Page 1

1.

Although fixed exchange rates are desirable for many reasons, nations that adopt fixed

exchange rates find that:

A)

fixed exchange rates are difficult to abandon once they become established.

B)

flexible exchange rates actually offer a nation more stability.

C)

the rate is often only successful for a few years before the peg is broken.

D)

intergovernmental agreements limit the fixed exchange rates to only a few

products.

2.

The average duration for a pegged exchange rate is about:

A)

5 years.

B)

10 years.

C)

2 years.

D)

It is indefinite.

3.

The sudden collapse of a fixed exchange rate system is known as:

A)

an exchange rate crisis.

B)

deflation.

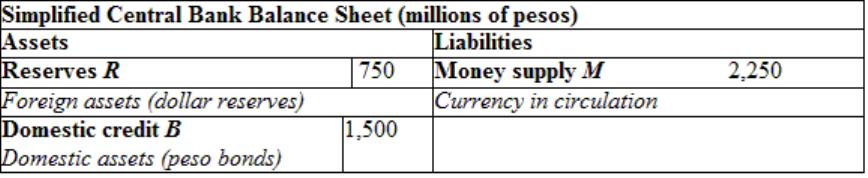

C)

an implosion.

D)

a financial cave-in.

4.

The depreciation in value of a nation’s currency hits a crisis point when the decline in

value exceeds:

A)

50% for all nations.

B)

10% for large nations and 20% for small nations.

C)

2% for all nations.

D)

the rise in nominal prices and wages.

5.

An exchange rate crisis causes all of the following, EXCEPT:

A)

a large and sudden depreciation of the currency.

B)

economic hardships.

C)

political turmoil.

D)

a sharp appreciation of the currency.

6.

An exchange rate crisis is defined as:

A)

a depreciation of 5% to 10% in a developing economy.

B)

a depreciation of 10% to 15% in an advanced country.

C)

a depreciation of 20% to 25% in an emerging economy.

D)

a depreciation of 10% to 15% in an advanced country and a depreciation of 20% to

25% in an emerging economy.

Page 2

7.

One economic cost of an exchange rate crisis is:

A)

a decrease in the rate of inflation.

B)

an increase in exports.

C)

a slowing in a country’s rate of economic growth.

D)

an increase in employment.

8.

As evident from EU nations pegging to the German mark (before currency union) and

nations pegging to the U.S. dollar:

A)

the mark was overvalued, while the dollar was undervalued.

B)

when currency crises occur, they are more severe in emerging markets, yet they

can affect both developing and emerging market economies.

C)

nations pegging their currencies to the mark had lower rates of interest, yet

domestic credit volume was lower in nations pegging to the dollar.

D)

currency crises are very uncommon, yet when they occur, the media often makes

too much of the issue in their reports.

9.

Which of the following is correct?

A)

Exchange rate crises typically impose larger costs on advanced countries than on

emerging market countries.

B)

Exchange rate crises typically impose larger costs on emerging market countries

than on advanced countries.

C)

Exchange rate crises typically impose the same costs on advanced countries and on

emerging market countries.

D)

Exchange rate crises typically do not impose any costs on advanced countries.

10.

The effect of an exchange crisis on large nations compared with small ones:

A)

is less severe, with a better recovery in a shorter period.

B)

is more severe, with a worse chance of full recovery in a shorter period.

C)

is about the same in terms of recovery but not in terms of unemployment.

D)

is more severe because the crisis affects interaction between a number of trading

partners.

11.

In emerging markets, the reductions in growth of GDP as a result of exchange rate

crises:

A)

is never very much.

B)

is not a problem because the IMF and World Bank make up the difference.

C)

is more than 50% per year.

D)

is about 10% of total GDP.

Page 3

12.

A nation experiencing financial difficulties often has simultaneous crises. Which of the

following is NOT typically concurrent for such nations?

A)

a banking crisis

B)

a default crisis

C)

an exchange rate crisis

D)

a climate crisis

13.

Which of the following occurs during a banking crisis?

A)

Banks close or declare bankruptcy.

B)

A government is unable to pay principal or interest on debt owed to banks.

C)

No one wants to borrow from banks.

D)

A country’s central bank runs out of reserve currencies.

14.

Which of the following occurs during a default crisis?

A)

Banks close or declare bankruptcy.

B)

A government is unable to pay principal or interest on debt owed to banks.

C)

No one wants to borrow from banks.

D)

A country’s central bank runs out of reserve currencies.

15.

The likelihood of an exchange rate crisis is more than ___ times higher during a default

crisis.

A)

2

B)

3

C)

5

D)

10

16.

Why might a default crisis be associated with an exchange rate crisis?

A)

A large depreciation causes a sudden decrease in the local currency value of

international debts denominated in other currencies.

B)

A government is unable to pay principal or interest on debt owed to banks.

C)

A large depreciation causes a sudden increase in the local currency value of

international debts denominated in other currencies.

D)

Banks close or declare bankruptcy.

17.

Typically, an exchange rate crisis can be caused by:

A)

a government default on debt.

B)

a banking crisis, triggered by adverse shocks.

C)

sudden infusion of credit into the economy.

D)

a government default on debt and a banking crisis, triggered by adverse shocks.

Page 4

18.

Which of the following is correct?

A)

The likelihood of an exchange rate crisis increases if a country is having a banking

crisis.

B)

The likelihood of an exchange rate crisis decreases if a country is having a banking

and default crisis.

C)

There is no relationship between an exchange rate crisis and banking or default

crises.

D)

When a banking or default crisis occurs, countries typically are forced to appreciate

their currencies.

19.

The reason for the concurrence of exchange rate crises and other financial disruptions

centers on:

A)

the inherent instability of most banks in low-income nations.

B)

the tendency of most elected officials to be susceptible to influence and corruption.

C)

the fact that changes in exchange rates can raise debt burdens (denominated in

other currencies) to intolerable levels.

D)

the tendency of the current administration to react by nationalizing banks and

implementing capital controls.

20.

A banking crisis often threatens a fixed exchange rate (or peg). Why?

A)

Banks have to provide funds to maintain the fixed exchange rate.

B)

The central bank may have to bail out insolvent banks by inflating the currency,

which could cause a loss of reserves.

C)

The central bank has to close relationships with foreign banks, and there is no way

to implement the fixed exchange rate system.

D)

The banking crisis means that domestic banks hold onto foreign currency reserves

rather than exchanging them with the central bank.

21.

