36

Mini-Case 12-2: Bowden Brake Service (Part B)

One day while you are in Bowden Brake Service getting your brakes repaired, Jim storms into

his office, slamming doors and shouting about the local financial institutions. After a few

minutes of building your courage, you approach Jim and ask him what the problem is. He shouts,

“It’s the financial institutions in this town! Not one of them will lend me the money I need to

expand my business. They all said I needed to take a closer look at my financial position before I

consider expanding. One of them said something about ratio analysis. I know a lot about cars and

brakes, but what is ratio analysis?”

You tell Jim you will perform a ratio analysis for the business if he gives you a free brake job.

Jim provides you with the following financial statements.

Bowden Brake Service

Income Statement

Year Ending December 31, 2007

Net Sales $780,000

Costs of Goods Sold:

Beginning Inventory $104,000

Purchases 526,480

Goods Available for Sale $630,480

Ending Inventory 134,400

Costs of Goods Sold 496,080

Gross Margin $283,920

Operating Expenses:

Rent 24,000

Insurance 5,250

Advertising 6,000

Travel 2,500

Interest 72,750

Taxes (Property, etc.) 2,500

Salaries & Admin. Expenses 97,000

Utilities 12,500

Supplies 1,360

Total Operating Expenses $223,860

Net Profit $60,060

Bowden Brake Service

Balance Sheet

December 31, 2007

Assets

Current Assets:

Cash $20,000

Accounts Receivable 10,000

Notes Receivable 5,000

Inventory 134,400

Total Current Assets $169,400

Fixed Assets:

Land 147,000

Machinery 73,000

Equipment 160,800

Less Accumulated Depreciation (30,200) 203,600

Total Fixed Assets 350,600

Total Assets $520,000

Liabilities & Owner’s Equity

Current Liabilities:

Accounts Payable 40,500

Notes Payable 20,200

Accrued Salaries Payable 4,300

Total Current Liabilities: 65,000

Long-term Liabilities: Long-term Loan 325,000

Total Liabilities $390,000

Owner’s Equity, Jim Bowden $130,000

Total Liabilities and Net Worth $520,000

115) Were the bankers correct? Do you think Jim should expand the business?

116) The break-even point ________.

A) occurs where a company’s total revenue equals its total expenses

B) is the point at which a company neither earns a profit nor incurs a loss

C) tells a business owner the minimum level of activity needed to keep her company in operation

D) All of the above

117) Which of the following is an assumption of break-even analysis?

A) Fixed expenses remain constant for all levels of sales volume.

B) Variable expenses change in direct proportion to changes in sales volume.

C) Changes in sales volume have no effect on unit sales price.

D) All of the above

118) Refer to the following information:

Smith Office Supply Industry Mean

Current Ratio 2.3 1.8

Quick Ratio .4 .8

Average Inventory Turnover 2.0 3.9

Net Sales-to-Working Capital 4.0 7.8

Debt-to-Net Worth Ratio 3.0 1.7

Net Profit to Equity Ratio 40.1 percent 22.2 percent

Which of the following statements is most likely false?

A) Smith relies heavily on inventory to meet its debt obligations.

B) Smith is sufficiently capitalized.

C) Smith’s sales are inadequate.

D) Smith’s prices may be too high and/or the inventory too “stale.”

Refer to the following Gunther’s Emporium information to answer the question(s) below:

Gunther’s Emporium expects net sales of $2,396,919 for the upcoming year, with variable

expenses totaling $1,813,443 and fixed expenses of $412,190.

119) Using break-even analysis, what is Gunther’s contribution margin?

A) 4 percent

B) 32 percent

C) 24 percent

D) 12 percent

120) Gunther’s Emporium expects net sales of $2,396,919 for the upcoming year, with variable

expenses totaling $1,813,443 and fixed expenses of $412,190. What is Gunther’s break-even

point?

A) $1,876,324

B) $1,693,276

C) $5,667,009

D) Insufficient information given to determine.

121) If Gunther’s net profit target for the year is $190,000, what sales level must he achieve?

A) $2,473,796

B) $1,876,324

C) $5,667,009

D) None of the above

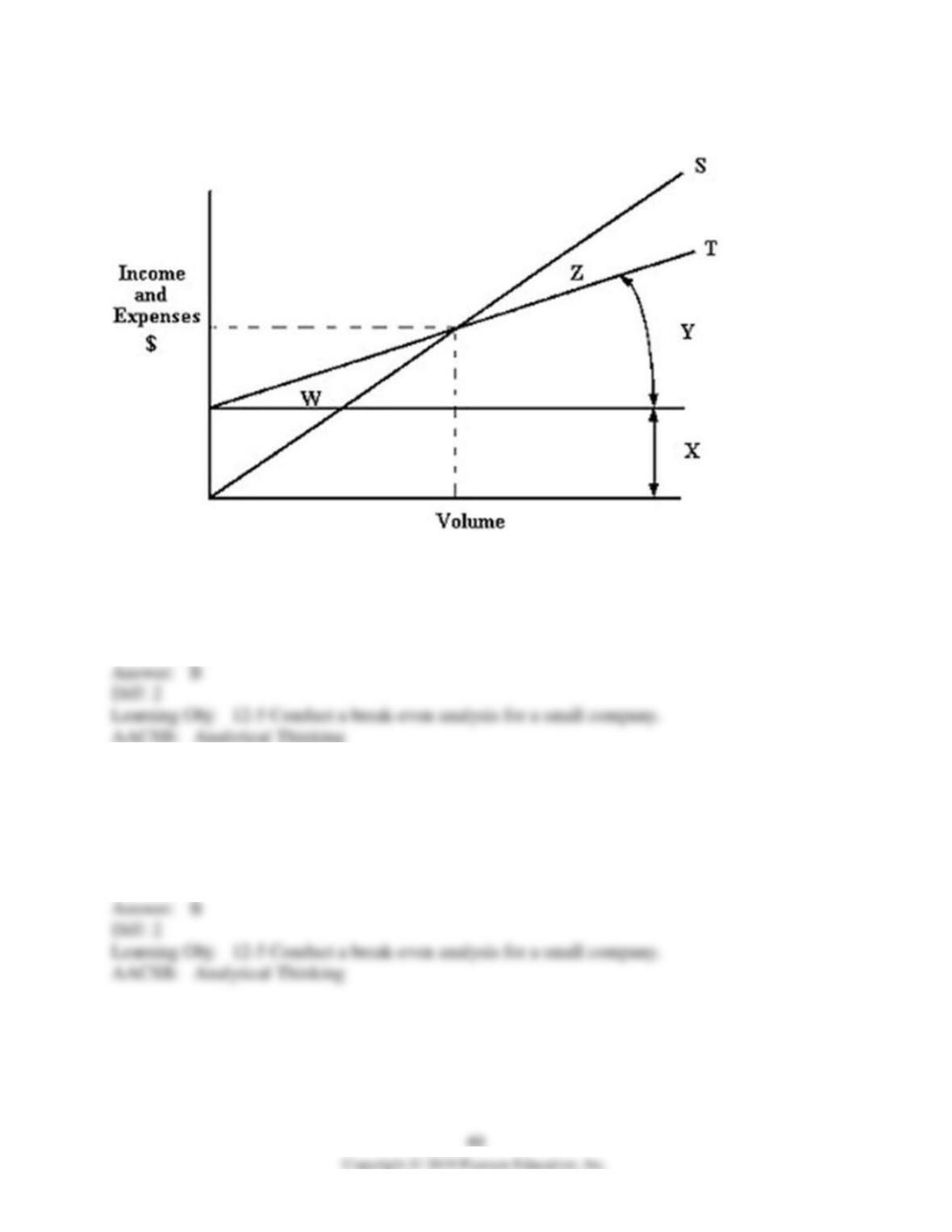

Refer to the following break-even chart to answer the question(s) below:

122) Line T is the ________ line, while line S is the ________ line.

A) total revenue; total expense

B) total expense; total revenue

C) fixed cost; variable cost

D) variable cost; fixed cost

123) The area labeled ________ represents the firm’s fixed expenses, while ________ represents

its variable expenses.

A) Z; W

B) X; Y

C) Y; X

D) W; Z

124) The area labeled ________ is the “profit area.”

A) W

B) X

C) Y

D) Z

125) The area labeled ________ is the “loss area.”

A) W

B) X

C) Y

D) Z

126) The break-even point is the level of operation at which a business neither earns a profit nor

incurs a loss, and lets the business owner know the minimum level of activity required to keep

the firm in operation.

127) Fixed expenses are those that do not vary with changes in the volume of sales, but do vary

with production.

128) On a break-even chart, the break-even point occurs at the intersection of the fixed expense

line and the total revenue line.

129) Why is it important for an entrepreneur, about to launch a business, to perform a break-even

analysis? Describe the steps in calculating it.

130) Explain the procedure for constructing a graph that visually portrays the firm’s break-even

point (the point where revenues equal expenses).

131) What are the advantages and the disadvantages of using break-even analysis?

Mini-Case 12-1: Bowden Brake Service (Part A)

Jim Bowden, owner of Bowden Brake Service, is planning to expand his six-year-old brake

service to include tune-ups and tire services. Based on budget estimates for the upcoming year,

Jim expects net sales to be $825,000 with a cost of goods sold of $530,000 and total operating

expenses of $210,000. From the budget he created, Jim computes fixed expenses to be $168,000,

while variable expenses (including cost of goods sold) are $572,000. Jim is concerned that the

new cost structure may damage his ability to produce a profit and he wants to perform a break-

even analysis for the upcoming year to gain insight.

132) If Jim were to reduce his fixed costs by 10 percent by reducing a middle management

position, what benefit would that be to him and the company? What would his new contribution

margin be?

133) Help Jim compute the break-even point for his brake service.

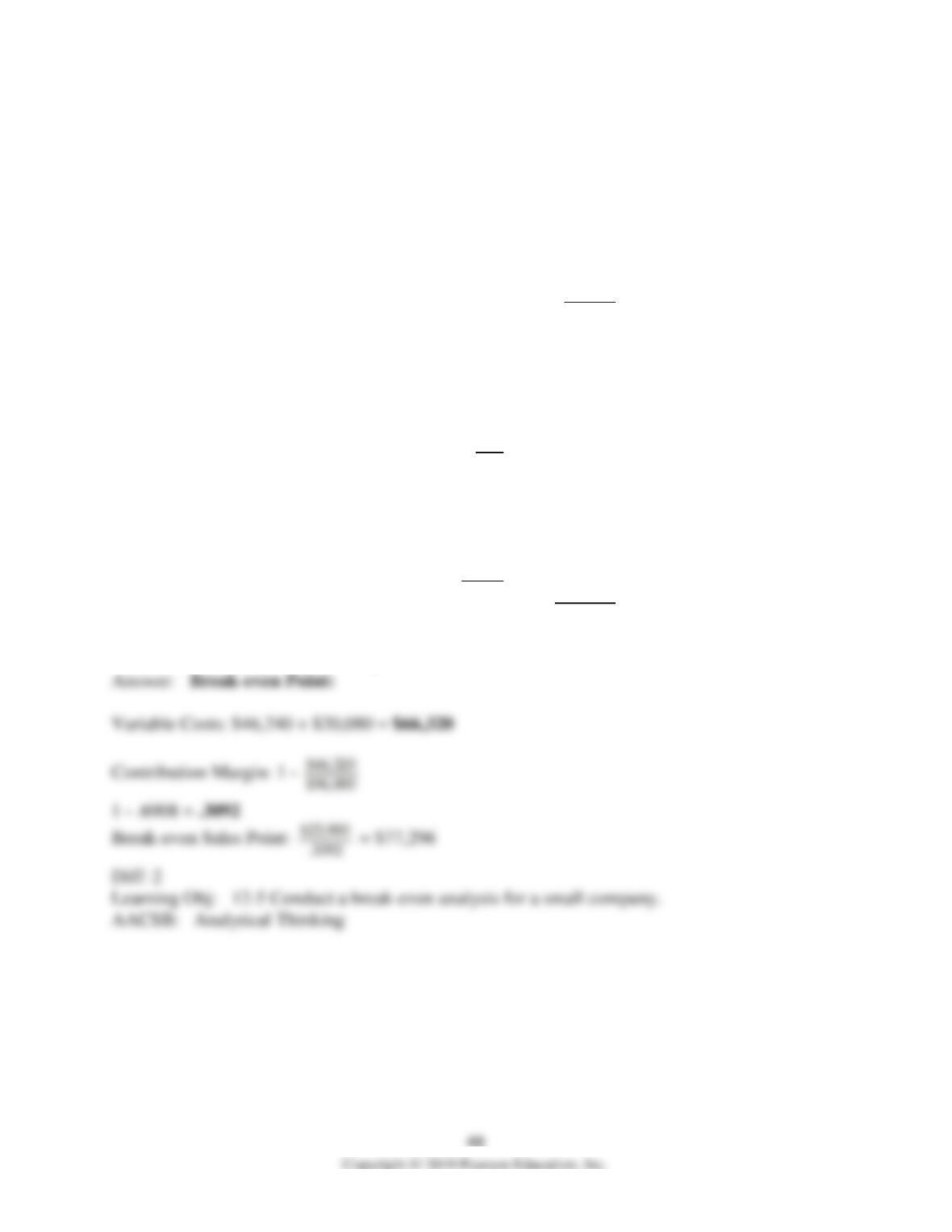

Mini-Case 12-3: Birmingham’s Stereo Shop

Birmingham’s Stereo Shop expects net sales of $280,000 in the upcoming year, with a cost of

goods sold of $173,600 and total expenses of $76,200. Birmingham expects variable expenses

(including cost of goods sold) to be $195,700 and fixed expenses to be $54,100.

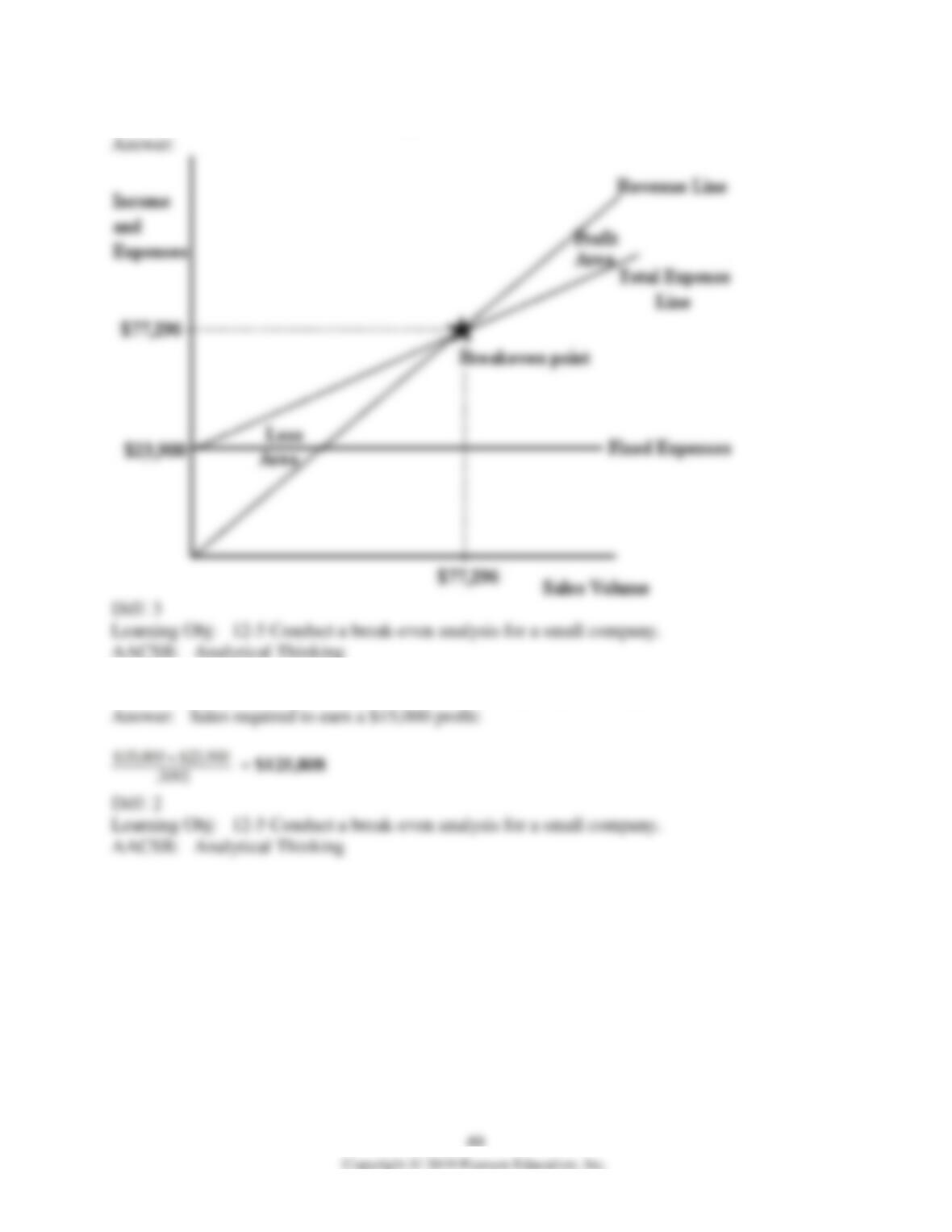

134) What level of sales would Birmingham’s have to achieve if it wanted to make a $25,000

profit?

135) Construct a break-even chart for Birmingham’s.

136) Compute a break-even point in dollars.

137) Suppose that the manufacturer desires a profit of $9,000 on this product. How many units

must be sold?

Mini-Case 12-6: Crazy Harry’s

The following is a pro forma income statement for Crazy Harry’s.

Crazy Harry’s

Pro Forma Income Statement

Sales $96,000

Cost of Goods Sold 46,240

Gross Profit $49,760

Fixed Expenses

Rent $2,400

Insurance 3,000

Salaries 16,500

Taxes 1,100

Miscellaneous Fixed Expenses 900

Total Fixed Expenses $23,900

Variable Expenses

Wages $11,200

Advertising 5,700

Benefits 2,800

Other Variable Expenses 1,120

Total Variable Expenses $20,080

Net Profit $5,040

138) Calculate Harry’s break-even point.

139) Create a break-even chart for Harry.

140) If Harry’s profit target is $15,000, what level of sales must be achieved?