Chapter 09 – Pure Competition in the Long Run

51. In the context of analyzing economic efficiency, we can interpret the market demand

curve to be showing:

52. In the context of analyzing economic efficiency, we can interpret the market supply curve

to be showing:

53. Pure competition produces a socially optimal allocation of resources in the long run

because:

Chapter 09 – Pure Competition in the Long Run

54. When a purely competitive firm is in long-run equilibrium and is allocatively efficient:

55. Which is true of a purely competitive firm in the long-run equilibrium?

56. Resources are efficiently allocated when production occurs at that output at which:

Chapter 09 – Pure Competition in the Long Run

57. Resources are efficiently allocated when production occurs at that output level where

price:

58. When a purely competitive firm is in long-run equilibrium, price is equal to:

Chapter 09 – Pure Competition in the Long Run

59. Refer to the graph above, showing the long-run supply and demand curves in a purely

competitive market. The curves suggest that this industry is:

60. Refer to the graph above, showing the long-run supply and demand curves in a purely

competitive market. The curves suggest that in this industry, the marginal benefit to

consumers of each unit of the product is:

61. Refer to the graph above, showing the long-run supply and demand curves in a purely

competitive market. The curves suggest that in this industry, the dollars’ worth of other

products that have to be sacrificed in order to produce each unit of the output of this industry

is:

Chapter 09 – Pure Competition in the Long Run

62. Refer to the graph above, showing the long-run supply and demand curves in a purely

competitive market. We know that in this market, the marginal:

63. Refer to the graph above, showing the long-run supply and demand curves in a purely

competitive market. We know that when this market reaches equilibrium, the marginal:

64. In a purely competitive industry, an optimal allocation of scarce resources occurs when:

Chapter 09 – Pure Competition in the Long Run

9-26

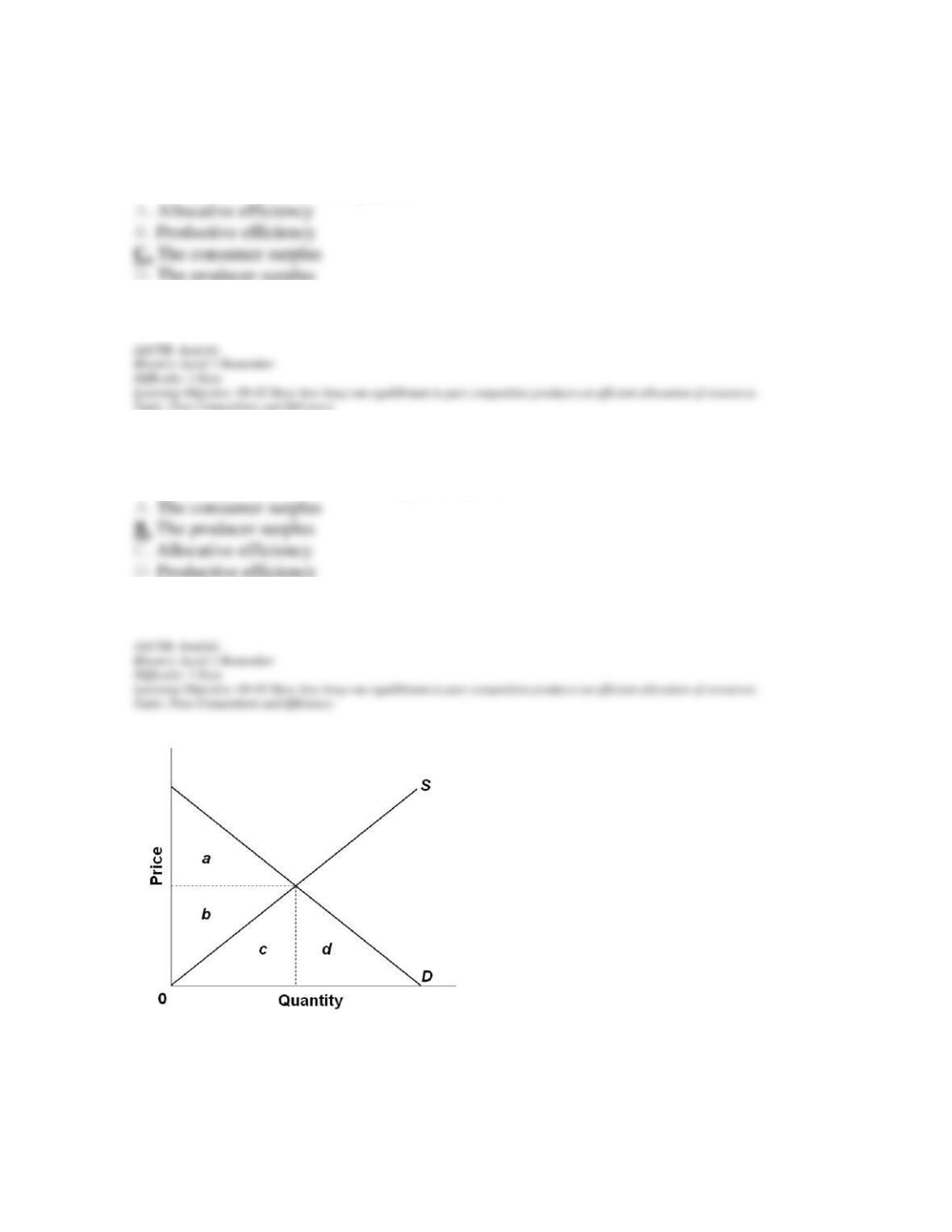

65. The difference between the maximum price a consumer is willing to pay for a product and

the actual price the consumer pays is:

66. The difference between the actual price that a producer receives and the minimum

acceptable price a producer is willing to accept is:

Chapter 09 – Pure Competition in the Long Run

67. Refer to the graph above representing the purely competitive market for a product. When

the market is at equilibrium, the consumer surplus would be represented by the area:

68. Refer to the graph above representing the purely competitive market for a product. When

the market is at equilibrium, the value of the total benefits derived by consumers from this

product would be represented by the area:

69. Refer to the graph above representing the purely competitive market for a product. When

the market is at equilibrium, the producer surplus would be represented by the area:

Chapter 09 – Pure Competition in the Long Run

70. Refer to the graph above representing the purely competitive market for a product. When

the market is at equilibrium, the total opportunity cost of producing the equilibrium output

level would be represented by the area:

71. Refer to the graph above representing the purely competitive market for a product. When

the market is at equilibrium, the total revenues from selling the equilibrium output level

would be represented by the area:

72. Refer to the graph above representing the purely competitive market for a product. When

Chapter 09 – Pure Competition in the Long Run

73. Refer to the graph above representing the purely competitive market for a product. When

allocative efficiency is attained in this market, the sum of the consumer and producer surplus

will be areas:

74. If there is allocative efficiency in a purely competitive market for a product, the maximum

price consumers are willing to pay is:

75. When there is allocative efficiency in a purely competitive market for a product, the

minimum price producers are willing to accept is:

Chapter 09 – Pure Competition in the Long Run

76. A patent gives a firm the power to charge a price that:

77. If the maker of a patented drug sells the drug at a price above the equilibrium price, then

there:

78. If the patent on a drug expires and the average price of the drug falls to a lower

equilibrium price, there will be:

Chapter 09 – Pure Competition in the Long Run

79. If a competitive firm successfully adopts a better production technology ahead of the

others, then:

80. Competitive firms will always try to earn more than a normal profit by doing the

following, except:

81. Creative destruction is most often associated with:

Chapter 09 – Pure Competition in the Long Run

82. Creative destruction is illustrated by which of the following pairs of products:

83. In the long run for a purely competitive market, there are no fixed costs.

84. When a competitive firm decides to produce no output because the product’s price is

below the average variable cost, that is a long-run decision.

Chapter 09 – Pure Competition in the Long Run

85. The short-run supply curve of a purely competitive industry tends to be steeper than the

long-run supply curve.

86. When a competitive firm is in long-run equilibrium, its accounting profits are greater than

zero.

87. When a competitive firm finds itself with an average total cost that is higher than the price

of the product in the long run, it will decide that it could do better in another industry or

market.

Chapter 09 – Pure Competition in the Long Run

88. When a competitive firm finds itself with positive profits in the long run, then it will

decide that it could do better by moving to a different industry.

89. When a competitive firm finds that in its short-run equilibrium situation, its marginal cost

is higher than its average total cost, if things are not expected to change, then the firm will

exit the industry in the long run.

90. It is possible for a competitive firm that is maximizing profits in the short run to make its

profits even bigger in the long run by expanding its plant.

Chapter 09 – Pure Competition in the Long Run

91. In long-run equilibrium, a competitive firm produces where P = MR = MC = minimum

ATC and earns normal economic profits.

92. When firms in a purely competitive industry are earning profits that are greater than

normal, the supply of the product will tend to decrease in the long run.

93. When new firms enter a purely competitive industry, the market supply curve will shift to

the left.

94. When some firms leave a purely competitive industry, the market supply curve will shift

in such a way that the remaining firms’ profits will increase.

Chapter 09 – Pure Competition in the Long Run

95. In the long run, pure competition forces firms to produce at the minimum of average total

cost and charge a price consistent with that cost.

96. A purely competitive firm that is earning positive profits in its short-run equilibrium

situation will continue to earn positive profits at the long-run equilibrium.

97. The long-run supply curve for a competitive, decreasing-cost industry is downsloping.

98. The reason why the long-run supply curve for a purely competitive industry may be

upsloping is because of diminishing marginal returns.

Chapter 09 – Pure Competition in the Long Run

99. An upward-sloping long-run supply curve indicates a constant-cost industry.

100. Productive efficiency refers to long-run market conditions where marginal cost is equal

to marginal revenue.

101. An under-allocation of resources is occurring in a purely competitive industry whenever

the price of the product is greater than marginal cost.

102. In pure competition, resources are optimally allocated when production occurs at the

output level where P=MC.

Chapter 09 – Pure Competition in the Long Run

103. Consumer surplus is the difference between the minimum price a consumer is willing to

pay for a good and the market price of the product.

104. Producer surplus is the difference between the market price a producer receives for a

product and the minimum price producers are willing to accept for a product.

105. Competitive markets produce equilibrium prices and quantities that maximize the sum of

consumer and producer surpluses.

106. If a market is allocatively efficient, it means that at the equilibrium price, the maximum

price consumers are willing to pay is equal to the minimum acceptable price for producers.

Chapter 09 – Pure Competition in the Long Run

107. Efficiency or deadweight losses occur in purely competitive markets when P = MC =

lowest ATC.

108. The operation of the “invisible hand” means the pursuit of private interests promotes

social interests in pure competition.

109. The transformative effects of competition that foster the development of new products or

new production methods benefit everyone in society.

110. From the viewpoint of a firm, competition can come even from other firms that are not in

the same industry.

Chapter 09 – Pure Competition in the Long Run

111. Creative destruction is something that our society should try to avoid, through

government regulation of business.

112. Creative destruction entails both costs as well as benefits.

113. The costs of competition’s creative destruction are often widespread, while the benefits

often accrue to only a few.