Freddie Mac and Ginnie Mae were organized to provide

A. a primary market for mortgage transactions.

B. liquidity for the mortgage market.

C. a primary market for farm loan transactions.

D. liquidity for the farm loan market.

E. a source of funds for government agencies. Liquidity for the mortgage market.

The beta of Apple stock has been estimated as 2.3 using regression analysis on a sample

of historical returns. A commonly-used adjustment technique would provide an adjusted

beta of

A. 2.20.

B. 1.87.

C. 2.13.

D. 1.66.

The beta of an active portfolio is 1.36. The standard deviation of the returns on the

market index is 22%. The

nonsystematic variance of the active portfolio is 1.2%. The standard deviation of the

returns on the active

portfolio is

A. 3.19%.

B.31.86%.

C. 42.00%.

D. 27.57%.

E. 2.86%.

Investors trade previously issued securities in the ________ market(s).

A. primary

B. secondary

C. primary and secondary

D. derivatives

Xlink Company has an expected ROE of 15%. The dividend growth rate will be

_______ if the firm follows a policy of plowing back 75% of earnings.

A. 3.75%

B. 11.25%

C. 8.25%

D. 15.0%

Which of the following orders instructs the broker to sell at or below a specified price?

A. Limit-sell order

B. Stop-loss

C. Limit-buy order

D. Stop-buy order

E. Market order

Consider the regression equation:

rirf = g0 + g1bi + g2s2(ei) + eit

where:

rirt = the average difference between the monthly return on stock i and the monthly risk

free rate

bi = the beta of stock i

s2(ei) = a measure of the nonsystematic variance of the stock i

If you estimated this regression equation and the CAPM was valid, you would expect

the estimated coefficient, g1, to be

A. 0.

B. 1.

C. equal to the risk free rate of return.

D. equal to the average difference between the monthly return on the market portfolio

and the monthly risk free rate.

E. equal to the average monthly return on the market portfolio.

One property of a risky portfolio that combines an active portfolio of mispriced

securities with a market portfolio

is that, when optimized, its squared Sharpe measure increases by the square of the

active portfolio’s

A. Sharpe ratio.

B.information ratio.

C. alpha.

D. Treynor measure.

E. None of the options are correct.

The M-squared measure considers

A. only the return when evaluating mutual funds.

B. the risk-adjusted return when evaluating mutual funds.

C. only the total risk when evaluating mutual funds.

D. only the market risk when evaluating mutual funds.

E. None of the options are correct.

Suppose two portfolios have the same average return and the same standard deviation

of returns, but Aggie Fund has a lower beta than Raider Fund. According to the Treynor

measure, the performance of Aggie Fund

A. is better than the performance of Raider Fund.

B. is the same as the performance of Raider Fund.

C. is poorer than the performance of Raider Fund.

D. cannot be measured as there are no data on the alpha of the portfolio.

With regard to a futures contract, the short position is held by

A. the trader who bought the contract at the largest discount.

B. the trader who has to travel the farthest distance to deliver the commodity.

C. the trader who plans to hold the contract open for the lengthiest time period.

D. the trader who commits to purchasing the commodity on the delivery date.

E. the trader who commits to delivering the commodity on the delivery date.

Stephanie Watson is 23 years old and has accumulated $4,000 in her selfdirected

defined contribution pension plan. Each year she contributes $2,000 to the plan, and her

employer contributes an equal amount. Stephanie thinks she will retire at age 67 and

figures she will live to age 81. The plan allows for two types of investments. One offers

a 3.5% riskfree real rate of return. The other offers an expected return of 10% and has a

standard deviation of 23%. Stephanie now has 5% of her money in the riskfree

investment and 95% in the risky investment. She plans to continue saving at the same

rate and keep the same proportions invested in each of the investments. Her salary will

grow at the same rate as inflation. How much can Stephanie be sure of having in the

safe account at retirement?

A. $37,221

B. $16,423

C. $11,856

D. $21,156.

E. $49,219

Diversifiable risk is also referred to as

A. systematic risk or unique risk.

B. systematic risk or market risk.

C. unique risk or market risk.

D. unique risk or firm-specific risk.

The expectations hypothesis of futures pricing

A. is the simplest theory of futures pricing.

B. states that the futures price equals the expected value of the future spot price of the

asset.

