CHAPTER 9—LINEAR PROGRAMMING Key

1. When an LP objective function is to maximize profits:

2. If X > 0 in the primal solution:

3. When the primal LP problem is to maximize revenue subject to various input constraints, the shadow prices

of inputs in the dual constraints:

4. If the primal objective function is to minimize cost subject to output constraints, the dual objective function is

5. For managerial decision problems analyzed using the LP approach:

6. Unit costs are always constant if:

7. If the objective function is to maximize revenue subject to a binding labor constraint, then the shadow price

of labor is:

8. If the capital slack variable = 0, then:

9. Constrained profit maximization requires:

10. If QA > 0, then the marginal value of inputs employed:

11. Linear programming is an analytical technique used to:

12. Linear programming assumes:

13. For costs to be a linear function of output:

14. To determine the quantity to be produced by each production process at varying points along an isoquant,

managers could use:

15. When the costs of all inputs rise by a given percentage, the isocost line:

16. Profit contribution equals total:

17. Net profits equals profit contribution minus:

18. Combinations of products that generate the same level of profit are shown graphically by:

19. When the objective function coincides with the boundary of the feasible space:

20. Slack variables:

21. A negative value for a given slack variable implies:

22. If a linear programming problem involves the minimization of advertising costs subject to audience marital

status and income constraints, the objective function is:

23. If slack exists in the solution of the primal LP, the dual shadow price variable is:

24. When some capacity constraints are binding, although others are nonbinding:

25. The cost of capacity subject to constraints is:

26. Linear Programming Concepts. Indicate whether each of the following statements is true or false. Defend

your answer.

A.

Linear programming can be used for solving any type of constrained optimization problem where the relations involved can be

approximated by linear equations.

B.

Linear revenue, cost and profit relations will be observed when output prices, input prices, and average variable costs are constant.

C.

Equal distances along a given production process ray in a linear programming problem always represent an identical level of output

D.

At isoquant segment midpoints, each adjacent production process must be used to produce 50% of output efficiently.

E.

Maximizing a LP profit contribution objective function always results in also maximizing total net profits.

True. Linear revenue, cost and profit relations will be observed when output prices, input prices, and average variable costs are

constant.

27. LP Basics. Indicate whether each of the following statements is true or false and why.

A.

In profit maximization linear programming problems, negative values for slack variables are impossible.

B.

Binding constraints indicate positive slack variables at the optimum solution.

C.

Points not on process rays represent unattainable technologies.

D.

Constant input prices is the only requirement for a total cost function to be linear.

E.

Changing input prices will not alter the slope of a given isoquant line.

28. Fixed Input Relations. Extreme Biking, Inc., assembles high-end extreme mountain bicycles at a plant in

Lexington, Massachusetts. The plant uses labor (L) and capital (K) in an assembly line process to produce

output (Q) where:

Q

= 0.01L1/2K1/2

MPL

MPK

A.

Calculate how many units of output can be produced with 25 units of labor and 400 units of capital, and with 225 units of labor and

3,600 units of capital. Are returns to scale increasing, constant, or diminishing?

B.

Calculate the change in the marginal product of labor as labor grows from 25 to 36 units, holding capital constant at 400 units.

Similarly, calculate the change in the marginal product of capital as capital grows from 400 to 625 units, holding labor constant at 25

units. Are returns to each factor increasing, constant, or diminishing?

C.

Assume now and throughout the remainder of the problem that labor and capital must be combined in the ratio 25L:400K. How much

output could be produced if the company faces a constraint of L = 25,000 and K = 500,000 during the coming production period?

D.

What are the marginal products of each factor under the conditions described in part C?

With L = 25 and K = 400 available:

B.

False. Binding constraints are those constraints which intersect at the optimum solution, and therefore take on a value of zero (no excess

of the input).

False. Constant returns to scale, and constant input prices result in a linear total cost function.

False. The slope of an isocost line is given by the ratio of input prices (e.g., Y = C0/PY + (PX/PY)X). Therefore, if individual input prices

rise or fall by a given percentage, then the isocost line slope will be affected.