Financial crises tend to happen in pairs or triplets because:

A)

a democracy is good in some ways but puts too much financial power in the control

of the people.

B)

when financial fundamentals such as debt, real GDP, and fiscal discipline are

weak, then trade, investment, consumers, business firms, and the financial sector

are affected in a number of ways.

C)

for there to be a currency crisis, consumer debt must be rising.

D)

the central bank usually has everything under control, so crises are generally the

fault of greedy firms.

Page 5

22.

To maintain the peg, a nation must keep its money supply constant, which it does by:

A)

buying and selling foreign reserves and domestic assets for its own currency.

B)

requiring all banks to back deposits 100%.

C)

backing the currency by foreign reserves 100%.

D)

selling only foreign reserves for its own currency.

23.

When maintaining a peg, if the central bank runs out of foreign currency reserves, then:

A)

it can always print more of the domestic currency.

B)

it can back the money supply by purchasing domestic assets.

C)

it can sell its own currency and purchase foreign currency reserves.

D)

it must allow the domestic currency to float.

24.

When analyzing problems in maintaining a fixed exchange rate system, simplifying

assumptions must be made. Which of the following is NOT a simplifying assumption?

A)

The domestic government issues no bonds.

B)

The price level is stable and purchasing power parity (PPP) holds.

C)

Output is exogenous.

D)

Everyone believes the peg will hold, so there is uncovered interest parity (UIP).

25.

When a nation is maintaining an exchange rate peg, its money supply is typically

backed by:

A)

gold.

B)

nothing.

C)

domestic bonds and foreign exchange assets purchased with the national currency.

D)

domestic credit only.

26.

In the home economy, when “money” is a liability of the government, the supply of

money is equal to:

A)

gold reserves on a one-to-one basis.

B)

the physical quantity of currency and coins in circulation.

C)

the assets in a nation’s account at the IMF.

D)

the total of bonds (domestic credit) plus foreign currency and gold reserves held by

the central bank.

27.

What results in changes in the domestic money supply?

A)

changes in the central bank’s holding of domestic credit only

B)

changes in the central bank’s holding of foreign reserves only

C)

some combination of changes in the central bank’s holdings of domestic credit or

foreign reserves

D)

changes in the nation’s stock of gold

Page 6

28.

Which of the following is counted in the domestic assets of a central bank?

A)

money that the central bank issues to pay for purchases of domestic bonds

B)

domestic bonds that it purchases with money that it issues

C)

reserve currencies that it purchases with money that it issues

D)

money that it issues to purchase reserve currencies

29.

A balance sheet for the central bank shows assets of _____ and liabilities of ______.

A)

gold and silver; foreign obligations

B)

reserves (foreign currency and foreign bonds); domestic currency (money supply)

C)

private individuals; public entities

D)

large money center banks; corporate borrowers

30.

Saudi Arabia pegs its currency (the riyal, or SAR) to the U.S. dollar. Currently, the

exchange rate is SAR3.75 = $US1. Suppose that the Saudi Arabian money multiplier is

1. By how much will the Saudi Arabian money supply change when the Saudi central

bank buys $1 million of additional reserves?

A)

+SAR 1 million

B)

–SAR 1 million

C)

+SAR 3.75 million

D)

–SAR 3.75 million

31.

Saudi Arabia pegs its currency (the riyal, or SAR) to the U.S. dollar. Currently, the

exchange rate is SAR3.75 = $US1. Suppose that the Saudi Arabian money multiplier is

1. By how much will the Saudi Arabian money supply change when the Saudi central

bank makes loans of SAR 1 million?

A)

+SAR 1 million

B)

–SAR 1 million

C)

+SAR 3.75 million

D)

–SAR 3.75 million

32.

Saudi Arabia pegs its currency (the riyal, or SAR) to the U.S. dollar. Currently, the

exchange rate is SAR3.75 = $US1. Suppose that the Saudi Arabian money multiplier is

1. Which of the following is NOT included in the assets of the Saudi Arabian central

bank?

A)

reserves

B)

domestic credit

C)

the money supply

D)

domestic credit and the money supply

Page 7

33.

Saudi Arabia pegs its currency (the riyal, or SAR) to the U.S. dollar. Currently, the

exchange rate is SAR3.75 = $US1. Suppose that the Saudi Arabian money multiplier is

1. How does the Saudi Arabian central bank maintain the pegged exchange rate of

SAR3.75 = $US1?

A)

It sells dollars (for Saudi riyals) in foreign exchange markets whenever the

SAR–$US rate falls below SAR3.75 = $US1.

B)

It buys dollars (with Saudi riyals) in foreign exchange markets whenever the

SAR–$US rate rises above SAR3.75 = $US1.

C)

It sells Saudi riyals (for dollars) in foreign exchange markets whenever the

SAR–/$US rate rises above SAR3.75 = $US1.

D)

It buys Saudi riyals (with dollars) in foreign exchange markets whenever the

SAR–$US rate rises above SAR3.75 = $US1.

34.

If the central bank holds no foreign currency reserves, the nation’s exchange rate is:

A)

fixed.

B)

pegged.

C)

under the control of the IMF.

D)

floating.

35.

(Table: Mexico’s Central Bank Balance Sheet) If the country sells 325 million pesos of

foreign assets and issues domestic credit worth 425 million pesos, what will be the

money supply in the economy?

A)

750 million pesos

B)

1,500 million pesos

C)

2,350 million pesos

D)

It will be unchanged.

Page 8

36.

(Table: Mexico’s Central Bank Balance Sheet) If the country sells 325 million pesos of

foreign assets and reduces domestic credit by 425 million pesos, then:

A)

the reserves will be 450 million pesos.

B)

the domestic assets will be 1,125 million pesos.

C)

the domestic assets will be 1,075 million pesos.

D)

the reserves will be 1,075 million pesos.

37.

(Table: Mexico’s Central Bank Balance Sheet) To maintain a fixed exchange rate, which

of the following will Mexico do?

A)

always buy more government bonds

B)

always sell more government bonds

C)

buy and sell reserves

D)

print more money

38.

What must a nation’s central bank do to maintain a fixed exchange rate?

A)

achieve a balanced budget

B)

keep the level of foreign reserves above zero so that it can prevent a fall in value of

its currency

C)

keep the level of foreign reserves at zero

D)

hold only foreign government bonds to back the currency 100%

39.

A drawback to using changes in domestic credit to adjust the domestic money supply to

maintain a peg:

A)

is problems in emerging market economies as a result of bond market instability.

B)

is the lack of expertise in financial matters in the central banks of emerging

markets.

C)

is the requirement that currencies flip flop from fixed to floating.

D)

is that nations are ignoring a potentially more effective source of currency

adjustment.

Page 9

40.

Which method would the central bank NOT use to keep the exchange value of its

currency fixed?

A)

It would purchase its own currency for foreign reserves when the domestic credit

expanded.

B)

It would ensure that the domestic money supply remained constant.

C)

It would sell its own currency for foreign reserves when domestic credit contracted.

D)

It would ensure that the domestic money supply increased to maintain uncovered

interest and PPP.

41.

Which of the following methods would the central bank NOT use to keep the exchange

value of its currency fixed?

A)

It would purchase its own currency for foreign reserves when the domestic credit

expanded.

B)

It would sell its own currency for foreign reserves when domestic credit contracted.

C)

It would ensure that the domestic money supply stayed constant to maintain

uncovered interest and PPP.

D)

It would ensure that the domestic money supply increased to maintain PPP.

42.

Aruba pegs its currency (the Aruban florin) to the U.S. dollar at a rate of Af 2 = $US1.

Suppose that the actual exchange rate is equal to this pegged rate. Now suppose that the

Aruban central bank buys dollars. Which of the following describes the effect of this

dollar purchase on Aruba’s exchange rate?

A)

upward pressure on the exchange rate (depreciation of florin)

B)

downward pressure on the exchange rate (appreciation of florin)

C)

no effect on the exchange rate

D)

Not enough information is provided to answer.

43.

Aruba pegs its currency (the Aruban florin) to the U.S. dollar at a rate of Af 2 = $US1.

Suppose that the actual exchange rate is equal to this pegged rate. Now suppose that the

Aruban central bank buys dollars. Which of the following describes what will happen to

Aruba’s exchange rate?

A)

The exchange rate will appreciate.

B)

The exchange rate will depreciate.

C)

The exchange rate will not change.

D)

Not enough information is provided to answer.

Page 10

44.

Aruba pegs its currency (the Aruban florin) to the U.S. dollar at a rate of Af 2 = $US1.

Suppose that the actual exchange rate is equal to this pegged rate. Which of the

following best describes the effect on Aruba’s money supply from purchasing dollars?

A)

The money supply will increase.

B)

The money supply will decrease.

C)

The money supply will not change.

D)

The money supply will not change as the exchange rate appreciates.

45.

Aruba pegs its currency (the Aruban florin) to the U.S. dollar at a rate of Af 2 = $US1.

Suppose that the actual exchange rate is equal to this pegged rate. Which of the

following best describes the effect on Aruba’s interest rates from purchasing dollars?

A)

Interest rates will rise.

B)

Interest rates will fall.

C)

Interest rates will not change.

D)

Interest rates will rise as the exchange rate depreciates.

46.

Aruba pegs its currency (the Aruban florin) to the U.S. dollar at a rate of Af 2 = $US1.

Suppose that the actual exchange rate is equal to this pegged rate. Suppose that Aruba’s

money supply is Af 20 billion and Aruba’s central bank holds $5 billion of dollar

reserves and Af 10 billion of domestic bonds. What is the backing ratio for Aruban

florins?

A)

10.5%

B)

21%

C)

50%

D)

89.5%

47.

Aruba pegs its currency (the Aruban florin) to the U.S. dollar at a rate of Af 2 = $US1.

Suppose that the actual exchange rate is equal to this pegged rate. Suppose that Aruba’s

money supply is Af 20 billion and Aruba’s central bank holds $5 billion of dollar

reserves and Af 10 billion of domestic bonds. What will happen to Aruba’s backing ratio

if its central bank sells $2.5 billion of U.S. dollars to Aruban citizens?

A)

It will not change.

B)

It will fall to 33%.

C)

It will fall to 2.6%.

D)

It will fall to 81%.

Page 11

48.

El Salvador has dollarized; that is, it uses the U.S. dollar as its currency. What is the

backing ratio for El Salvador’s currency?

A)

0%

B)

25%

C)

75%

D)

100%

49.

To have adequate protection to cover a depreciation, the central bank must keep its

foreign currency reserves at the level at which:

A)

they are growing at the same rate as GDP.

B)

they are equal to the demand for money minus the amount of domestic credit (held

by the central bank).

C)

they are greater than zero.

D)

they are worth three months of import protection.

50.

The degree of danger of breaking the peg focuses on:

A)

how problematic defaults are for the domestic banking system.

B)

the volatility of interest rates.

C)

the ratio of domestic bonds to foreign currency reserves in backing the domestic

money supply.

D)

how difficult it is for the nation to maintain a current account surplus.

Page 12

51.

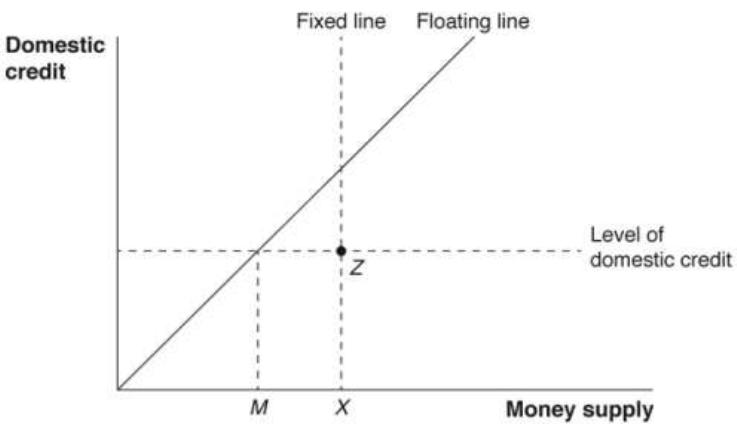

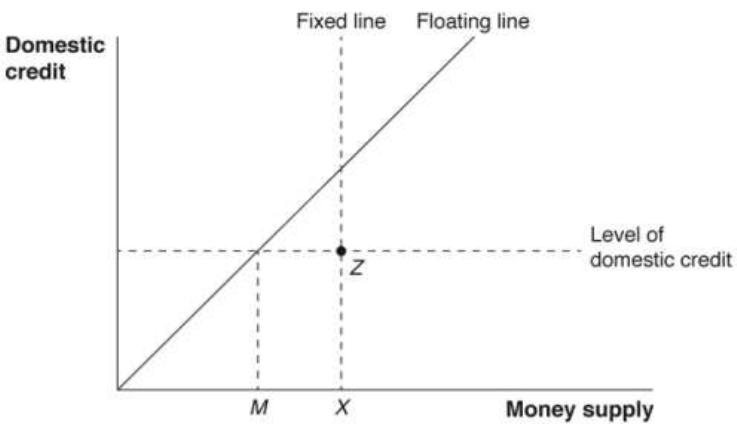

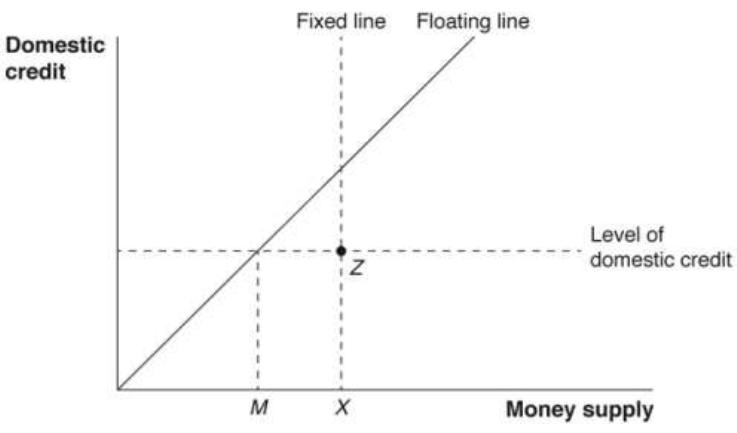

(Figure: Central Bank Balance Sheet) All points on the floating line are so named

because:

A)

at every point on the line, the supply of money is equal to bond holdings so that

reserves are equal to zero.

B)

at every point above the line, the exchange rate floats.

C)

at every point below the line, the exchange rate is backed 100% by reserves.

D)

exchange rates can only float if the economy is “on” the floating line.

Page 13

52.

(Figure: Central Bank Balance Sheet) All points on the fixed line (XZ) are so named

because:

A)

at every point on the line, the supply of money is equal to bond holdings so that

reserves are equal to zero.

B)

at every point on the line, the supply of money is greater than domestic bond

holdings so that reserves are greater than zero.

C)

at every point to the right of the line, the money supply is backed 100% by

reserves.

D)

exchange rates will float unless the economy is “on” the fixed line.

Page 14

53.

(Figure: Central Bank Balance Sheet) When an economy with a pegged exchange rate

operates with the money supply backed 100% by reserves, it is at point __________ on

the diagram, and the situation is known as __________.

A)

Z; complete sterilization

B)

B; modified fixed/float

C)

M; freely floating system

D)

X; currency board system

54.

When a country adopts a currency board system:

A)

it no longer needs to hold any reserves.

B)

its reserves equal 100% of its money supply.

C)

it can create money by lending to domestic borrowers.

D)

its reserves must equal 50% of its money supply.

55.

To maintain the peg, a nation must keep its circulating money supply constant. What

factor(s) (in addition to its own actions) might result in a change in the money supply?

A)

a change in the demand for money produced by an output shock or a change in

foreign rates of interest

B)

an increase in the trade gap

C)

the issuance of new government bonds by the nation’s government

D)

a crackdown on money laundering activities by multinational corporations

Page 15

56.

If the price level is fixed, the demand for money depends on changes in which of the

following?

A)

the exchange rate with trading partners

B)

government purchases of domestic bonds

C)

GDP and/or the domestic rate of interest

D)

the total value of assets held by the central bank

57.

With a credible peg, whenever there is a rise in the foreign interest rate:

A)

there is a drop in the domestic interest rate.

B)

the exchange rate changes.

C)

there is an equal rise in the domestic interest rate.

D)

there will be no change in the domestic interest rate.

58.

When output falls or the foreign rate of interest rises, what must the central bank do and

why?

A)

It must sell foreign currency reserves for its own currency to raise rates of interest

and decrease the supply of money.

B)

It must buy foreign currency reserves with its own currency to lower rates of

interest and increase the supply of money.

C)

It must resist the temptation to do something immediately and let the situation

work itself out.

D)

It must ask the domestic government to issue more bonds to raise domestic rates of

interest.

59.

Consider an economy with a fixed exchange rate and money supply equal to 2 billion

pesos. The country has 1 billion in reserves and 1 billion in domestic credit. If there is a

sudden decline in the demand for money, then:

A)

the country needs to reduce its reserves to maintain the exchange rate.

B)

the country needs to increase its reserves to maintain the exchange rate.

C)

the country will face rising interest rates and, thus, a sharp appreciation of the peso.

D)

the country will see a sharp increase in the demand for loans.

60.

Assume the money supply is backed by bonds and reserves, and the exchange rate is

pegged. If the domestic demand for money falls, what happens to the level of bonds and

reserves?

A)

The level of bonds and reserves both rise.

B)

The level of bonds stays the same, while the level of reserves falls.

C)

The level of bonds rises, while the level of reserves falls.

D)

The level of bonds falls and the level of reserves rises.

Page 16

61.

Assume the money supply is backed by bonds and reserves, and the exchange rate is

pegged. If the demand for money rises, how might the central bank maintain the peg?

A)

by selling back domestic bonds and foreign currency reserves

B)

by selling domestic bonds equal to the increase in demand

C)

by purchasing reserves equal to the increase in demand

D)

by selling reserves equal to the increase in demand

62.

Consider an economy with a fixed exchange rate and money supply equal to 2 billion

pesos. The country has 1 billion in reserves and 1 billion in domestic credit. If the output

in the country were to increase by 5%, then:

A)

the money demand would increase by 10%.

B)

the central bank would have to increase reserves by 5%.

C)

the central bank would have to decrease reserves by 5%.

D)

the central bank would have to decrease domestic credit.

63.

Consider an economy with a fixed exchange rate and money supply equal to 2 billion

pesos. The country has 1 billion in reserves and 1 billion in domestic credit. If as a result

of some exogenous events, foreign interest rate increases, then the central bank in the

home country:

A)

will have to decrease the reserves to maintain the peg.

B)

will have to decrease the domestic assets.

C)

will have to increase the reserves to maintain the peg.

D)

will do nothing.

64.

If domestic credit is constant, then any change in the demand for money will result in:

A)

a change in foreign credit.

B)

a change in the rate of interest.

C)

an inverse change in the price level.

D)

an equal change in foreign currency reserves.

65.

If domestic credit is constant and the money supply changes, then:

A)

reserves will remain constant.

B)

foreign credit will remain constant.