C. is not a zero-sum game.

D. is the simplest theory of futures pricing and states that the futures price equals the

expected value of the future spot price of the asset.

E. is the simplest theory of futures pricing and is not a zero-sum game.

Given a stock index with a value of $1,200, an anticipated dividend of $45, and a

risk-free rate of 6%, what should be the value of one futures contract on the index?

A. $1,227.00

B. $1,070.00

C. $993.40

D. $995.09

E. $1,000.00

Performance evaluation of hedge funds is complicated by

A. liquidity premiums.

B. survivorship bias.

C. unreliable market valuations of infrequently-traded assets.

D. merger arbitrage.

E. All of the options are correct.

Consider a single factor APT. Portfolio A has a beta of 2.0 and an expected return of

22%. Portfolio B has a beta of 1.5 and an expected return of 17%. The risk-free rate of

return is 4%. If you wanted to take advantage of an arbitrage opportunity, you should

take a short position in portfolio __________ and a long position in portfolio _______.

A. A; A

B. A; B

C. B; A

D. B; B

E. A; the riskless asset

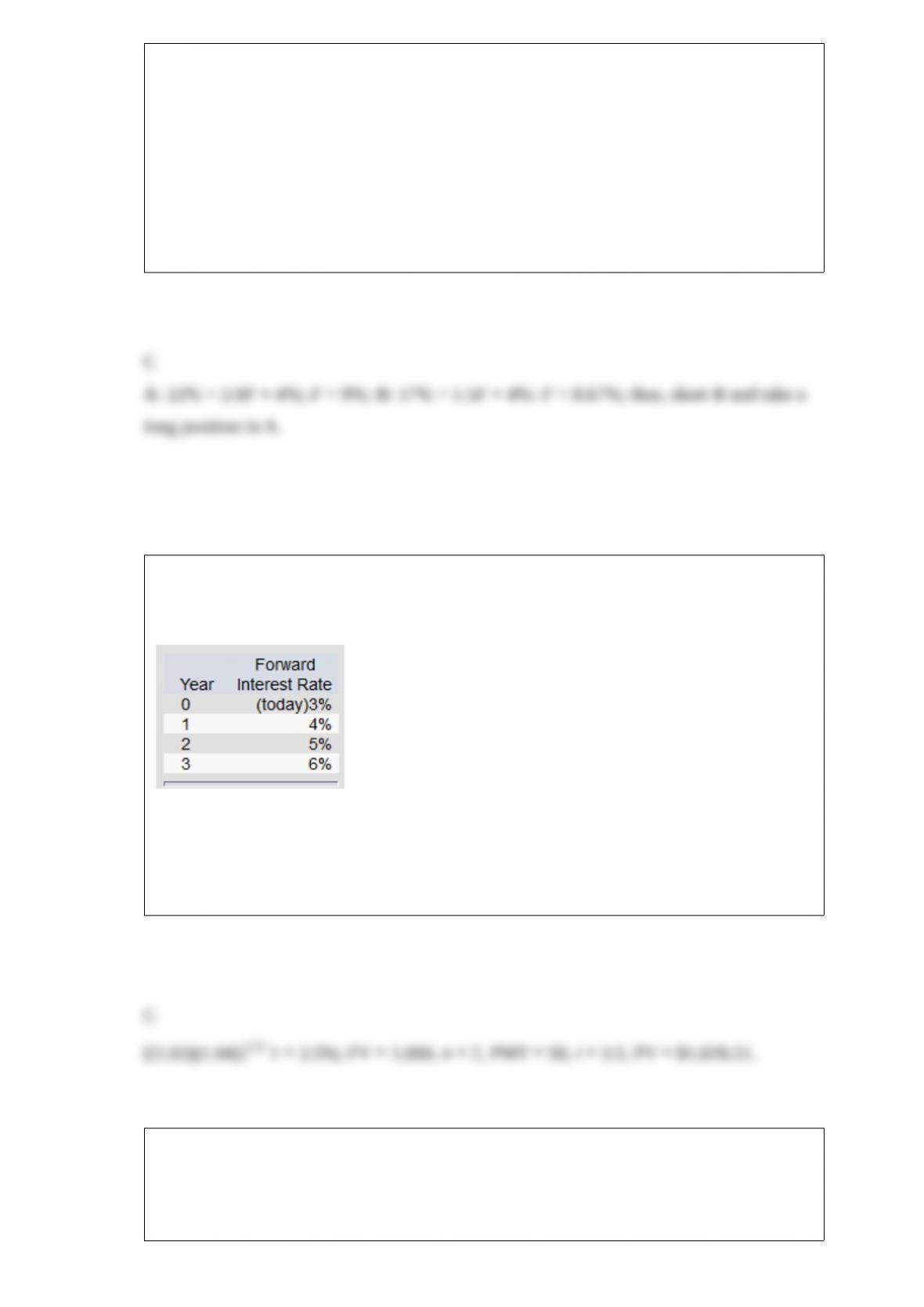

What is the price of a 2-year maturity bond with a 5% coupon rate paid annually? (Par

value = $1,000.) Suppose that all investors expect that interest rates for the 4 years will

be as follows:

A. $1,092.97

B. $1,054.24

C. $1,028.51

D. $1,073.34

E. None of the options are correct.

Suppose the risk-free return is 4%. The beta of a managed portfolio is 1.2, the alpha is

1%, and the average return is 14%. Based on Jensen’s measure of portfolio

performance, you would calculate the return on the market portfolio as

A. 11.5%.

B. 14%.

C. 15%.

D. 16%.

When interest rates decline, the duration of a 10-year bond selling at a premium

A. increases.

B. decreases.

C. remains the same.

D. increases at first, then declines.

E. decreases at first, then increases.

Two bonds are selling at par value, and each has 17 years to maturity. The first bond has

a coupon rate of 6%, and the second bond has a coupon rate of 13%. Which of the

following is false about the durations of these bonds?

A. The duration of the higher coupon bond will be higher.

B. The duration of the lower coupon bond will be higher.

C. The duration of the higher coupon bond will equal the duration of the lower coupon

