In general, maximum levels of losses in the property-casualty industry are more

predictable for liability lines than for property lines.

Answer:

An FI that is short-funded faces the risk that the return of reinvesting assets could

exceed the cost of funding those assets.

Answer:

Under the doctrine of sovereign immunity, creditors cannot force repayment of the

debt.

Answer:

The exposure to foreign exchange risk by U.S. FIs has decreased with the growth of the

various derivative markets.

Answer:

The source of strength doctrine involving failed FIs in multibank holding company

corporate structures has been widely accepted by the courts.

Answer:

Currently, federal standards do not allow investment banks to covert to a bank holding

company structure.

Answer:

Exercise of a put option on interest rate futures by the buyer of the option results in the

buyer putting to the writer the bond futures contract at an exercise price higher than the

currently trading bond future.

Answer:

The goal of the Sarbanes-Oxley Act is to prevent deceptive accounting and

management practices and thus to increase confidence in corporate governance.

Answer:

Which of the following is NOT TRUE?A. The fastest growing area of finance

companies in recent years has been in the area of leasing and business loans.

B. Consumer loans represent the largest portion of the loan portfolio of finance

companies.

C. Finance companies rely on short-term commercial paper and customer deposits to

finance their assets.

D. Finance companies rely on short-term commercial paper and long-term debt to

finance their assets.

E. Finance companies are now the largest issuers of commercial paper in the U.S.

Answer:

Commercial letters of credit are guarantees that are issued to cover contingencies that

are potentially more severe and less predictable than those covered by standby letters of

credit.

Answer:

Personal credit institutions may be willing to approve of collateral that depository

institutions do not find acceptable.

Answer:

One problem with using CRA statistical credit scoring models to evaluate sovereign

credit risk is the classification into only two possible outcomes.

Answer:

Similar to loans, non-government bonds expose a lender to principal payment default

risk.

Answer:

One of the reasons for the development of internal risk measurement models is the

proposal of the BIS to impose capital requirements on the trading portfolios of FIs.

Answer:

Business loans represent 60% of the loan portfolio of finance companies.

Answer:

Federal Reserve primary credit loans available to DIs are generally at rates lower than

the federal funds target rate.

Answer:

Finance companies have traditionally been subject to state-imposed usury ceilings on

the maximum loan rate charged to any individual customers.

Answer:

The profit on bond call options moves asymmetrically with interest rates.

Answer:

All classes of mutual fund shares may legally charge an annual 12b-1 fee.

Answer:

Sales finance institutions compete directly with depository institutions for consumer

loans.

Answer:

Since 1990, commercial banks decreased the proportion of business loans and increased

the proportion of mortgages in their portfolios.

Answer:

Managing interest rate risk for less creditworthy FI’s by running a cap/floor book may

require the backing of external guarantees such as standby letters of credit because of

the nature of the options.

Answer:

There is a positive relationship between the interest rate charged on a retail loan and the

expected return on the loan.

Answer:

By the early 1990s interstate banking pacts basically had opened the doors for nearly all

banks to practice interstate branching in any geographic locations.

Answer:

Bank runs occur because customers know that banks will be forced to liquidate assets at

fire-sale prices.

Answer:

Commercial banks that have invested in Internet and mobile banking services and

products have significantly outperformed those banks that have chosen to avoid these

markets.

Answer:

Banks in given size classes tend to have very little difference in cost structures.

Answer:

The initial risk-based deposit insurance program implemented on January 1, 1993 was

based on capital adequacy and supervisory judgments involving asset quality, loan

underwriting standards and other operating risks.

Answer:

Class C shares of a mutual fund usually convert to Class A shares after some length of

time which may be as long as 6 to 8 years.

Answer:

Sovereign risk involves restrictions placed on borrowers and investors regarding the

movement of funds into and out of a foreign country.

Answer:

Open-end mutual funds issue a fixed number of shares as liabilities.

Answer:

Historical evidence indicates that load funds perform better than no-load funds.

Answer:

In the U.S., MMDAs typically are transaction accounts without limitations on the size

or number of checks or transfers that can occur each month.

Answer:

In many ways, SLCs perform similar functions for a borrower as do loan

commitments.

Answer:

The secondary market for the trading of swaps is second in liquidity to the U.S. T-bill

market.

Answer:

The Financial Services Modernization Act of 1999 allows bank holding companies to

open insurance underwriting affiliates.

Answer:

The growth of HMOs has increased the amount of health insurance premiums collected

by life insurance companies.

Answer:

The adverse effects of a contagious run include the restrictions on the ability of

individuals to transfer wealth through time and a negative impact on the level or rate of

savings.

Answer:

Which of the following refers to the process used to determine the value of mutual fund

shares each per day? A. Directed brokerage.

B. Marking-to-market.

C. Late trading.

D. Market timing.

E. Spinning.

Answer:

Off-balance-sheet items are A. items omitted from the short form balance sheet.

B. contingent assets and liabilities.

C. risk-free assets and liabilities.

D. exceptionally risky assets and liabilities.

E. foreign (off shore) assets and liabilities.

Answer:

A company that specializes in making installment loans to consumers would best be

categorized as a A. sales finance institution.

B. personal credit institution.

C. business credit institution.

D. lease finance company.

E. factoring company.

Answer:

The decline in European FX volatility during the last decade has been offset in part by

A. the greater volatilities of Asian currencies.

B. a reduction in inflation rates in European countries.

C. the fixing of exchange rates among European countries.

D. the replacement of domestic currencies with the euro.

E. None of the above.

Answer:

An FI’s net interest income reflects A. its asset-liability structure.

B. rates of interest when the assets and liabilities were put on the books.

C. the riskiness of its loans and investments.

D. the cost of its deposit and non-deposit sources of funds.

E. All of the above.

Answer:

The Community Reinvestment Act and the Home Mortgage Disclosure Act were both

passed to provide incentives to comply with A. entry regulation.

B. credit allocation regulation.

C. consumer protection regulation.

D. safety and soundness regulation.

E. investor protection regulation.

Answer:

Is the bank in compliance with the requirements?A. No, it does not meet the minimum

reserve requirements.

B. Yes, it meets the minimum reserve requirements.

C. Yes, it meets the minimum requirement only after using the 2 percent carryover

allowance.

D. Yes, it meets the minimum requirement only after using the 4 percent carryover

allowance.

E. No, it does not meet the minimum reserve requirements even after using the 4

percent carryover allowance.

Answer:

What is the least important factor determining bankruptcy, according to the Altman

Z-score model? A. Working capital to assets ratio

B. Retained earnings to assets ratio

C. Earnings before interest and taxes to assets ratio

D. Market value of equity to book value of long-term debt ratio

E. Sales to assets ratio

Answer:

As of 2012, assets of property-casualty insurers totaled approximately ________, which

was ______ of the assets of the life insurance industry. A. $900 billion; 20 percent

B. $1,600 billion; 30 percent

C. $4,250 billion; 90 percent

D. $5,750 billion; 105 percent

E. $7,700 billion; 120 percent

Answer:

Which of the following indicates the need to place a hedge? A. The price movement in

the underlying cash asset cannot be forecasted perfectly.

B. The prices of the assets or liabilities are imperfectly correlated over time with the

prices on the futures.

C. Basis risk prevents the minimum risk of the portfolio from reaching zero.

D. Treasury has been issuing more shorter-dated bonds to finance U.S. budget deficits.

E. Spot bonds and futures on bonds are traded in different markets.

Answer:

Which term refers to the risk that interest income will decrease as maturing assets are

replaced with new, more current assets? A. Credit risk.

B. Refinancing risk.

C. Reinvestment risk.

D. Liquidity risk.

E. Sovereign risk.

Answer:

If the amount lost per dollar on a defaulted loan is 40 percent, then a bank that does not

permit the loss of a loan to exceed 10 percent of its bank capital should set its

concentration limit (as a percentage of capital) to A. 5 percent.

B. 15 percent.

C. 25 percent.

D. 30 percent.

E. 50 percent.

Answer:

For property-casualty insurers, losses are higher for lines that are exposed to A. long

tails and low inflation.

B. long tails and high inflation.

C. short tails and low inflation.

D. short tails and high inflation.

E. short tails and no inflation.

Answer:

The primary regulators of savings institutions are A. the Federal Reserve and the FDIC.

B. the Office of Thrift Supervision and the FDIC.

C. the FDIC and the Office of the Comptroller of the Currency.

D. the Office of Thrift Supervision and the Comptroller of the Currency.

E. the Federal Reserve and the Comptroller of the Currency.

Answer:

What is the cost to the insured depositors if the insured depositor transfer resolution

method is used by the regulators to resolve the bank failure? A. $0.

B. $100 million

C. $30 million.

D. $40 million.

E. $60 million.

Answer:

Many states in the U.S. impose liquid asset ratios on insurance companies which may

be met by A. cash and excess reserves.

B. cash and municipal bonds from within the state of operation.

C. cash and government securities.

D. cash and policyholder reserves.

E. cash only.

Answer:

The following information is for a collateralized mortgage obligation (CMO). Tranche

A has a face value of $110 million and pays 5 percent annually. Tranche B has a face

value of $90 million and pays 7 percent annually.

What is the principal outstanding on Tranche A and Tranche B after the end of year

payment in the previous question?A. $110 million on Tranche A and $90 million on

Tranche B

B. $95 million on Tranche A and $90 million on Tranche B.

C. $106.8 million on Tranche A and $90 million on Tranche B.

D. $110 million on Tranche A and $86.8 million on Tranche B.

E. $108.4 million on Tranche A and $88.4 million on Tranche B.

Answer:

As of 2012, the primary regulator of both the life and property-casualty insurance

industry is/are the A. state insurance commissions.

B. NAIC.

C. Federal Reserve.

D. IRIS.

E. new federal oversight commission yet to be named.

Answer:

Choose among the following major banking laws.

A. The McFadden Act of 1927

B. The Glass-Steagall Act of 1933

C. The Depository Institutions Deregulation and Monetary Control Act (DIDMCA) of

1980

D. The Garn-St Germain Depository Institutions Act of 1982

E. The Competitive Equality in Banking Act of 1987

F. The Financial Institutions Reform, Recovery, and Enforcement Act of 1989

G. The Federal Deposit Insurance Corporation Improvement Act (FDICIA) of 1991

H. The Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994

I. Financial Services Modernization Act of 1999

This legislation introduced risk based deposit insurance premiums.

Answer:

If Bank A acquires Bank C, what is the new Herfindahl Index (HHI)? A. 60.

B. 100.

C. 5,800.

D. 5,050.

E. 6,525.

Answer:

Those regulatory agencies that have adopted some form of book value accounting

standard to measure an FI’s capital include all of the following except A. The Securities

and Exchange Commission (SEC).

B. The Federal Reserve.

C. The Office of the Comptroller of the Currency (OCC).

D. The FDIC.

E. State regulatory agencies.

Answer:

The following information is for a collateralized mortgage obligation (CMO). Tranche

A has a face value of $50 million and pays 6 percent annually. Tranche B has a face

value of $50 million and pays 8 percent annually. All mortgages have maturities of 30

years.

If at the end of the first year, the trustee of the CMO receives total cash flows of $10

million, how are they distributed to Tranche A and B, respectively? A. $5,558,628;

$4,441,372.

B. $4,441,372; $5,558,868.

C. $4,000,000; $6,000,000.

D. $6,000,000; $4,000,000.

E. $5,558,628; $4,000,000.

Answer:

