1) Cho, Elton, and Gruber tested the APT by examining the number of factors in the

return generating process and found that

a. Five factors were required using Roll-Ross procedures.

b. Six factors were present when using historical beta.

c. Fundamental betas indicated a need for three factors.

d. All of the above.

e. None of the above.

2) The error caused by not using the true market portfolio has become known as the

a. Portfolio deviation.

b. CAPM shift.

c. Benchmark error.

d. Market error.

e. Beta error.

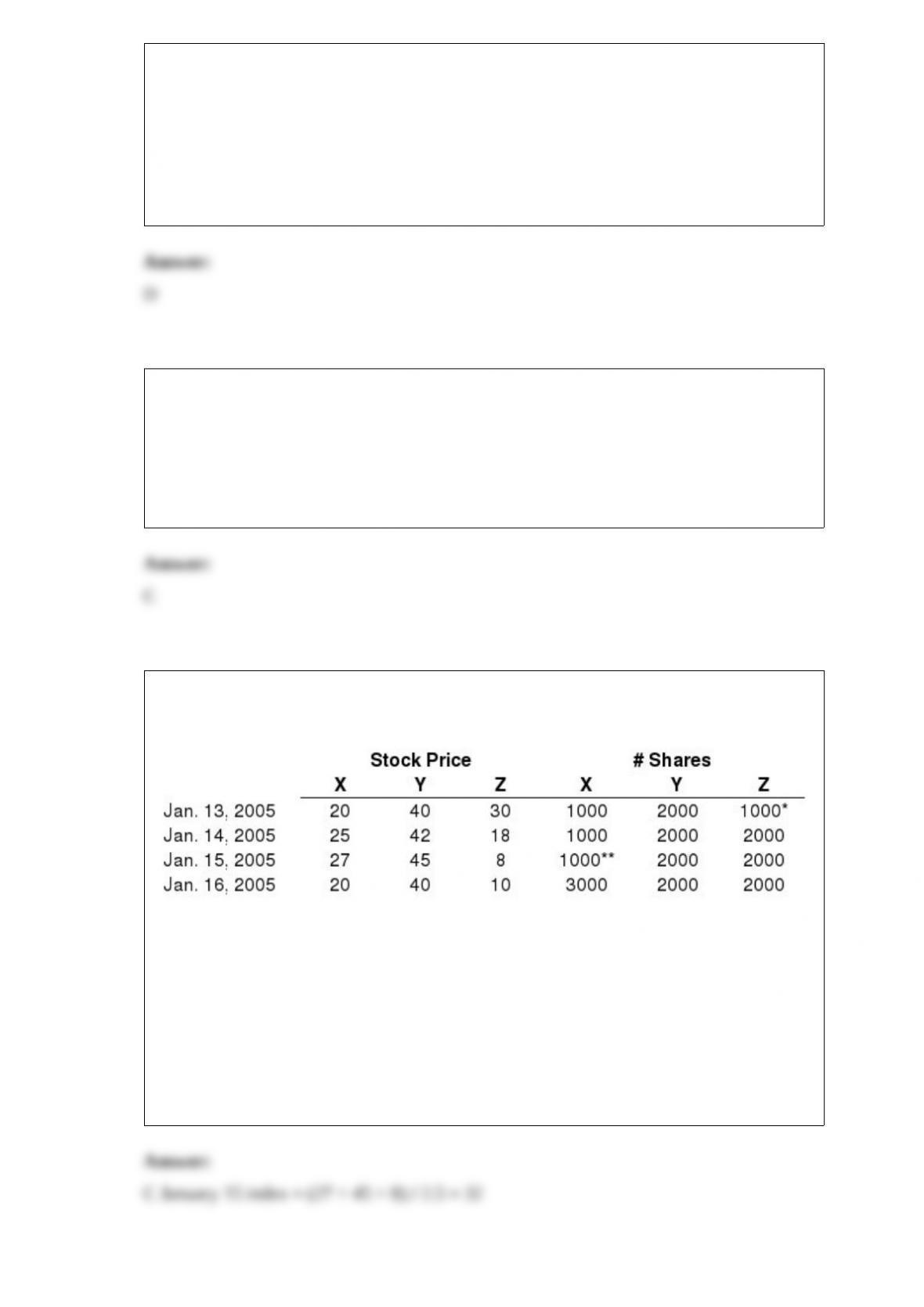

3) Exhibit 5.2

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

*2:1 Split on Stock Z after Close on Jan. 13, 2005

**3:1 Split on Stock X after Close on Jan. 15, 2005

The base date for index calculations is January 13, 2005

Refer to Exhibit 5.2. Calculate a price weighed average for January 15th.

a.30

b.36.13

c.32

d.34

e.None of the above

4) Exhibit 25.8

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Which of the following statements is true?

a. Sector/security selection hurt the portfolio performance; returns were 1.4% less than

if the manager invested the funds in stocks and bond indexes.

b. Sector/security selection improved the port-folio performance by 1.4%; each sector

return was higher than for index value.

c. Sector/security selection hurt the portfolio performance; returns were 6.8% less than

if the manager invested the funds in stocks and bond indexes.

d. Sector/security selection improved the port-folio performance by 6.8%; each sector

return was higher than for index return.

e. None of the above is a true statement.

5) Exhibit 23.4

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Black Gold Industries (BGI) is an independent oil producer with production capacity of

500,000 barrels per month. Due to the cost structure of the business, BGI needs to

receive $56.50 per barrel in order to remain solvent. On the other side of this situation

is Petrochemicals Unlimited (PU) which uses an average of 500,000 barrels of West

Texas crude oil in its normal production operations. The nature of PU’s business is such

that they will financially suffer if they have to pay more than an average of $57.80 per

barrel for oil over the next six years. To hedge against their exposure to volatile oil

prices, BI and PU contact a swap dealer to arrange the six-year oil swap described

below:

Refer to Exhibit 23.4. Barring default by PU or BGI, how much compensation does the

swap dealer receive each month?

a. $150,000

b. $210,000

c. $175,000

d. $250,000

e. None of the above

6) Suppose you consider investing $1,000 in a load fund which charges a fee of 2%, and

you expect the fund to earn 11% over the next year. Alternatively, you could invest in a

no-load fund with similar risk that is expected to earn 7% and charges a 1/2 percent

redemption fee. Which is better and by how much?

a. Funds are equal

b. No-load fund by $36.98

c. Load fund by $45.25

d. Load fund by $23.15

e. No-load fund by $15.52

7) The convexity of a bond is affected as follows:

a. Positively with maturity.

b. Positively with yield.

c. Inversely with coupon.

d. Choices a and b

e. Choices a and c

8) If, for the S&P Industrials Index, the profit margin was 0.30 and the equity turnover

ratio was 11, the ROE would be:

a. 0.033%

b. 3.300%

c. 33.00%

d. 36.70%

e. 333.00%

9) In a forward rate agreement (FRA) two parties agree today to a future exchange of

cash flows based on two different interest rates.

10) Exhibit 20.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

December futures on the S&P 500 stock index trade at 250 times the index value of

1187.70. Your broker requires an initial margin of 10% percent on futures contracts.

The current value of the S&P 500 stock index is 1178.

Suppose at expiration the futures contract price is 250 times the index value of 1170.

Disregarding transaction costs, what is your percentage return?

a. 1.87%

b. -0.68%

c. -14.90%

d. 10.36%

e. None of the above

11) Index movements are influenced by differential prices of the components in a(n)

a.Equally-weighted index.

b.Price-weighted index.

c.Unweighted index.

d.Value-weighted index.

