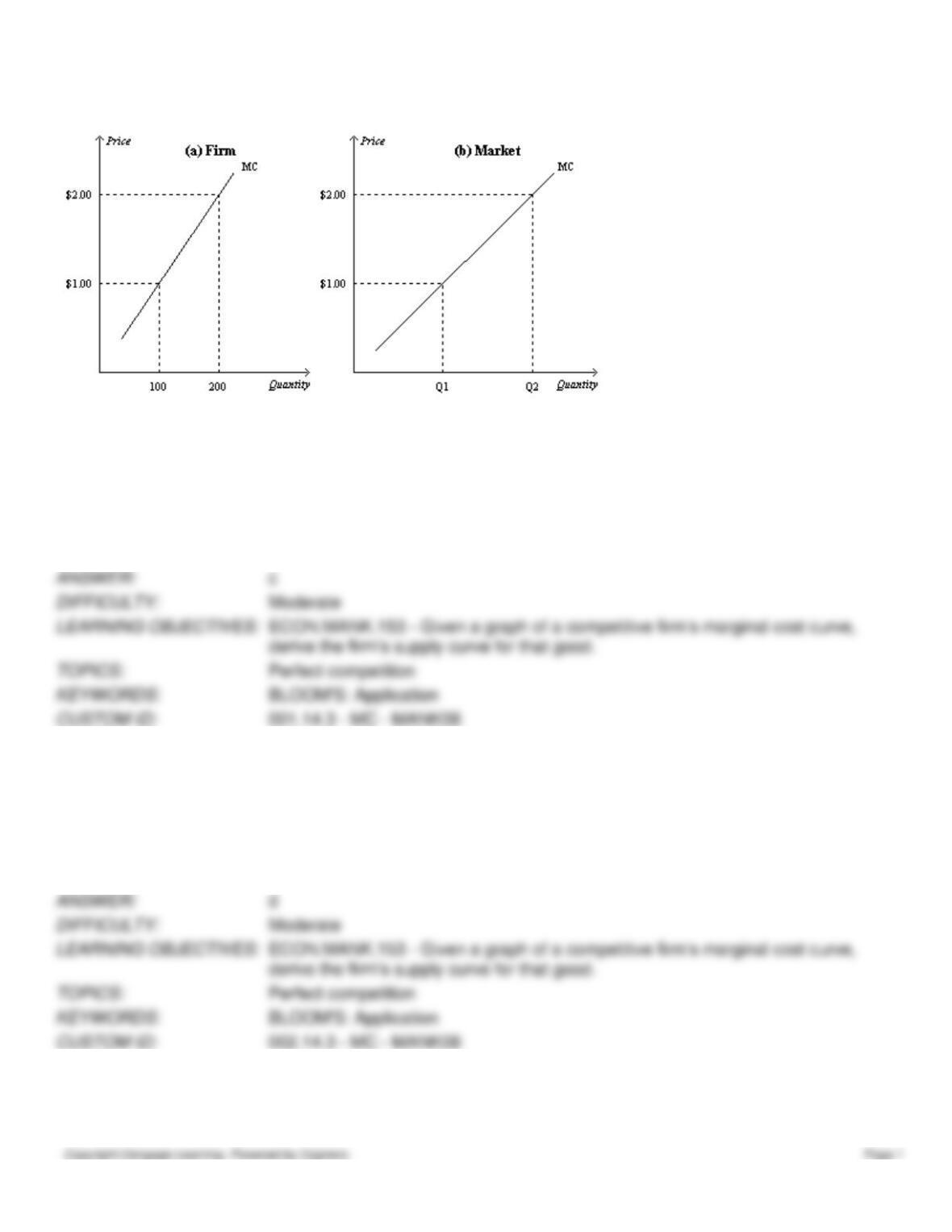

Figure 14-9

In the figure below, panel (a) depicts the linear marginal cost of a firm in a competitive market, and panel (b) depicts the

linear market supply curve for a market with a fixed number of identical firms.

1. Refer to Figure 14-9. If there are 300 identical firms in this market, what level of output will be supplied to the market

when price is $1.00?

a.

