1) the present exchange rate is c$1 = us$.77. the 1-year futures rate is c$1 = us$.73. the

yield on a 1-year u.s. bill is 4%. a yield of __________ on a 1-year canadian bill will

make investors indifferent between investing in the u.s. bill and the canadian bill.

a.9.7%

b.2.9%

c.2.8%

d.2%

2) an example of a derivative security is _________.

a.a common share of general motors

b.a call option on intel stock

c.a ford bond

d.a u.s. treasury bond

3) which strategy benefits from upside price movement and has some protection should

the price of the security fall?

a.bull spread

b.long put

c.short call

d.straddle

4) kara’s kittens typically produces and sells at its optimal (lowest per-unit cost) level of

30 scratching posts per week. kara’s also maintains an inventory of 20 scratching posts.

if prices are sticky and there is a positive demand shock this week resulting in demand

for 40 scratching posts, we would expect kara’s to:

a.sell the additional scratching posts out of its inventory and rebuild the inventory later

when a negative demand shock occurs.

b.permanently expand production to 40 scratching posts per week.

c.raise prices on scratching posts.

d.introduce a new line of scratching posts.

5) an investor has a long time horizon and desires to earn the market rate of return.

however, the investor will need to withdraw funds each year from her investment

portfolio. the biggest constraint a planner would face with this client is a ___________

constraint.