bond.

D. There is no consistent statement that can be made about the durations of the bonds.

E. The duration of the higher coupon bond will be higher, and the duration of the higher

coupon bond will equal the duration of the lower coupon bond.

Home bias refers to

A. the tendency to vacation in your home country instead of traveling abroad.

B. the tendency to believe that your home country is better than other countries.

C. the tendency to give preferential treatment to people from your home country.

D. the tendency to overweight investments in your home country.

E. None of the options are correct.

A coupon bond that pays interest of $90 annually has a par value of $1,000, matures in

nine years, and is selling today at a $66 discount from par value. The yield to maturity

on this bond is

A. 9.00%.

B. 10.15%.

C. 11.25%.

D. 12.32%.

E. None of the options are correct.

A company paid a dividend last year of $1.75. The expected ROE for next year is

14.5%. An appropriate required return on the stock is 10%. If the firm has a plowback

ratio of 75%, the dividend in the coming year should be

A. $1.80.

B. $2.12.

C. $1.77.

D. $1.94.

In a multifactor APT model, the coefficients on the macro factors are often called

A. systematic risk

B. firm-specific risk.

C. idiosyncratic risk.

D. factor loadings.

According to James Tobin, the long-run value of Tobin’s Q should move toward

A. 0.

B. 1.

C. 2.

D. infinity.

E. None of the options are correct.

Smart Draw Company is expected to have per share FCFE in year 1 of $1.20, per share

FCFE in year 2 of $1.50, and per share FCFE in year 3 of $2.00. After year 3, per share

FCFE is expected to grow at the rate of 10% per year. An appropriate required return

for the stock is 14%. The stock should be worth _______ today.

A. $33.00

B. $40.68

C. $55.00

D. $66.00

E. $12.16

The current market price of a share of CSCO stock is $22. If a put option on this stock

has a strike price of $20, the put

A.is out of the money.

B. is in the money.

C. sells for a higher price than if the strike price of the put option was $25.

D. is out of the money and sells for a higher price than if the strike price of the put

option was $25.

E. is in the money and sells for a higher price than if the strike price of the put option

was $25.

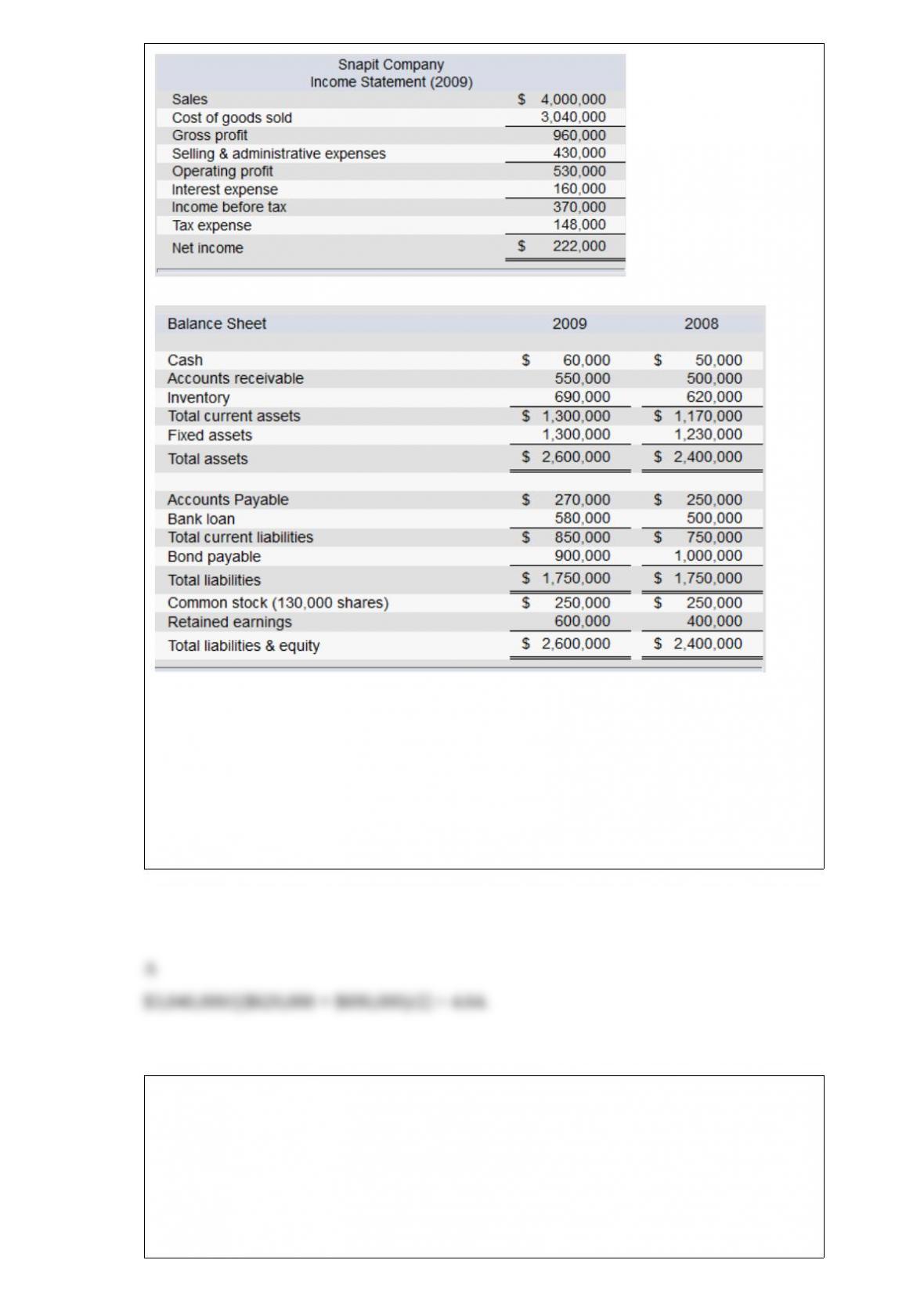

The financial statements of Snapit Company are given below.

Note: The common shares are trading in the stock market for $100 each.

Refer to the financial statements of Snapit Company. The firm’s inventory turnover ratio

for 2009 is

A. 4.64.

B. 4.16.

C. 4.41.

D. 4.87.

E. None of the options are correct.

The risk-free rate and the expected market rate of return are 0.056 and 0.125,

respectively. According to the capital asset pricing model (CAPM), the expected rate of

return on a security with a beta of 1.25 is equal to

A. 0.142.

B. 0.144.

C. 0.153.

D. 0.134.

E. 0.117.

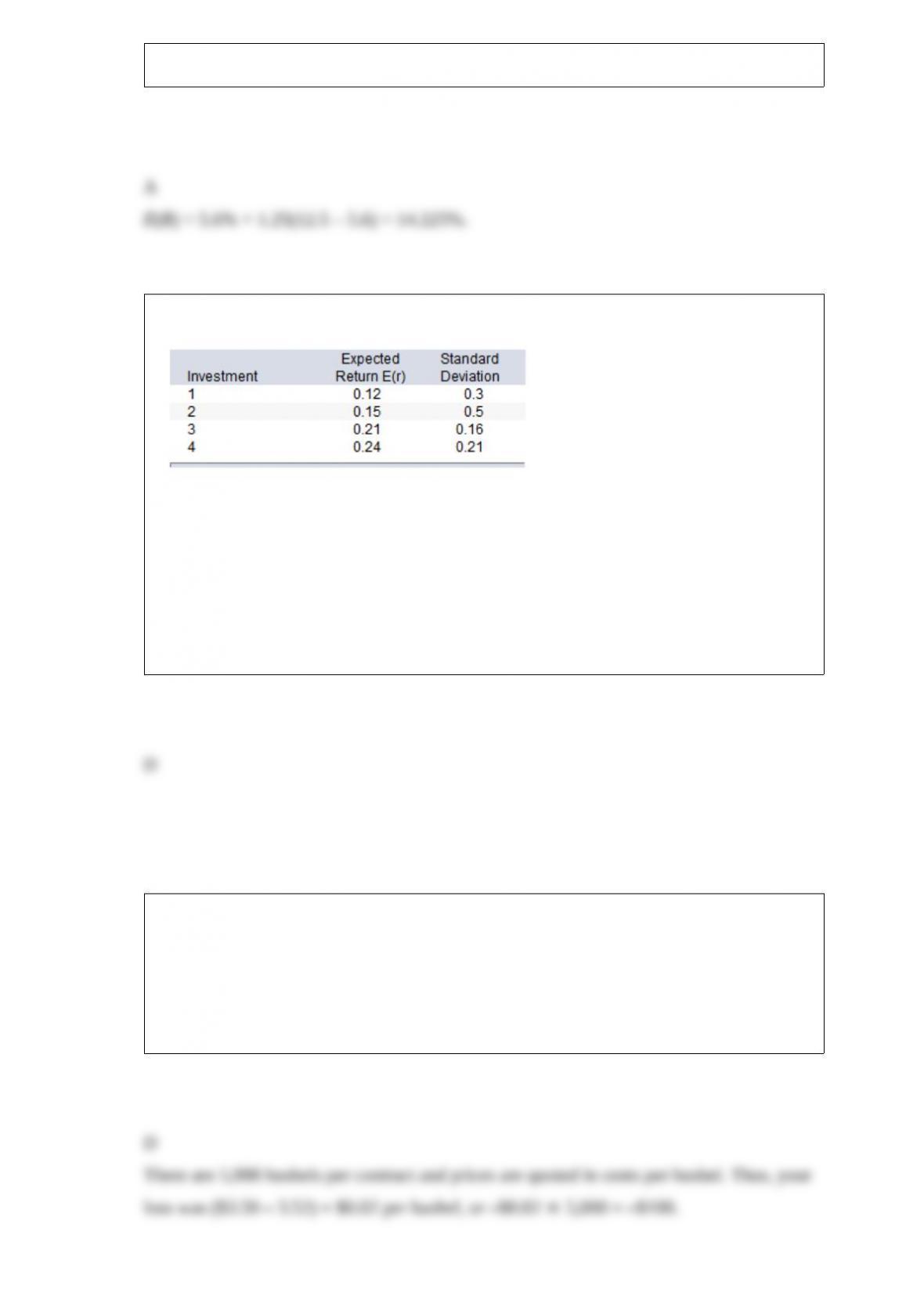

Use the below information to answer the following question.

U = E(r ) – (A/2)s2

Which investment would you select if you were risk neutral?

A. 1

B. 2

C. 3

D. 4

E. Cannot be determined from the information given.

If you are risk neutral, your only concern is with return, not risk.

You sold a futures contract on corn at a futures price of 350, and at the time of

expiration, the price was 352. What was your profit or loss?

A. $2.00

B. –$2.00

C. $100

D. –$100

You sold a futures contract on corn at a futures price of 331, and at the time of

expiration, the price was 343. What was your profit or loss?

A. –$12.00

B. $12.00

C. –$600

D. $600