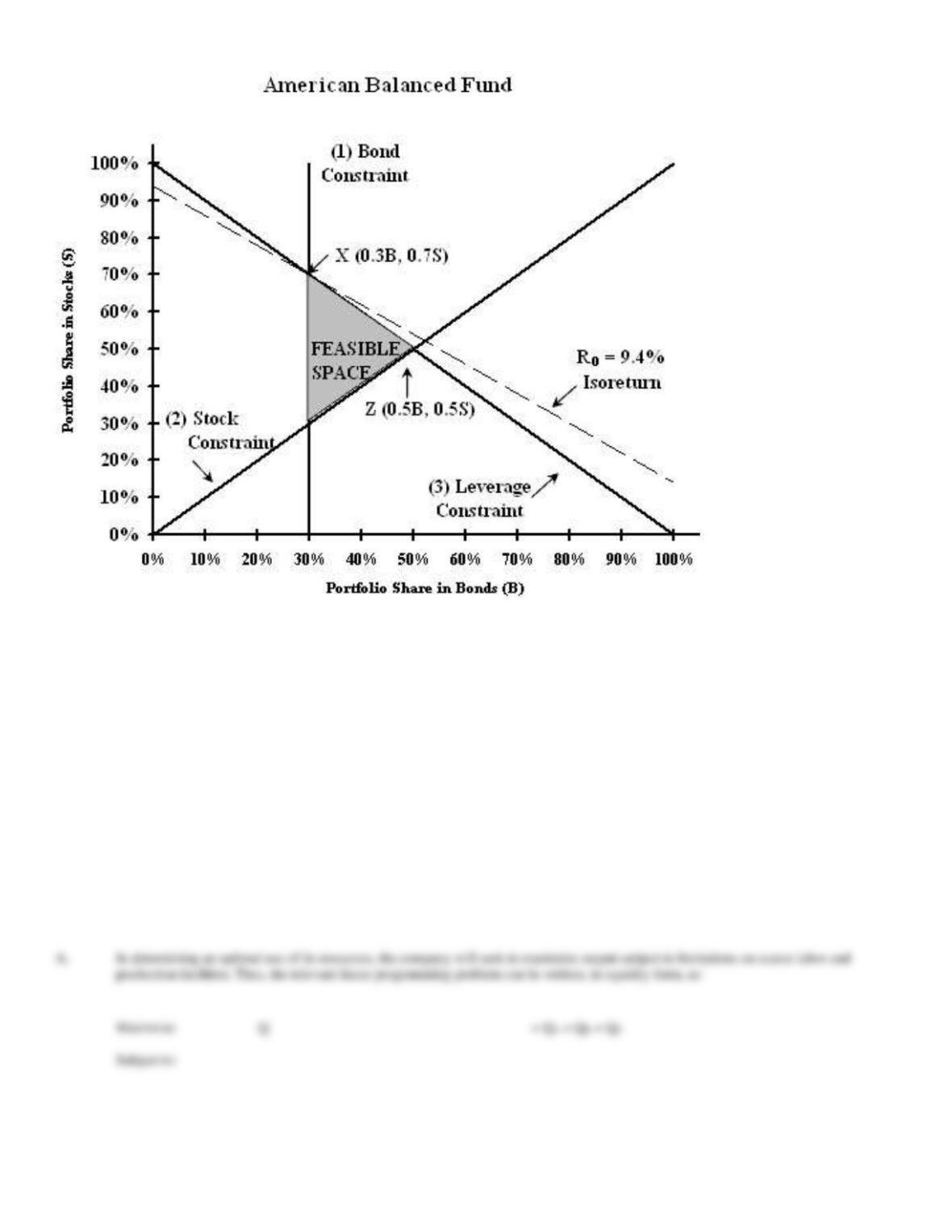

29. Return Maximization. The American Balanced Fund is an open-end investment company (mutual fund)

designed to meet the needs of investors planning for future retirement. ABF seeks to provide current income

plus capital growth by investing in a diversified portfolio of high-quality stocks and investment-grade bonds.

The fund’s bylaws state that at least 30% of the portfolio must be invested in bonds in order to reduce downside

risk during bear markets. The fund’s growth potential is maintained by a requirement that the share of the

portfolio invested in common stocks must be at least as large as the share devoted to bonds. Like most mutual

funds, ABF is prohibited from using leverage (borrowing) to enhance investor ABF returns. Without leverage,

stock and bond investments cannot exceed 100% of ABF’s portfolio. And finally, the fund’s investment

management committee currently projects an expected return of 10% on stocks and 8% on bonds.

A.

Set up and interpret the linear programming problem ABF would use to determine the optimal portfolio percentage holdings in stocks

(S) and bonds (B). Use both the inequality and equality forms of the constraint conditions.

B.

Use a graph to determine the optimal solution, and check your answer algebraically. Interpret the solution.

C.

Holding all else equal, how much would the expected return on bonds have to rise before the optimal investment policy determined in

part A would change?

D.

What is the maximum share of the portfolio that could be converted into cash if management projects a downturn in both stock and

bond prices?

In this problem, the goal is to maximize expected return, R, subject to the various stock, bond and leverage constraints. The relevant

linear programming problem is:

Thus,

= 0.001 – 0.00125 = -0.00025

diminishing.

complementary labor is also available.

capital are employed and the remaining 100,000 units are surplus.

the MPK = 0.

%

.

%

.

b

o

n

d

s

.

o

c

k

s

e

d

(point Y on the graph).

30. Optimal Production. Canine Products, Inc., produces and markets a new moist and chewy nugget dog food

called “Chow Hound” being test marketed in the San Diego market. This product is similar to several others

offered by Canine Products, and can be produced with currently available equipment and personnel using any of

three alternative product methods. Method A requires 6 hours of labor and 1 processing facility hour to produce

100 bags of dog food, QA. Method B requires 3 labor and 3 processing facility hours per QB. Method C requires

2 labor hours and 4 processing facility hours per unit of QC. Because of slack demand for other products CP

currently has 15 labor hours and 5 processing facility hours available per week for producing Chow Hound.

A.

Using the equality form of the constraint conditions, set up and interpret the linear program Canine Products would use to maximize

production of Chow Hound given currently available resources.

B.

Calculate and interpret all solution values.

Maximize:

Q

= QA + QB + QC

Subject to: