero coupon bond yielding 10 percent

annually? A. 0.50 years.

B. 2.00 years.

C. 4.40 years.

D. 5.00 years.

E. 4.05 years.

Answer:

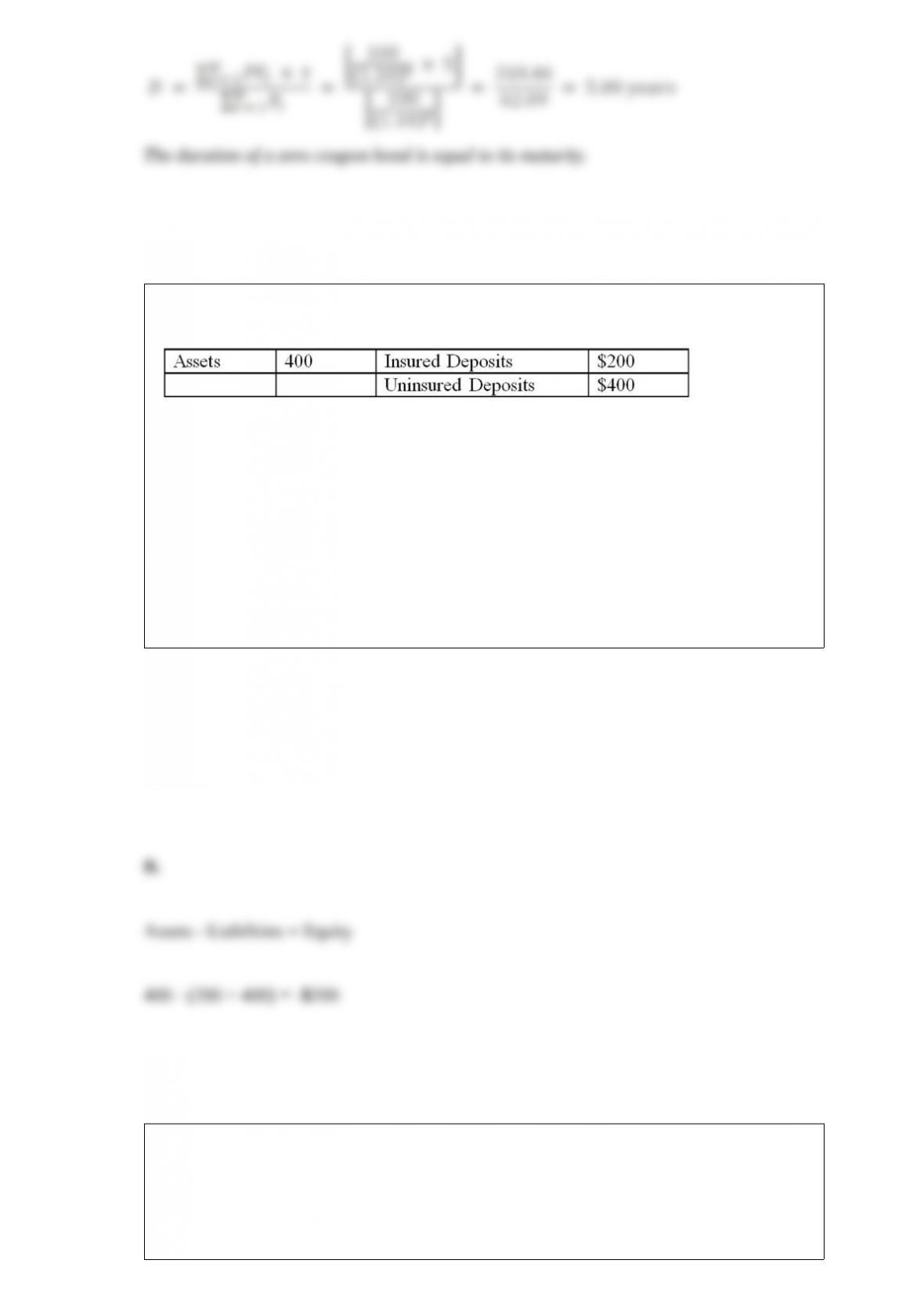

The following market value balance sheet of a failed bank ($ millions)

What is the market value of capital?A. $200 million.