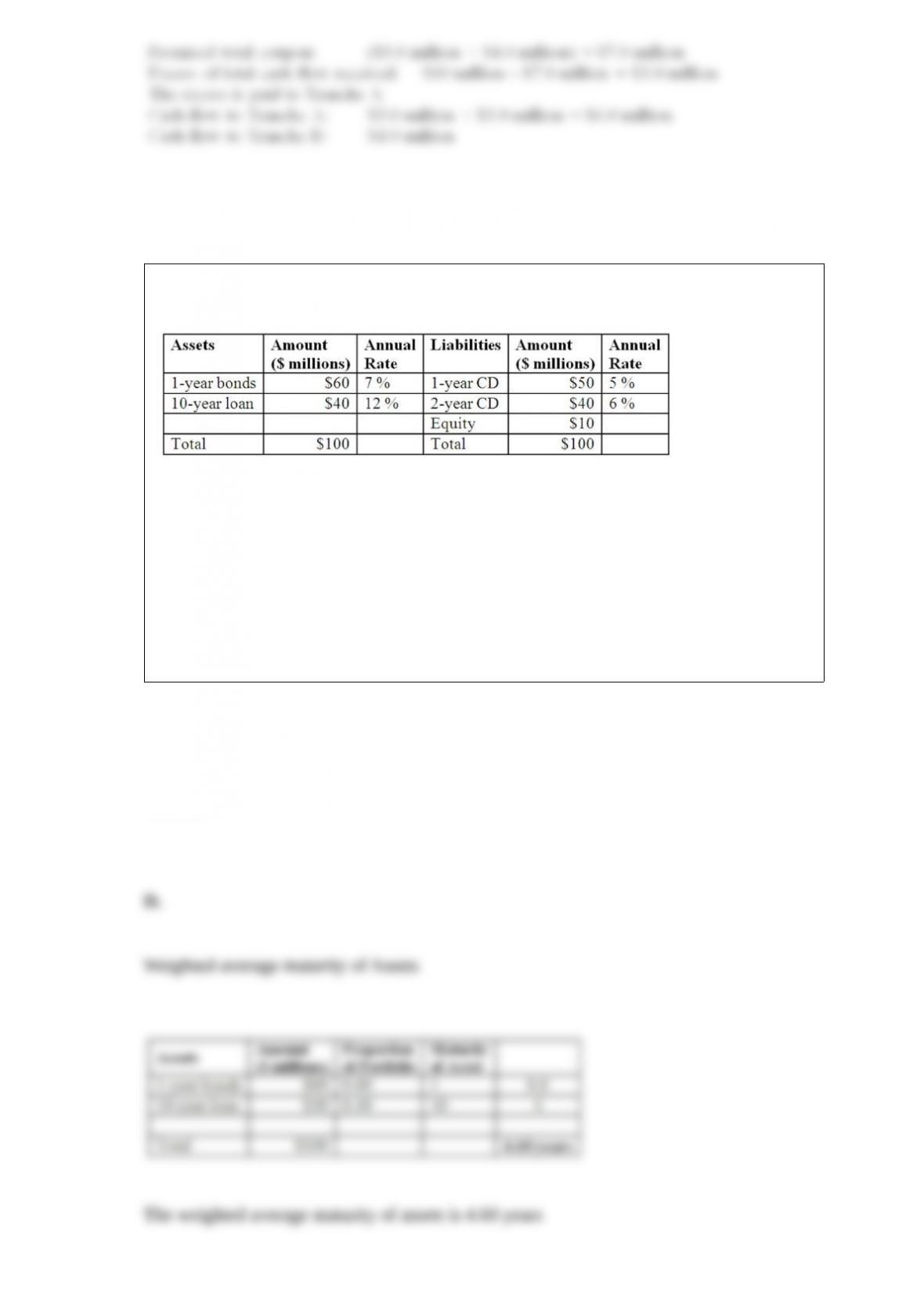

Hadbucks National Bank current balance sheet appears below. All assets and liabilities

are currently priced at par and pay interest annually.

What is the

weighted average maturity of assets? A. 5.50 years.

B. 6.40 years.

C. 5.00 years.

D. 4.60 years.

E. 10.0 years.

Answer:

A forward contract A. has more credit risk than a futures contract.

B. is more standardized than a futures contract.

C. is marked to market more frequently than a futures contract.

D. has a shorter time to delivery than a futures contract.

E. is less risky than a futures contract.

Answer:

What is the number of T-Bill futures contracts necessary to hedge the balance sheet if

the duration of the deliverable T-bills is 0.25 years and the current price of the futures

contract is $98 per $100 face value? A. 6,212 contracts.

B. 6,805 contracts.

C. 6,900 contracts.

D. 7,112 contracts.

E. 7,327 contracts.

Answer:

Which legislation authorizes federal agencies to sell delinquent and defaulted loan

assets? A. Federal Debt Collection Improvements Act.

B. Financial Services Modernization Act.

C. The Bank Holding Company Act.

D. Depository Institutions Deregulation and Monetary Control Act.

E. Financial Institutions Reform Recovery and Enforcement Act.

Answer:

According to PPP, the new exchange rate of Russian rubles to U.S. dollars isA. 0.15.

B. 0.1425.

C. 0.141.

D. 0.1605.

E. 0.159.

Answer:

Which of the following is not a qualitative factor in credit risk analysis? A. Borrower

reputation.

B. Borrower ethnic origin.

C. Leverage position of the borrower.

D. The level of interest rates.

E. Collateral available.

Answer:

A small local bank failed because a housing market collapse following the departure of

the area’s largest employer. What type of risk applies to the failure of the institution? A.

Firm-specific risk.

B. Technological risk.

C. Operational risk.

D. Sovereign risk.

E. Insolvency risk.

Answer:

What is the average return earned (both explicit and implicit) by the account holder

over the full year if the minimum balance is reduced to $200? A. 2.01 percent.

B. 2.65 percent.

C. 3.78 percent.

D. 5.35 percent.

E. 6.13 percent.

Answer:

What is the spread earned by the bank if the end-of-year exchange rate is €1.77/$? A.

-1.00 percent.

B. -0.70 percent.

C. -0.25 percent.

D. 0.00 percent.

E. 0.20 percent.

Answer: