Name:

Class:

Date:

Chapter 09: Monopoly

a.

e × f

b.

d × f

c.

c × g

d.

a × f

e.

b × g

107. If a monopolist that does not practice price discrimination is operating at an output level where price equals average

total cost, we can conclude that:

a.

its economic profit is $0.

b.

it is not maximizing profit.

c.

it should go out of business in the long run.

d.

it is not earning a normal profit.

e.

it should shut down in the short run.

108. In the short run, a monopolist will always shut down when:

a.

total cost is greater than total revenue at all output levels.

b.

total variable cost is greater than fixed cost.

c.

total revenue is greater than total variable cost at all output levels.

d.

total revenue is greater than fixed cost at all output levels.

e.

total variable cost is greater than total revenue at all output levels.

109. The supply curve for a monopolist:

a.

is its marginal cost curve.

b.

is vertical because there are no close substitutes for its product.

c.

is horizontal because there are no close substitutes for its product.

d.

slopes upward.

e.

does not exist.

Name:

Class:

Date:

Chapter 09: Monopoly

110. Which of the following factors explain the difference in long-run profits earned by a monopolist and a perfectly

competitive firm?

a.

Monopolists experience economies of scale.

b.

Perfectly competitive firms have high opportunity costs.

c.

The demand for the monopolist’s output is inelastic.

d.

The demand for the monopolist’s output is elastic.

e.

There are no barriers to entry in perfect competition.

111. Which of the following is most likely to be true of a monopoly in long-run equilibrium if it enjoys a patent and earns

economic profit in the short run?

a.

It will earn only a normal profit in the long run.

b.

It will suffer an economic loss and stop producing in the long run.

c.

It will earn a positive economic profit in the long run.

d.

It will achieve productive efficiency in the long run.

e.

It will achieve allocative efficiency in the long run.

112. Barriers to entry:

a.

cause monopolies to experience diseconomies of scale in the long run.

b.

prevent monopolies from earning profit in the short run.

c.

may allow monopolies to earn profit in the long run.

d.

prevent government from regulating a monopoly.

e.

prevent a natural monopoly from raising its price.

113. The figure below shows the cost and revenue curves for a monopolist that does not practice price discrimination. The

consumer surplus at the profit-maximizing level of output is:

Figure 9.6

Name:

Class:

Date:

Chapter 09: Monopoly

a.

represented by the area under the demand curve and above the price line corresponding to $136.

b.

represented by the area under the demand curve and above the line corresponding to an average total cost of

$110.

c.

represented by the area under the marginal revenue curve and the line corresponding to a marginal revenue of

$60.

d.

$0.

e.

equal to total consumer expenditure.

114. The figure below shows the cost and revenue curves for a monopolist. The output level that is most likely to achieve

allocative efficiency in this market is _____.

Figure 9.6

a.

700 units

b.

810 units

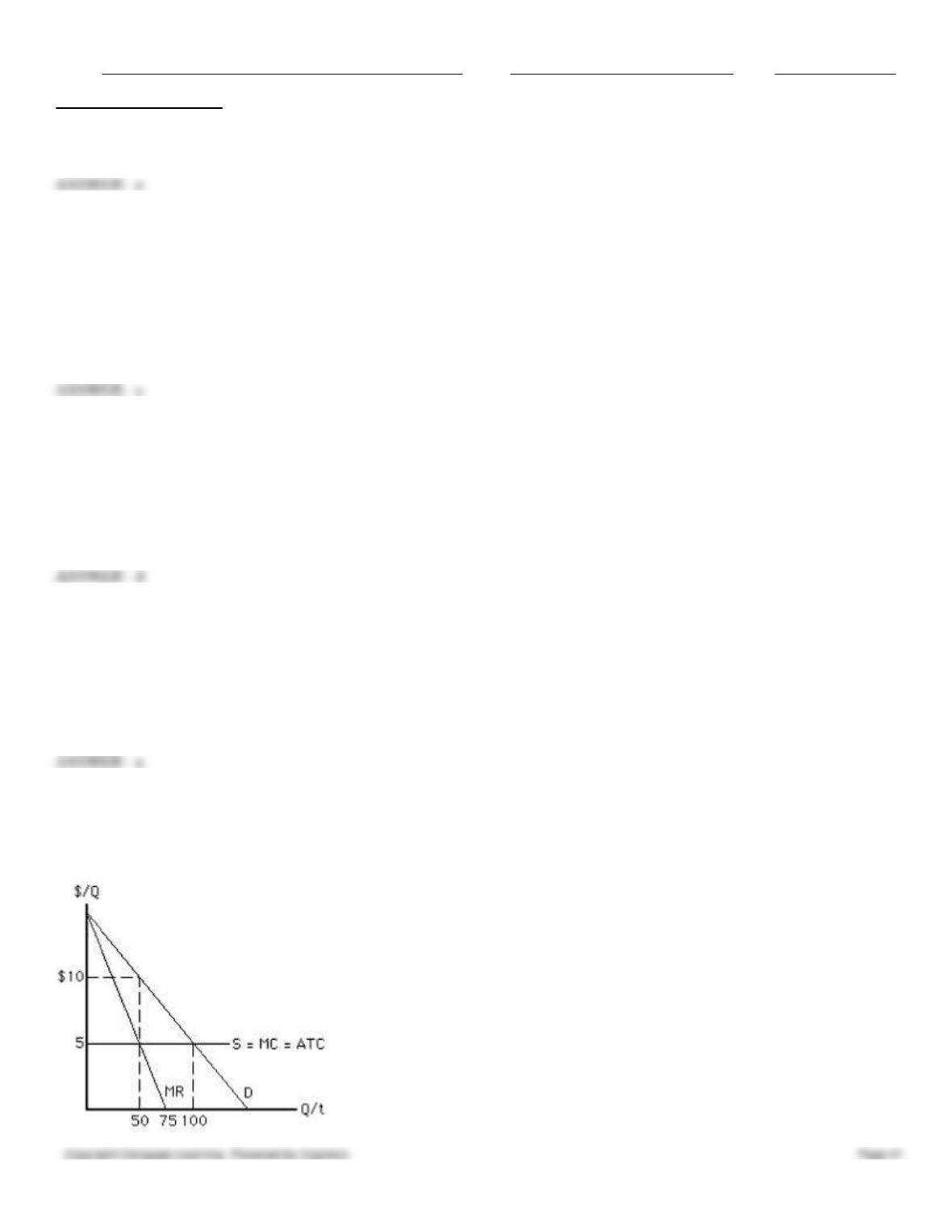

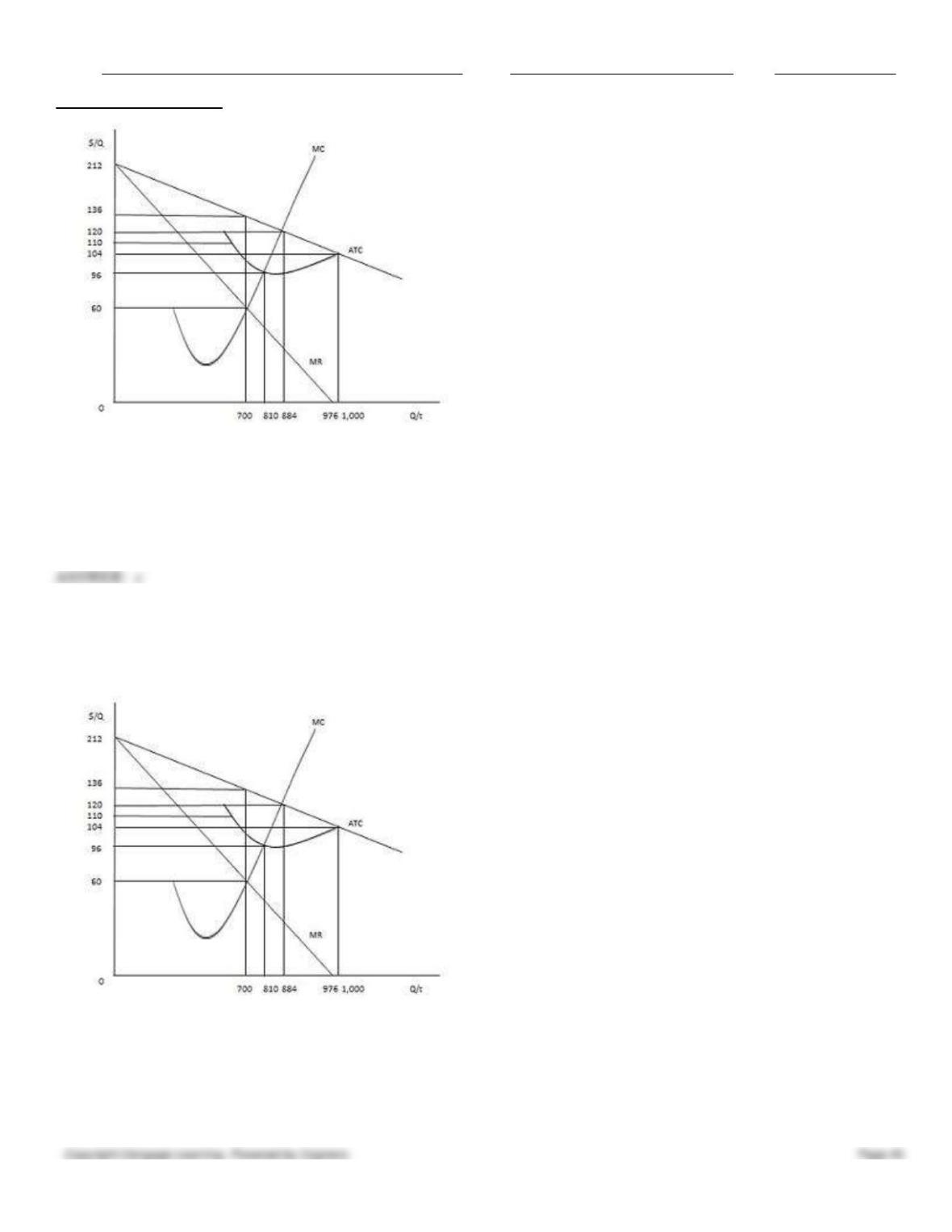

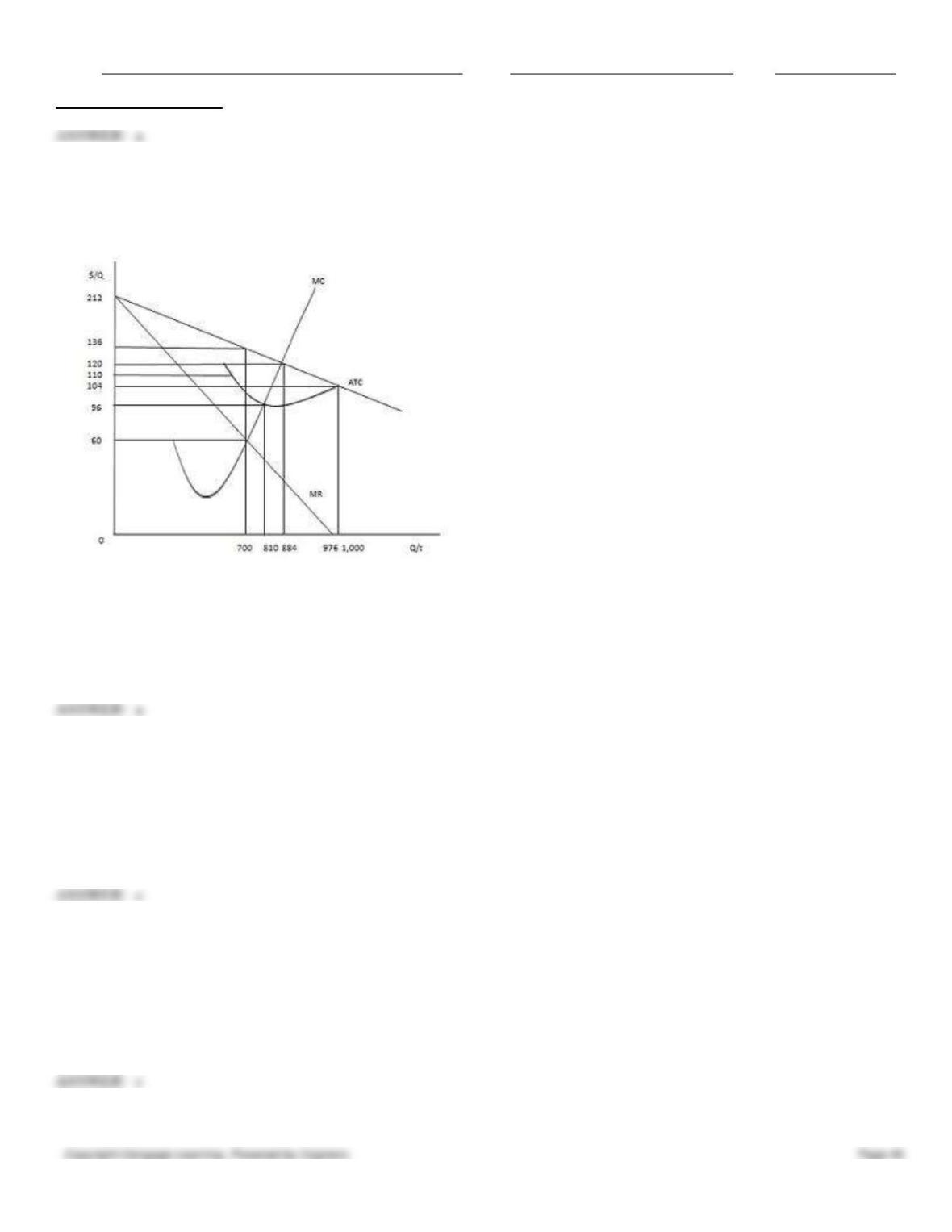

c.

884 units

d.

976 units

e.

1,000 units

115. Which of the following is true for both perfect competition and monopoly?

a.

Firms produce a differentiated product.

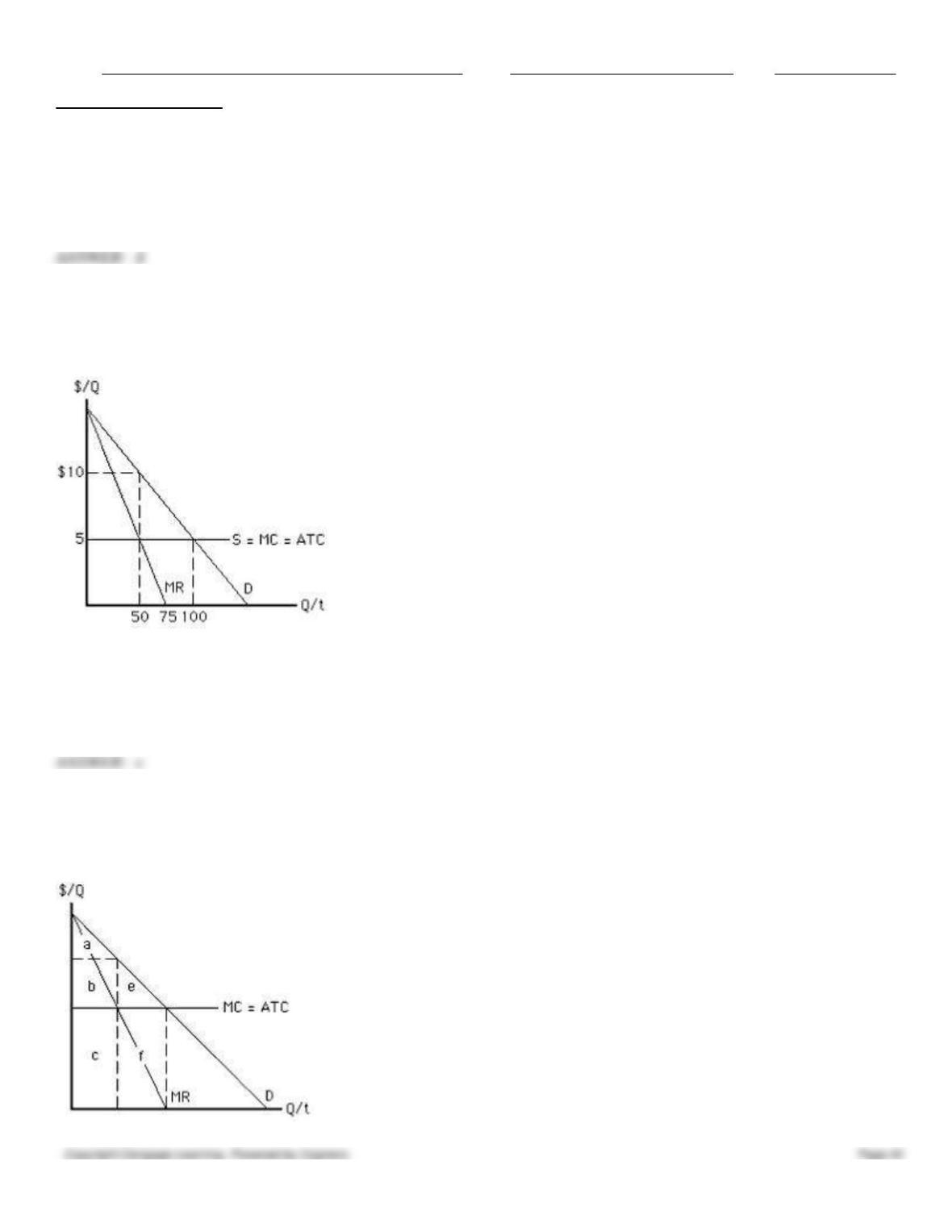

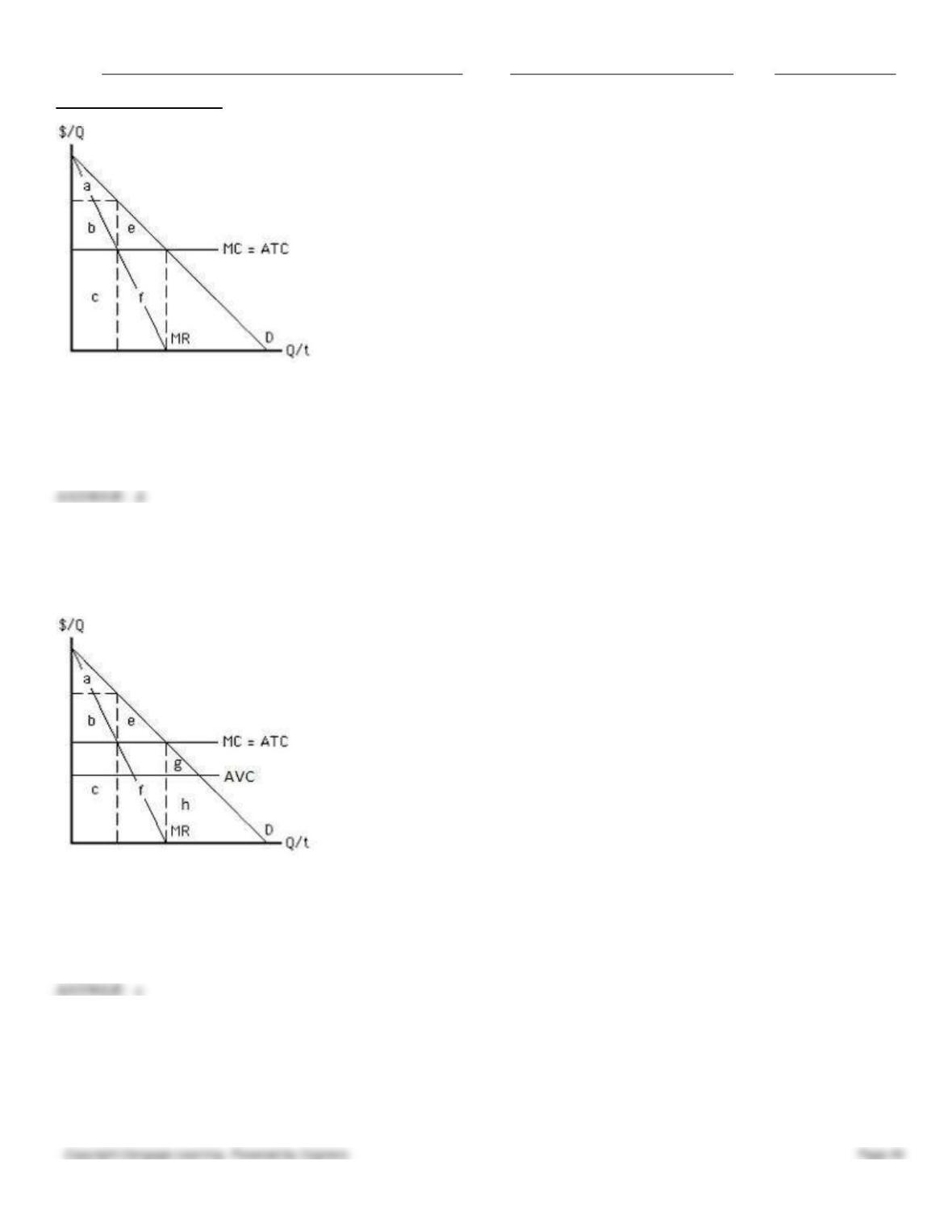

