Name:

Class:

Date:

Chapter 08: Perfect Competition

True / False

1. An industry consists of all firms that supply output to a particular market.

a.

True

b.

False

True

2. If a perfectly competitive firm raises its price, its sales decrease to zero.

a.

True

b.

False

True

3. Perfectly competitive firms are sometimes called price makers because they have significant control over product price.

a.

True

b.

False

False

4. Marginal revenue is the change in total revenue from using one more unit of an input in the short run.

a.

True

b.

False

False

5. For a perfectly competitive firm, price is identical to marginal revenue at every quantity.

a.

True

b.

False

True

6. The golden rule of profit maximization states that firms maximize profit by producing at the level of output at which

price equals average total cost.

a.

True

b.

False

False

7. When marginal revenue equals marginal cost, the firm just breaks even.

a.

True

b.

False

False

8. A perfectly competitive firm has a horizontal supply curve in the short run.

a.

True

b.

False

False

9. The short-run industry supply curve in a perfectly competitive market is the horizontal sum of each firm’s short-run

supply curve.

Name:

Class:

Date:

Chapter 08: Perfect Competition

a.

True

b.

False

True

10. In short-run equilibrium, a perfectly competitive firm can never earn an economic profit.

a.

True

b.

False

False

11. In a perfectly competitive market, profit attracts entry of new firms in the market in the long run.

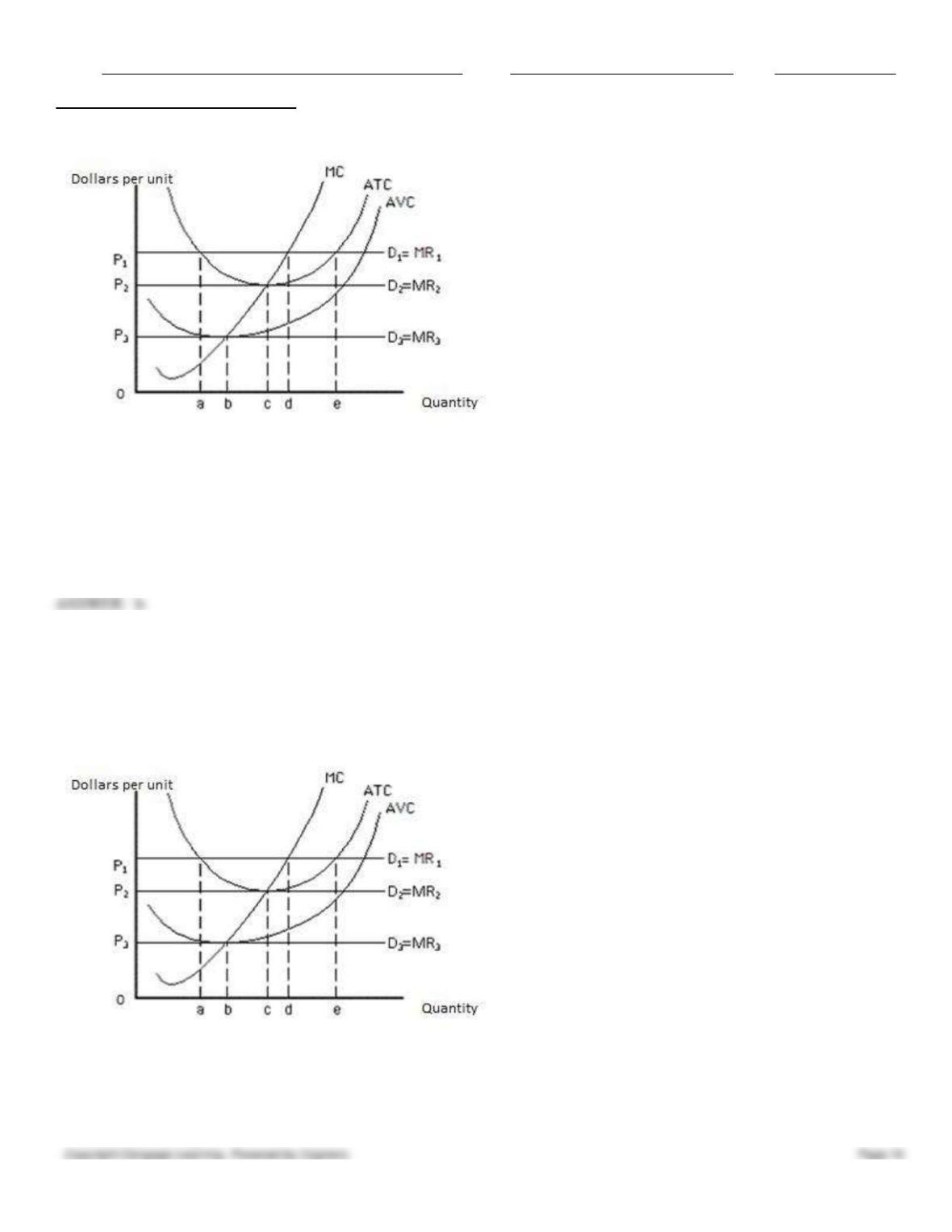

a.

True

b.

False

True

12. In perfect competition, no firm can earn a normal profit In the long run.

a.

True

b.

False

False

13. A firm that minimizes average cost will not survive in the long run.

a.

True

b.

False

False

14. After an increase in demand in a constant-cost industry, the long-run average cost curves of firms shift upward.

a.

True

b.

False

False

15. An increasing-cost industry is one in which per-unit cost increases as output expands in the long run.

a.

True

b.

False

True

16. In a perfectly competitive, increasing-cost industry, if price and quantity increase, demand must have increased.

a.

True

b.

False

True

17. Firms in a perfectly competitive market achieve both allocative and productive efficiency in the short run.

a.

True

b.

False

False

18. Mobility of resources ensures productive efficiency in a perfectly competitive market.

Name:

Class:

Date:

Chapter 08: Perfect Competition

a.

True

b.

False

True

19. A perfectly competitive firm is allocatively efficient because price is identical to marginal cost at every quantity.

a.

True

b.

False

True

20. Consumers benefit from market exchange when the maximum price they are willing to pay for a unit of a good is less

than what they usually pay.

a.

True

b.

False

False

21. Consumer surplus is the area above the supply curve and below the market-clearing price.

a.

True

b.

False

False

22. It is possible for a firm to enjoy a short-run producer surplus while suffering a short-run economic loss.

a.

True

b.

False

True

Multiple Choice

23. Which of the following would not help identify market structure?

a.

The number of firms in a market

b.

The type of product produced in a market

c.

The ease of entry into a market

d.

The forms of competition among the firms in a market

e.

The price of a good sold in a market

e

24. Which of the following is likely to be present in a perfectly competitive market?

a.

Patents

b.

Government licenses

c.

Nonprice competition such as advertising

d.

High capital costs

e.

Firms producing identical products

25. Which of the following is not necessarily a characteristic of a perfectly competitive market structure?

a.

Low prices

Name:

Class:

Date:

Chapter 08: Perfect Competition

b.

A large number of buyers and sellers

c.

A homogeneous product

d.

Perfect information

e.

Easy entry and exit in the long run

a

26. Which of the following is true of a perfectly competitive market?

a.

Firms experience constant returns to scale.

b.

Firms face significant barriers to entry.

c.

Firms experience decreasing returns to scale.

d.

Each firm chooses the price at which it wants to sell its product.

e.

Each seller supplies only a small fraction of the total amount in a market.

e

27. Which of the following characterizes a perfectly competitive market?

a.

A few firms fiercely competing by slashing prices

b.

Product differentiation through aggressive advertising

c.

Perfect information

d.

Limited resource mobility

e.

Barriers to entry, such as licenses

c

28. In a perfectly competitive industry, we are likely to find that _____.

a.

firms produce a wide variety of products

b.

there exist strict barriers to entry

c.

firms do not earn positive profits in the short run

d.

firms do not advertise

e.

firms can choose the price of their products

29. Perfectly competitive firms respond to changing market conditions by varying their:

a.

price.

b.

output.

c.

market share.

d.

cost structures.

e.

advertising campaigns.

30. A firm in a perfectly competitive market:

a.

can raise the price of its product and sell more output.

b.

has to lower the price of its product to sell more output.

c.

can increase its supply to lower the market price.

d.

can decrease its supply to increase the market price.

Name:

Class:

Date:

Chapter 08: Perfect Competition

e.

has to accept the market price for its product.

31. Which of the following firms is most likely to be a perfectly competitive firm?

a.

One of the three largest automobile manufacturers in the United States

b.

One of the “Seven Sisters,” which are oil-producing companies

c.

A public school operated by the government

d.

A farm that grows soybeans

e.

A manufacturer of refrigerators

32. Which of the following best approximates a perfectly competitive market structure?

a.

Automobile manufacturing

b.

The insurance market

c.

Foreign exchange markets

d.

The airlines industry

e.

Manufacture of stereo equipment

33. The price charged by a perfectly competitive firm is determined by:

a.

each individual firm.

b.

a group of firms acting together as a cartel.

c.

market demand and market supply.

d.

the firm’s total costs.

e.

the firm’s average variable cost.

34. Perfectly competitive firms are price takers because:

a.

each firm is too small compared to the market to be able to affect price.

b.

one firm determines the market price and all other firms accept this price.

c.

firms charge the price that government determines.

d.

firms must accept any price that consumers offer them.

e.

firms earn high profits by charging different prices to different groups of consumers.

35. If every firm in a market is a price taker, then which of the following is true?

a.

There are a large number of sellers in the market.

b.

There are many substitutes of the products sold in the market.

c.

There is limited resource mobility.

d.

There are few consumers for the product being sold in the market.

e.

A few firms in the market have market power.

36. The demand curve for the output of a perfectly competitive firm is _____.

Name:

Class:

Date:

Chapter 08: Perfect Competition

a.

perfectly inelastic

b.

perfectly elastic

c.

unit elastic

d.

downward sloping

e.

nonlinear

37. Suppose the market for hot pretzels in New York City is perfectly competitive. Which of the following is true of the

demand in this market?

a.

The demand curve facing each seller is perfectly elastic.

b.

The demand curve facing each seller is perfectly inelastic.

c.

The market demand curve is perfectly elastic.

d.

The market demand curve is perfectly inelastic.

e.

The market demand curve is positively sloped.

a

38. The demand curve facing a perfectly competitive firm is:

a.

vertical at the equilibrium quantity.

b.

upward sloping.

c.

a straight line through the origin.

d.

a horizontal straight line at the market price.

e.

downward sloping.

39. Adam’s Apples, a small firm supplying apples in a perfectly competitive market, decides to cut its production to half

this year. Which of the following is likely to occur in this case?

a.

The market price of apples will increase.

b.

The market price of apples will decrease.

c.

The market demand for apples will increase.

d.

The market price of apples will not be affected.

e.

The market supply curve of apples will shift rightward.

40. Suppose Thelma and Louise both sell tomatoes in a perfectly competitive market. If Louise increases the amount of

tomatoes that she sells in the market, _____.

a.

Thelma must reduce the amount of tomatoes she sells

b.

the price Thelma can charge for her output decreases

c.

the price Thelma can charge for her output increases

d.

the price at which Thelma sells her output is unaffected

e.

Thelma’s profits must fall

41. Individual firms in a perfectly competitive market can:

a.

sell more only by lowering their prices.

Name:

Class:

Date:

Chapter 08: Perfect Competition

b.

sell all they produce at the market price.

c.

earn more profit if they charge a price above the market price.

d.

earn more profit if they charge a price below the market price.

e.

exit the market only if the existing firms allow it.

42. A farmer in the Midwest who produces wheat faces a horizontal demand curve because:

a.

the quantity supplied by him is so large relative to the market that it has no impact on the market price for

wheat.

b.

the quantity supplied by him is so small relative to the market that it has no impact on the market price for

wheat.

c.

he produces a good for which there are no substitutes.

d.

he produces a good for which there are no complements.

e.

he produces a good that no other firm in the market produces.

43. Suppose the equilibrium price in a perfectly competitive industry is $100 and a firm in the industry charges $112.

Which of the following is likely to happen?

a.

The firm will not be able to sell any of its output.

b.

The firm will sell more output than its competitors.

c.

The firm’s profits will increase.

d.

The firm’s revenue will increase.

e.

The firm will gradually take over the entire industry.

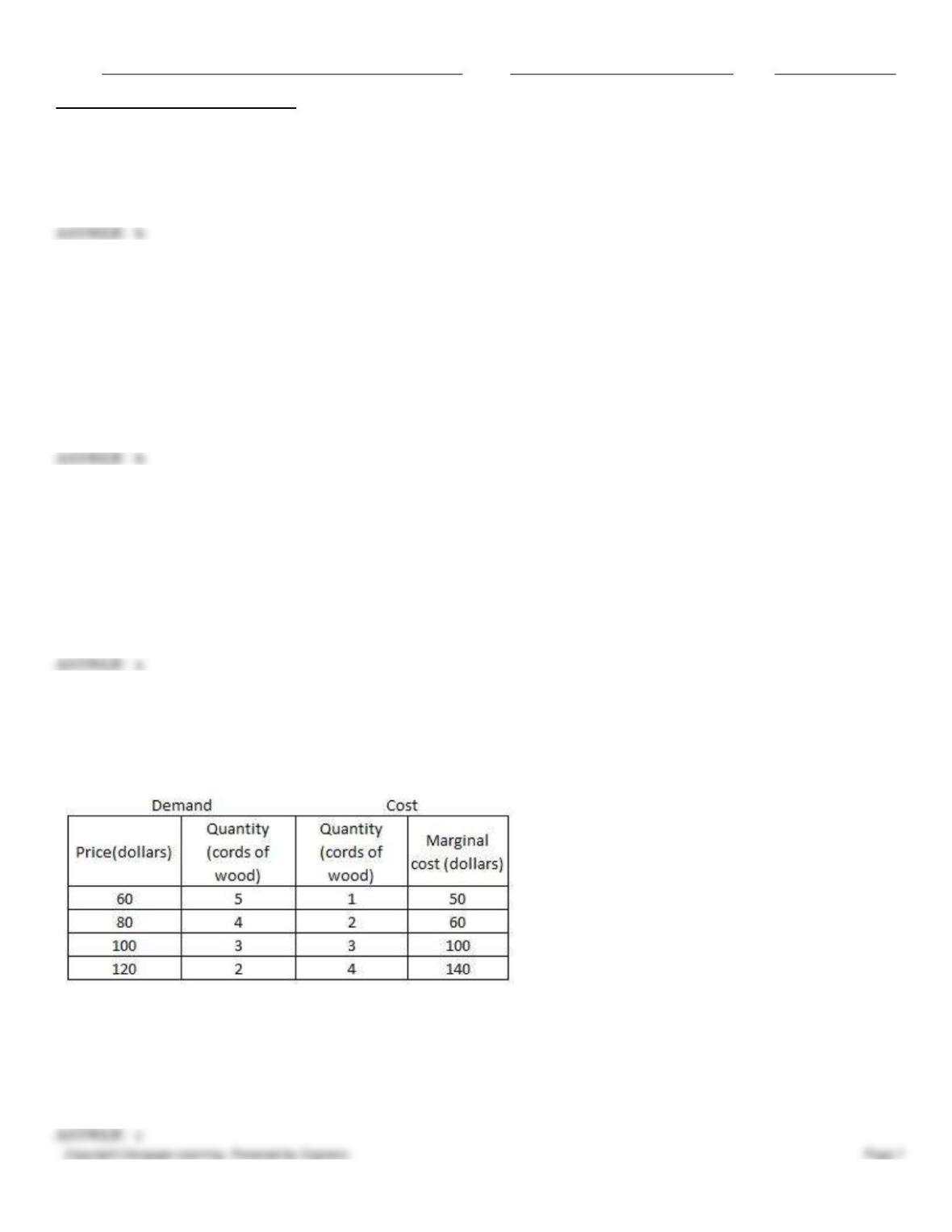

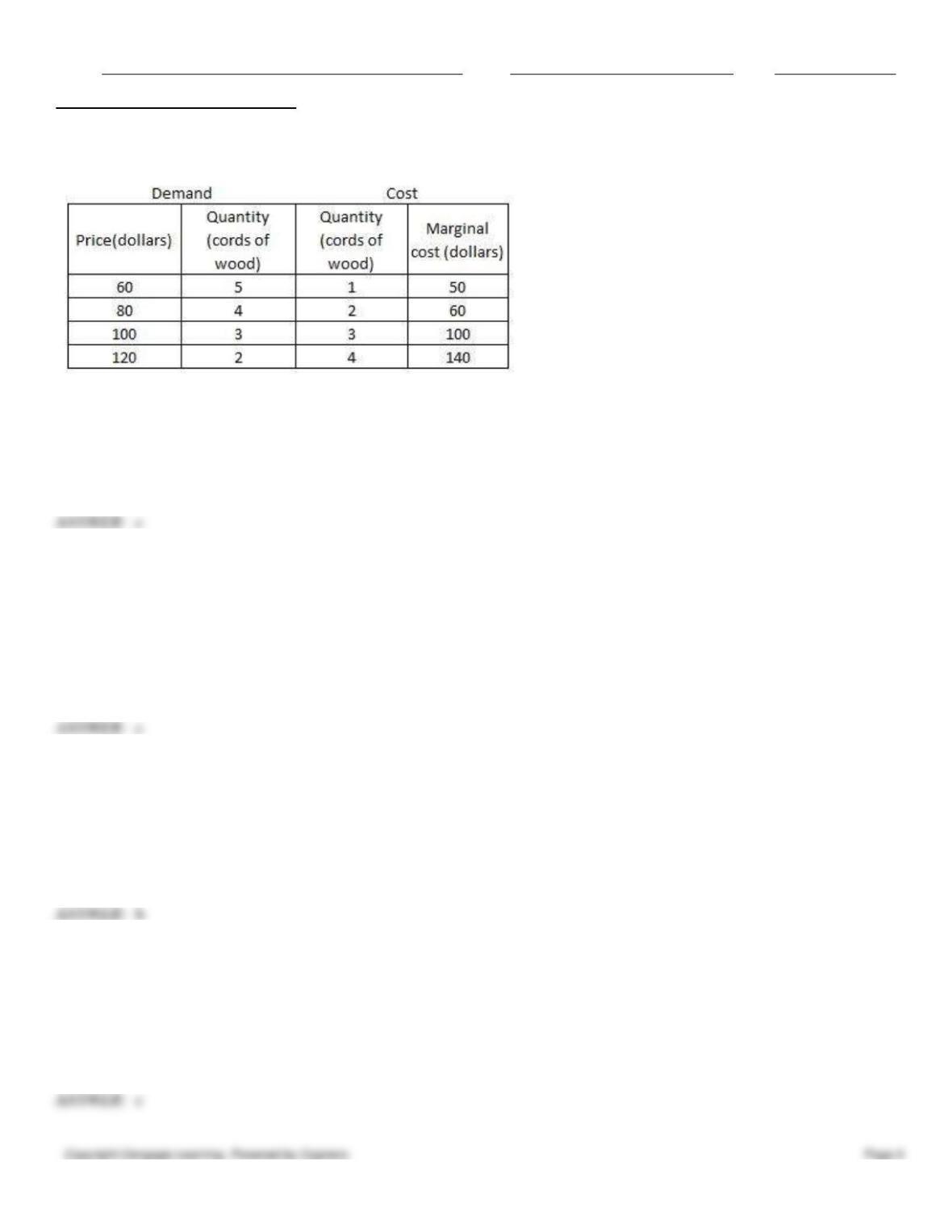

44. The perfectly competitive firewood market is composed of 1,000 identical consumers and 1,000 identical firms. The

table given below shows cost for one representative firm and the demand schedule for one representative consumer. The

equilibrium price in this market is _____.

Table 8.1

a.

$60

b.

$80

c.

$100

d.

$120

e.

below $60

Name:

Class:

Date:

Chapter 08: Perfect Competition

45. The perfectly competitive firewood market is composed of 1,000 identical consumers and 1,000 identical firms. The

table given below shows cost for one representative firm and the demand schedule for one representative consumer. The

profit-maximizing quantity for each firm in this market is _____.