C)

reserves will change by a larger percentage than the change in the money supply.

D)

foreign interest rates will begin to increase.

Page 17

66.

A ratio indicating how safe the peg is from breaking is calculated by _______ and is

called ________.

A)

foreign reserves as a percent of GDP; the safety margin

B)

foreign reserves as a percent of the total money supply; the backing ratio

C)

money demand as a percent of money supply; the financial adequacy quotient

D)

foreign reserves as a percent of domestic credit; the marginal propensity to break

67.

An economy is better able to withstand a shock to the money demand if:

A)

the backing ratio is lower.

B)

the country holds more domestic assets.

C)

the backing ratio is higher.

D)

the country holds fewer reserves.

68.

When the backing ratio is higher, the peg is:

A)

less stable.

B)

higher.

C)

safer.

D)

less credible.

69.

Whenever a nation opts to back its fixed exchange rate 100% with foreign currency

reserves, it is known as:

A)

a floating rate system.

B)

a currency peg.

C)

a currency board.

D)

a full concentration ratio.

70.

When the central bank adopts a currency board, it is considered ______, because a

shock to money demand _______.

A)

a hard peg; can be covered at any level without a change in domestic credit

B)

a soft peg; can be absorbed by a change in domestic credit

C)

a reversion to floating rates; is impossible

D)

the reinstatement of a gold standard; cannot be covered any other way

71.

Which of the following is NOT likely to cause a money demand shock under a fixed

exchange rate system?

A)

a decline in foreign interest rates

B)

a sudden decline in domestic output

C)

a sudden increase in domestic output

D)

a change in marginal tax rate in the foreign country

Page 18

72.

Special situations in emerging markets and developing economies, such as volatile

output and an export dependent economy, usually mean:

A)

the prudent level of reserves is much higher than for higher-income nations.

B)

there is no way they are able to maintain an exchange rate peg.

C)

pegging exchange rates is even more important.

D)

pegging exchange rates is much easier because the economies are smaller.

73.

What is a problem in emerging markets that affects a nation’s ability to peg its currency?

A)

The low level of GDP means the demand for money is always small.

B)

The high level of GDP means the demand for money is always large.

C)

As the nation develops, the ratio of the demand for money to GDP rises.

D)

Because of the volatility of GDP, the demand for money is volatile and the nation

must hold higher levels of reserves to peg.

74.

Uncovered interest parity may actually result in domestic interest rates being ____ than

foreign rates because of investors’ perceived risk of holding assets based in the domestic

currency.

A)

lower

B)

more unstable

C)

higher

D)

more stable

75.

The risk premium is the difference between foreign and domestic rates of interest under

parity. This premium has three distinct parts. Which of the following is NOT a factor in

the risk premium?

A)

the currency premium

B)

the country premium

C)

the default risk premium

D)

the floating risk premium

76.

Emerging markets and developing economies may have to raise domestic rates of

interest suddenly if:

A)

the supply of money unexpectedly drops.

B)

the IMF calls in loans with no warning.

C)

the risk premium for its currency rises dramatically.

D)

domestic investors wish to repatriate their profits earned overseas.

Page 19

77.

If a nation’s interest rate on foreign currency deposits is higher inside than outside the

nation, which of the following is the cause?

A)

a fall in the domestic money supply

B)

a country premium, meaning investors are concerned about defaults or capital

controls

C)

a currency premium

D)

an exchange rate premium

78.

When other emerging market nations experience an exchange rate crisis, it affects

healthy emerging market economies (raises risk premiums) because of investor worry.

This phenomenon is known as:

A)

emerging market dysfunction.

B)

the law of like outcomes.

C)

experiential judgment.

D)

contagion.

79.

To what does global contagion refer?

A)

an equalization of world interest rates

B)

elimination of risk premiums between countries

C)

adverse changes in market sentiment based on events in faraway places

D)

switching to fixed exchange rates by emerging market economies

80.

An example in the text of Argentina’s convertibility plan during 1993–94 indicated that

because of a growing economy, the central bank expanded the supply of money to

maintain its U.S. dollar peg by:

A)

acquiring foreign reserves.

B)

buying domestic bonds.

C)

issuing new government liabilities.

D)

selling gold.

81.

Because of a rise in its risk premium and subsequent rise in interest rates, Argentina

experienced a fall in ____, which resulted in a decline in ____.

A)

investor confidence; GDP

B)

GDP; the supply of money

C)

the demand for money; the backing ratio

D)

the supply of money; domestic credit

Page 20

82.

Argentina could reduce the supply of money and help out ailing banks without

abandoning its peg because:

A)

Argentina got long-overdue help from the IMF.

B)

Argentina had adequate foreign currency reserves to be able to draw them down.

C)

Argentina’s central bank financed the help by buying more Argentinian bonds.

D)

Argentina temporarily suspended convertibility but eventually restored it.

83.

Investors in emerging markets often require ______ added to their return because they

are concerned about defaults and exchange rate volatility.

A)

collateral deposits

B)

credit swap default insurance

C)

a risk premium

D)

compensation for their executives

84.

Part of the default risk in developing nations is investor fear of all of the following,

EXCEPT:

A)

bank failures.

B)

election fraud.

C)

surprise taxation.

D)

capital controls.

85.

What is the likely cause of an interest rate spread for similar assets denominated in the

same currency?

A)

There is doubt that the currency’s value will hold.

B)

It is due to the country risk where the assets are originated.

C)

It depends on the geographic difference between borrowers and lenders.

D)

It is because in some markets, the middlemen “take” more of a cut.

86.

How was Argentina affected by the Tequila Crisis in Mexico in 1994?

A)

The price of tequila rose to levels that made imports of the beverage drop.

B)

Because of Mexico’s currency crisis and the failure of its peg, Argentina was

forced to contract its money supply and raise interest rates to restore investor

confidence.

C)

Argentina had to lower its interest rates to stimulate its economy.

D)

Argentina no longer could maintain its dollar peg.

Page 21

87.

If the central bank desires to purchase additional domestic bonds to stimulate the

economy, then to maintain the peg, what must it do?

A)

Decrease domestic spending.

B)

Sell enough reserves to keep the interest rate unchanged.

C)

Convince the public and investors that the peg is credible.

D)

Immediately lower domestic rates of interest.

88.

When the central bank offsets a fall in interest rates with the sale of foreign currency

reserves, the action is called:

A)

an offsetting movement.

B)

a foreign reserve counteraction.

C)

a central bank inside-out operation.

D)

a nonsterilized intervention.

89.

A shock to domestic credit, whereby the holding of domestic bonds decreases, would

result in:

A)

a rise in the backing ratio and the need for the central bank to purchase domestic

bonds.

B)

a fall in the backing ratio and the need for the central bank to sell domestic bonds.

C)

a fall in the backing ratio and the need for the central bank to purchase foreign

currency reserves.

D)

a rise in the backing ratio and the need for the central bank to purchase foreign

currency reserves.

90.

When the central bank engages in sterilization of reserves, it is:

A)

buying reserves to offset the purchase of government bonds.

B)

selling reserves to offset the sale of government bonds.

C)

selling reserves to offset the purchase of government bonds.

D)

printing more money.

91.

An expansion of the domestic money supply can be offset by the sale of foreign

reserves. This technique is called:

A)

repatriation.

B)

revaluation.

C)

sterilization.

D)

reversion.

Page 22

92.

In the event a nation adopts a currency board system to peg its exchange rate:

A)

sterilization occurs more often.

B)

sterilization is impossible.

C)

sterilization means all traders have access to currency reserves.

D)

the nation will have to abandon the system whenever the central bank wants to take

a holiday.

93.

Although the argument is weak, sterilization under a pegged system could benefit the

economy by:

A)

replacing outstanding debt (denominated in the domestic currency) with currency,

thus reducing privately held debt.

B)

reducing interest rates and stimulating the economy.

C)

holding down the level of government borrowing.

D)

providing funds for worker training and technology upgrades.

94.

A danger to the peg is a situation in which the central bank lends to insolvent private

financial institutions to bail them out of crises. Why might this cause a problem?

A)

The private financial institutions are often corrupt and should not be bailed out.

B)

Foreign investors are helped and domestic investors harmed.

C)

It requires a drawdown of foreign reserves to maintain the peg, lowering the

backing ratio.

D)

The central bank is assuming more than its share of political power, which can

cause problems down the road.

95.

Whenever the central bank lends to solvent but illiquid private financial institutions, it

does not endanger the peg. Why not?

A)

The money demand and supply increase together, so interest rates are not affected,

and the purchase of new domestic credit, when repaid, will restore the backing

ratio.

B)

The central bank finances the lending by selling reserves and the backing ratio is

lower.

C)

Private illiquid banks could borrow internationally, if needed, to repay their loans.

D)

The peg is guaranteed by the administration, which stands ready to support it by

selling reserves.

Page 23

96.

When there is a banking crisis under a peg, the monetary authority may be tempted to

bail out the banks. Why is this risky?

A)

Banks are the least important entity in the financial sector, and attention should be

paid to manufacturing, which is more important.

B)

Banks are critical to the success of the economy, and when they are in bad shape, it

is best to allow the weaker banks to fail and support the stronger ones.

C)

The central bank would have to sell reserves to maintain the peg, and they could

fall to an unsafe level.

D)

The monetary authority would be forced to buy reserves in exchange for domestic

currency—so there would be plenty of money in circulation.

97.

In emerging markets, a banking crisis threatens the peg when a bailout occurs because:

A)

the central bank will act too cautiously.

B)

the central bank will bail out other financial firms as well.

C)

the central bank cannot then lend to other solvent banks.

D)

fear of unsafe banks might encourage depositors to convert funds into foreign

currency deposits offshore.

98.

Argentina’s experience in defending its peg after 1994 resulted in all of the following,

EXCEPT:

A)

an increase in the nominal rate of interest as the risk premium rose because of the

Tequila Crisis.

B)

a bailout of domestic banks damaged by excessive defaults.

C)

domestic investors selling pesos and purchasing assets denominated in U.S. dollars.

D)

a significant decrease in the nominal rate of interest as the risk premium rose.

99.

How did the IMF step in to help Argentina in 1994?

A)

The IMF required it to immediately let its currency float.

B)

The IMF required it to repay all past-due loans as a condition for new lending.

C)

The IMF extended emergency loans to help it restore its backing ratio.

D)

The IMF required it to immediately let its currency float and to repay all past-due

loans as a condition for new lending.

100.

How did the Tequila Crisis eventually turn out?

A)

Argentina defaulted in May 1997, and its economy has not recovered.

B)

Argentina’s central bank reduced its holding of domestic credit to zero and

achieved a 100% backing ratio.

C)

Argentina allowed its currency to float.

D)

Argentina increased exports enough so that no lending was needed.

Page 24

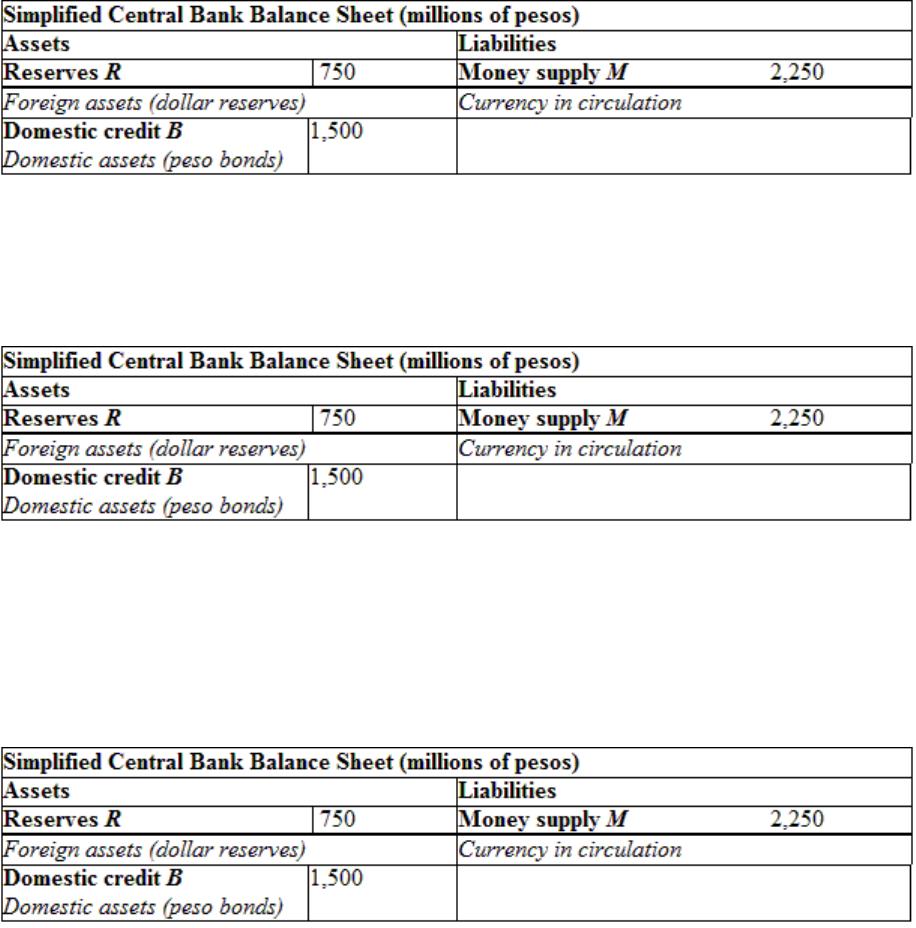

101.

(Table: Central Bank Balance Sheet) In the balance sheet provided, if the central bank

did not issue debt (domestic and foreign), then:

A)

it would have to reduce currency reserves by 375.

B)

it would increase currency reserves by 450.

C)

it would increase domestic assets by 450.

D)

it would have to reduce currency reserves by 450.

102.

(Table: Central Bank Balance Sheet) Using the balance sheet provided, if the central

bank issues 100 million more in foreign debt, then:

A)

the backing ratio would be equal to 95%.

B)

the backing ratio would be equal to 105%.

C)

there is no change in the backing ratio.

D)

the backing ratio would decrease to 50%.

Page 25

103.

(Table: Central Bank Balance Sheet) From the information given, what can we can

determine the backing ratio to be?

A)

50%

B)

95%

C)

45%

D)

5.2%

104.

The name for borrowing by the central bank to fund the purchase of foreign currency

reserves:

A)

is sterilization bonds.

B)

is official government debt.

C)

is foreign debt liabilities.

D)

is municipal bonds.

105.

How can a central bank change the composition of the money supply and increase the

backing ratio?

A)

It can confiscate any foreign currency held by private citizens.

B)

It can borrow from the public and investing in foreign currency assets.

C)

It can bail out insolvent banks.

D)

It can expand the money supply.

106.

The instruments with which central banks borrow reserves to increase the backing ratio

to more than 100% are known as:

A)

zero coupon bonds.

B)

sterilization bonds.

C)

repurchase agreements.

D)

government-guaranteed bonds.

Page 26

107.

A phenomenon that has perplexed many is that emerging market economies have sought

to ____ their foreign currency reserves, thus _____ the backing ratio to _____.

A)

decrease; raising; more than 50%

B)

increase; lowering; less than $15 billion

C)

get rid of; lowering; less than $30 billion

D)

increase; raising; more than 100%

108.

From 2003 to 2009, the backing ratio for the Chinese economy rose to more than 100%.

How did this happen?

A)

China’s monetary authority printed new money and sold it for foreign reserves.

B)

The export revenues were piling up, and China held them rather than spent them.

C)

China’s monetary authority sold large amounts of sterilization bonds, even as they

increased the supply of money.

D)

China reverted to a gold standard.

109.

Countries accumulate foreign currency reserves for all of the following reasons,

EXCEPT:

A)

to achieve a higher backing ratio.

B)

to safeguard against future shortfalls in foreign capital.

C)

to safeguard against a domestic banking crisis.

D)

to improve the stature of the country in the WTO.

110.

Which of the following is the most likely use of foreign currency reserves?

A)

investing in advanced countries

B)

investing in domestic infrastructure projects

C)

creating economic development funds for poor economies

D)

using them for manipulating domestic fiscal policy

111.

Low-income nations may be considering the cost of holding excess reserves as an

insurance premium against a future currency crisis. Economists have commented that

holding:

A)

excess reserves is necessary and prudent.

B)

reserves is unnecessary because the economy can always switch to floating rates.

C)

excess reserves to such an extent is much too costly for poor countries.

D)

excess reserves makes little difference when looking at the entire economy.

Page 27

112.

Whenever a nation has experienced a major banking crisis, the central bank may choose

to maintain a backing ratio of more than 100% because of a fear of:

A)

unemployment.

B)

a panic leading to capital flight.

C)

accounting irregularities.

D)

expropriation through excessive taxation.

113.

Paul Krugman has analyzed fixed currency pegs and the likely cause for them to break.

His model is one in which the central bank is under political control, which results in:

A)

fiscal dominance by the elected government whereby the central bank must print

money to fund government deficits.

B)

authority of the central bank to set rules for proper monetary management.

C)

the establishment of a currency board to manage the pegged exchange rate.

D)

the ability to control the money supply and interest rates to maintain the peg.

114.

Nations that depend on money creation from the central bank because they cannot

borrow to fund deficits are in a situation that economists call:

A)

fiscal dominance.

B)

fiscal inadequacy.

C)

monetary insufficiency.

D)

fiscal insufficiency.

115.

Once a nation “runs out” of reserves to back the currency, the peg cannot be maintained

because:

A)

the supply of money grows uncontrollably at the same rate that the central bank

monetizes deficits.

B)

the central bank cannot raise or lower the supply of money.

C)

the IMF will refuse to lend reserves to such a nation.

D)

the nation’s currency is overvalued so that its exports diminish.

116.

With pegged exchange rates, in the case of fiscal dominance, if investors are unaware of

pending problems as the central bank continuously monetizes government bonds, then at

some point:

A)

the IMF will step in and take over management of the currency.

B)

the nation will reverse course and begin accumulating foreign currency reserves.

C)

reserves will run out, the money supply and inflation will rise, and after that point

the fixed exchange rate cannot be sustained.

D)

the government will be forced to give up control of the central bank.

Page 28

117.

The effect of continued government deficit includes all of the following, EXCEPT a(n):

A)

decrease in reserves.

B)

increase in interest rates.

C)

decrease in inflation.

D)

rapid increase in domestic credit.

118.

The behavior of prices and exchange rates at the time of the crisis will:

A)

increase in a predictable, smooth manner.

B)

exhibit erratic jumps upward.

C)

show an underlying stability.

D)

decrease at first before finding a new equilibrium.

119.

If investors are aware of problems, they launch a ______ attack on the currency and the

central bank is forced _____.

A)

predatory; to sell the remaining foreign currency reserves

B)

speculative; to immediately switch to a floating rate to avoid losing the remaining

foreign currency reserves

C)

tentative; to build up foreign reserves quickly

D)

wholesale; to raise interest rates

120.

Because of speculative attacks due to the belief a fixed rate will fail, pegged exchange

rates:

A)

usually exhibit a long, lingering decline and eventual failure.

B)

often collapse suddenly.

C)

will be revived as the central bank has a wake-up call from the financial sector.

D)

are usually not a good idea in the first place.

121.

The example of Peru during the mid-1980s demonstrates all of the following, EXCEPT:

A)

how quickly the peg can break after profligate debt monetization.

B)

how slowly a peg can break after a debt crisis.

C)

how converting to a floating rate can conserve the last reserves.

D)

the effects on inflation and the exchange rate following the switch to floating.

122.

One may predict the timing of a crisis by analyzing the expectations of investors with

respect to:

A)

the tendency of the central bank to monetize debt.

B)

the health of the economy, especially unemployment and GDP.

C)

the long-run current account deficit.

D)

the credentials of bank officials and their previous experience handling currency

crises.

Page 29

123.

A situation in which maintaining the peg could cause worse harms to the economy (such

as high interest rates) may sway even prudent and cautious central bankers to abandon

it. This situation is called:

A)

the rolling peg.

B)

the contingency claim.

C)

a contingent commitment.

D)

a partial peg.

124.

Weighing the costs and benefits of maintaining the peg would involve comparing the

cost of:

A)

output gaps and a slower economy versus the benefits from additional trade.

B)

fixed prices versus the benefits of higher interest rates.

C)

a trade deficit versus the benefits of greater economic growth.

D)

international instability versus the benefits of lower rates of interest.

125.

Expected depreciation threatens a peg because of all the following, EXCEPT:

A)

when investors expect the peg to fail it will fail in multiple equilibrium situations.

B)

market sentiment will raise the currency premium and lower confidence.

C)

economic fundamentals are crucial to whether a peg holds or fails.

D)

investor confidence may wane and cause a rise in interest rates.

126.

Whenever the market believes there will be a depreciation (the peg will break) then:

A)

the benefits of pegging are greater than the costs of maintaining the peg.

B)

the benefits of depreciation are greater than the costs of depreciation.

C)

the benefits of pegging are negative.

D)

there are never any benefits from depreciation.

127.

In general, when there is a large shock to domestic output, the government finds:

A)

it is less difficult to maintain the peg.

B)

maintaining the peg carries a higher present and future cost, especially if credibility

is low.

C)

it is impossible to maintain the peg.

D)

central bankers are insensitive to the concerns of the population.

Page 30

128.

In general, whenever the benefits of pegging outweigh the costs of a credible peg, what

will the government always choose to do?

A)

depreciate

B)

peg

C)

float

D)

purchase more government bonds

129.

In general, whenever the costs of pegging outweigh the benefits of a non-credible peg,

the government will always:

A)

depreciate.

B)

peg.

C)

make temporary fixed rates permanent.

D)

sell more government bonds.

130.

In general, when market expectations indicate a non-credible peg, or when the costs of

the peg are not greater than the benefits of pegging, what will be the equilibrium

situation?

A)

to depreciate

B)

to peg

C)

uncertain, because in this situation there is no self-fulfilling equilibrium

D)

to sell more government bonds

131.

Under what circumstances will a peg have a longer grace period before investors get

nervous and dump the currency?

A)

when there is no coordinated effort to attack the currency

B)

when there is a lower cost to the economy of maintaining the peg

C)

when traders and speculators are spread out and small in size with no common

belief about the situation

D)

when there is no coordinated effort to attack the currency, a lower cost to the

economy of maintaining the peg, and when traders and speculators are spread out

and small in size with no common belief about the situation

132.

Anticipating the outcome of a peg, economists believe the stable condition is a situation

in which combinations of investor beliefs and government actions coincide. Such a

condition is called:

A)

exchange rate harmony.

B)

a firm peg.

C)

a contingent peg.

D)

a self-confirming equilibrium.

Page 31

133.

Who was the noted financier who speculated against the British pound in 1992 and put

pressure on the exchange rate by selling pounds for German Deutsche Marks, eventually

forcing Britain to float?

A)

John MacMillan

B)

Tony Blair

C)

Gordon Brown

D)

George Soros

134.

Among the solutions proposed for avoiding a foreign exchange crisis are all of the

following, EXCEPT using:

A)

capital controls.

B)

a floating exchange rate.

C)

a currency board or a hard peg.

D)

soft pegs or dirty floats.

135.

The hypothesis that intermediate regimes or a lack of full commitment to a peg will

eventually destroy it results in nations choosing the extremes of peg or float. This

hypothesis is known as:

A)

the trilemma of floating.

B)

the corners hypothesis.

C)

the soft peg dilemma.

D)

the temporary contradiction.

136.

What is the basic difference between the cause(s) of a currency crisis according to the

first-generation model and the second-generation model?

137.

What are the three types of crises discussed in the text? List and briefly explain.

138.

What are the similarities and differences between the impact of a currency crisis on an

advanced country and the impact on emerging country?

139.

Emerging markets and developing economies are more likely to want to maintain fixed

exchange rates because of their dependence on exports. However, these regimes are

often more difficult for them. Why?

Page 32

140.

(Table: Mexico’s Central Bank Balance Sheet) Suppose output in Mexico rises, causing

money demand to change by 75 million pesos. What will happen to reserves, domestic

credit, and the backing ratio? Explain how these changes take place.

141.

(Table: Mexico’s Central Bank Balance Sheet) Suppose foreign interest rates rise in the

United States, causing money demand to change by 150 million pesos. What will

happen to reserves, domestic credit, and the backing ratio? Explain how these changes

take place.

142.

Explain why domestic interest rates may not equal foreign interest rates.

143.

(Table: Mexico’s Central Bank Balance Sheet) Suppose the central bank engages in an

open-market purchase of 300 million pesos. What will happen to reserves, domestic

credit, and the backing ratio? Explain how these changes take place.

144.

A recent phenomenon is the tendency of emerging market economies to accumulate

excess foreign currency reserves so that their backing ratios exceed 100%. What

possible reasons could explain this activity? Is it a sound economic policy? Why or why

not?

145.

Explain the essence of the first-generation crisis model.

Page 33

146.

What is the difference between myopic and forward-looking investors, and what are the

implications for fixed exchange rates?

147.

What is meant by a self-confirming equilibrium?

148.

Some remedies and preventive measures have been put forth to slow or forestall

currency crises, such as capital controls and intermediate regimes. Discuss these

measures and comment on whether they would be effective—why or why not.

Page 35

Page 36

Page 37