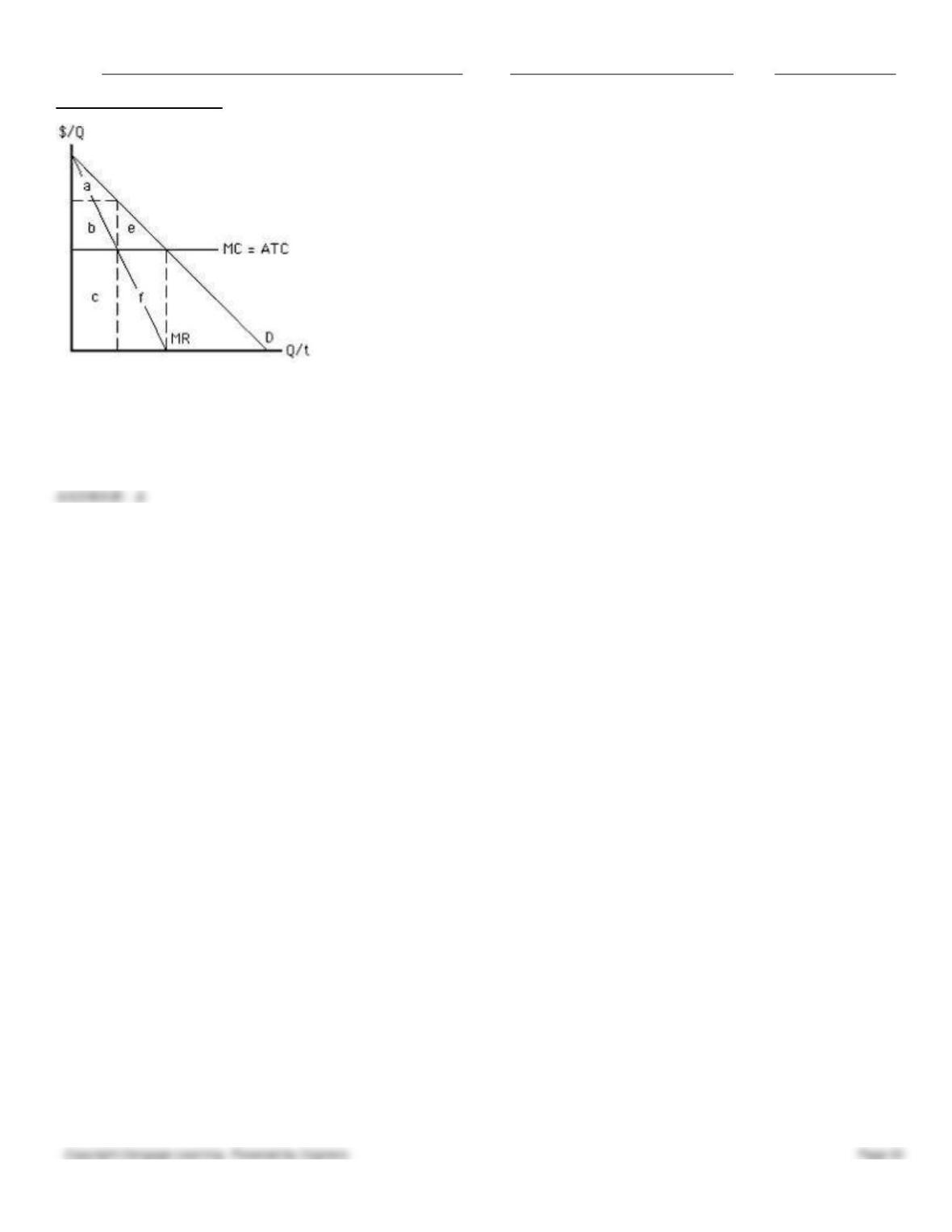

b.

Firms cannot earn economic profit in the long run.

c.

Individual firms have no ability to control the price of their output but must accept the market price.

d.

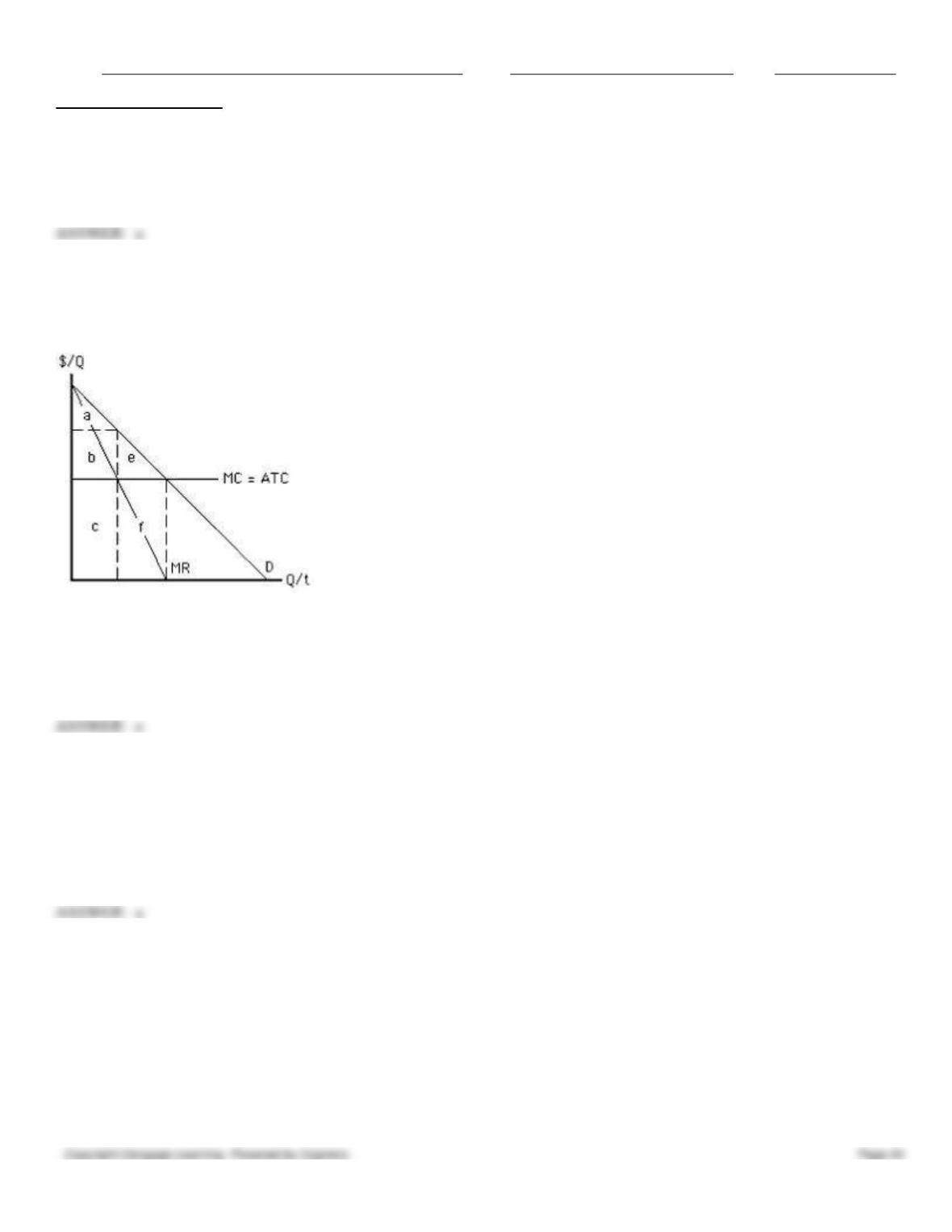

Firms go out of business in the long run if total revenue cannot cover total cost.

e.

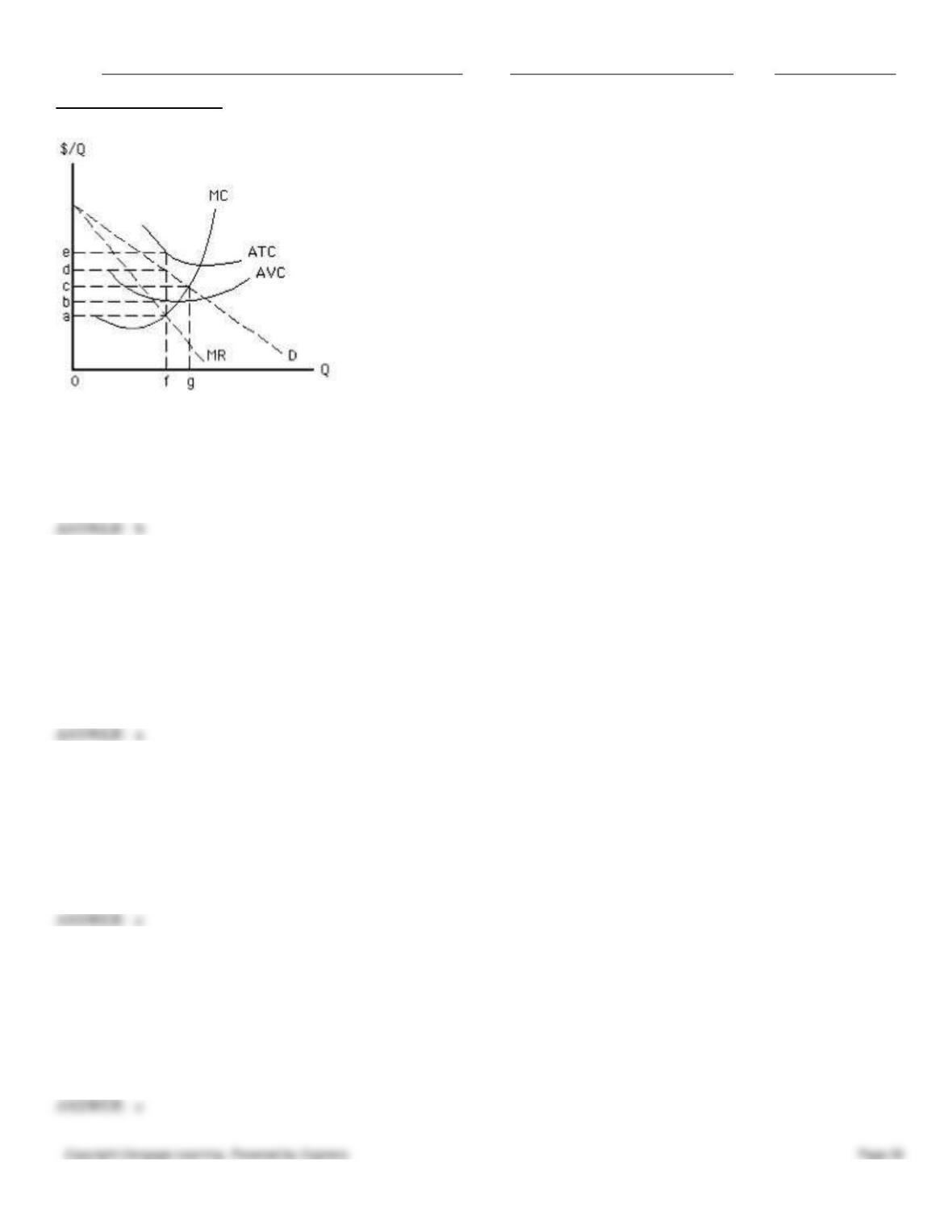

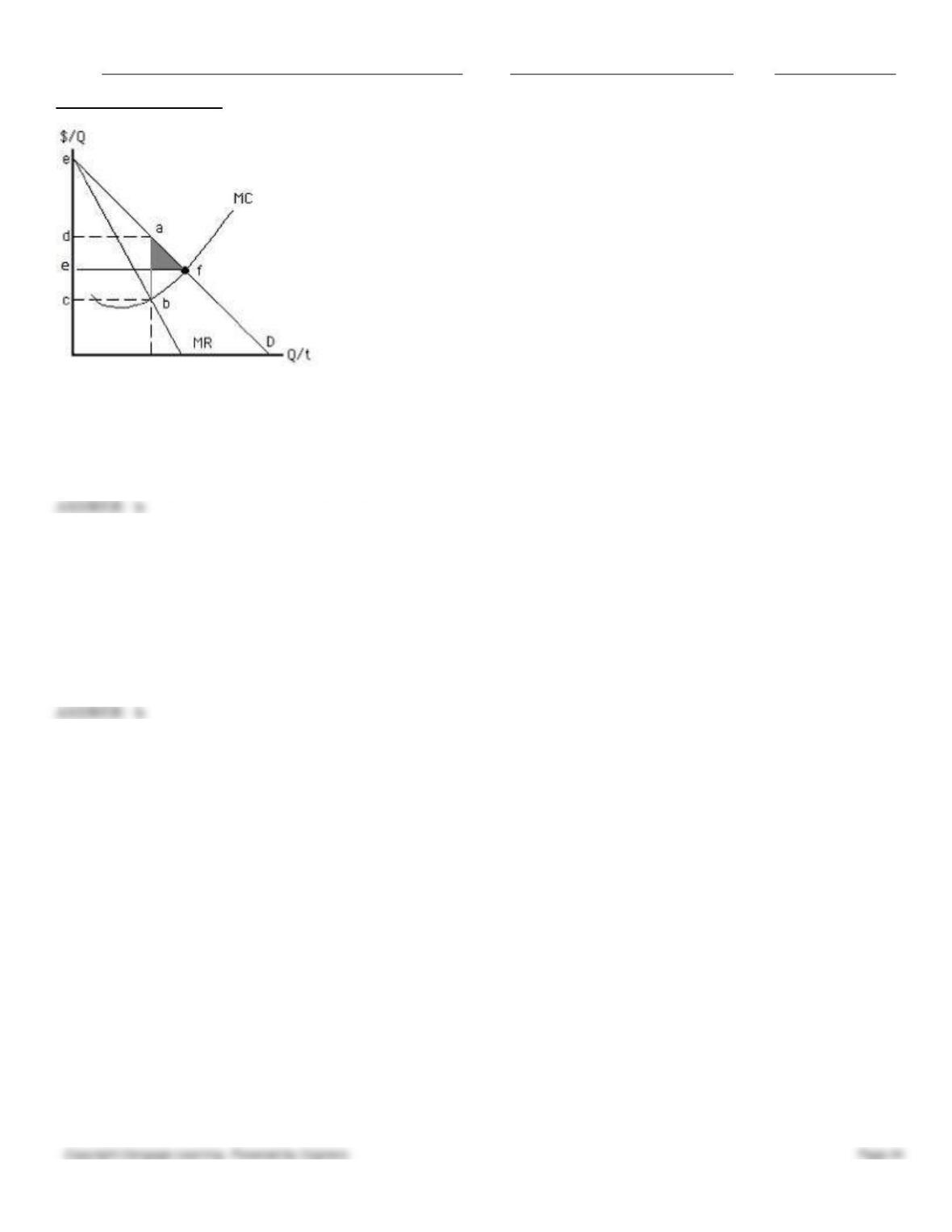

Firms usually earn economic profit in the long run.

116. Unlike perfectly competitive firms, monopolists:

a.

earn positive short-run economic profit even if price is less than average variable cost at all rates of output.

Name:

Class:

Date:

Chapter 09: Monopoly

b.

sell any quantity of output at any price they choose.

c.

earn long-run economic profits.

d.

reduce the sales of firms in other industries through advertising.

e.

face a perfectly elastic demand curve.

117. Which of the following is true when a perfectly competitive firm is in short-run equilibrium but not when a non–

discriminating monopolist is in equilibrium?

a.

Price equals marginal cost.

b.

Price is greater than marginal cost.

c.

Marginal revenue equals marginal cost.

d.

Marginal revenue is less than marginal cost.

e.

Marginal revenue is greater than average revenue.

118. Which of these is a key difference between a perfectly competitive firm and a monopolist that does not practice price

discrimination?

a.

The marginal cost curve is U-shaped for a perfectly competitive firm but not for a monopolist.

b.

Price is equal to average revenue for a perfectly competitive firm in equilibrium but not for a monopolist.

c.

Price is equal to marginal revenue for a perfectly competitive firm in equilibrium but not for a monopolist.

d.

The average revenue curve is the demand curve for a perfectly competitive firm but not for a monopolist.

e.

A monopolist aims to maximize profits, while a perfectly competitive firm tries to maximize total revenue.

119. When compared to firms in perfect competition, monopolists tend to charge:

a.

lower prices and offer lower quantities of output.

b.

higher prices and offer lower quantities of output.

c.

lower prices and offer higher quantities of output.

d.

higher prices and offer higher quantities of output.

e.

higher prices but offer the same quantity of output.

120. Which of the following would distinguish a competitive firm from a monopolist?

a.

The slope of the marginal cost curve faced by the firm

b.

The slope of the demand curve faced by the firm

c.

The rule of profit maximization followed by the firm

d.

The relationship between the firm’s marginal revenue and total revenue

e.

The existence of diseconomies of scale in production

121. If the government breaks up a monopoly that does not practice discrimination and faces a horizontal marginal cost

curve into a perfectly competitive market, _____.

a.

output and price will decrease

b.

output will increase and price will decrease

Name:

Class:

Date:

Chapter 09: Monopoly

c.

output and price will increase

d.

output will decrease and price will increase

e.

output and price will remain unchanged

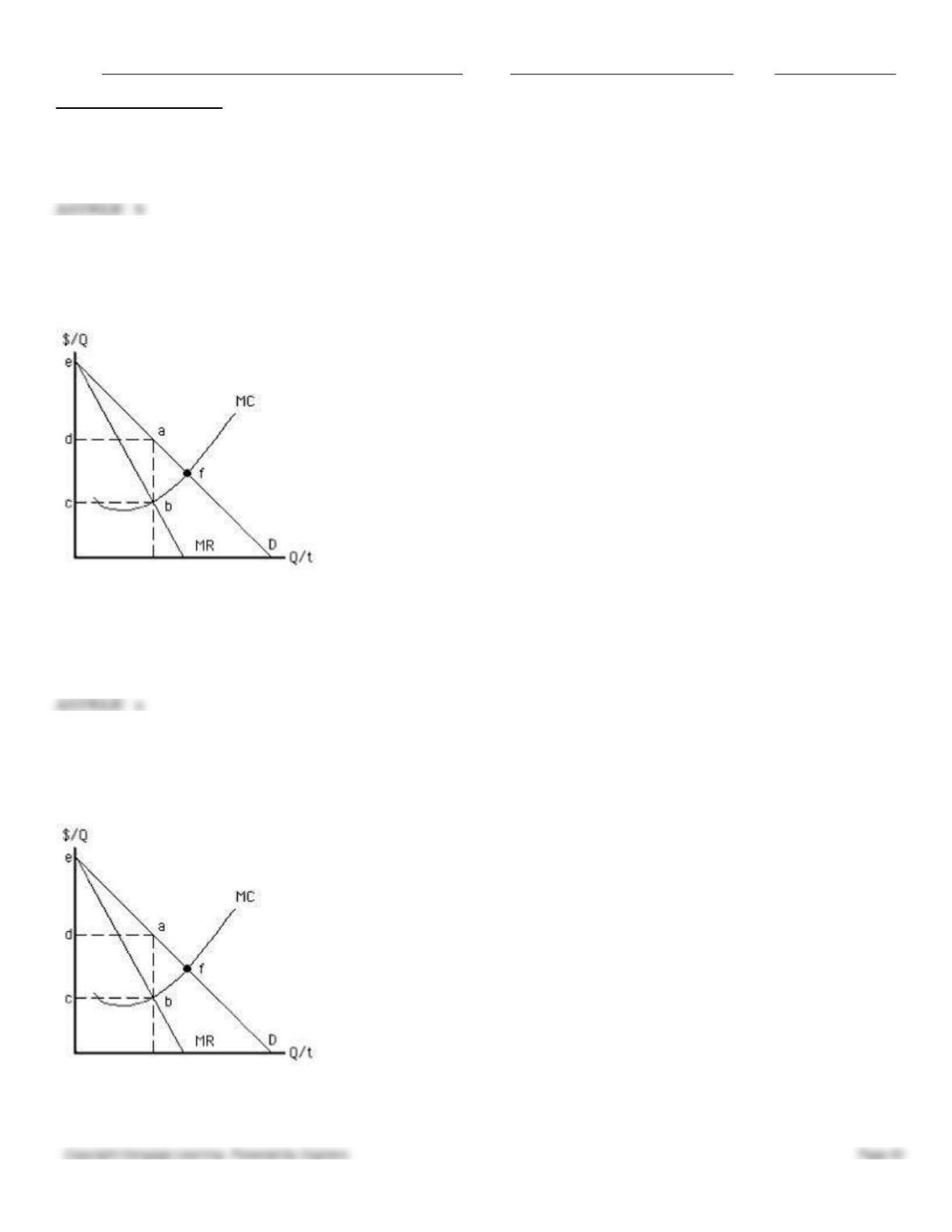

122. The figure given below depicts a monopoly market in the absence of price discrimination. Consumer surplus in this

market is represented by the area:

Figure 9.8

a.

eda.

b.

ecf.

c.

dacb.

d.

dafc.

e.

abf.

a

123. The figure below shows the cost and revenue curves for a monopolist. The deadweight loss arising under the

monopoly is represented by the area:

Figure 9.8

a.

ecf.

b.

eda.

c.

dabc.

Name:

Class:

Date:

Chapter 09: Monopoly

d.

dafc.

e.

abf.

e

124. Which of these is a similarity between a monopolist that does not practice price discrimination and a perfectly

competitive firm?

a.

The firms face the same amount of competition from new entrants into the market.

b.

The firms have an equal number of rivals.

c.

The firms face perfectly price elastic demand curves.

d.

Price equals marginal revenue at all output rates for both types of firms.

e.

Price equals average revenue at all output rates for both types of firms.

e

125. Perfectly competitive firms and monopolistic firms determine their respective profit-maximizing output levels where:

a.

price equals marginal cost.

b.

total revenue is maximized.

c.

average total cost is minimized.

d.

marginal cost equals marginal revenue.

e.

price is at the maximum possible level.

126. Empirical estimates indicate that the annual deadweight loss of monopoly in the United States:

a.

ranges from about 1 percent to 5 percent of national income.

b.

ranges from about 10 percent to 20 percent of national income.

c.

is approximately 10 percent of national income.

d.

is approximately $1 billion.

e.

is approximately $1 trillion.

a

127. The figure given below depicts the cost and revenue curves facing a profit-maximizing monopolist that does not

discriminate among its customers. Given the figure, which of the following is true?

Figure 9.9

Name:

Class:

Date:

Chapter 09: Monopoly

a.

An output of 50 units is allocatively efficient, but the monopolist is likely to produce 100 units.

b.

An output of 50 units is allocatively efficient, but the monopolist is likely to produce 75 units.

c.

An output of 75 units is allocatively efficient, but the monopolist is likely to produce 100 units.

d.

An output of 100 units is allocatively efficient, but the monopolist is likely to produce 50 units.

e.

An output of 100 units is allocatively efficient, but the monopolist is likely to produce 75 units.

128. The figure given below depicts the cost and demand conditions facing a profit-maximizing monopolist that does not

discriminate among its customers. The deadweight loss of monopoly equals _____.

Figure 9.9

a.

$5

b.

$250

c.

$125

d.

$500

e.

$10

129. The figure below shows the cost and revenue curves faced by a profit-maximizing monopolist. Which of the

following areas shown in the figure given below represents consumer surplus under monopoly?

Figure 9.10

a.

Area a

Name:

Class:

Date:

Chapter 09: Monopoly

b.

Area b

c.

Area c

d.

Area f

e.

Area e

130. The figure below shows the cost and revenue curves faced by a profit-maximizing monopolist. _____ on the figure

represents the deadweight loss of monopoly.

Figure 9.10

a.

Area a

b.

Area b

c.

Area c

d.

Area f

e.

Area e

131. If a perfectly competitive industry is monopolized, consumer surplus:

a.

can be expected to decrease.

b.

usually remains constant.

c.

becomes equal to producer surplus.

d.

becomes double of producer surplus.

e.

increases from zero to a high value.

132. The true deadweight loss created by a monopolist that does not practice discrimination is most likely to be less than

the loss indicated by the shaded area in the figure below, when:

Figure 9.11

Name:

Class:

Date:

Chapter 09: Monopoly

a.

the monopolist experiences diseconomies of scale.

b.

the monopolist charges lower prices to discourage competition.

c.

the monopolist engages in rent seeking.

d.

the monopolist advertises more to maintain its position.

e.

the monopolist faces diminishing marginal returns.

133. The actual deadweight loss from monopoly in the United States is likely to be greater than the calculated estimates

because some:

a.

monopolies experience strong economies of scale.

b.

monopolists spend resources to secure and maintain their monopoly.

c.

monopolists often keep price lower than their profit-maximizing level in order to increase barriers to entry.

d.

monopolists’ markets are contestable.

e.

monopolists’ prices and profits are regulated by the government.

134. The figure below shows the cost and revenue curves faced by a profit-maximizing monopolist. If the monopolist

engages in perfect price discrimination, its profit-maximizing output will be _____.

Figure 9.6

Name:

Class:

Date:

Chapter 09: Monopoly

a.

700 units

b.

810 units

c.

884 units

d.

976 units

e.

1,000 units

135. The figure below shows the cost and revenue curves faced by a profit-maximizing monopolist. If the monopolist

engages in perfect price discrimination, the price of the monopolist’s good will be:

Figure 9.6

a.

$120 for the 884th unit.

b.

$212 for the 884th unit.

c.

$120 for all units.

d.

$136 for all units.

e.

$104 for all units.

Name:

Class:

Date:

Chapter 09: Monopoly

a

136. The figure below shows the cost and revenue curves faced by a profit-maximizing monopolist. If the monopolist

engages in perfect price discrimination, the price of the monopolist’s good will:

Figure 9.6

a.

vary between $212 and $120.

b.

vary between $212 and $104.

c.

be $136 for all units.

d.

be $110 for all units.

e.

be $104 for all units.

a

137. Which of the following is true for a monopolist that engages in perfect price discrimination?

a.

Perfect price discrimination restricts the total output produced by the monopolist.

b.

Perfect price discrimination allows the monopolist to just break even and transfers the gain to consumers.

c.

Perfect price discrimination results in the maximization of consumer surplus.

d.

Perfect price discrimination creates a deadweight loss.

e.

Perfect price discrimination allows the monopolist to reap the entire gains from production.

e

138. The practice of charging different prices to different consumers for the same product is called:

a.

arbitration.

b.

unit pricing.

c.

price discrimination.

d.

predatory pricing.

e.

marginal cost pricing.

c

139. A monopolist practices price discrimination by:

Name:

Class:

Date:

Chapter 09: Monopoly

a.

charging different buyers different prices for different products.

b.

charging different buyers different prices for the same product.

c.

selling at a price below average total cost.

d.

selling at a price below marginal cost.

e.

selling at a price above marginal revenue.

140. A major fruit juice manufacturer fails in its attempt to engage in price discrimination between students and all other

consumers of fruit juice. Which of the following explanations is most likely to account for this failure?

a.

The students resold the juice to other consumers.

b.

The market for fruit juice was monopolistically competitive.

c.

The price elasticity of demand for fruit juice was different for each group.

d.

The cost of producing the fruit juice was extremely high.

e.

The students preferred to purchase juice from other small juice manufacturers.

a

141. For which of the following products would price discrimination be easiest?

a.

Orange juice

b.

Diamonds

c.

Compact disks

d.

Haircuts

e.

Gasoline

142. Which of the following is not a condition for price discrimination?

a.

A downward-sloping demand curve for products

b.

The presence of strong diseconomies of scale

c.

The presence of different groups of buyers with different price elasticity of demand

d.

The absence of a scope for reselling a product

e.

The presence of some amount of market power with a producer

143. A price-discriminating monopolist divides its customers into two segments based on price elasticity of demand. If it

sells its product for a price of $42 in the market segment where demand is relatively less price elastic, the price in the

market segment where demand is more price elastic will be:

a.

$42.

b.

greater than $42.

c.

less than $42.

d.

less than the marginal revenue in that market segment.

e.

equal to the marginal revenue in that market segment.

c

144. When a price-discriminating monopolist divides its customers into two market segments, the price in each segment is

determined by finding the level of output where that market’s:

Name:

Class:

Date:

Chapter 09: Monopoly

a.

average revenue equals average total cost.

b.

average revenue equals average variable cost.

c.

marginal revenue equals average total cost.

d.

marginal revenue equals marginal cost.

e.

marginal cost equals average total cost.

145. A monopolist that engages in perfect price discrimination:

a.

divides all buyers into two mutually exclusive groups.

b.

refuses to sell its output to consumers of rival brands.

c.

charges the same price for every unit sold.

d.

charges a different price for every unit sold.

e.

charges a high price to bulk consumers of its product.

146. Which of the following is observed when perfect price discrimination is practiced by a monopolist?

a.

Profit is lower than it would be without discrimination.

b.

Total revenue is lower than it would be without discrimination.

c.

Average revenue is less than average cost.

d.

Consumer surplus is zero.

e.

Profit is zero.

147. When a monopolist practices perfect price discrimination, _____.

a.

the equilibrium quantity traded in the market and the consumer surplus are the same as under perfect

competition

b.

the equilibrium quantity traded in the market is greater but the consumer surplus is the same as under perfect

competition

c.

the equilibrium quantity traded in the market and the consumer surplus are both lower than under perfect

competition

d.

the equilibrium quantity traded in the market is the same but consumer surplus is lower than under perfect

competition

e.

the equilibrium quantity traded in the market is lower but consumer surplus is the same as under perfect

competition

148. The figure below shows the cost and revenue curves faced by a monopolist. If the monopolist practices perfect price

discrimination, deadweight loss will be _____.

Figure 9.10

Name:

Class:

Date:

Chapter 09: Monopoly

a.

equal to area a

b.

equal to area b

c.

equal to area c + area a

d.

zero

e.

equal to area e

d

149. The figure below shows the cost and revenue curves faced by a monopolist. The area _____ represents monopoly

profit with perfect price discrimination.

Figure 9.12

a.

f

b.

c

c.

a + b + e

d.

g

e.

h + a

c

150. The figure below shows the cost and revenue curves faced by a monopolist. If this monopolist practices perfect price

discrimination, the consumer surplus is:

Figure 9.10

Name:

Class:

Date:

Chapter 09: Monopoly

a.

equal to area a + b + c.

b.

equal to area b + e.

c.

equal to area b.

d.

equal to zero.

e.

equal to area e.