Table 8.1

a.

zero cords of wood

b.

one cord of wood

c.

two cords of wood

d.

three cords of wood

e.

four cords of woods

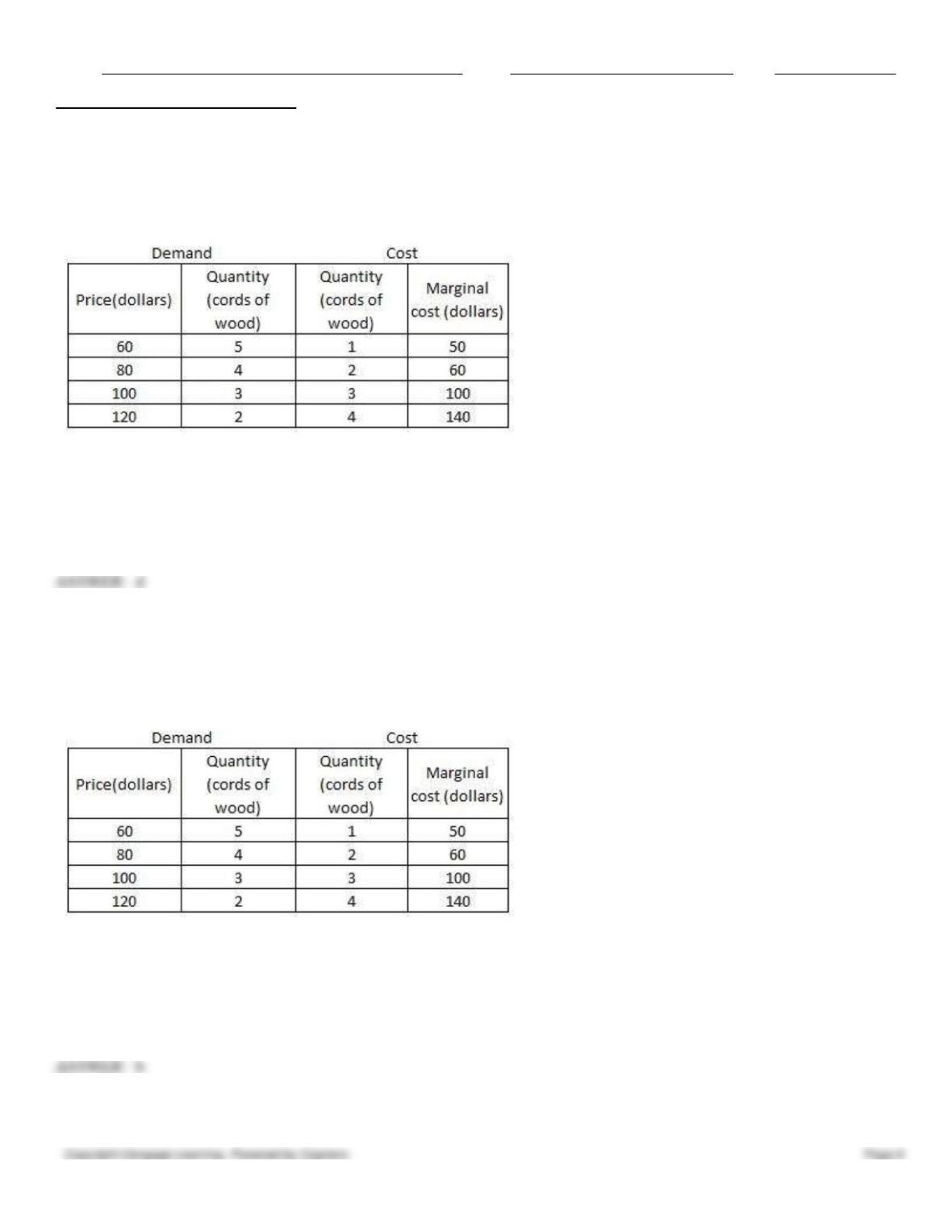

46. The perfectly competitive firewood market is composed of 1,000 identical consumers and 1,000 identical firms. The

table given below shows cost for one representative firm and the demand schedule for one representative consumer. The

demand curve facing a single firm will be a:

Table 8.1

a.

horizontal line at a price of $120.

b.

horizontal line at a price of $100.

c.

vertical line at a quantity of 3 cords of firewood.

d.

horizontal line at a price of $60.

e.

vertical line at a quantity of 4 cords of firewood.

47. The perfectly competitive firewood market is composed of 1,000 identical consumers and 1,000 identical firms. The

table given below shows cost for one representative firm and the demand schedule for one representative consumer.

Name:

Class:

Date:

Chapter 08: Perfect Competition

_____ cords of firewood will be bought and sold in the market at equilibrium.

Table 8.1

a.

5,000

b.

4,000

c.

3,000

d.

2,000

e.

1,000

c

48. In Connecticut, the market for apples is perfectly competitive. Suppose consumers’ tastes change so that the market

demand for apples increases. In this case, the demand curves faced by individual firms will:

a.

not change.

b.

become less elastic.

c.

shift upward.

d.

become upward sloping.

e.

shift downward.

c

49. Economists assume that firms seek to:

a.

maximize accounting profit.

b.

maximize economic profit.

c.

maximize total revenue.

d.

earn normal profit.

e.

maximize cost.

50. Economic theory assumes that:

a.

the goal of firms is to maximize their sales.

b.

firms are concerned only about the quantity supplied in a market.

c.

the goal of firms is to maximize their profit.

d.

firms are concerned only about the price of their product.

e.

firms are concerned only about the utility consumers gain from consumption.

c

Name:

Class:

Date:

Chapter 08: Perfect Competition

51. Which of the following is true of economic profit?

a.

It equals total revenue minus total cost.

b.

It excludes implicit cost.

c.

It is any profit lower than a normal profit.

d.

Firms attempt to maximize accounting profit and are not concerned about economic profit.

e.

It is always equal to zero in a perfectly competitive market in the short run.

52. Which of the following is true of the total revenue curve of a perfectly competitive firm?

a.

It is horizontal.

b.

It is vertical.

c.

The slope of the curve decreases as output increases.

d.

The slope of the curve increases as output increases.

e.

The slope of the curve remains constant slope as output increases.

53. The total revenue curve for a perfectly competitive firm_____.

a.

is a vertical line intersecting the horizontal axis

b.

is a horizontal line intersecting the vertical axis

c.

is a backward-bending curve

d.

is a straight line that starts from the origin and slopes upward

e.

starts at the origin, slopes upward at first, and then slopes downward

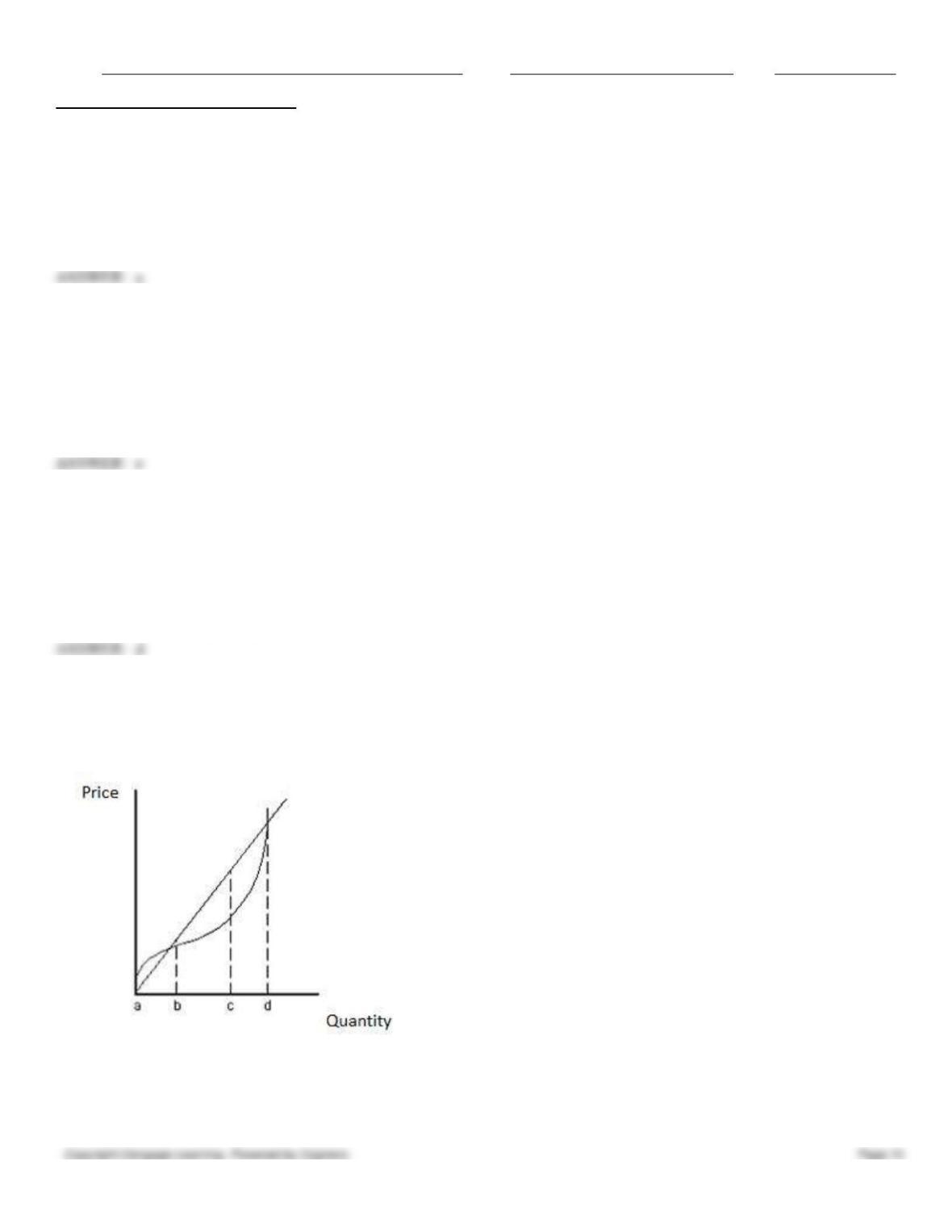

54. The following figure shows the total cost and total revenue curves of a firm. The firm maximizes profit at an output

represented by _____.

Figure 8.1

a.

point a

b.

point b

c.

point c

Name:

Class:

Date:

Chapter 08: Perfect Competition

d.

point d

e.

a point beyond point d

55. The shape of the total cost curve between the output levels represented by points a and b in the following figure

reflects _____.

Figure 8.1:

a.

fixed costs

b.

increasing profits

c.

diminishing marginal returns

d.

increasing marginal returns

e.

economies of scale

56. The total revenue curve in the following figure reflects _____.

Figure 8.1:

a.

a constant rate of profit for the competitive firms

Name:

Class:

Date:

Chapter 08: Perfect Competition

b.

diminishing marginal revenue

c.

increasing marginal revenue

d.

the fact that perfectly competitive firms are price takers

e.

the fact that consumers will purchase more from a firm that sells its product at higher prices

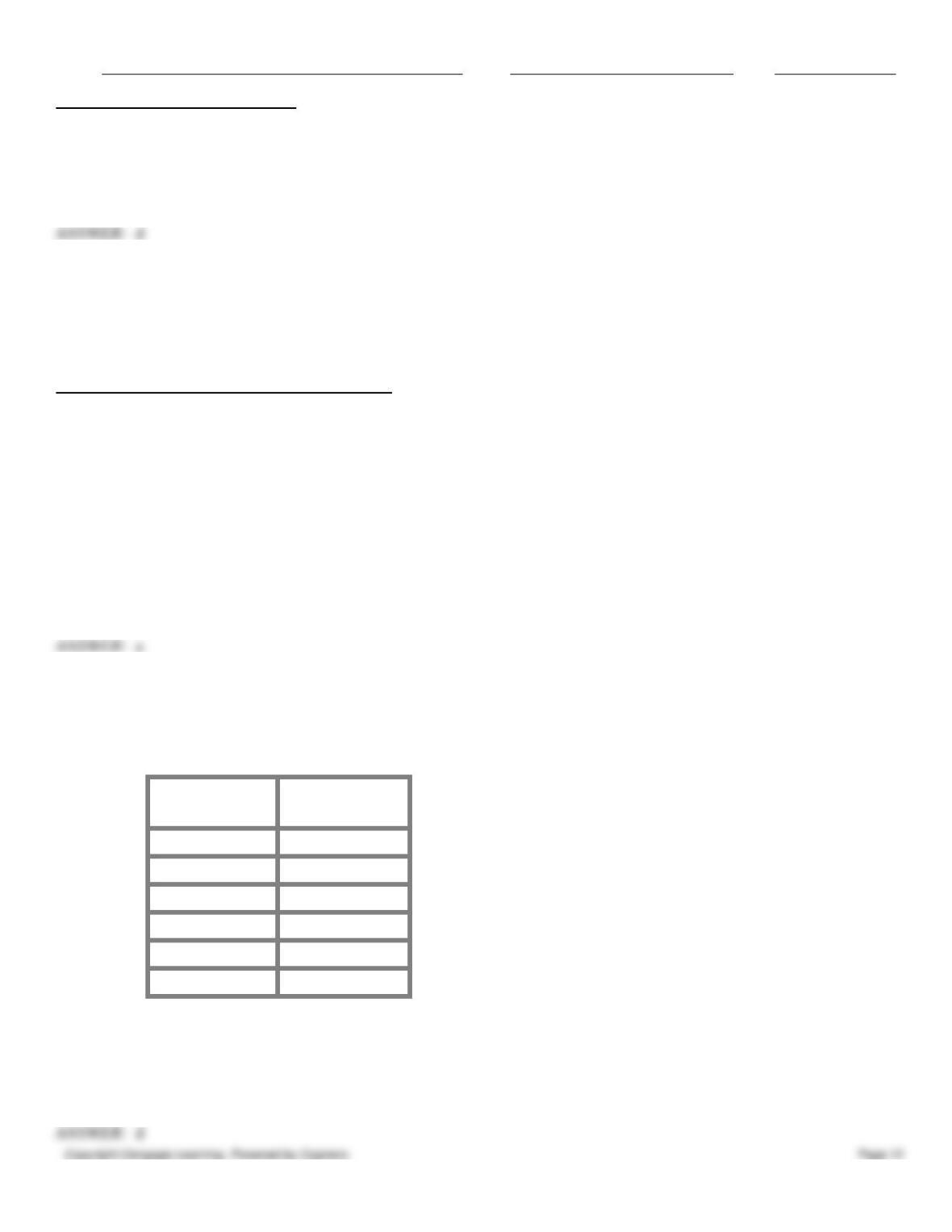

57. The table given below shows the output supplied by a firm and its total cost of production. If the market price is $8.50,

the profit-maximizing output and profit are _____.

Table 8.2

Quantity

of output

Total

Cost ($)

0

50

10

85

20

150

30

220

40

305

50

455

a.

40 units and $35, respectively

b.

40units and $0, respectively

c.

0 units and −$50, respectively

d.

30 units and $25, respectively

e.

50 units and $30, respectively

58. The following table shows the output supplied by a firm and its total cost of production. It represents a firm in the

_____.

Table 8.2

Quantity

Total

of output

Cost ($)

0

50

10

85

20

150

30

220

40

305

50

455

a.

long run because there is no fixed cost

b.

short run because there is no equilibrium

c.

long run because there is an equilibrium level of output

d.

short run because a firm incurs fixed cost

e.

long run because there is a normal profit

Name:

Class:

Date:

Chapter 08: Perfect Competition

59. A perfectly competitive firm that earns an economic profit in the short run choose the output that:

a.

maximizes its total revenue.

b.

minimizes its total cost.

c.

maximizes the difference between total revenue and total cost.

d.

maximizes the difference between total revenue and explicit cost.

e.

maximizes the difference between total revenue and implicit cost.

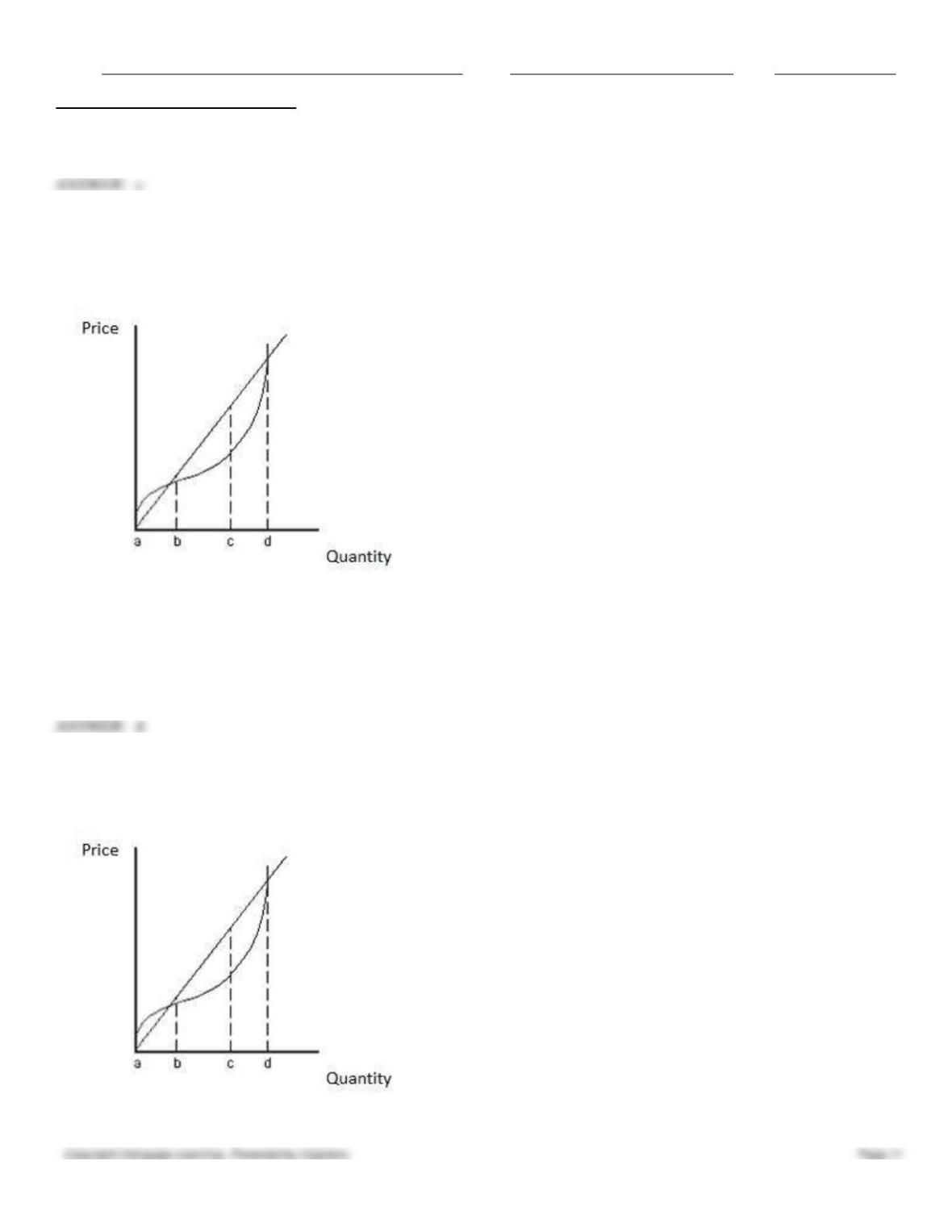

60. The following figure shows short-run profit maximization by a perfectly competitive firm. _____, the marginal

revenue of the firm is equal to its marginal cost.

Figure 8.2

a.

At the output level represented by point a

b.

At the output level represented by point b

c.

At the output level represented by point c

d.

Between the output levels represented by points a and b

e.

Between the output levels represented by points c and d

61. Marginal revenue is defined as:

a.

total revenue divided by quantity.

b.

total revenue minus total cost.

c.

the change in total revenue divided by the change in quantity.

d.

the change in total revenue divided by quantity.

e.

the change in total revenue divided by the change in per unit price.

62. The slope of the total revenue curve for a perfectly competitive firm equals:

a.

marginal revenue.

b.

economic profit.

Name:

Class:

Date:

Chapter 08: Perfect Competition

c.

accounting profit.

d.

average revenue.

e.

normal profit.

63. _____ is the change in total cost from producing one more unit of the output.

a.

Marginal cost

b.

Variable cost

c.

Opportunity cost

d.

Average cost

e.

Fixed cost

64. The Hound Dog Bus Company contemplates expanding its New Mexico operations by offering services from Raton to

Santa Fe. It has estimated that the total cost of the trip will be $400, of which $150 is the fixed cost, which it has already

paid. The company expects an increase in revenue by $275 from the trip. The Hound Dog Bus Co. should:

a.

offer this service because it will earn a positive economic profit.

b.

not offer this service because marginal revenue is less than marginal cost.

c.

offer this service because total revenue exceeds fixed cost.

d.

not offer this service because total cost exceeds total revenue.

e.

offer this service because the additional revenue exceeds the additional cost of this service.

65. The Hound Dog Bus Company contemplates expanding its Virginia operations by offering services from Fairfax to

Arlington. The total cost of the trip would be $120, of which $50 is the fixed cost, which it has already paid. The firm

expects to earn $60 in revenue from the trip. The Hound Dog Bus Company should:

a.

offer this service because it will earn a positive economic profit.

b.

not offer this service because the marginal revenue is less than the marginal cost.

c.

offer this service because total revenue exceeds fixed cost.

d.

not offer this service because total cost exceeds total revenue.

e.

offer this service because the added revenue exceeds the added cost of this service.

66. Average revenue is:

a.

total revenue minus total cost.

b.

total revenue divided by the quantity of output.

c.

total revenue divided by the quantity of the variable input.

d.

the change in total revenue divided by the change in output.

e.

the change in total revenue divided by the change in the quantity of an input used.

67. If a perfectly competitive firm sells its product at the market price of $14 per unit, _____.

a.

its marginal revenue is $14 and its average revenue is less than $14 per unit

b.

its marginal revenue is less than $14 per unit and its average revenue is also less than $14 per unit

Name:

Class:

Date:

Chapter 08: Perfect Competition

c.

its average revenue is $14 and its marginal revenue is less than $14 per unit

d.

its average revenue is $14 and its marginal revenue is also $14

e.

its average and marginal revenue are $14 only for the first unit sold

68. For perfectly competitive firms, which of the following correctly shows the relationship among market price (P),

average revenue (AR), and marginal revenue (MR)?

a.

Price = Average revenue (AR) = Marginal revenue (MR)

b.

Price > Average revenue (AR) = Marginal revenue (MR)

c.

Price = Average revenue AR > Marginal revenue (MR)

d.

Price = Average revenue (AR) < Marginal revenue (MR)

e.

Price < Average revenue (AR) = Marginal revenue (MR)

69. If a firm is producing at an output level where the total revenue curve intersects the total cost curve, which of the

following is true of the firm?

a.

Its revenue is maximized.

b.

Its cost is maximized.

c.

Its cost is minimized.

d.

Its profit is maximized.

e.

Its profit is zero.

70. For a perfectly competitive firm, ____.

a.

price equals marginal revenue at all output levels

b.

price equals marginal revenue only at the profit-maximizing quantity

c.

price exceeds marginal revenue at all output levels

d.

price is less than marginal revenue only at the profit-maximizing quantity

e.

price is less than marginal revenue at all output levels

71. A perfectly competitive firm’s profit per unit of output equals:

a.

price minus average variable cost.

b.

price minus marginal cost.

c.

total revenue minus total cost.

d.

price times quantity.

e.

price minus average total cost.

72. Consider the following figure that shows the demand and the cost curves of a perfectly competitive firm. The firm will

earn zero economic profit _____.

Figure 8.3

Name:

Class:

Date:

Chapter 08: Perfect Competition

a.

at a price of P1

b.

at a price of P2

c.

at a price of P3

d.

at a price between P1 and P2

e.

at a price above P1

73. Consider the following figure that shows the demand and the cost curves of a perfectly competitive firm. At a market

price of P1, the profit-maximizing quantity for the firm is _____.

Figure 8.3

a.

a units of output

b.

b units of output

c.

e units of output

d.

d units of output

Name:

Class:

Date:

Chapter 08: Perfect Competition

e.

