Top Flight Stock currently sells for $53. A one-year call option with strike price of $58

sells for $10, and the risk-free interest rate is 5.5%. What is the price of a one-year put

with strike price of $58?

A. $10.00

B. $12.12

C. $16.00

D.$11.98

E. $14.13

The compensation from a CDS can come from

A. the CDS holder delivering the defaulted bond to the CDS issuer in return for the

bond’s par value.

B. the CDS issuer paying the swap holder the difference between the par value of the

bond and the bond’s market price.

C. the federal government paying off on the insurance claim.

D. the CDS holder delivering the defaulted bond to the CDS issuer in return for the

bond’s par value, and the CDS issuer paying the swap holder the difference between the

par value of the bond and the bond’s market price.

E . None of the options are correct.

___________ the return on a stock beyond what would be predicted from market

movements alone.

A. An irrational return is

B. An economic return is

C. An abnormal return is

D. None of the options are correct.

E. All of the options are correct.

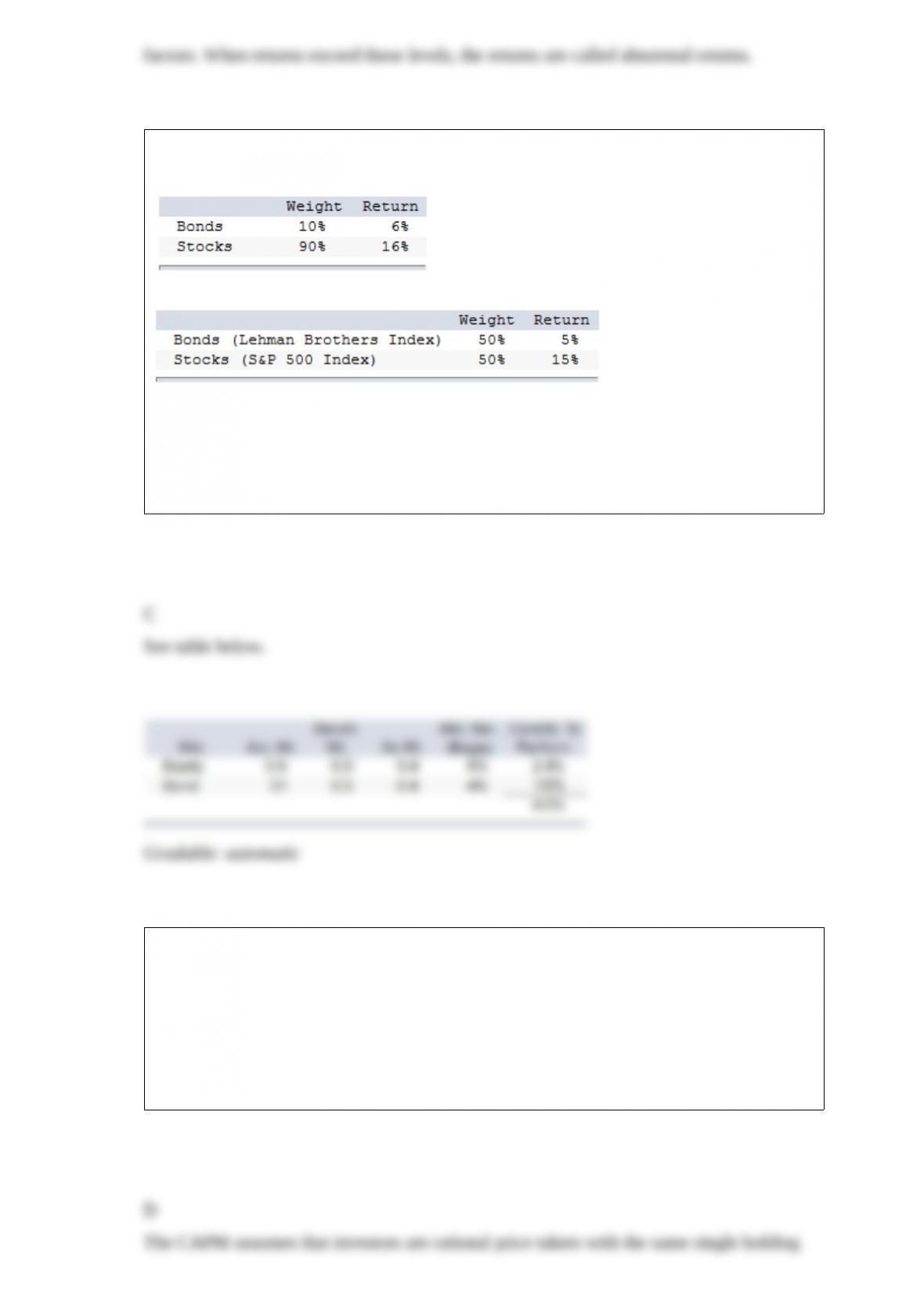

In a particular year, Aggie Mutual Fund earned a return of 15% by making the

following investments in the following asset classes:

The return on a bogey portfolio was 10%, calculated as follows:

The contribution of asset allocation across markets to the total excess return was

A. 1%.

B. 3%.

C. 4%.

D. 5%.

The capital asset pricing model assumes

A. all investors are rational.

B. all investors have the same holding period.

C. investors have heterogeneous expectations.

D. all investors are rational and have the same holding period.

E. all investors are rational, have the same holding period, and have heterogeneous

expectations.

The present exchange rate is C$ = U.S. $0.78. The 1-year future rate is C$ = U.S. $0.76.

The yield on a 1-year U.S. bill is 4%. A yield of __________ on a 1-year Canadian bill

will make an investor indifferent between investing in the U.S. bill and the Canadian

bill.

A. 2.4%

B. 1.3%

C. 6.4%

D. 6.7%

E. None of the options are correct.

In the Treynor-Black model,

A.portfolio weights are sensitive to large alpha values, which can lead to infeasible long

or short positions for

many portfolio managers.

B. portfolio weights are not sensitive to large alpha values, which can lead to infeasible

long or short positions

for many portfolio managers.

C. portfolio weights are sensitive to large alpha values, which can lead to the optimal

portfolio for most portfolio

managers.

D. portfolio weights are not sensitive to large alpha values, which can lead to the

optimal portfolio for most

Foreign exchange futures markets are __________, and the foreign exchange forward

markets are

__________.

A. informal; formal

B. formal; formal

C. formal; informal

D. informal; informal

E. organized; unorganized

An investor invests 30% of his wealth in a risky asset with an expected rate of return of

0.11 and a variance of

0.12 and 70% in a T-bill that pays 3%. His portfolio’s expected return and standard

deviation are __________

and __________, respectively.

A. 0.086; 0.242

B. 0.054; 0.104

C. 0.295; 0.123

D. 0.087; 0.182

E. None of the options are correct.

Consider the one-factor APT. The standard deviation of returns on a well-diversified

portfolio is 18%. The standard deviation on the factor portfolio is 16%. The beta of the

well-diversified portfolio is approximately

A. 0.80.

B. 1.13.

C. 1.25.

D. 1.56.

The growth in per share FCFE of FOX, Inc. is expected to be 15% per year for the next

three years, followed by a growth rate of 8% per year for two years. After this five-year

period, the growth in per share FCFE is expected to be 3% per year, indefinitely. The

required rate of return on FOX, Inc. is 13%. Last year’s per share FCFE was $1.85.

What should the stock sell for today?

A. $28.99

B. $24.47

C. $26.84

D. $27.74

E. $19.18

You sold short 100 shares of common stock at $45 per share. The initial margin is 50%.

At what stock price would you receive a margin call if the maintenance margin is 35%?

A. $50

B. $65

C. $35

D. $40

Suppose the 1-year risk-free rate of return in the U.S. is 5%. The current exchange rate

is 1 pound = U.S. $1.60. The 1-year forward rate is 1 pound = $1.57. What is the

minimum yield on a 1-year risk-free security in Britain that would induce a U.S.

investor to invest in the British security?

A. 2.44%

B. 2.50%

C. 7.00%

D. 7.62%

E. None of the options are correct.

A mutual fund had NAV per share of $16.75 on January 1, 2016. On December 31 of

the same year, the fund’s rate of return for the year was 26.6%. Income distributions

were $1.79, and the fund had capital gain distributions of $2.80. Without considering

taxes and transactions costs, what ending NAV would you calculate?

A. $17.44

B. $13.28

C. $14.96

D. $17.25

E. $16.62

Over the past year, you earned a nominal rate of interest of 12.5% on your money. The

inflation rate was 2.6%

over the same period. The exact actual growth rate of your purchasing power was

A. 9.15%.

B. 9.90%.

C. 9.65%.

D. 10.52%.

The current market price of a share of AT&T stock is $50. If a call option on this stock

has a strike price of $45, the call

A. is out of the money.

B. is in the money.

C. sells for a higher price than if the market price of AT&T stock is $40.

D. is out of the money and sells for a higher price than if the market price of AT&T

stock is $40.

E.is in the money and sells for a higher price than if the market price of AT&T stock is

$40.

Given a stock index with a value of $1,125, an anticipated dividend of $33, and a

risk-free rate of 4%, what should be the value of one futures contract on the index?

A. $1137.00

B. $1070.00

C. $993.40

D. $995.09

E. $1000.00

A coupon bond that pays interest semi-annually has a par value of $1,000, matures in

five years, and has a yield to maturity of 10%. The intrinsic value of the bond today will

be ________ if the coupon rate is 12%.

A. $922.77

B. $924.16

C. $1,075.80

D. $1,077.22

E. None of the options are correct.

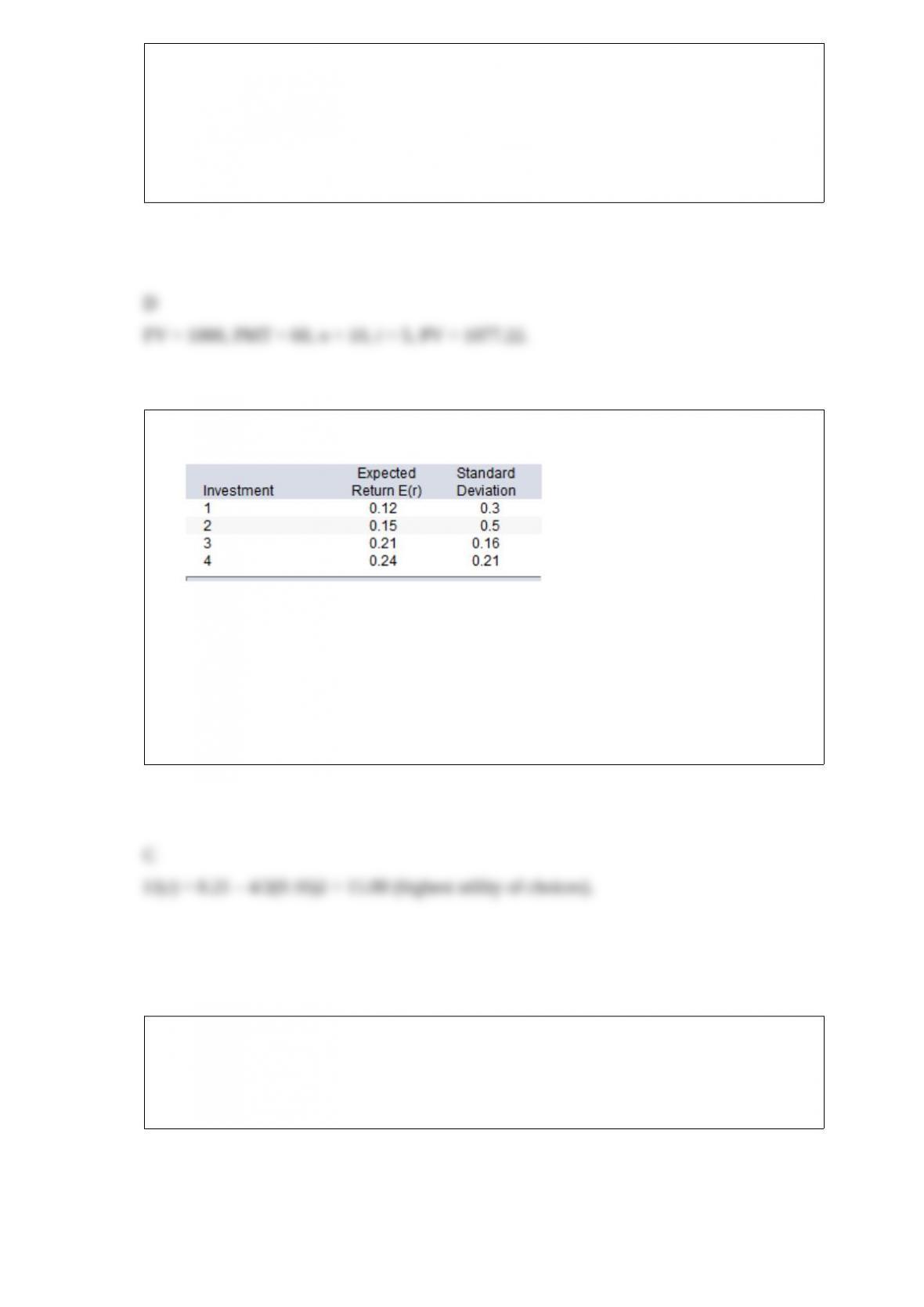

Use the below information to answer the following question.

U = E(r ) – (A/2)s2,where A = 4.0.

Based on the utility function above, which investment would you select?

A. 1

B. 2

C. 3

D. 4

E. Cannot be determined from the information given.

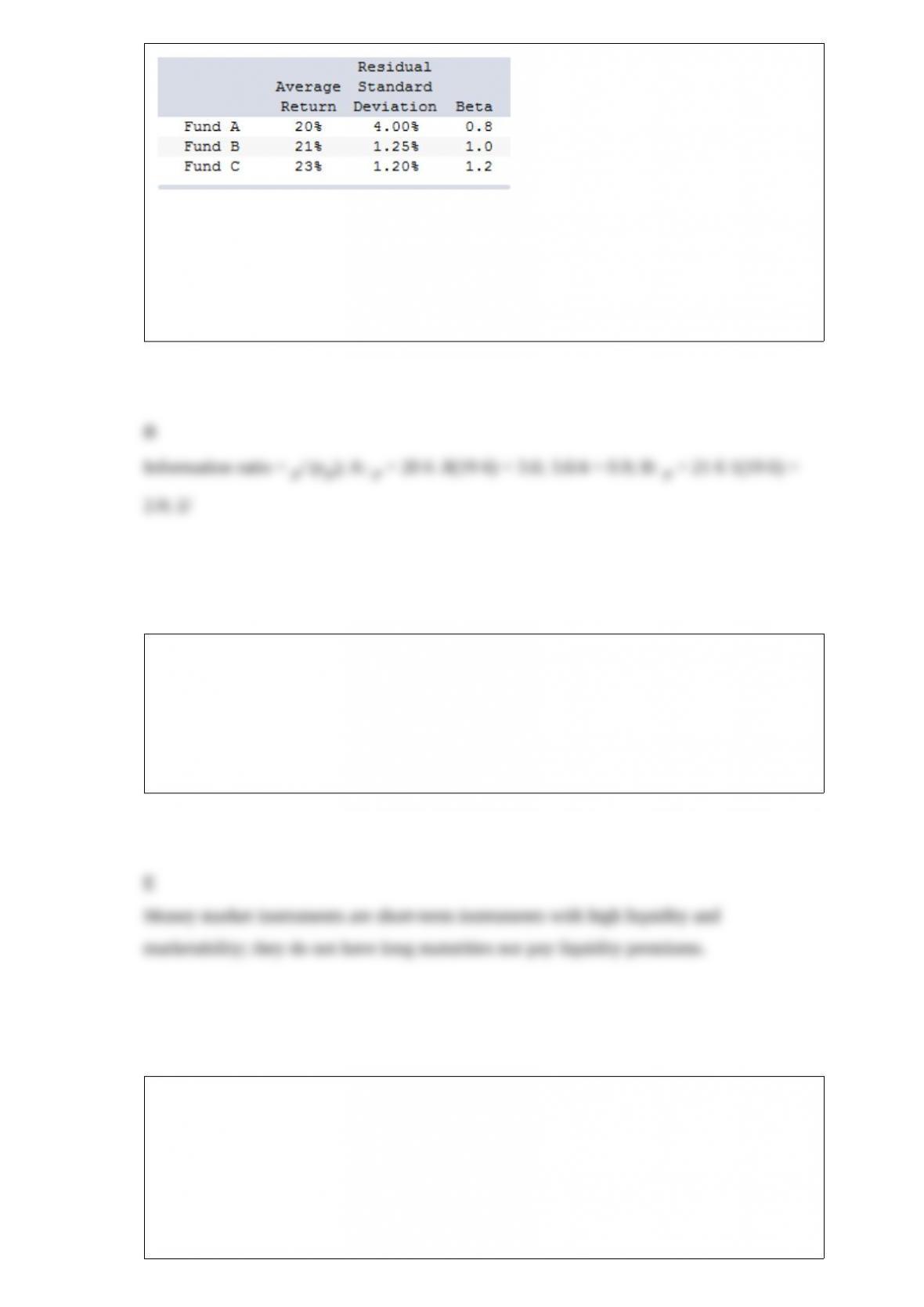

You want to evaluate three mutual funds using the information ratio measure for

performance evaluation. The risk-free return during the sample period is 6%, and the

average return on the market portfolio is 19%. The average returns, residual standard

deviations, and betas for the three funds are given below.

The fund with the highest information ratio measure is

A. Fund A.

B. Fund B.

C. Fund C.

D. Funds A and B (tied for highest).

E. Funds A and C (tied for highest).

The money market is a subsector of the

A. commodity market.

B. capital market.

C. derivatives market.

D. equity market.

E. None of the options are correct.

Consider the multifactor APT with two factors. Stock A has an expected return of

17.6%, a beta of 1.45 on factor 1, and a beta of .86 on factor 2. The risk premium on the

factor 1 portfolio is 3.2%. The risk-free rate of return is 5%. What is the risk-premium

on factor 2 if no arbitrage opportunities exist?

A. 9.26%

B. 3%

C. 4%

D. 7.75%

Tests of multifactor models indicate

A. the single factor model has better explanatory power in estimating security returns.

B. macroeconomic variables have no explanatory power in estimating security returns.

C. it may be possible to hedge some economic factors that affect future consumption

risk with appropriate portfolios.

D. multifactor models do not work.

E. None of the options are correct.

Other things equal, an increase in the government budget deficit

A. drives the interest rate down.

B. drives the interest rate up.

C. might not have any effect on interest rates.

D. increases business prospects.

A hedge ratio can be computed as

A. profit derived from one futures position for a given change in the exchange rate

divided by the change in value of the unprotected position for the same exchange rate.

B. the change in value of the unprotected position for a given change in the exchange