300

b.

6,000

c.

30,000

d.

60,000

2. Refer to Figure 14-9. If there are 300 identical firms in this market, what level of output will be supplied to the market

when price is $2.00?

a.

300

b.

6,000

c.

30,000

d.

60,000

3. Refer to Figure 14-9. If there are 400 identical firms in this market, what level of output will be supplied to the market

when price is $2.00?

a.

10,000

b.

20,000

c.

40,000

d.

80,000

4. Refer to Figure 14-9. If there are 600 identical firms in this market, what is the value of Q1?

a.

6,000

b.

12,000

c.

60,000

d.

120,000

5. Refer to Figure 14-9. If there are 100 identical firms in this market, what is the value of Q2?

a.

10,000

b.

20,000

c.

40,000

d.

80,000

6. Refer to Figure 14-9. When 100 identical firms participate in this market, at what price will 15,000 units be supplied to

this market?

a.

$1.00

b.

$1.50

c.

$2.00

d.

The price cannot be determined from the information provided.

7. Refer to Figure 14-9. If at a market price of $1.75, 52,500 units of output are supplied to this market, how many

identical firms are participating in this market?

a.

75

b.

100

c.

250

d.

300

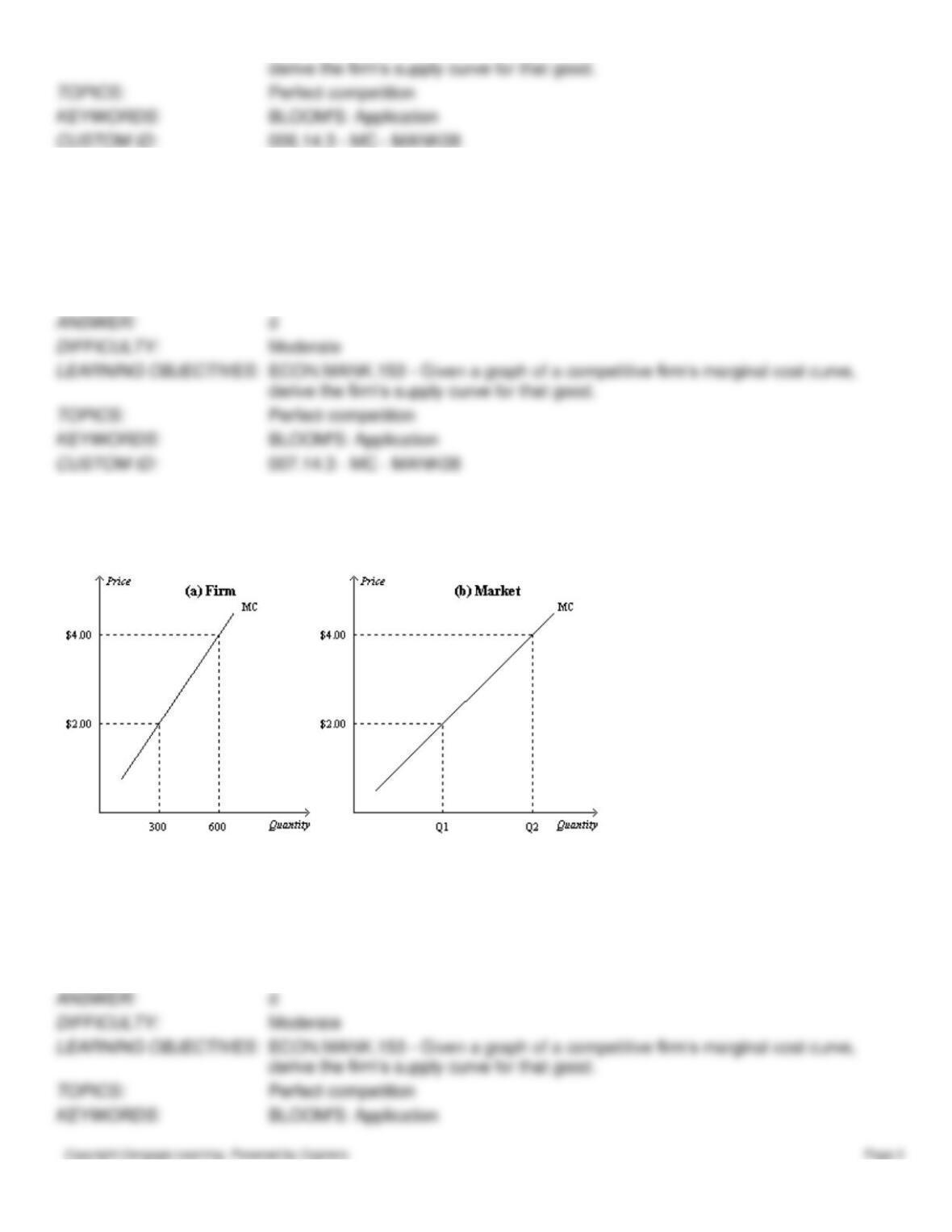

Figure 14–10

In the figure below, panel (a) depicts the linear marginal cost of a firm in a competitive market, and panel (b) depicts the

linear market supply curve for a market with a fixed number of identical firms.

8. Refer to Figure 14–10. If there are 500 identical firms in this market, what is the value of Q1?

a.

10,000

b.

20,000

c.

50,000

d.

150,000

9. Refer to Figure 14–10. If there are 500 identical firms in this market, what is the value of Q2?

a.

12,000

b.

60,000

c.

240,000

d.

300,000

10. Refer to Figure 14–10. If there are 700 identical firms in this market, what is the value of Q1?

a.

140,000

b.

210,000

c.

280,000

d.

420,000

11. Refer to Figure 14–10. If there are 700 identical firms in this market, what is the value of Q2?

a.

140,000

b.

210,000

c.

280,000

d.

420,000

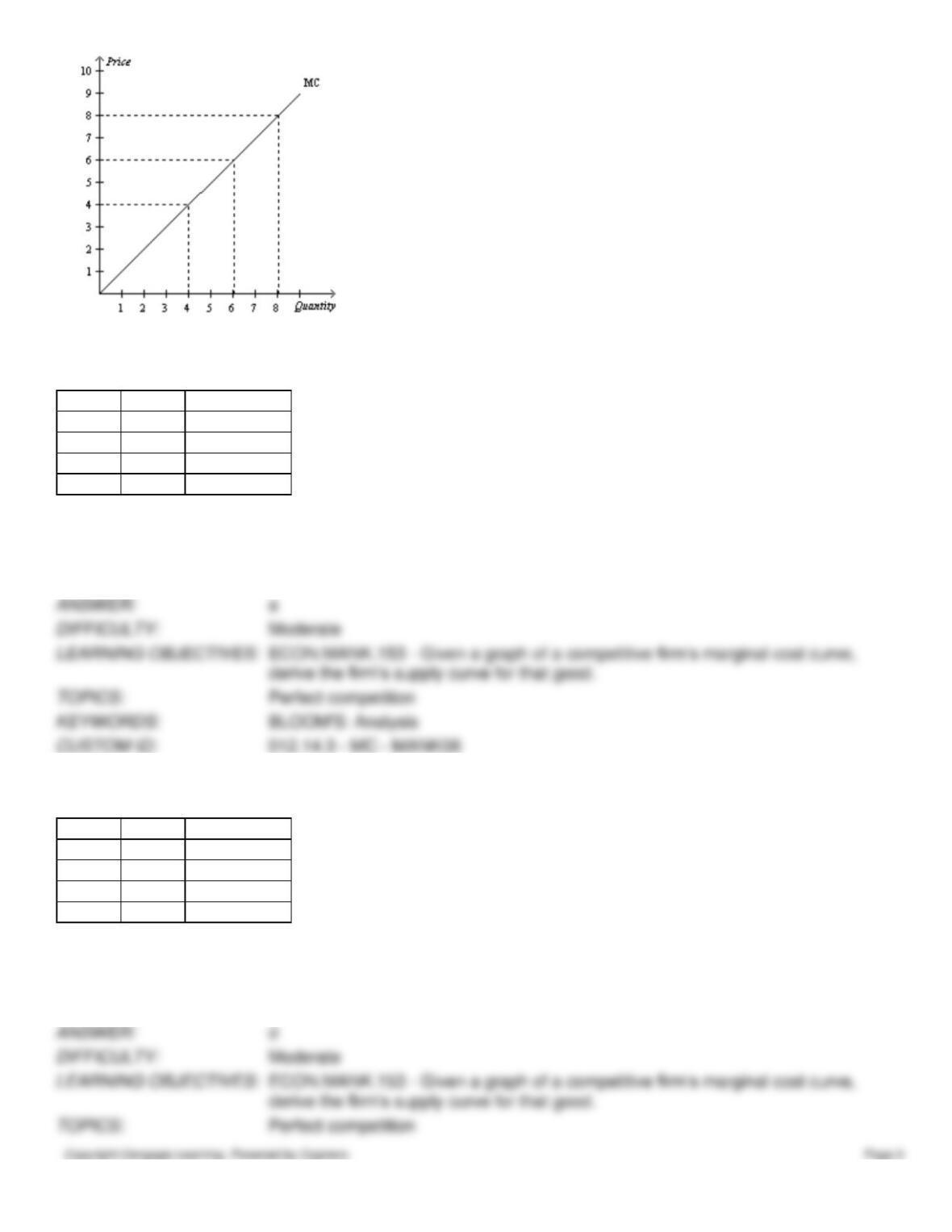

Figure 14–11

12. Refer to Figure 14-11. The figure above is for a firm operating in a competitive industry. If there were four identical

firms in the industry, which of the following price-quantity combinations would be on the market supply curve?

Point

Price

Quantity

A

$4

16

B

$4

32

C

$6

6

D

$8

64

a.

A only

b.

A and C only

c.

B only

d.

B and D only

13. Refer to Figure 14-11. The figure above is for a firm operating in a competitive industry. If there were eight identical

firms in the industry, which of the following price-quantity combinations would be on the market supply curve?

Point

Price

Quantity

A

$4

4

B

$4

32

C

$6

6

D

$8

64

a.

A only

b.

A and C only

c.

B only

d.

B and D only

14. The short-run market supply curve in a perfectly competitive industry

a.

shows the total quantity supplied by all firms at each possible price.

b.

is perfectly inelastic at the market price.

c.

is perfectly elastic at the market price.

d.

shows the variety of prices that different firms will charge for a given quantity.

15. In the short-run, a firm’s supply curve is equal to the

a.

marginal cost curve above its average variable cost curve.

b.

marginal cost curve above its average total cost curve.

c.

average variable cost curve above its marginal cost curve.

d.

average total cost curve above its marginal cost curve.

16. In a market with 1,000 identical firms, the short-run market supply is the

a.

marginal cost curve above average variable cost for a typical firm in the market.

b.

quantity supplied by the typical firm in the market at each price.

c.

sum of the prices charged by each of the 1,000 individual firms at each quantity.

d.

sum of the quantities supplied by each of the 1,000 individual firms at each price.

17. In a perfectly competitive market, the horizontal sum of all the individual firms’ supply curves is

a.

zero.

b.

equal to the industry profits.

c.

the market supply curve.

d.

a horizontal line.

18. In a perfectly competitive market, the market supply curve is

a.

the marginal cost curve above average total cost for a representative firm.

b.

the horizontal sum of all the individual firms’ supply curves.

c.

the vertical sum of all the individual firms’ supply curves.

d.

always a horizontal line.

19. In the short run for a particular market, there are 300 firms. Each firm has a marginal cost of $30 when it produces 200

units of output. $30 is above every firm’s average variable cost. One point on the market supply curve is

a.

quantity = 300; price = $30.

b.

quantity = 600,000; price = $90,000.

c.

quantity = 100,000; price = $30.

d.

quantity = 60,000; price = $30.

20. In the short run for a particular market, there are 5,000 firms. Each firm has a marginal cost of $7 when it produces

200 units of output. One point on the market supply curve is

a.

quantity = 5,000; price = $7.

b.

quantity = 35,000 price = $35,000.

c.

quantity = 1,000,000, price = $7.

d.

quantity = 1,000,000, price = $35,000.

Table 14–15

Quantity

Total Cost

0

$3

1

$8

2

$10

3

$12

4

$20

5

$35

6

$50

21. Refer to Table 14–15. What is the lowest price at which this firm would operate in the short run?

a.

$3.

b.

$4.

c.

$5.

d.

$6.

Table 14–15-a

Quantity

Total Cost

0

$4

1

$10

2

$16

3

$21

4

$24

5

$35

6

$48

22. Refer to Table 14–15–a. What is the lowest price at which this firm would operate in the short run?

a.

$5.

b.

$6.

c.

$7.

d.

$8.

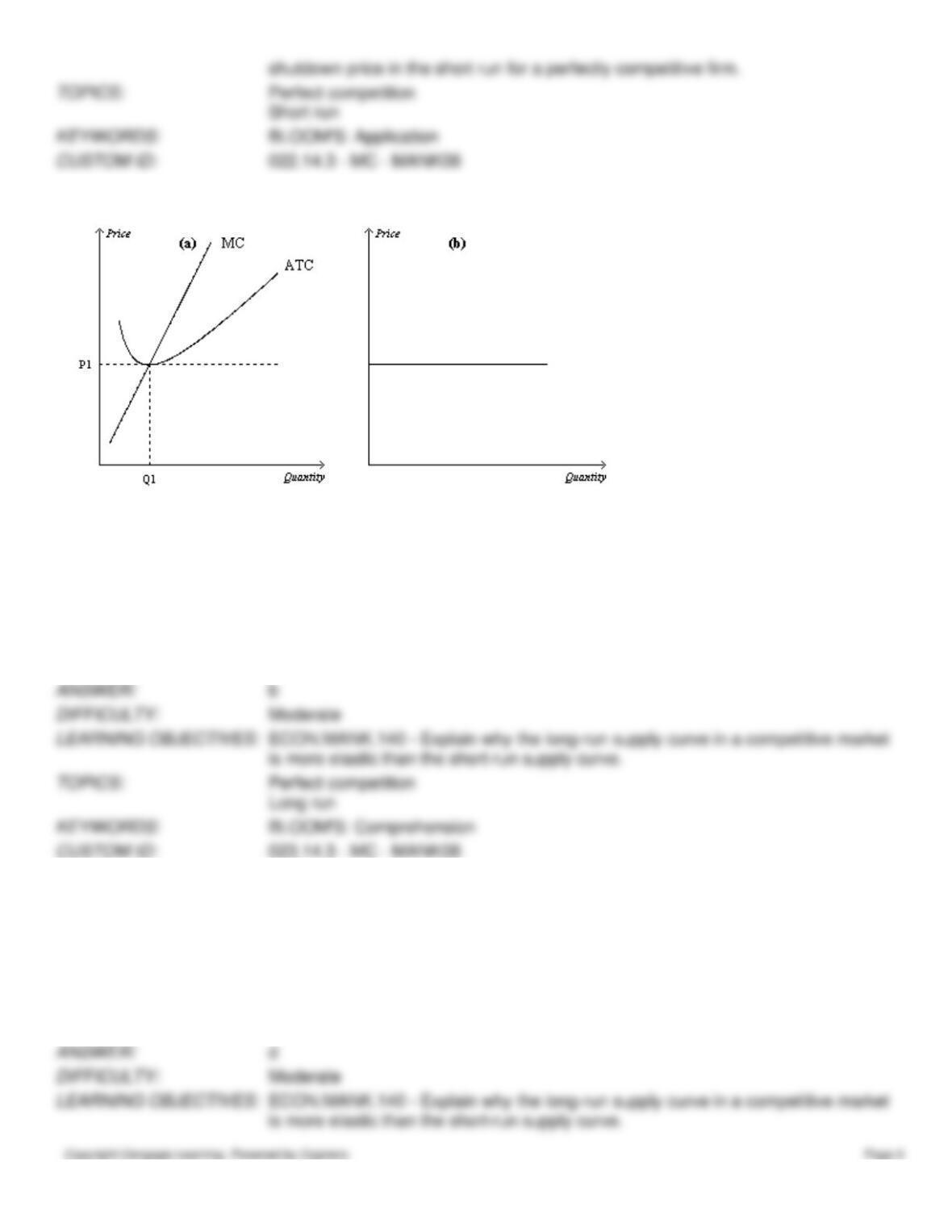

Figure 14–12

23. Refer to Figure 14-12. If the figure in panel (a) reflects the long-run equilibrium of a profit-maximizing firm in a

competitive market, the figure in panel (b) most likely reflects

a.

perfectly inelastic long-run market supply.

b.

perfectly elastic long-run market supply.

c.

the entry of firms into the industry when some resources used in production are available only in limited

quantities.

d.

the fact that zero profits cannot be sustained in the long run.

24. In a competitive market with identical firms,

a.

an increase in demand in the short run will result in a new price above the minimum of average total cost,

allowing firms to earn a positive economic profit in both the short run and the long run.

b.

firms cannot earn positive economic profit in either the short run or long run.

c.

firms can earn positive economic profit in the long run if the long-run market supply curve is upward sloping.

d.

free entry and exit into the market requires that firms earn zero economic profit in the long run even though

they may be able to earn positive economic profit in the short run.

25. When new firms enter a perfectly competitive market,

a.

economic profits of existing firms will continue to be zero.

b.

entering firms will earn zero economic profit upon entry into the market.

c.

existing firms may see their costs rise if more firms compete for limited resources.

d.

prices will rise as existing firms raise prices to keep new firms out of the market.

26. Suppose a competitive market is comprised of firms that face identical cost curves. The firms experience an increase

in demand that results in positive profits for the firms. Which of the following events are then most likely to occur?

(i)

New firms will enter the market.

(ii)

In the short run, price will rise; in the long run, price will rise further.

(iii)

In the long run, all firms will be producing at their efficient scale.

a.

(i) and (ii) only

b.

(i) and (iii) only

c.

(ii) and (iii) only

d.

(i), (ii) and (iii)

27. In the short run, there are 500 identical firms in a competitive market. The firms do not use any resources that are

available in limited quantities, and each of them has the following cost structure:

Output

Total Cost

0

$0

1

$10

2

$12

3

$15

4

$24

5

$35

The long-run supply curve for this market is

a.

positively sloped for all prices above $10.

b.

horizontal at a price of $5.

c.

horizontal at a price of $6.

d.

horizontal at a price of $7.

28. In the short run, there are 500 identical firms in a competitive market. The firms do not use any resources that are

available in limited quantities, and each of them has the following cost structure:

Output

Total Cost

0

$0

1

$10

2

$12

3

$15

4

$24

5

$35

Which of the following is a point on the long-run supply curve?

a.

P=$10, Q=500.

b.

P=$6, Q=1,000.

c.

P=$5, Q=500.

d.

P=$5, Q=1,500.

29. In the short run, a market consists of 100 identical firms. The market price is $8, and the total cost to each firm of

producing various levels of output is given in the table below. What will total quantity supplied be in the market?

Quantity

Total Costs

0

$1

1

$7

2

$14

3

$22

4

$31

5

$41

a.

200 units

b.

300 units

c.

400 units

d.

500 units

30. In the short run, a market consists of 100 identical firms. The market price is $6, and the total cost to each firm of

producing various levels of output is given in the table below. What will total quantity supplied be in the market?

Quantity

Total Costs

0

$1

1

$7

2

$12

3

$21

4

$32

5

$45

a.

100 units

b.

200 units

c.

300 units

d.

400 units

31. When existing firms in a competitive market are profitable, an incentive exists for

a.

new firms to seek government subsidies that would allow them to enter the market.

b.

new firms to enter the market, even without government subsidies.

c.

existing firms to raise prices.

d.

existing firms to increase production.

32. The assumption of a fixed number of firms is appropriate for analysis of

a.

the short run but not the long run.

b.

the long run but not the short run.

c.

both the short run and the long run.

d.

neither the short run nor the long run.

33. Entry into a market by new firms will increase the

a.

supply of the good.

b.

profits of existing firms.

c.

price of the good.

d.

marginal cost of producing the good.

34. When new firms have an incentive to enter a competitive market, their entry will

a.

increase the price of the product.

b.

drive down profits of existing firms in the market.

c.

shift the market supply curve to the left.

d.

increase demand for the product.

35. When firms have an incentive to exit a competitive market, their exit will

a.

lower the market price.

b.

necessarily raise the costs for the firms that remain in the market.

c.

raise the profits of the firms that remain in the market.

d.

shift the demand for the product to the left.

36. When new firms enter a perfectly competitive market,

a.

demand increases.

b.

the short-run market supply curve shifts right.

c.

the short-run market supply curve shifts left.

d.

existing firms will increase prices to keep the new firms from entering.

37. The entry of new firms into a competitive market will

a.

increase market supply and increase market price.

b.

increase market supply and decrease market price.

c.

decrease market supply and increase market price.

d.

decrease market supply and decrease market price.

38. The exit of existing firms from a competitive market will

a.

increase market supply and increase market price.

b.

increase market supply and decrease market price.

c.

decrease market supply and increase market price.

d.

decrease market supply and decrease market price.

39. When managers of firms in a competitive market observe falling profits, they may infer that the market is

experiencing

a.

a violation of conventional market forces.

b.

over-investment.

c.

the entry of new firms.

d.

too few firms in the market.

40. Willie’s Wading Adventures sells hip waders for fishing and duck hunting in a perfectly competitive market. If hip

waders sell for $100 each and average total cost per unit is $95 at the profit-maximizing output level, then in the long run

a.

more firms will enter the market.

b.

some firms will exit from the market.

c.

the equilibrium price per unit will rise.

d.

average total costs will fall.

41. Phil sells duck calls in a perfectly competitive market. If duck calls sell for $10 each and average total cost per unit is

$11 at the profit-maximizing output level, then in the long run

a.

more firms will enter the market.

b.

some firms will exit from the market.

c.

the equilibrium price per duck call will fall.

d.

average total costs will fall.

42. Roger owns a small health store that sells vitamins in a perfectly competitive market. If vitamins sell for $12 per bottle

and the average total cost per bottle is $12.50 at the profit-maximizing output level, then in the long run

a.

more firms will enter the market.

b.

some firms will exit from the market.

c.

the equilibrium price per bottle will fall.

d.

average total costs will fall.

43. Roger owns a small health store that sells vitamins in a perfectly competitive market. If vitamins sell for $12 per bottle

and the average total cost per bottle is $11.50 at the profit-maximizing output level, then in the long run

a.

more firms will enter the market.

b.

some firms will exit from the market.

c.

the equilibrium price per bottle will rise

d.

average total costs will rise.

44. When market conditions in a competitive industry are such that firms cannot cover their total production costs, then

a.

the firms will suffer long-run economic losses.

b.

the firms will suffer short-run economic losses that will be exactly offset by long-run economic profits.

c.

some firms will exit the market, causing prices to rise until the remaining firms can cover their total

production costs.

d.

all firms will go out of business, since consumers will not pay prices that enable firms to cover their total

production costs.

45. If occupational safety laws were changed so that firms no longer had to take expensive steps to meet regulatory

requirements, we would expect that

a.

the demand for products in this industry would increase.

b.

the market price of products in this industry would decrease in the short run but not in the long run.

c.

the firms in the industry would make a long-run economic profit.

d.

competition would force producers to pass the lower production costs on to consumers in the long run.

46. The textile industry is composed of a large number of small firms. In recent years, these firms have suffered economic

losses, and many sellers have left the industry. Economic theory suggests that these conditions will

a.

shift the demand curve outward so that price will rise to the level of production cost.

b.

cause the remaining firms to collude so that they can produce more efficiently.

c.

cause the market supply to decline and the price of textiles to rise.

d.

cause firms in the textile industry to suffer long-run economic losses.

47. Suppose that the organic-produce industry is composed of a large number of small firms. In recent years, these firms

have suffered economic losses, and many sellers have left the industry. Economic theory suggests that these conditions

will

a.

shift the demand curve outward so that price will rise to the level of production cost.

b.

cause the remaining firms to collude so that they can produce more efficiently.

c.

cause the market supply to decline and the price of organic produce to rise.

d.

cause firms in the organic-produce industry to suffer long-run economic losses.

48. If there is an increase in market demand in a perfectly competitive market, then in the short run

a.

there will be no change in the demand curves faced by individual firms in the market.

b.

the demand curves for firms will shift downward.

c.

the demand curves for firms will become more elastic.

d.

profits will rise.

49. If there is an increase in market demand in a perfectly competitive market, then in the short run prices will

a.

rise.

b.

remain unchanged at the minimum of average total cost.

c.

fall.

d.

remain unchanged at the minimum of marginal cost.

50. Which of the following statements is not correct?

a.

In a long-run equilibrium, marginal firms make zero economic profit.

b.

To maximize profit, firms should produce at a level of output where price equals average variable cost.

c.

The amount of gold in the world is limited. Therefore, the gold jewelry market probably has a long-run supply

curve that is upward sloping.

d.

Long-run supply curves are typically more elastic than short-run supply curves.

51. Which of the following statements is not correct about competitive firms?

a.

In a long-run equilibrium, firms must be operating at their efficient scale.

b.

In the short run, the number of firms in an industry may be fixed.

c.

In the long run, the number of firms can adjust to changing market conditions.

d.

In the short run, firms must be operating at a level of output where price equals average variable cost.

Scenario 14-4

Victor is the recipient of $1 million from a lawsuit. Victor decides to use the money to purchase a small business in

Florida. His business operates in a perfectly competitive industry. If Victor would have invested the $1 million in a risk–

free bond fund, he could have earned $100,000 each year. After he bought the small business, Victor quit his job as a

market analyst with Research, Inc., where he used to earn $75,000 per year.

52. Refer to Scenario 14-4. At the end of the first year of operating his new business, Victor’s accountant reported an

accounting profit of $150,000. What was Victor’s economic profit?

a.

-$150,000

b.

-$50,000

c.

-$25,000

d.

$25,000

53. Refer to Scenario 14-4. What is Victor’s opportunity costs of operating his new business?

a.

$25,000

b.

$75,000

c.

$100,000

d.

$175,000

54. Refer to Scenario 14-4. How large would Victor’s accounting profits need to be to allow him to attain zero economic

profit?

a.

$100,000

b.

$125,000

c.

$175,000

d.

$225,000

Scenario 14-5

A study sponsored by the Food Consumer Safety Board found that consumption of irradiated tomatoes increased the

health of laboratory rats. As a result of national press coverage of the report, the demand for irradiated tomatoes increased

dramatically. Organic farmers were able to switch from organic production of tomatoes to irradiated production with no

additional cost. Assume that the tomato market satisfies all of the assumptions of perfect competition.

55. Refer to Scenario 14-5. As a result of the increase in the demand for tomatoes, we would predict that in the short run

that the

a.

production of tomatoes would be at efficient scale.

b.

price of tomatoes would rise.

c.

total cost for existing irradiated tomato producers must rise.

d.

number of firms in the market would fall as prices fall and firms exit the market.

56. Refer to Scenario 14–5. If the increased production of irradiated tomatoes caused a rise in the marginal transportation

costs of moving irradiated tomatoes to market, the

a.

short-run market supply curve for irradiated tomatoes would be affected but not the long-run market supply.

b.

long-run market supply curve for irradiated tomatoes would be perfectly elastic.

c.

long-run market supply of irradiated tomatoes would be downward sloping.

d.

long-run market supply of irradiated tomatoes would be upward sloping.

57. When a profit-maximizing firm in a competitive market has zero economic profit, accounting profit

a.

is negative.

b.

is at least zero.

c.

is also zero.

d.

could be positive, negative or zero.

58. As a general rule, when accountants calculate profit they account for explicit costs but usually ignore

a.

certain outlays of money by the firm.

b.

implicit costs.