between d and e units of output

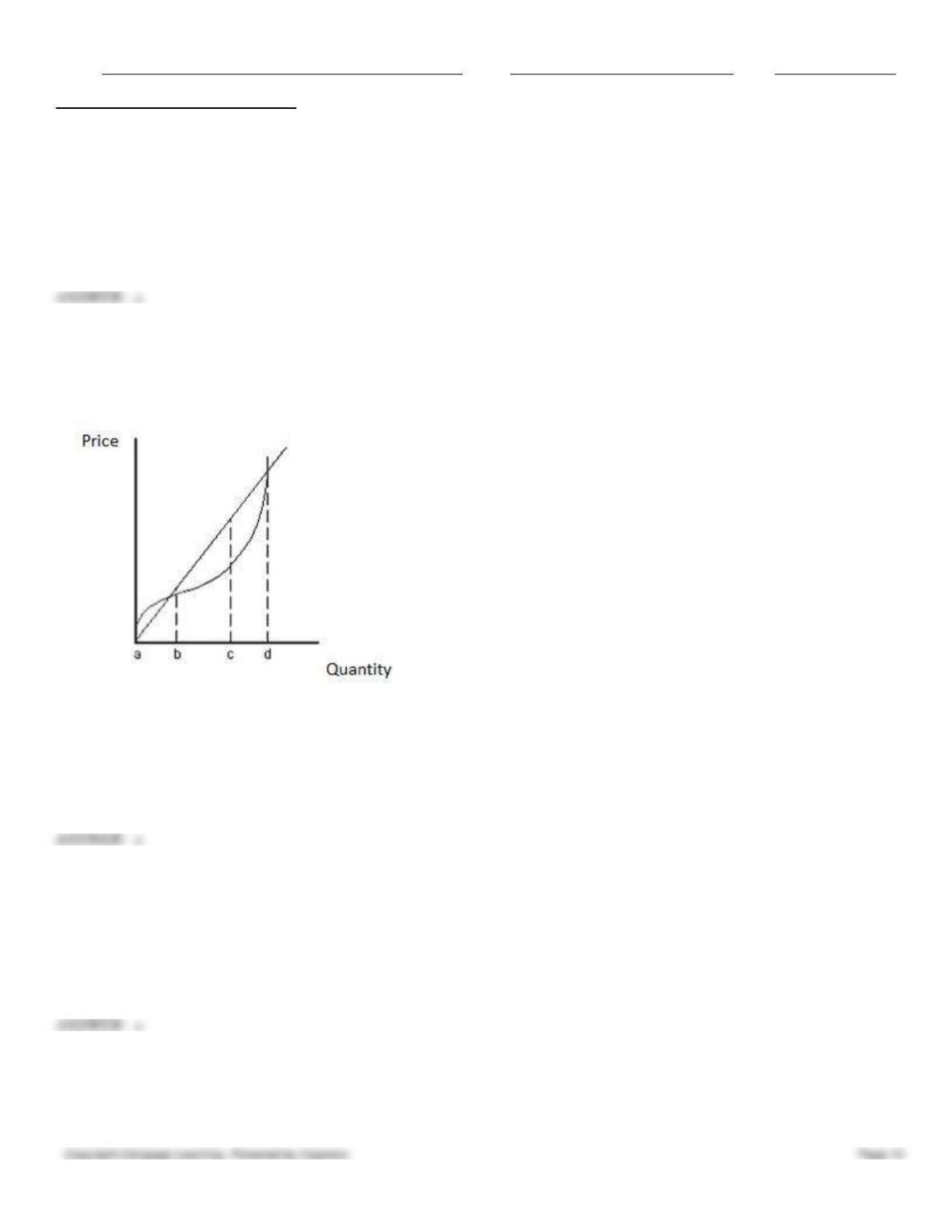

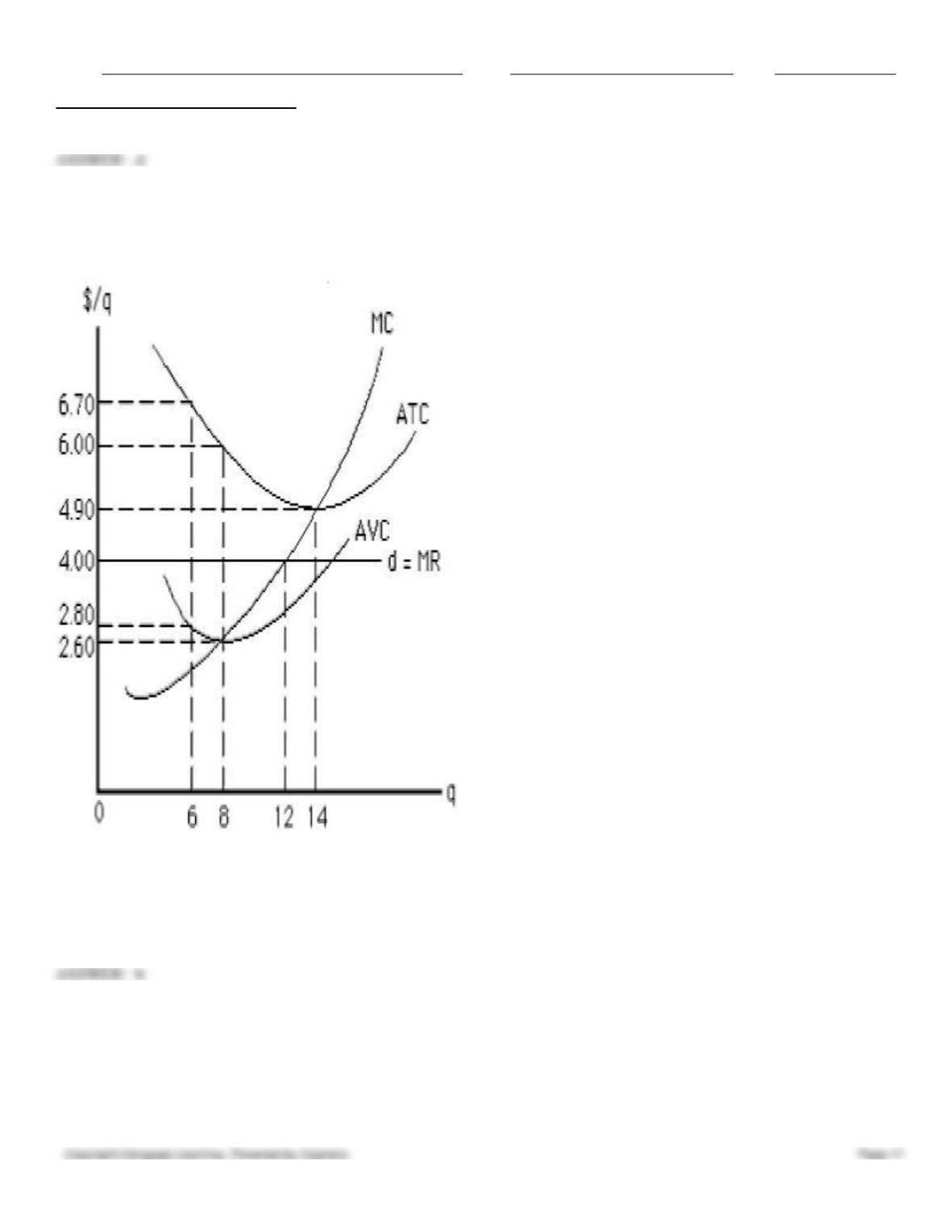

74. Consider the following figure that shows the demand and the cost curves of a perfectly competitive firm. If the price-

taking firm is currently producing 6 units, it should _____ to maximize profit in the short run.

Figure 8.4

a.

keep producing 6 units

b.

increase production to 12 units

c.

increase production to 14 units

d.

increase production to 8 units

e.

decrease production below 6 units.

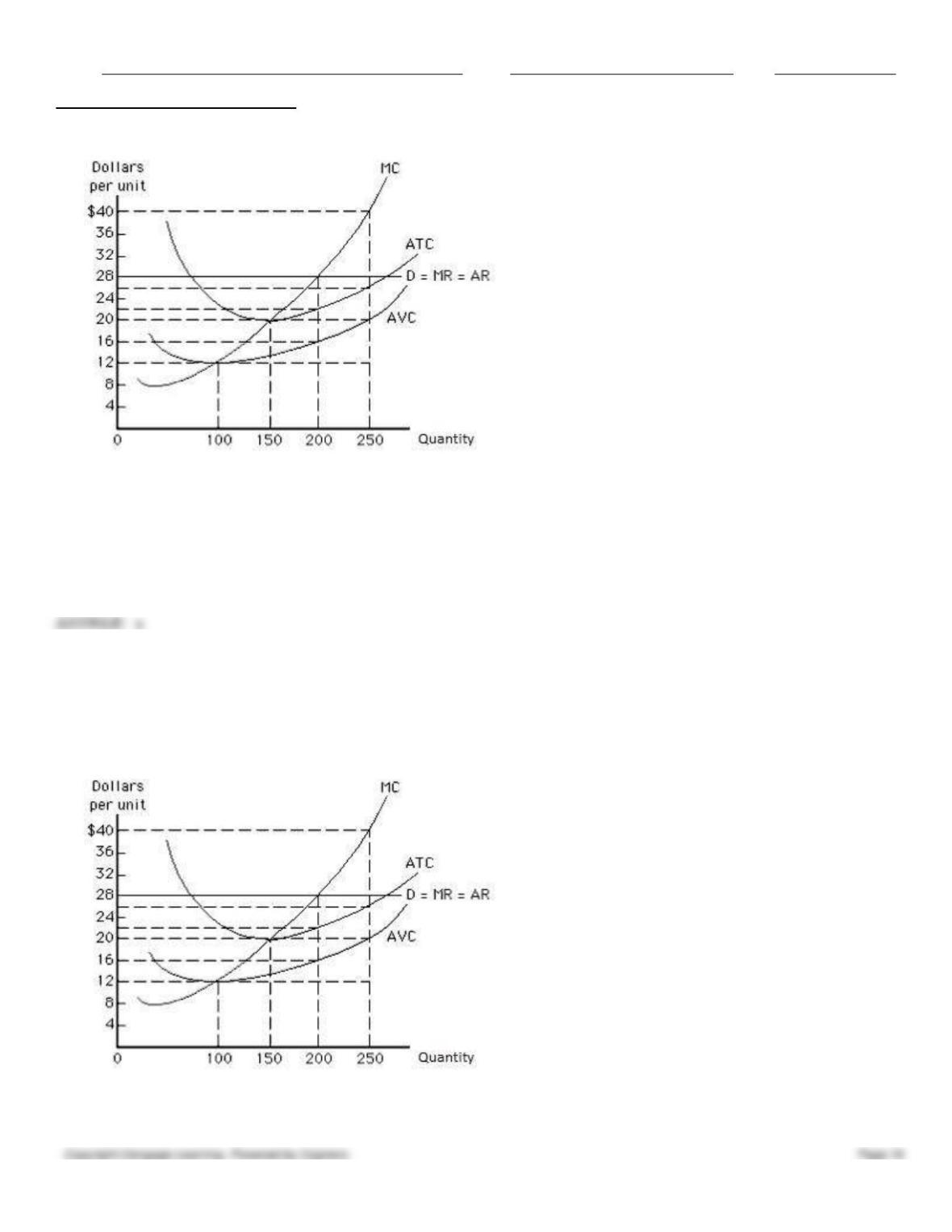

75. The figure given below shows the demand and the cost curves of a perfectly competitive firm. The market price equals

_____.

Figure 8.5

Name:

Class:

Date:

Chapter 08: Perfect Competition

a.

$28

b.

$12

c.

$40

d.

$20

e.

$24

a

76. The figure given below shows the demand and the cost curves of a perfectly competitive firm. Total revenue at the

profit-maximizing output equals _____.

Figure 8.5

a.

$2,400