e.All of the above

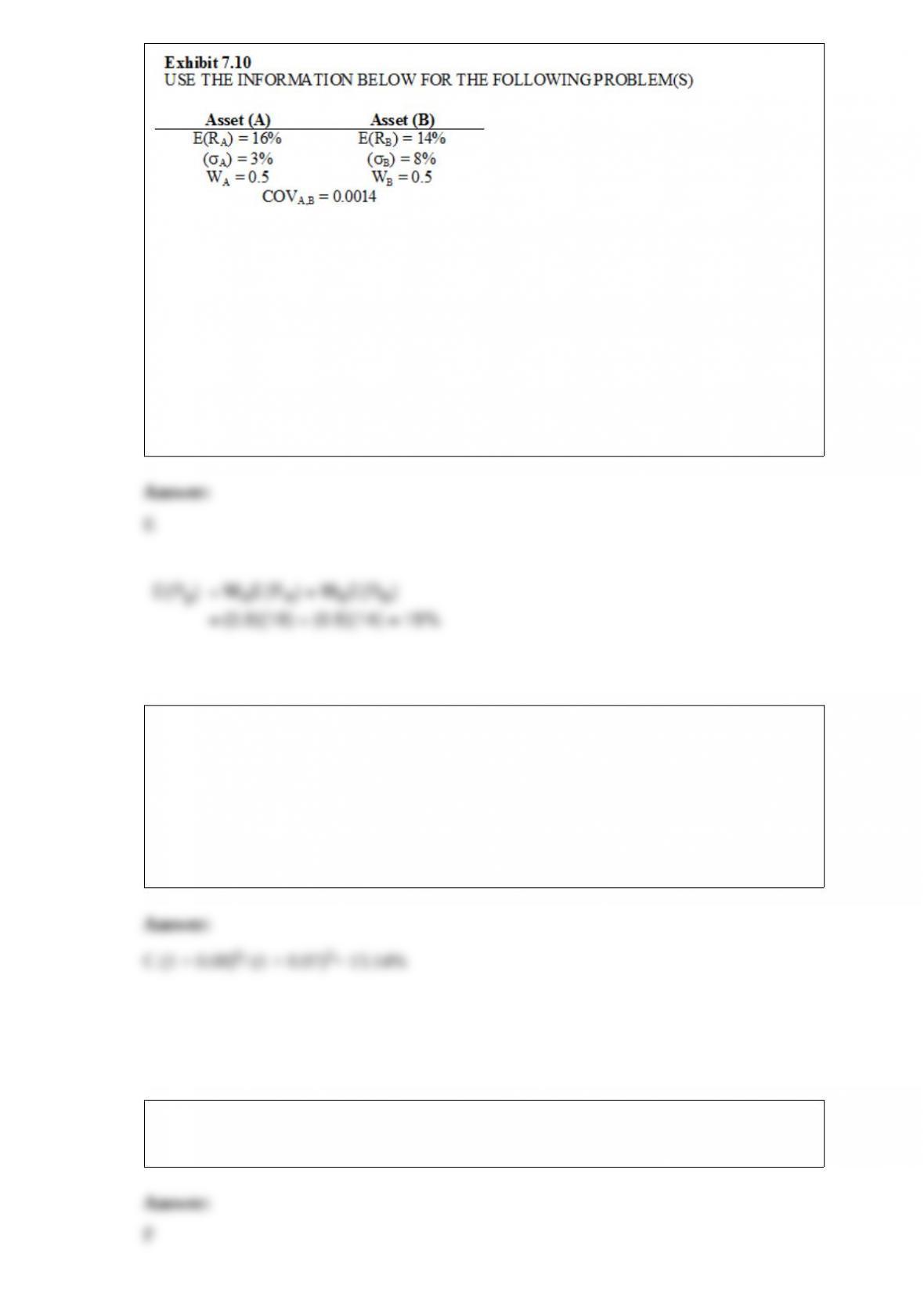

12)

Refer to Exhibit 7.10. What is the expected return of a portfolio of two risky assets if

the expected return E(Ri), standard deviation (si), covariance (COVi,j), and asset weight

(Wi) are as shown above?

a. 11%

b. 12%

c. 13%

d. 14%

e. 15%

13) Suppose the current 6 year spot rate is 8% and the current 5 year spot rate is 7%.

What is the one year forward rate in five years?

a. 12.62%

b. 11.58%

c. 13.14%

d. 14.65%

e. 15.14%

14) Contrary trading rules assert that investors tend to be wrong except at market peaks

and troughs.

15) The dividend growth models are only meaningful for companies that have a

required rate of return that exceeds their dividend growth rate.

16) The Morgan Stanley group index for Europe, Australia, and the Far East (EAFE) is

a price weighted index.

17) A substitution swap relies heavily on interest rate expectations.

18) A long strip position indicates that an investor is bullish but conservative.

19) Given an optimistic economic and stock-market outlook for a country, the investor

should underweight the allocation to this country in his/her portfolio.

20) The ability to retire at a certain age is a typical example of a long-term,

lower-priority goal.