B. -$200 million.

C. $0.

D. $400 million.

E. $600 million.

Answer:

A buyer of a loan participation is exposed to A. risk exposure to the original borrower

defaulting.

B. risk exposure to the failure of the selling bank.

C. moral hazard problems because the borrower is no longer monitored by the seller.

D. Answers A and B only.

E. Answers A and C only.

Answer:

Which of the following is a reason for an FI to sell a residential real estate loan rather

than securitize it through GNMA?A. The loan is too large to meet securitization

standards.

B. The loan is not insured by FHA or guaranteed by the VA.

C. The loan recipient’s income cannot be verified.

D. The loan carries a non-standard adjustable interest rate.

E. All of the above.

Answer:

If the firm commitment price is $15 and one million shares are sold in the primary

market for $15.50 and then resold in the secondary market for $15.75, what is the

underwriter’s profit/loss? A. -$500,000.

B. $500,000.

C. $750,000.

D. -$750,000.

E. 0

Answer:

Calculation of the “add-on” to the risk-based capital ratio to measure market risk A.

may be done using the Basic Indicator Approach.

B. may be done using the standardized model proposed by regulators.

C. may be done using the DI’s own internal market risk model.

D. Answers A and B only.

E. Answers B and C only.

Answer:

What is the maximum yield change expected if a 98 percent confidence (one-tailed)

limit is used?A. 3.30%.

B. 20.0%.

C. 33.0%.

D. 39.2%.

E. 46.6%.

Answer:

On loans fully secured by physical, non-real estate loans, the Basel Committee has set a

loss given defaults (LGD) rate of A. 15 percent

B. 25 percent

C. 40 percent

D. 45 percent

E. 60 percent

Answer:

Vulture funds are A. management consulting firms that employ turn-around specialists.

B. portfolios consisting of stakes in distressed companies.

C. mutual funds that grow by acquiring their competitors.

D. mutual funds that invest only in highly-leveraged transactions.

E. companies offering burial insurance contracts.

Answer:

Which of the following is NOT a key characteristic of loans sold in the short-term loan

sale market? A. Issued as a secured loan.

B. Loans to investment grade borrowers or better.

C. Issued with a fixed rate.

D. Sold in units of $1 million and up.

E. Issued for 90 days or less.

Answer:

The long-term mutual fund sector includes A. money market mutual funds.

B. equity funds.

C. bond funds.

D. Answers B and C only.

E. All of the above.

Answer:

Your U.S. bank issues a one-year U.S. CD at 5 percent annual interest to finance a C

$1.274 million (Canadian dollar) investment in two-year, fixed rate Canadian bonds

selling at par and paying 7 percent annually. You expect to liquidate your position in

one year. Currently, spot exchange rates are US $0.78493 per Canadian dollar.

Your position is exposed to A. interest rate risk only.

B. credit risk only.

C. exchange rate risk only.

D. interest rate and exchange rate risk only.

E. interest rate risk, exchange rate risk, and credit risk.

Answer:

An FI offers a $2,500 minimum balance NOW account paying 4 percent annual interest,

and there are no service charges as long as the customer maintains the minimum

balance. The customer maintains a balance of $5,000, and averages 750 checks per

year. Each check has a processing cost to the FI of $0.15. What is the annual gross

interest return on this account to the customer? A. $112.50.

B. $100.00.

C. $312.50.

D. $137.50.

E. $212.50.

Answer:

The portfolio of a bank that contains assets and liabilities that are relatively illiquid and

held for longer holding periods A. is the trading portfolio.

B. is the investment portfolio.

C. contains only long term derivatives.

D. is subject to regulatory risk.

E. cannot be differentiated on the basis of time horizon and liquidity.

Answer: