Page 1

Use the following to answer question 1:

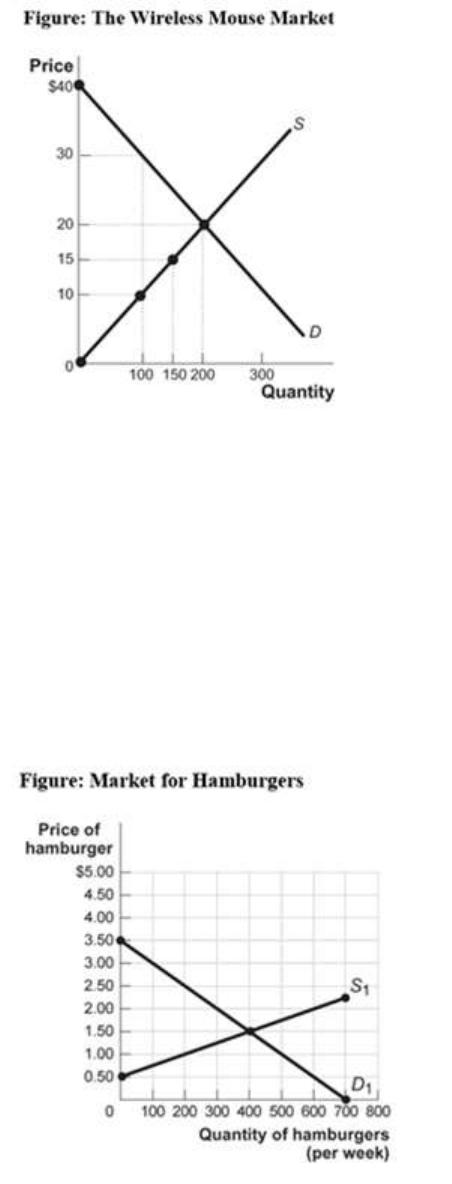

1.

(Ref 9-1 Figure: Wireless Mouse Market) Use the graph to calculate consumer surplus

when the market is at equilibrium.

A)

$4,000

B)

$5,000

C)

$2,000

D)

$3,000

Use the following to answer questions 2-4:

Page 2

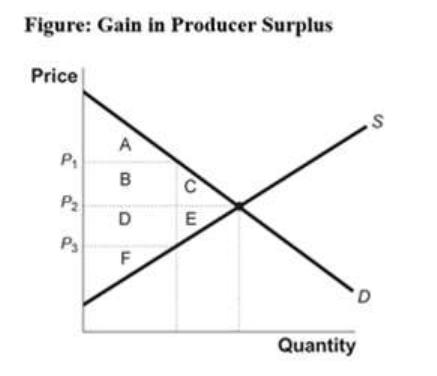

2.

(Ref 9-2 Figure: The Market for Hamburgers) The figure The Market for Hamburgers

shows the weekly market for hamburgers in Irvine, Kentucky. If the price of a

hamburger is $1 and 200 hamburgers are supplied, producer surplus will equal:

A)

$60.

B)

$65.

C)

$50.

D)

$360.

3.

(Ref 9-2 Figure: The Market for Hamburgers) The figure The Market for Hamburgers

shows the weekly market for hamburgers in Irvine, Kentucky. If 400 hamburgers are

sold, producer surplus will equal:

A)

$650.

B)

$400.

C)

$510.

D)

$200.

4.

(Ref 9-2 Figure: The Market for Hamburgers) The figure The Market for Hamburgers

shows the weekly market for hamburgers in Irvine, Kentucky. If the price of burgers

falls from $1.50 to $1.00, there is a loss in producer surplus. How much of the loss

accrues as a direct result of the hamburgers that are no longer supplied in the market?

A)

$50

B)

$45

C)

$75

D)

$90

5.

Total surplus is:

A)

the difference between price and the cost to the seller.

B)

the sum of consumer and producer surplus.

C)

equal to the area below the demand curve.

D)

always more for consumers than producers.

6.

Maximum total surplus in the market for chocolate occurs when:

A)

total net gain to producers is minimized.

B)

all consumers who value chocolate can buy chocolate.

C)

all producers can sell their chocolate.

D)

the market is in equilibrium.

Page 3

7.

The total surplus in a market is the:

A)

excess supply due to a price above the equilibrium price.

B)

surplus that accrues when a good is not scarce, defined as the total amount (if any)

by which quantity supplied exceeds quantity demanded at a zero price.

C)

net benefit to consumers, defined as the excess of consumer surplus over producer

surplus.

D)

sum of consumer surplus and producer surplus.

Use the following to answer question 8:

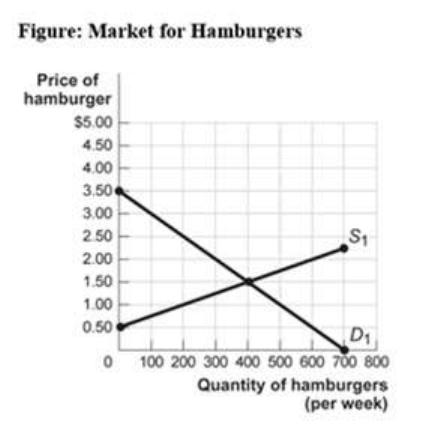

8.

Look at the figure Gain in Producer Surplus. Which areas represent producer surplus

when the price is equal to P2?

A)

D, E, and F

B)

B and C

C)

D and E

D)

A, B, and C

Page 4

Use the following to answer question 9:

9.

(Ref 9-4 Figure: The Market for Hamburgers) Look at the figure The Market for

Hamburgers. The maximum total surplus for the market is _____, and it occurs at a

price equal to _____.

A)

$550; $1.50

B)

$600; $1.50

C)

$1,050; $2

D)

Not enough information is provided to answer this question, since the maximum

total surplus could occur anywhere.

10.

Suppose you pay $10 to see Ryan Reynolds in his next movie. Suppose Mr. Reynolds

receives $31 million to work in this movie. This means that:

A)

you would have been better off being more self-reliant in the movie market.

B)

Ryan Reynolds received a producer surplus of $31 million.

C)

you received a consumer surplus of $10.

D)

you and Ryan Reynolds benefited from this transaction.

11.

Total surplus is:

A)

$50; $50

B)

$100; $50

C)

$50; $25

D)

$100; $25

Page 5

12.

Alex is willing to buy the last ticket to the Billy Bragg concert for $15, while Jake is

willing to pay $25. Alex is first in line and buys a ticket for $15. He then resells his

ticket to Jake for $20. By reselling the ticket instead of going to the concert himself,

Alex caused:

A)

the sum of the consumer and producer surplus to increase.

B)

the sum of the consumer and producer surplus to decrease.

C)

a deadweight loss of $5.

D)

consumer surplus to decrease and producer surplus to increase.

13.

Suppose the equilibrium rent for apartments in Boston is $1,600. If the city of Boston

imposes a price ceiling of $1,200, there will be a(n):

A)

increase in producer surplus for each landlord.

B)

surplus of new apartments in Boston.

C)

increase in consumer surplus for Bostonians who can find apartments for $1,200.

D)

increase in total surplus.

14.

When a market is in equilibrium and there is no outside intervention to change the

equilibrium price:

A)

total surplus is minimized.

B)

inefficiency is maximized.

C)

no mutually beneficial trades are missed.

D)

some mutually beneficial trades may be missed.

15.

If the market for grapefruit is in equilibrium without any outside intervention to change

the equilibrium price:

A)

total surplus is minimized.

B)

there is some deadweight loss.

C)

a few mutually beneficial trades are missed.

D)

consumer and producer surplus are maximized.

16.

A competitive market for cell phone chargers is in equilibrium. If the price temporarily

falls below the equilibrium price:

A)

producer surplus will rise.

B)

producer surplus will fall.

C)

the change in producer surplus is indeterminate.

D)

there will be no change in producer surplus.

Page 6

17.

When a market is efficient:

A)

there is no way to make some people better off without making other people worse

off.

B)

consumers who value buying a good the least are the ones who can purchase the

good.

C)

producers whose willingness to accept a price above the market price can sell their

good.

D)

there are ways to make everyone better off.

18.

If the government intervened in the market by lowering the price of a good below the

equilibrium price, which scenario would NOT occur?

A)

Some consumers would receive an increase in consumer surplus.

B)

Producers would likely lose some producer surplus.

C)

The outcome would be efficient.

D)

Total surplus would be lower.

19.

Which factor is key in the effectiveness of well-functioning markets?

A)

outcomes that are equitable for consumers and producers

B)

the role of the government to deliver economic signals to consumers and producers

C)

a significant degree of government intervention to maximize efficiency

D)

your right to use and dispose of your private property as you see fit

20.

Property rights are an important feature of an effective market because they:

A)

lead to the development of government control over prices.

B)

prevent harm to the environment from pollution.

C)

give owners of goods and services the right to use and dispose of those goods and

services as they choose.

D)

are the basis for an equitable tax system.

21.

The lack of property rights and inaccuracy of prices as economic signals often lead to:

A)

too much competition in markets.

B)

an increase in consumer surplus and a decrease in producer surplus.

C)

an increase in total surplus.

D)

market failure.

Page 7

22.

Market failure refers to a situation in which:

A)

markets fail to reach a fair outcome.

B)

markets establish a high price for necessities.

C)

market-determined wages are not high enough to raise all workers above the

poverty line.

D)

markets fail to reach an efficient outcome.

23.

A factor that is not a possible reason for market failure is:

A)

firms having too much market power.

B)

externalities.

C)

public goods.

D)

extremely high prices for medical care.

Use the following to answer questions 24-25:

24.

(Ref 9-5 Figure: Gain in Consumer Surplus) Refer to Figure 9-5: Gain in Consumer

Surplus. Identify the area or areas that represent the gain in consumer surplus to

consumers already participating in the market when the price falls from P1 to P2.

A)

A and B

B)

B

C)

B and C

D)

C

Page 8

25.

(Ref 9-5 Figure: Gain in Consumer Surplus) Refer to Figure 9-5: Gain in Consumer

Surplus. Identify the area or areas that represent the total change in consumer surplus

when the price falls from P1 to P2.

A)

A and B

B)

B and C

C)

D and E

D)

A, B, and C

Use the following to answer questions 26-27:

26.

(Ref 9-6 Figure: Wireless Mouse Market) Refer to Figure 9-6: Wireless Mouse Market.

Calculate producer surplus when the market is in equilibrium.

A)

$4,000

B)

$2,000

C)

$8,000

D)

$1,000

27.

(Ref 9-6 Figure: Wireless Mouse Market) Refer to Figure 9-6: Wireless Mouse Market.

Calculate the change in producer surplus when the price increases from $10 to $15.

A)

$250

B)

$1,000

C)

$625

D)

$1,125

Page 9

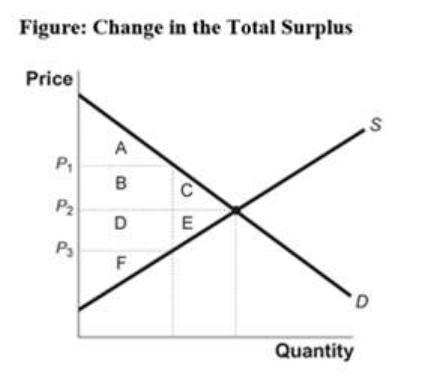

Use the following to answer questions 28-29:

28.

(Ref 9-7 Figure: Change in Total Surplus) Refer to Figure 9-7: Change in Total Surplus.

Which areas represent the change in total surplus when the price falls from P1 to P2?

A)

A, B, and C

B)

B and C

C)

B, C, D, and E

D)

C and E

29.

(Ref 9-7 Figure: Change in Total Surplus) Refer to Figure 9-7: Change in Total Surplus.

Which areas represent the change in total surplus when the price falls from P2 to P3?

A)

A, B, and C

B)

B and C

C)

B, C, D, and E

D)

C and E

Page 10

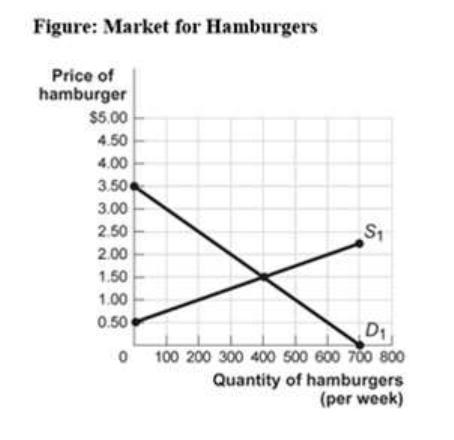

Use the following to answer questions 30-32:

30.

(Ref 9-8 Figure: The Market for Hamburgers) Refer to Figure 9-8: The Market for

Hamburgers shows the weekly market for hamburgers in Tuscaloosa. If the price of a

burger is $2, consumer surplus will equal:

A)

$650.

B)

$400.

C)

$225.

D)

$450.

31.

(Ref 9-8 Figure: The Market for Hamburgers) Refer to Figure 9-8: The Market for

Hamburgers shows the weekly market for hamburgers in Tuscaloosa. If 400 hamburgers

are sold, consumer surplus will equal:

A)

$650.

B)

$400.

C)

$225.

D)

$450.

Page 11

32.

(Ref 9-8 Figure: The Market for Hamburgers) Refer to Figure 9-8: The Market for

Hamburgers shows the weekly market for hamburgers in Tuscaloosa. If the price of a

hamburger falls from $2.00 to $1.50, the gain in consumer surplus to consumers who

are persuaded to buy at the lower price (and who were not buying when the price was

$2.00) is equal to:

A)

$100.

B)

$75.

C)

$50.

D)

$25.

Use the following to answer questions 33-45:

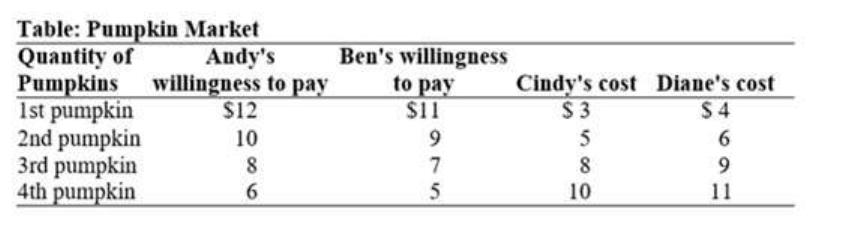

33.

(Ref 9-9 Table: Pumpkin Market) Refer to Table 9-9: The Pumpkin Market. There are

two consumers, Andy and Ben, in the market for pumpkins. Their willingness to pay for

each pumpkin is shown in the table Pumpkin Market. There are two producers of

pumpkins, Cindy and Diane, and their costs are also shown. The equilibrium price for

pumpkins is:

A)

$12.

B)

$10.

C)

$8.

D)

$6.

34.

(Ref 9-9 Table: Pumpkin Market) Refer to Table 9-9: The Pumpkin Market. There are

two consumers, Andy and Ben, in the market for pumpkins. Their willingness to pay for

each pumpkin is shown in the table Pumpkin Market. There are two producers of

pumpkins, Cindy and Diane, and their costs are also shown. The equilibrium quantity of

pumpkins is:

A)

two.

B)

three.

C)

four.

D)

five.

Page 12

35.

(Ref 9-9 Table: Pumpkin Market) Refer to Table 9-9: The Pumpkin Market. There are

two consumers, Andy and Ben, in the market for pumpkins. Their willingness to pay for

each pumpkin is shown in the table Pumpkin Market. There are two producers of

pumpkins, Cindy and Diane, and their costs are also shown. The equilibrium price for

pumpkins is $8 and the equilibrium quantity is 5. At the equilibrium price and quantity,

Andy buys _____ pumpkins and his consumer surplus is _____.

A)

four; $2

B)

three; $6

C)

two; $8

D)

one; $4

36.

(Ref 9-9 Table: Pumpkin Market) Refer to Table 9-9: The Pumpkin Market. There are

two consumers, Andy and Ben, in the market for pumpkins. Their willingness to pay for

each pumpkin is shown in the table Pumpkin Market. There are two producers of

pumpkins, Cindy and Diane, and their costs are also shown. The equilibrium price for

pumpkins is $8 and the equilibrium quantity is 5. At the equilibrium price and quantity,

Ben buys _____ pumpkins, and his consumer surplus is _____.

A)

four; $2

B)

three; $6

C)

two; $4

D)

one; $3

37.

(Ref 9-9 Table: Pumpkin Market) Refer to Table 9-9: The Pumpkin Market. There are

two consumers, Andy and Ben, in the market for pumpkins. Their willingness to pay for

each pumpkin is shown in the table Pumpkin Market. There are two producers of

pumpkins, Cindy and Diane, and their costs are also shown. The equilibrium price for

pumpkins is $8 and the equilibrium quantity is 5. At the equilibrium price and quantity,

total consumer surplus is:

A)

$10.

B)

$8.

C)

$6.

D)

$0.

Page 13

38.

(Ref 9-9 Table: Pumpkin Market) Refer to Table 9-9: The Pumpkin Market. There are

two consumers, Andy and Ben, in the market for pumpkins. Their willingness to pay for

each pumpkin is shown in the table Pumpkin Market. There are two producers of

pumpkins, Cindy and Diane, and their costs are also shown. The equilibrium price for

pumpkins is $8 and the equilibrium quantity is 5. At the equilibrium price and quantity,

Cindy sells _____ pumpkins, and her producer surplus is _____.

A)

four; $2

B)

three; $8

C)

two; $3

D)

one; $5

39.

(Ref 9-9 Table: Pumpkin Market) Refer to Table 9-9: The Pumpkin Market. There are

two consumers, Andy and Ben, in the market for pumpkins. Their willingness to pay for

each pumpkin is shown in the table Pumpkin Market. There are two producers of

pumpkins, Cindy and Diane, and their costs are also shown. The equilibrium price for

pumpkins is $8 and the equilibrium quantity is 5. At the equilibrium price and quantity,

Diane sells _____ pumpkins, and her producer surplus is _____.

A)

four; $11

B)

three; $8

C)

two; $6

D)

one; $4

40.

(Ref 9-9 Table: Pumpkin Market) Refer to Table 9-9: The Pumpkin Market. There are

two consumers, Andy and Ben, in the market for pumpkins. Their willingness to pay for

each pumpkin is shown in the table Pumpkin Market. There are two producers of

pumpkins, Cindy and Diane, and their costs are also shown. The equilibrium price for

pumpkins is $8 and the equilibrium quantity is 5. At the equilibrium price and quantity,

total producer surplus is:

A)

$0.

B)

$8.

C)

$11.

D)

$14.

Page 14

41.

(Ref 9-9 Table: Pumpkin Market) Refer to Table 9-9: The Pumpkin Market. There are

two consumers, Andy and Ben, in the market for pumpkins. Their willingness to pay for

each pumpkin is shown in the table Pumpkin Market. There are two producers of

pumpkins, Cindy and Diane, and their costs are also shown. The equilibrium price for

pumpkins is $8 and the equilibrium quantity is 5. At the equilibrium price and quantity,

total surplus is:

A)

$40.

B)

$36.

C)

$24.

D)

$8.

42.

(Ref 9-9 Table: Pumpkin Market) Refer to Table 9-9: The Pumpkin Market. There are

two consumers, Andy and Ben, in the market for pumpkins. Their willingness to pay for

each pumpkin is shown in the table Pumpkin Market. There are two producers of

pumpkins, Cindy and Diane, and their costs are also shown. The equilibrium price for

pumpkins is $8 and the equilibrium quantity is 5. If Andy consumes one more pumpkin

and Ben consumes one fewer pumpkin than in equilibrium, total surplus will _____ by

_____.

A)

increase; $17

B)

increase; $15

C)

decrease; $8

D)

decrease; $3

43.

(Ref 9-9 Table: Pumpkin Market) Refer to Table 9-9: The Pumpkin Market. There are

two consumers, Andy and Ben, in the market for pumpkins. Their willingness to pay for

each pumpkin is shown in the table Pumpkin Market. There are two producers of

pumpkins, Cindy and Diane, and their costs are also shown. The equilibrium price for

pumpkins is $8 and the equilibrium quantity is 5. If Andy consumes one fewer pumpkin

and Ben consumes one more pumpkin than in equilibrium, total surplus will _____ by

_____.

A)

increase; $17

B)

increase; $15

C)

decrease; $8

D)

decrease; $1

Page 15

44.

(Ref 9-9 Table: Pumpkin Market) Refer to Table 9-9: The Pumpkin Market. There are

two consumers, Andy and Ben, in the market for pumpkins. Their willingness to pay for

each pumpkin is shown in the table Pumpkin Market. There are two producers of

pumpkins, Cindy and Diane, and their costs are also shown. The equilibrium price for

pumpkins is $8 and the equilibrium quantity is 5. If Cindy sells one more pumpkin and

Diane sells one fewer pumpkin than in equilibrium, total surplus will _____ by _____.

A)

increase; $16

B)

increase; $14

C)

decrease; $4

D)

decrease; $2

45.

(Ref 9-9 Table: Pumpkin Market) Refer to Table 9-9: The Pumpkin Market. There are

two consumers, Andy and Ben, in the market for pumpkins. Their willingness to pay for

each pumpkin is shown in the table Pumpkin Market. There are two producers of

pumpkins, Cindy and Diane, and their costs are also shown. The equilibrium price for

pumpkins is $8 and the equilibrium quantity is 5. If Cindy sells one fewer pumpkin and

Diane sells one more pumpkin than in equilibrium, total surplus will _____ by _____.

A)

increase; $16

B)

increase; $14

C)

decrease; $1

D)

decrease; $2

46.

Which statement is true concerning the relationship between efficiency and equity?

A)

Policies designed to increase efficiency will also increase equity.

B)

Policies designed to increase equity will also increase efficiency.

C)

Policies designed to increase efficiency may decrease equity.

D)

There is no trade-off between efficiency and equity if policies are fair.

47.

If there is an increase in demand (parallel shift of demand to the right), assuming a

positively sloped supply curve and a negatively sloped demand curve, total surplus:

A)

will increase.

B)

will decrease.

C)

will remain the same.

D)

may change, but we can’t tell how.

48.

If there is an increase in supply, assuming a positively sloped supply curve and a

negatively sloped demand curve, total surplus:

A)

will increase.

B)

will decrease.

C)

will remain the same.

D)

may change, but we can’t tell how.

Page 16

49.

If there is a decrease in demand (parallel shift of demand to the right), assuming a

positively sloped supply curve and a negatively sloped demand curve, total surplus:

A)

will increase.

B)

will decrease.

C)

will remain the same.

D)

may change, but we can’t tell how.

50.

If there is a decrease in supply (parallel shift of demand to the right), assuming a

positively sloped supply curve and a negatively sloped demand curve, total surplus:

A)

will increase.

B)

will decrease.

C)

will remain the same.

D)

may change, but we can’t tell how.

51.

If total surplus falls, there may have been a(n) _____ in demand or a(n) _____ in supply.

A)

increase; decrease

B)

increase; increase

C)

decrease; decrease

D)

decrease; increase

52.

If total surplus rises, there may have been a(n) _____ in demand or a(n) _____ in

supply.

A)

increase; decrease

B)

increase; increase

C)

decrease; decrease

D)

decrease; increase

Page 17

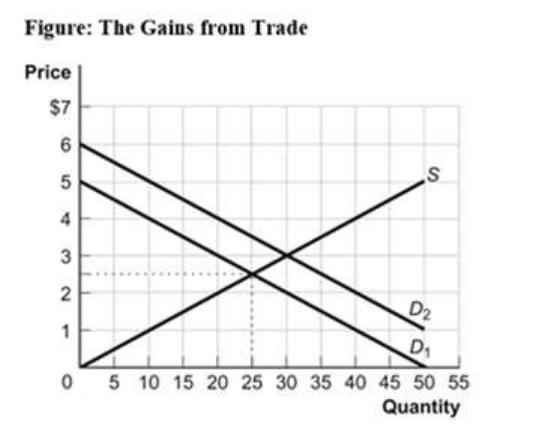

Use the following to answer questions 53-55:

53.

(Ref 9-10 Figure: The Gains from Trade) Refer to Figure 9-10: The Gains from Trade.

What is the total surplus in this market when the demand curve is D1 and the market is

in equilibrium?

A)

$25.00

B)

$31.25

C)

$62.50

D)

$90.00

54.

(Ref 9-10 Figure: The Gains from Trade) Refer to Figure 9-10: The Gains from Trade.

What is the total surplus in this market when the demand curve is D2 and the market is

in equilibrium?

A)

$31.25

B)

$45.00

C)

$62.50

D)

$90.00

55.

(Ref 9-10 Figure: The Gains from Trade) Refer to Figure 9-10: The Gains from Trade.

When demand increases from D1 to D2, equilibrium total surplus:

A)

decreases by $10.00.

B)

increases by $12.75.

C)

decreases by $15.00.

D)

increases by $27.50.

Page 18

56.

Coffee and tea are substitutes in consumption. If there is an increase in the price of

coffee, assuming a positively sloped supply curve and a negatively sloped demand

curve, total surplus in the tea market:

A)

will increase.

B)

will decrease.

C)

will not change.

D)

may change, but we cannot determine the change without more information.

57.

If a frost destroys much of the grapefruit crop, assuming a positively sloped supply

curve and a negatively sloped demand curve, total surplus in the grapefruit market:

A)

will increase.

B)

will decrease.

C)

will not change.

D)

may change, but we cannot determine the change without more information.

58.

If the price is above the equilibrium price in the market for grapefruit, assuming a

positively sloped supply curve and a negatively sloped demand curve, total surplus:

A)

will be greater than if price were at equilibrium.

B)

will be less than if price were at equilibrium.

C)

will be the same as if price were at equilibrium.

D)

may be different than if price were at equilibrium, but we cannot determine this

without more information.

59.

If the price is below the equilibrium price in the market for grapefruit, assuming a

positively sloped supply curve and a negatively sloped demand curve, total surplus:

A)

will be greater than if price were at equilibrium.

B)

will be less than if price were at equilibrium.

C)

will be the same as if price were at equilibrium.

D)

may be different than if price were at equilibrium, but we cannot determine this

without more information.

60.

Suppose a competitive market has a downward-sloping demand curve and a horizontal

supply curve. If the supply curve shifts downward, equilibrium price will _____,

equilibrium quantity will _____, consumer surplus will _____, and producer surplus

will _____.

A)

decrease; increase; increase; decrease

B)

decrease; decrease; increase; not change

C)

decrease; increase; increase; not change

D)

decrease; increase; not change; increase

Page 19

Use the following to answer questions 61-63:

61.

(Ref 9-10 Figure: Consumer and Producer Surplus) Refer to Figure 9-10: Consumer and

Producer Surplus. If the price is held above equilibrium, consumer surplus will be

_____ if the market were in equilibrium and total surplus will be _____ if the market

were in equilibrium.

A)

greater than; less than

B)

less than; the same as

C)

greater than; the same as

D)

less than; less than

62.

(Ref 9-10 Figure: Consumer and Producer Surplus) Refer to Figure 9-10: Consumer and

Producer Surplus. If the price is held below equilibrium, producer surplus will be _____

if the market were in equilibrium and total surplus will be _____ if the market were in

equilibrium.

A)

less than; less than

B)

greater than; the same as

C)

less than; the same as

D)

greater than; less than

63.

(Ref 9-10 Figure: Consumer and Producer Surplus) Refer to Figure 9-10: Consumer and

Producer Surplus. An increase in supply will:

A)

increase consumer surplus.

B)

will have no impact on consumer surplus

C)

decrease consumer surplus

D)

not enough information to determine the impact on consumer surplus

Page 20

64.

Peanut butter is an inferior good. If there is an increase in income, total surplus in the

peanut butter market:

A)

will increase.

B)

will decrease.

C)

will not change.

D)

may change, but we cannot determine the change without more information.

65.

If the technology of producing peanuts improves, total surplus in the peanut butter

market:

A)

will increase.

B)

will decrease.

C)

will not change.

D)

may change, but we cannot determine the change without more information.

66.

The total surplus generated in the market for blackberries is the total net gain to

consumers in that market.

A)

True

B)

False

67.

Total surplus is the excess of consumer surplus over producer surplus.

A)

True

B)

False

68.

The gains from trade are the reason that consumers and producers are better off

participating in a market economy than they would be if each tried to be self-sufficient.

A)

True

B)

False

69.

Total surplus shows the total benefit to society from production and consumption of a

good.

A)

True

B)

False

70.

Total surplus in a market is the excess of the number of consumers above the optimum

number.

A)

True

B)

False

Page 21

71.

Total surplus in a market is the number of extra consumers and producers that are not

needed for the market to come to an equilibrium price and quantity.

A)

True

B)

False

72.

When there is a positive amount of total surplus in a market, it means that the cost of

producing the good is zero.

A)

True

B)

False

73.

If the market for smartphones is initially in equilibrium at a price of $250 and

consumption is reallocated so that Amanda, who values a phone at $300, is required to

give it to Brent, who values a phone at $225, total surplus in the smartphone market will

increase.

A)

True

B)

False

74.

If the market for tickets to the World Series is in equilibrium but owners of tickets who

would have sold their tickets are not allowed to sell, while fans who would not sell their

tickets are required to sell, total surplus would decrease.

A)

True

B)

False

75.

If the market for concert tickets is in equilibrium and the fire marshal tries to reduce the

number of tickets sold, all other things equal, total surplus will decrease.

A)

True

B)

False

76.

Efficiency exists when there is no way to make someone better off without making

someone else worse off.

A)

True

B)

False

77.

Prices above equilibrium on agricultural products like milk exist to maximize the

consumer surplus.

A)

True

B)

False

Page 22

78.

There is a trade-off between equity and efficiency in that policies designed to promote

equity often come at the cost of decreased efficiency.

A)

True

B)

False

79.

Policies designed to promote efficiency will never decrease equity; however, policies

designed to promote equity will usually decrease efficiency.

A)

True

B)

False

80.

Efficiency deals with helping society decide what its goals should be.

A)

True

B)

False

81.

Efficiency addresses the best way to achieve a goal once it has been determined.

A)

True

B)

False

82.

Property rights and the role of prices as economic signals are two features that make

markets function effectively.

A)

True

B)

False

83.

If property rights are restricted by government regulation, many more mutually

beneficial transactions will occur.

A)

True

B)

False

84.

Property rights benefit sellers of goods much more than they benefit consumers.

A)

True

B)

False

85.

Prices are important economic signals because they convey information about how

much consumers are willing to pay for a good and how much it costs sellers to produce

a good.

A)

True

B)

False

Page 23

86.

Prices are important economic signals because they convey information about how

much producers are willing to pay for a good and how much it costs consumers to

produce a good.

A)

True

B)

False

87.

Market failure occurs when a market fails to produce efficient outcomes for society.

A)

True

B)

False

88.

When a monopolist prevents mutually beneficial trades from occurring, total surplus

increases.

A)

True

B)

False

89.

Externalities occur when the welfare of others not involved in the production or

consumption of a good or service are affected in ways that markets don’t take into

account on their own.

A)

True

B)

False

90.

A price below the equilibrium price will cause a reduction in consumer surplus.

A)

True

B)

False

Use the following to answer questions 91-92:

Page 24

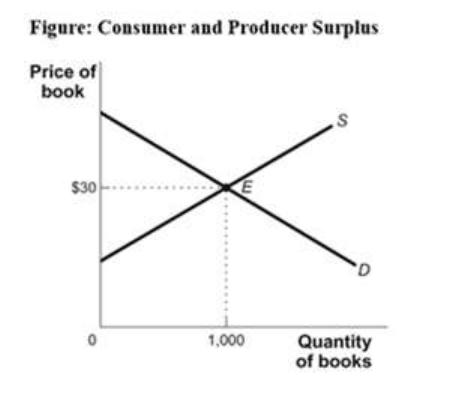

91.

(Ref 9-11 Figure: The Market for Books) Refer to Figure 9-11: The Market for Books.

At the equilibrium price of $24, find the total surplus in the market for books.

92.

(Ref 9-11 Figure: Market for Books) Refer to Figure 9-11: The Market for Books.

Suppose the price is temporarily $18. Do consumers gain or lose from this price, and by

how much? Do producers gain or lose from this price control, and by how much? How

is total surplus affected?

93.

Well-functioning markets allow:

A)

mutually beneficial trades to take place.

B)

consumers to gain at the expense of producers.

C)

producers to reap greater benefits, since they have greater power in the market.

D)

property rights to be unnecessary components of effective distribution.

Use the following to answer questions 94-96:

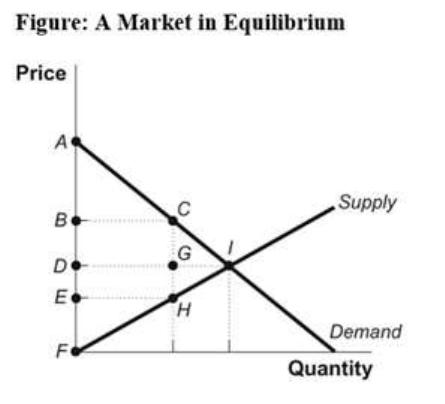

94.

(Ref 9-12 Figure: A Market in Equilibrium) Refer to Figure 9-12: A Market in

Equilibrium. At the equilibrium price, this market’s consumer surplus is equal to the

area:

A)

ABC.

B)

ADI.

C)

DIF.

D)

EHF.

Page 25

95.

(Ref 9-12 Figure: A Market in Equilibrium) Refer to Figure 9-12: A Market in

Equilibrium. At the equilibrium price, this market’s producer surplus is equal to the area:

A)

ADI.

B)

EHF.

C)

AIF.

D)

DIF.

96.

(Ref 9-12 Figure: A Market in Equilibrium) Refer to Figure 9-12: A Market in

Equilibrium. At the equilibrium price, this market’s total producer and consumer surplus

equals the area:

A)

BCDG.

B)

AIF.

C)

DIF.

D)

ADI.

97.

Suppose purchases do not occur because the value of the good to the potential seller

exceeds the value to a potential consumer. This situation will occur in:

A)

a market dominated by government regulation.

B)

well-functioning markets.

C)

a market made up of many buyers and sellers.

D)

a centralized market system.

98.

Markets work because they allocate sales to the sellers who are willing and able to

produce the good at the lowest cost. This statement shows how markets maximize:

A)

producer surplus.

B)

consumer surplus.

C)

total surplus.

D)

deadweight loss.

99.

Well-defined property rights:

A)

can allow for mutually beneficial trades.

B)

will result in government regulation.

C)

often result in more market failures.

D)

lead to more centralized decision making.

100.

Economic signals:

A)

result in shortages and surpluses.

B)

interfere with the trades that can be mutually beneficial.

C)

guide decision makers in their transactions in the marketplace.

D)

never provide adequate information to consumers.

Page 26

101.

Which statement(s) is/are true about market failures?

I. They arise when property rights are clearly defined.

II. They arise when information is available to all decision makers.

III. They arise when external costs are not considered in production decisions by

producers.

A)

I

B)

I and II

C)

III

D)

I, II, and III

Page 28

Page 29