a.tax

b.risk-tolerance

c.liquidity

d.social

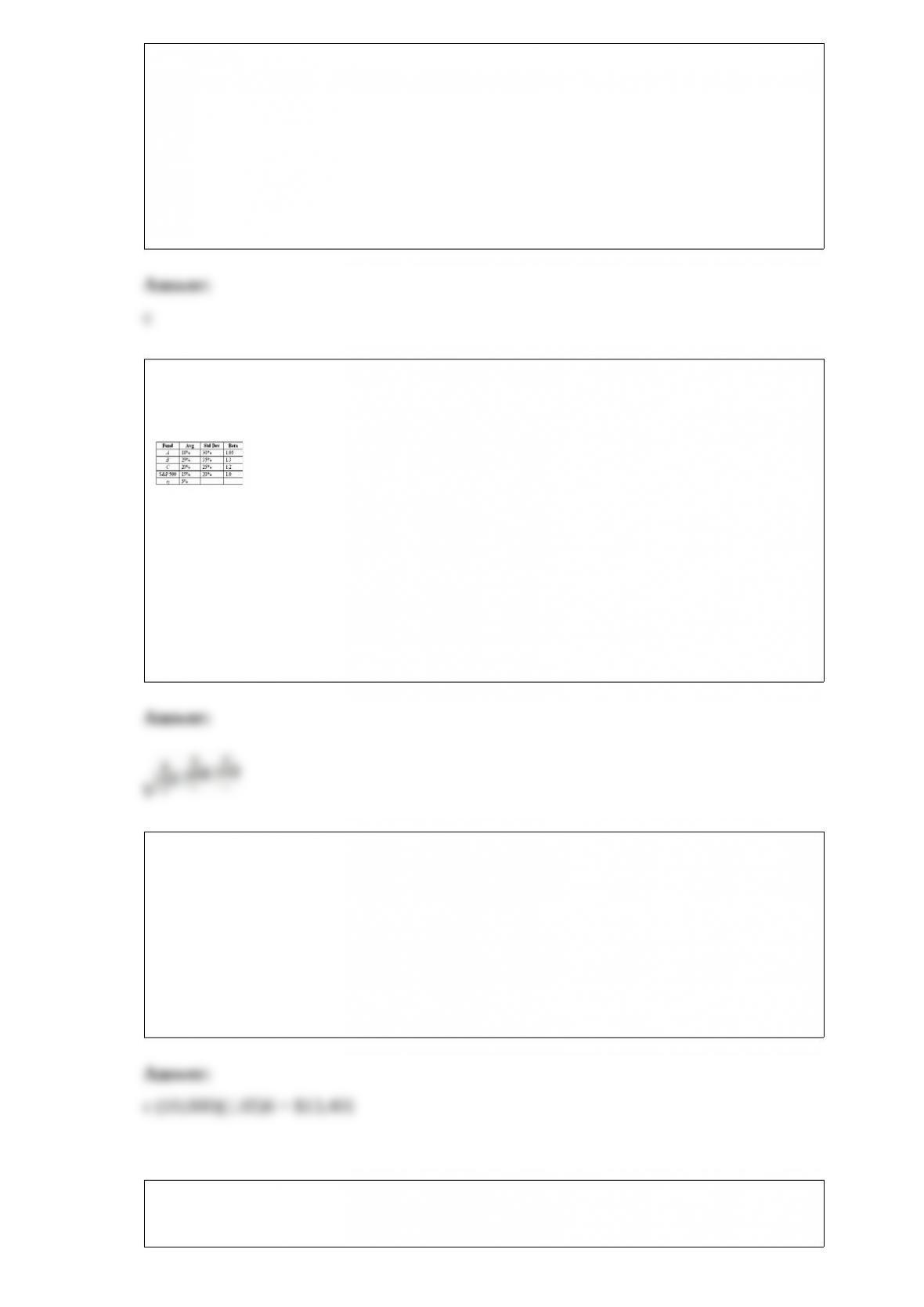

6) the risk-free rate, average returns, standard deviations, and betas for three funds and

the s&p 500 are given below.

if these portfolios are subcomponents that make up part of a well-diversified portfolio,

then portfolio ______ is preferred.

a.a

b.b

c.c

d.s&p 500

use the treynor measure. portfolio b is preferred.

7) you have purchased a guaranteed investment contract (gic) from an insurance firm

that promises to pay you a 5% compound rate of return per year for 6 years. if you pay

$10,000 for the gic today and receive no interest along the way, you will get

__________ in 6 years (to the nearest dollar).

a.$12,565

b.$13,000

c.$13,401

d.$13,676

8) when demand shocks lead to recessions, it is mainly due to:

a.price inflexibility.

b.the inability of government policy to affect demand.

c.unexpected changes in the supply of goods and services.

d.government regulations that prevent firms from adjusting output in response to the

shocks.

9) which of the following is a true statement?

a.the actual value of a call option is greater than its intrinsic value prior to expiration.

b.the intrinsic value of a call option is always greater than its time value prior to

expiration.

c.the intrinsic value of a call option is always positive prior to expiration.

d.the intrinsic value of a call option is greater than its actual value prior to expiration.

10) the value of a call option increases with all of the following except ___________.

a.stock price

b.time to maturity

c.volatility

d.dividend yield

11) the asset universe is the _____________________.

a.set of investments in which an investment company can legally invest

b.existing set of assets the investment company currently owns in one or more of its

portfolios

c.list of assets approved by the investment committee that may be placed into the

investment company’s portfolio

d.market portfolio of all available risky assets

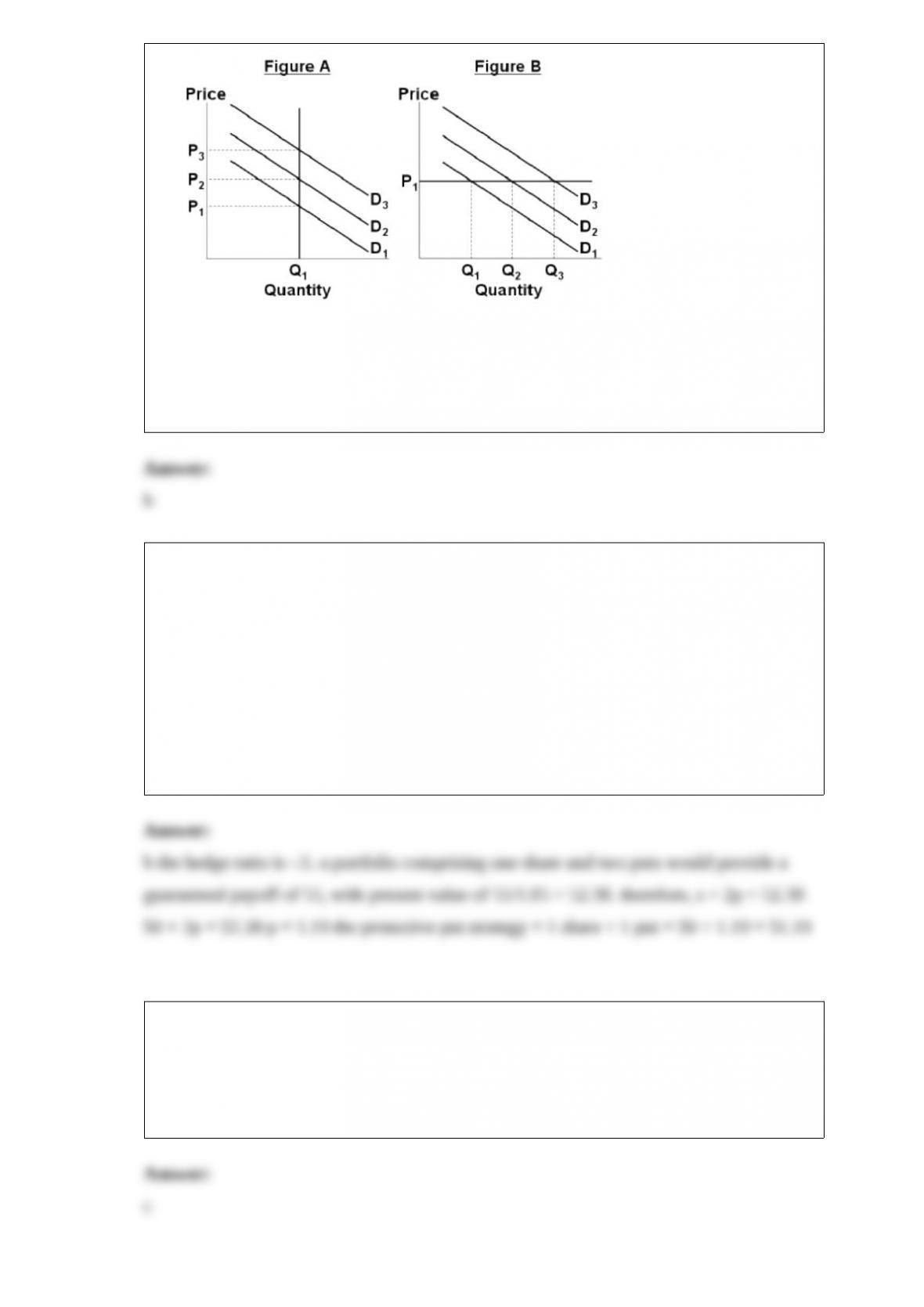

12)

refer to the above figures. which figure(s) represent a situation where prices are sticky?

a.a only.

b.b only.

c.both a and b.

d.neither a nor b.

13) you would like to hold a protective put position on the stock of avalon corporation

to lock in a guaranteed minimum value of $50 at year-end. avalon currently sells for

$50. over the next year, the stock price will increase by 10% or decrease by 10%. the

t-bill rate is 5%. unfortunately, no put options are traded on avalon co.

what would have been the cost of a protective put portfolio?

a.$48.81

b.$51.19

c.$52.38

d.$53.38

14) the intrinsic value of an out-of-the-money call option ___________.

a.is negative

b.is positive

c.is zero

d.cannot be determined

15) a possible limit on arbitrage activity that may allow behavioral biases to persist is

_______.

a.technical trends in prices

b.momentum effects

c.fundamental risk

d.trend reversals

16) joe bought a stock at $57 per share. the price promptly fell to $55. joe held on to the

stock until it again reached $57, and then he sold it once he had eliminated his loss. if

other investors do the same to establish a trading pattern, this would contradict

_______.

a.the strong-form emh

b.the weak-form emh

c.technical analysis

d.the semistrong-form emh

17) you would like to hold a protective put position on the stock of avalon corporation

to lock in a guaranteed minimum value of $50 at year-end. avalon currently sells for

$50. over the next year, the stock price will increase by 10% or decrease by 10%. the

t-bill rate is 5%. unfortunately, no put options are traded on avalon co.

suppose the desired put options with x = 50 were traded. what would be the hedge ratio

for the option?

a.-1

b.-.5

c..5

d.1