rate divided by the profit . derived from one futures position for the same exchange rate.

C. profit derived from one futures position for a given change in the exchange

rate plus the change in value of the unprotected position for the same exchange rate.

D. the change in value of the unprotected position for a given change in the exchange

rate plus by the profit derived from one futures position for the same exchange rate.

Assume that at retirement you have accumulated $500,000 in a variable annuity

contract. The assumed investment return is 6%, and your life expectancy is 15 years. If

the first year’s actual investment return is 8%, what is the starting benefit payment?

A. $30,000.00

B. $33,333.33

C. $51,481.38

D. $52,452.73

E. The answer cannot be determined from the information provided.

An American call option can be exercised

A.any time on or before the expiration date.

B.only on the expiration date.

C. any time in the indefinite future.

D. only after dividends are paid.

E. None of the options are correct.

The industry with the lowest ROE in 2015-2016 was

A. money center banks.

B. chemical products.

C. business software.

D. biotech.

E.-integrated oil and gas.

One of the problems with attempting to forecast stock market values is that

A. there are no variables that seem to predict market return.

B. the earnings multiplier approach can only be used at the firm level.

C. the level of uncertainty surrounding the forecast will always be quite high.

D. dividend-payout ratios are highly variable.

E. None of the options are correct.

Assume that you manage a $2 million portfolio that pays no dividends and has a beta of

1.3 and an alpha of 2% per month. Also, assume that the risk-free rate is 0.05% (per

month) and the S&P 500 is at 1,500. If you expect the market to fall within the next 30

days, you can hedge your portfolio by ______ S&P 500 futures contracts (the futures

contract has a multiplier of $250).

A. selling 1

B. selling 7

C. buying 1

D. buying 7

E. selling 11