Name:

Class:

Date:

Chapter 08: Perfect Competition

b.

$4,000

c.

$5,200

d.

$5,600

e.

$6,000

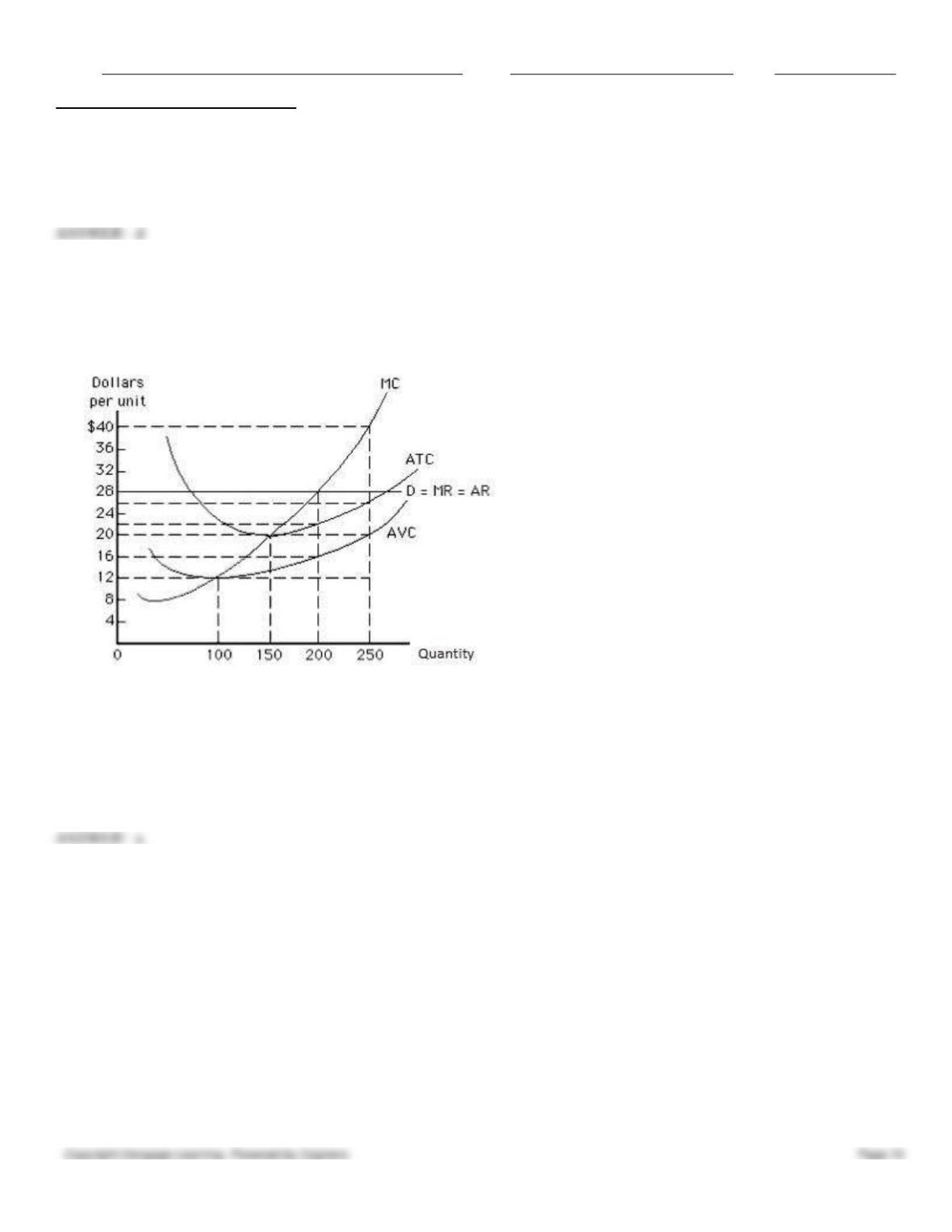

77. The following figure shows the demand and the cost curves of a perfectly competitive firm. Total cost at the profit-

maximizing output equals _____.

Figure 8.5

a.

$4,400

b.

$4,800

c.

$5,600

d.

$2,400

e.

$5,200

a

78. The following figure shows the demand and the cost curves of a perfectly competitive firm. At the profit-maximizing

output level, the firm experiences:

Figure 8.5

Name:

Class:

Date:

Chapter 08: Perfect Competition

a.

a loss of $3,200.

b.

a profit of $1,600.

c.

a profit of $1,200.

d.

zero profit or loss.

e.

a loss of $800.

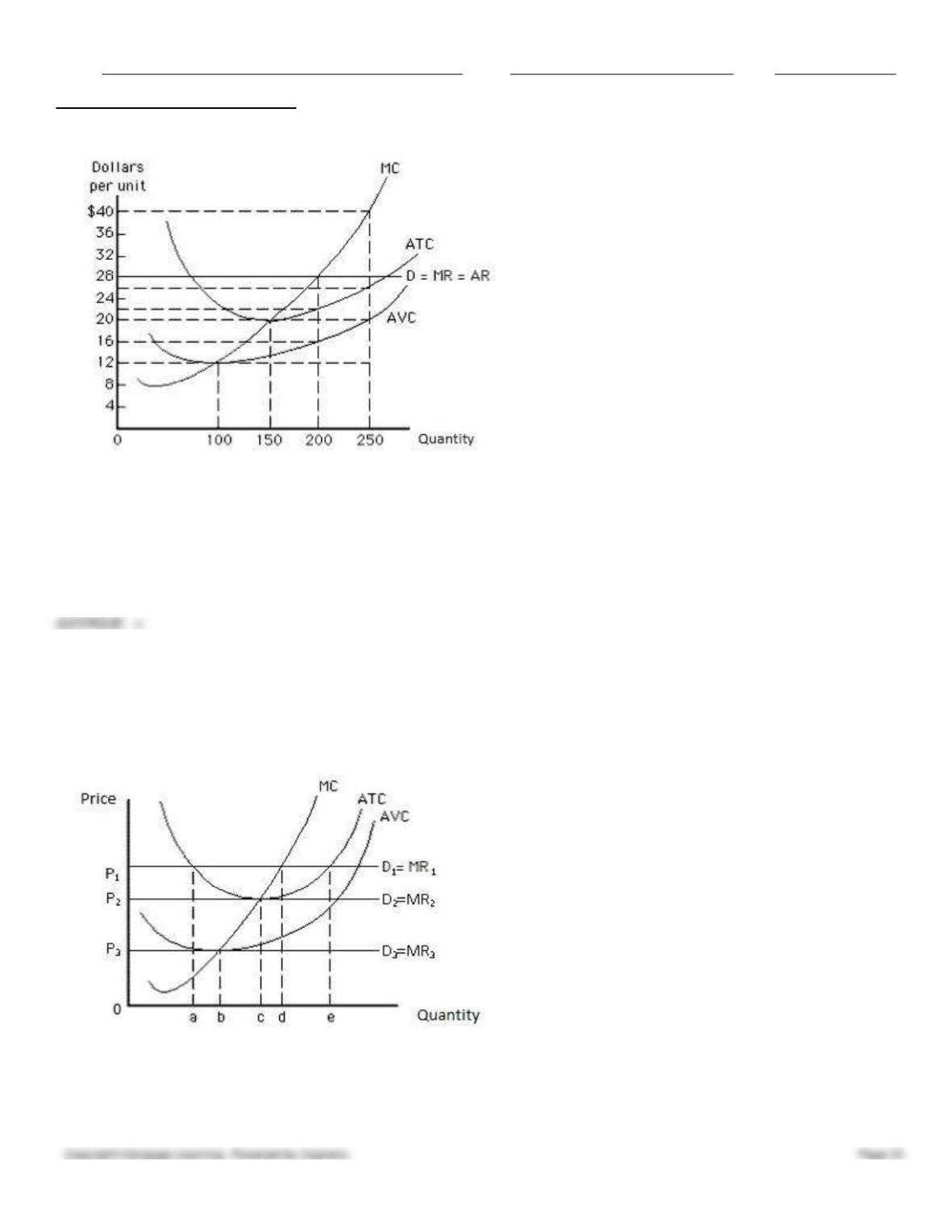

79. Consider the following figure that shows the demand and the cost curves of a perfectly competitive firm. _____, the

firm will shut down in the short run.

Figure 8.6

a.

At a price of P1

b.

At a price of P2

c.

At a price below P3

Name:

Class:

Date:

Chapter 08: Perfect Competition

d.

At a price above P1

e.

At a price between P2 and P3

c

80. In the short run, if a firm shuts down, its loss is equal to:

a.

zero.

b.

its variable cost.

c.

its fixed cost.

d.

its fixed cost minus its variable cost.

e.

its fixed cost minus total revenue.

c

81. If a firm shuts down in the short run, its total revenue is _____.

a.

zero

b.

equal to its fixed cost

c.

greater than its variable cost

d.

greater than its fixed cost

e.

less than its variable cost

a

82. If Harry’s Blueberries, a perfectly competitive firm, shuts down in the short run, Harry must pay:

a.

the variable cost but not the fixed cost of production.

b.

the marginal cost but not the variable cost of production.

c.

both the variable cost and the fixed cost of production.

d.

only the variable cost of production.

e.

only the fixed cost of production.

e

83. If a perfectly competitive firm is incurring losses in the short run, it:

a.

will incur a loss in the long run as well.

b.

will shut down.

c.

will continue to operate in the short run if its fixed cost is covered.

d.

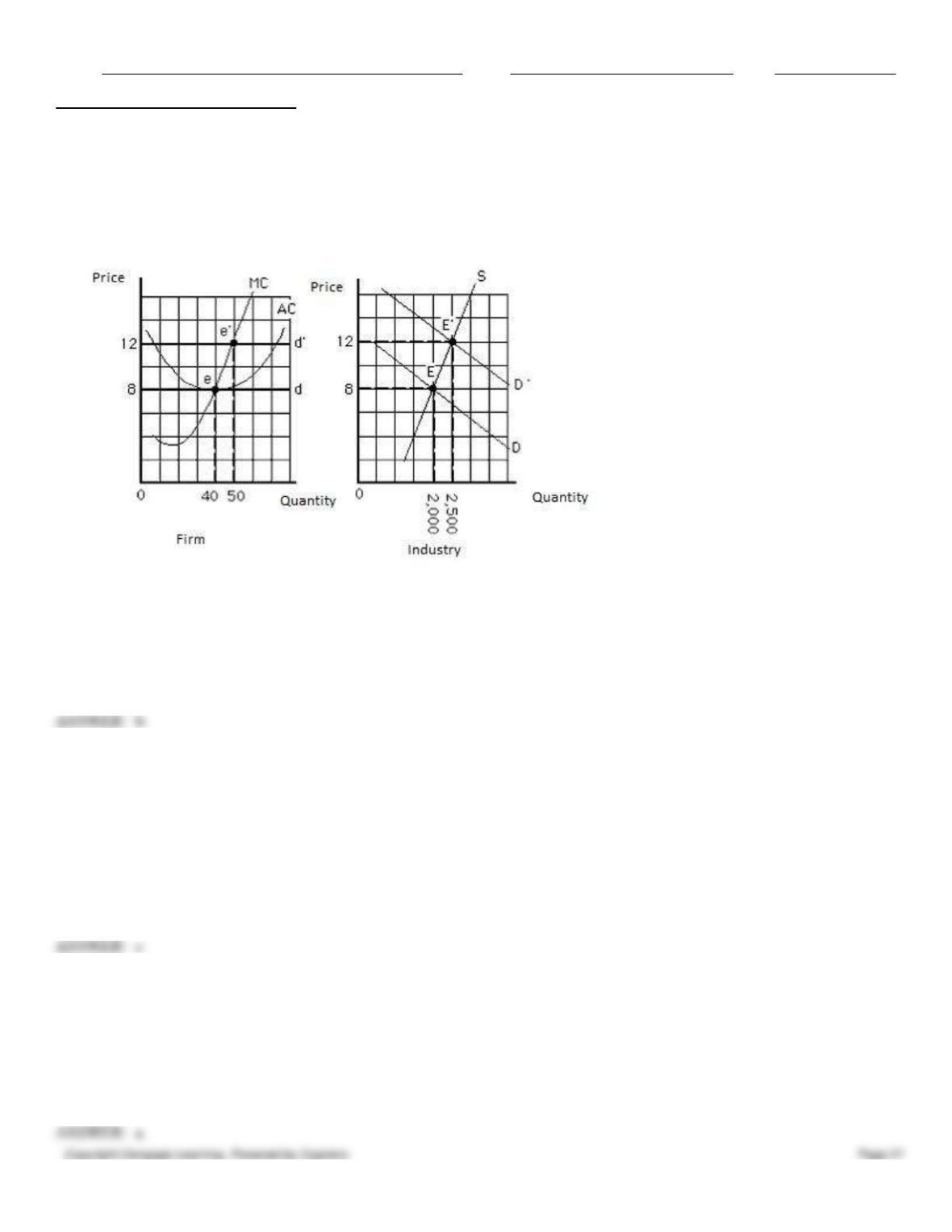

will continue to operate in the short run if its variable cost is covered.

e.

will raise its price in the short run.

84. If a manufacturer shuts down in the short run, it must be true that before the shutdown, at all positive output levels,

_____.

a.

average total cost was less than average variable cost

b.

fixed cost was greater than total revenue

c.

variable cost was greater than total revenue

d.

profit was zero

e.

total cost plus total revenue was less than profit

Name:

Class:

Date:

Chapter 08: Perfect Competition

85. At its present rate of output, Barrel O’ Biscuits, a perfectly competitive firm, finds that its marginal cost exceeds its

marginal revenue and its price exceeds its average variable cost. To maximize profit, the firm should _____.

a.

lower the price

b.

increase the price

c.

increase output

d.

decrease output

e.

produce at its current level of output

86. Suppose a firm finds it is better off operating than shutting down in the short run. At the quantity at which marginal

cost equals marginal revenue, _____.

a.

total cost equals total revenue

b.

average cost equals average revenue

c.

profit is maximized

d.

revenue is maximized

e.

cost is minimized

87. For a perfectly competitive firm operating at the profit-maximizing output level in the short run, _____.

a.

marginal revenue equals total revenue

b.

marginal cost equals price

c.

marginal cost equals average total cost

d.

marginal cost equals average variable cost

e.

average fixed cost equals price

88. Claude’s Copper Clappers sells clappers for $40 each in a perfectly competitive market. At its present level of output,

Claude’s marginal cost is $39, average variable cost is $45, and average total cost is $60. To improve his profit or loss

situation, Claude should:

a.

increase output.

b.

reduce output but not to zero.

c.

continue to produce the present level of output.

d.

shut down.

e.

increase the price.

89. Claude’s Copper Clappers sells clappers for $40 each in a perfectly competitive market. At its present level of output,

Claude’s marginal cost is $39, average variable cost is $25, and average total cost is $45. To improve his profit or loss

situation, Claude should:

a.

increase output.

b.

reduce output but not to zero.

c.

continue to produce the present level of output.

d.

shut down.

Name:

Class:

Date:

Chapter 08: Perfect Competition

e.

raise the price.

90. Claude’s Copper Clappers sells clappers for $60 each in a perfectly competitive market. At its present level of output,

Claude’s marginal cost is $65, average variable cost is $25, and average total cost is $62. To improve his profit or loss

situation, Claude should _____.

a.

increase output

b.

reduce output but not to zero

c.

continue to produce the present level of output

d.

shut down

e.

raise the price

91. Claude’s Copper Clappers sells clappers for $65 each in a perfectly competitive market. At its present level of output,

Claude’s marginal cost is $65, average variable cost is $45, and average total cost is $67. To maximize his profit or

minimize his loss, Claude should:

a.

increase output.

b.

reduce output but not to zero.

c.

continue producing the present level of output.

d.

shut down.

e.

raise the price.

92. A perfectly competitive firm sells 200 units at a market price of $40 per unit. Its marginal cost is $50, and it incurs a

variable cost of $10,000. To improve its profit or loss situation, this firm should _____.

a.

increase output sold to 300 units

b.

reduce output but not to zero

c.

continue to produce the present level of output

d.

shut down

e.

raise the price to $45 per unit

93. Assume a perfectly competitive firm incurs a total cost of $10,000, marginal cost of $38, and fixed cost of $2,000. It

sells 200 units of its product at a market price of $38 per unit. Which of the following is true in this case?

a.

The firm earns an economic profit of $7,600.

b.

The firm incurs an economic loss of $7,600.

c.

The average variable cost of production exceeds the market price.

d.

The average total cost of production is less than the market price.

e.

The firm earns an economic profit of $6,600.

94. If price is less than minimum average variable cost, a perfectly competitive firm that continues to produce in the short

run _____.

a.

earns a positive economic profit

b.

incurs a loss greater than its fixed cost

Name:

Class:

Date:

Chapter 08: Perfect Competition

c.

can cover all of its fixed cost and some of its variable cost

d.

can cover all of its variable cost and some of its fixed cost

e.

can cover both its fixed cost and its variable cost

95. In the short run, a firm will produce a positive amount of output as long as:

a.

price exceeds average variable cost.

b.

price exceeds marginal cost.

c.

price is less than average variable cost.

d.

average variable cost is less than average total cost.

e.

fixed cost exceeds total revenue.

a

96. Peggy’s Kegs sells kegs in a perfectly competitive market. If the firm decides to shut down due to economic losses in

the short run, its current loss is _____.

a.

zero

b.

greater than if it had kept selling kegs

c.

the same as the losses it incurred while operating

d.

equal to fixed cost

e.

less than its total revenue

97. Suppose a price-taking firm produces 400 units at its optimal output level. At that output rate, marginal cost is $200,

average total cost is $240, and average variable cost is $170. The firm will be forced to go out of business in the short run

if:

a.

the market price equals $200 per unit.

b.

the market price is between $170 per unit and $240 per unit.

c.

the market price falls below $170 per unit.

d.

the market price is between $200 per unit and $240 per unit.

e.

the market price equals $240 per unit.

c

98. A perfectly competitive firm is currently producing at a point where price is $10 and both marginal cost and average

variable cost are $7. To maximize profit or minimize loss in the short run, this firm should:

a.

raise its price.

b.

increase its output.

c.

reduce its output.

d.

lower its price.

e.

shut down.

99. Irrespective of whether a firm produces or shuts down in the short run, fixed cost is equal to its _____.

a.

average variable cost

b.

total cost

Name:

Class:

Date:

Chapter 08: Perfect Competition

c.

sunk cost

d.

total revenue

e.

marginal cost

100. Which of the following is true at the quantity at which average total cost equals average revenue?

a.

Economic profit is zero.

b.

Marginal cost equals marginal revenue.

c.

Economic profit is maximized.

d.

Total revenue is maximized.

e.

Total cost is minimized.

101. The significance of the minimum point on the average variable cost curve is that:

a.

it is the profit-maximizing level of output.

b.

it is the selling price of a good.

c.

it is the point of indifference between producing at a loss and shutting down.

d.

if the firm produces one more unit, its average variable cost will be less than its marginal cost.

e.

it shows the amount of total cost incurred by a firm in the production process.

102. The price that represents the shutdown point for a perfectly competitive firm corresponds to the _____.

a.

highest point on the marginal cost curve

b.

lowest point on the marginal cost curve

c.

highest point on the average variable cost curve

d.

lowest point on the average variable cost curve

e.

lowest point on the average total cost curve

103. A perfectly competitive firm’s short-run supply curve is the same as:

a.

the supply curve of all the other firms in the industry.

b.

the upward-sloping portion of its marginal cost curve.

c.

the portion of its marginal cost curve above the minimum average variable cost.

d.

the portion of its average variable cost curve above the average total cost curve.

e.

the market demand curve.

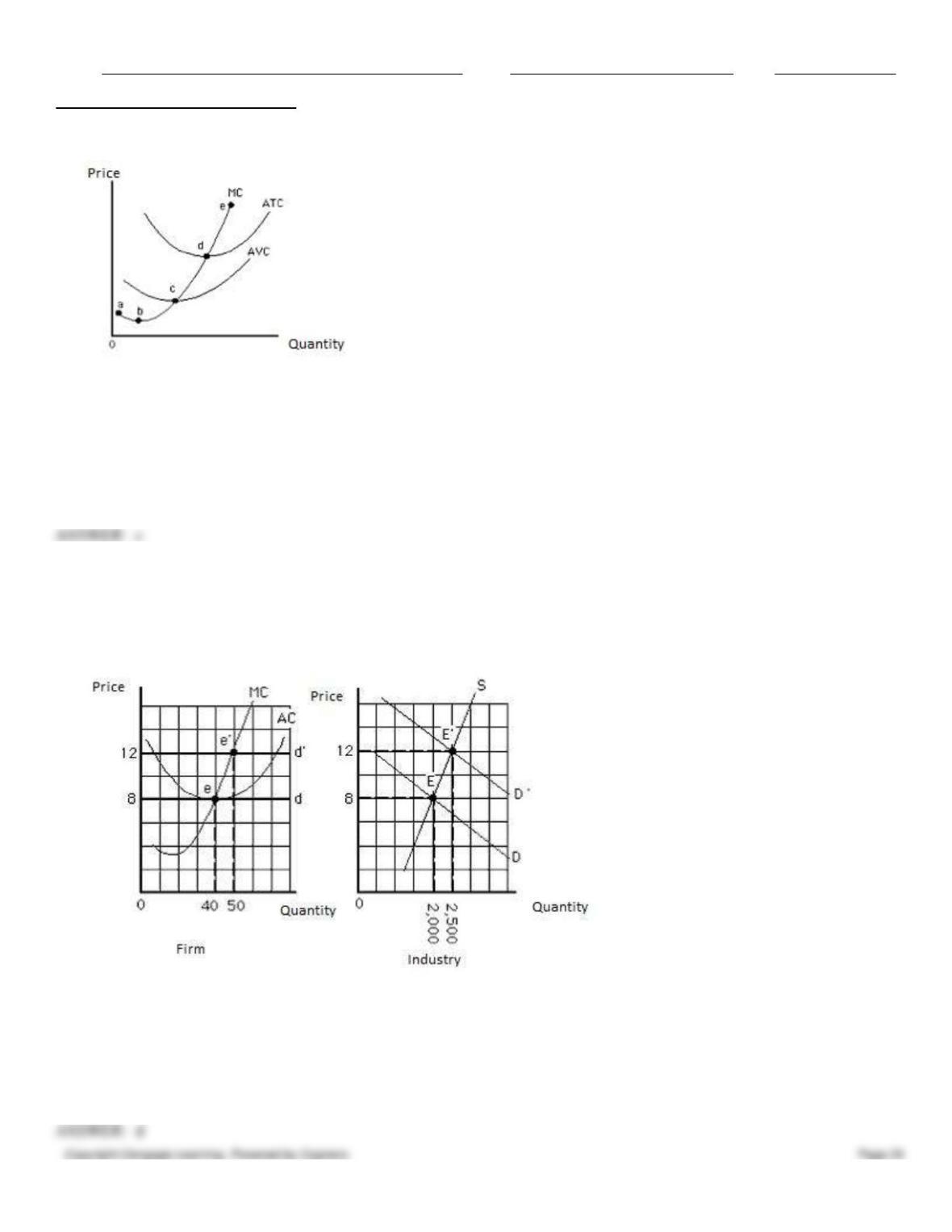

104. For the perfectly competitive firm represented in the figure given below, the short-run supply curve is:

Figure 8.7

Name:

Class:

Date:

Chapter 08: Perfect Competition

a.

abcde.

b.

bcde.

c.

cde.

d.

de.

e.

abcd.

c

105. Consider the following figure that shows a competitive firm on the left panel and a competitive market on the right

panel. Assuming all the firms in the market are identical, there are _____ firms in this industry.

Figure 8.8

a.

2,000

b.

2,500

c.

40

d.

50

e.

60

Name:

Class:

Date:

Chapter 08: Perfect Competition

106. Consider the following figure that shows a competitive firm on the left panel and a competitive market on the right

panel. The movement along the curve S from point E to E’ in the right panel of the figure represents:

Figure 8.8

a.

an increase in the number of firms in the industry.

b.

an increase in output supplied by each firm in the industry.

c.

both an increase in the number of firms in the industry and an increase in each firm’s output.

d.

an increase in the cost of production for the firms in the market.

e.

an increase in total revenue of the representative firm from $8 to $12.

107. Mary Ann and Donna provide lawn mowing services in a perfectly competitive market. When they began their

operations, the market rate for mowing lawns was $50 per lawn. After the price increased to $60, they were willing to

work on Saturdays as well. Their response to the price change will be shown by:

a.

a rightward shift of the market supply curve.

b.

a leftward shift of the market supply curve.

c.

an upward movement along their firm’s marginal cost curve.

d.

a downward movement along their firm’s marginal cost curve.

e.

a rightward shift in the market demand curve for mowing lawns.

108. The short-run equilibrium in a perfectly competitive market is determined by the:

a.

intersection of the market demand and market supply curves.

b.

intersection of the market demand and the largest firm’s supply curve.

c.

intersection of the market demand and the largest firm’s marginal cost curve.

d.

intersection of the market supply curve and the demand curve of the largest firm in a market.

e.

intersection of the market supply curve and the most profitable firm’s demand curve.

Name:

Class:

Date:

Chapter 08: Perfect Competition

109. Suppose an increase in population increases the demand for automobile repairs in New Haven County’s market for

auto repair, which is a perfectly competitive market. Which of the following is true in the short run?

a.

Auto repair centers may be able to earn an economic profit.

b.

Normal profits decrease.

c.

The market supply curve of auto repair services shifts to the left.

d.

The effect on equilibrium price and quantity is indeterminate.

e.

After firms adjust to the new equilibrium, the price of auto repair services will exceed the marginal cost.

110. A decline in market demand in a competitive industry will result in a(n):

a.

increase in the equilibrium price.

b.

decrease in the number of firms in the industry in the short run.

c.

economic profit for all firms in the industry.

d.

decrease in the equilibrium quantity.

e.

rightward shift of the market supply curve in the short run.

111. If new firms enter a perfectly competitive industry seeking economic profit and begin supplying goods in the market,

which of the following will occur?

a.

The market supply curve will shift leftward.

b.

The market supply curve will shift rightward.

c.

The market supply and demand curves will both shift to the left.

d.

The market supply and demand curves will both shift to the right.

e.

There will be a downward movement along a fixed supply curve.

112. In the long run, the entry of new firms in a competitive industry:

a.

drives up the equilibrium price.

b.

eliminates economic profits.

c.

reduces the equilibrium quantity.

d.

makes the demand curve facing each firm more inelastic.

e.

makes the market demand curve steeper.

113. When an industry supply curve shifts rightward so that economic profit is erased, _____.

a.

firms that charge a higher price exit the industry

b.

the quantity demanded decreases

c.

all firms in the industry incur economic losses

d.

the entry of new firms and the expansion of existing firms stop

e.

the marginal revenue of the existing firms increases

114. Which of the following factors ensures that economic profit will be zero in the long run in a competitive industry?

Name:

Class:

Date:

Chapter 08: Perfect Competition

a.

Each firm is small relative to the market.

b.

Each firm has access to perfect information.

c.

Goods produced in the market are homogeneous.

d.

Each firm is a price taker.

e.

There is easy entry and exit in the market.

115. Perfectly competitive firms will leave the industry that they are operating in if they _____.

a.

are unable to cover their variable costs

b.

suffer losses, despite covering variable costs in the short run

c.

experience economies of scale

d.

earn a normal profit

e.

experience economies of scope

116. Which of the following is true of a perfectly competitive firm in long-run equilibrium?

a.

The market supply curve is horizontal.

b.

The market demand curve is horizontal.

c.

It will minimize its average total cost.

d.

It will charge a price above its marginal cost.

e.

Marginal cost is minimized.

117. Which of the following is true for a perfectly competitive firm in long-run equilibrium?

a.

Marginal revenue (MR) = Marginal cost (MC) = Average total cost (ATC)

b.

Marginal revenue (MR) = Marginal cost (MC) = Average fixed cost (AFC)

c.

Marginal cost (MC) = Average total cost (ATC) = Average fixed cost (AFC)

d.

Marginal revenue (MR) = Marginal cost (MC) > Average total cost (ATC)

e.

Marginal revenue (MR) = Marginal cost (MC) > Average variable cost (AVC)

118. Long-run equilibrium for a perfectly competitive firm occurs when:

a.

Price (P) = Marginal cost (MC) = Short-run average total cost (SRATC) = Long-run average cost (LRAC).

b.

Marginal cost (MC) = Marginal revenue (MR) = Average fixed cost (AFC) = Short-run average total cost

SRATC.

c.

Marginal cost (MC) = Marginal revenue (MR) = Price (P) > Long-run average cost (LRAC).

d.

Price (P) = Marginal revenue (MR) = Long-run average variable cost (LRAVC) = Long-run average cost

(LRATC).

e.

Marginal cost (MC) = Marginal revenue (MR) = Average fixed cost (AFC) = Long-run average cost (LRAC).

119. Suppose a perfectly competitive firm and industry is in long-run equilibrium. A rightward shift of the market demand

curve is likely to:

a.

shift the demand curve facing the firm downward and increase the quantity supplied in the market.

Name:

Class:

Date:

Chapter 08: Perfect Competition

b.

shift the demand curve facing the firm upward and not cause any change in the quantity supplied in the

market.

c.

shift the demand curve facing the firm downward and increase the quantity supplied in the market.

d.

shift the demand curve facing the firm upward and increase quantity supplied in the market.

e.

shift the demand curve facing the firm downward and not cause any change in the quantity supplied in the

market.

120. Suppose a perfectly competitive firm and industry is in long-run equilibrium and the firm earns an economic profit in

the short run. Which of the following is likely to occur in the long run?

a.

The market supply curve will shift to the left, and the market price will increase.

b.

The market supply curve will shift to the right, and the market price will decrease.

c.

The firm will continue to earn economic profit.

d.

There will be an increase in the amount of economic profit earned by the firm.

e.

Industry output will decrease.

121. If a perfectly competitive firm is in long-run equilibrium and market demand suddenly decreases, the firm will

experience:

a.

a greater economic profit.

b.

a normal profit.

c.

a lower average total cost.

d.

a lower average variable cost.

e.

an economic loss.

e

122. If you were to put the following effects of a decrease in demand into the sequence in which they occur, which would

be the last one?

a.

The demand curve facing each individual firm shifts downward.

b.

Each firm reduces quantity supplied to the point where marginal cost equals its decreased marginal revenue.

c.

In the short run, the market price drops.

d.

Market output falls.

e.

A short-run loss forces some firms out of business in the long run.

e

123. The relationship between price and quantity supplied after firms fully adjust to any short-term economic profit or loss

resulting from a change in demand is illustrated by the _____.

a.

long-run industry supply curve

b.

Dutch auction model

c.

short-run firm supply curve

d.

constant-cost industry supply curve

e.

short-run industry supply curve

a

124. A constant-cost industry is one:

Name:

Class:

Date:

Chapter 08: Perfect Competition

a.

whose average costs are constant in the short run.

b.

that experiences economies of scale throughout its scale of operation.

c.

that experiences a stable demand in the long run.

d.

whose cost curves do not change as new firms enter the market.

e.

that faces increasing resource prices as new firms enter the market.

125. A horizontal long-run industry supply curve occurs under conditions of _____.

a.

economies of scale

b.

diseconomies of scale

c.

monopoly

d.

increasing costs

e.

constant costs

e

126. If an industry is a constant-cost industry, _____.

a.

the prices of its inputs increase even when output remains constant

b.

it uses the same amount of inputs even at higher levels of output

c.

the prices of its inputs rise at a constant rate as it uses more inputs

d.

the prices of its inputs remain the same as the number of firms increases

e.

firms in the industry experience economies of scale throughout their scales of operation

127. Suppose each firm’s long-run average cost of production does not vary with the entry of new firms in a perfectly

competitive industry and a long-run adjustment results in a smaller industry output but leaves price unchanged. Which of

the following is likely to be true in this case?

a.

The market demand curve did not shift.

b.

The market demand curve shifted to the left, and the market supply curve shifted to the right.

c.

The market supply curve shifted to the left, and the market demand curve shifted to the right.

d.

Both market supply and demand increased, but supply increased more than demand.

e.

The industry is a constant-cost industry.

e

128. Suppose a perfectly competitive constant-cost industry is in long-run equilibrium when market demand increases.

What will probably happen to a firm in this industry in the long run?

a.

There will be no change in the equilibrium price and quantity supplied by the firm.

b.

The equilibrium price will be higher in the long run.

c.

The equilibrium price will be lower in the long run.

d.

It will charge the same equilibrium price but will reduce its output.

e.

It will experience higher average total costs and will reduce its output.

a

129. The long-run supply curve for a constant-cost perfectly competitive industry is _____.

a.

a ray from the origin at a 45-degree angle

Name:

Class:

Date:

Chapter 08: Perfect Competition

b.

perfectly inelastic

c.

relatively inelastic

d.

perfectly elastic

e.

downward sloping

130. Suppose a perfectly competitive, increasing-cost industry is in long-run equilibrium when market demand increases.

What is likely to happen to a typical firm in the long run?

a.

It will not change either the equilibrium price charged or the equilibrium quantity supplied.

b.

The equilibrium price will be higher in the long run.

c.

The equilibrium price will be lower than the original equilibrium price in the long run.

d.

It will not change the equilibrium price but will increase output.

e.

It will experience a lower average total cost and will increase output.

131. In an increasing-cost industry, the entry of new firms _____.

a.

decreases the equilibrium price

b.

increases the average cost at each level of output

c.

shifts the industry demand curve to the left

d.

increases economic profits in the industry

e.

shifts the long-run industry supply curve to the right

132. Which of the following is most likely to be an increasing-cost industry?

a.

An industry whose firms experience diseconomies of scale

b.

An industry whose firms experience economies of scale

c.

An industry that is a major buyer in the markets for the inputs it uses

d.

An industry that is a very small buyer in the markets for the inputs it uses

e.

An industry in which the firms earn positive economic profit in the long run

133. The long-run market supply curve for an increasing-cost, perfectly competitive industry _____.

a.

is horizontal

b.

slopes upward

c.

is backward bending

d.

slopes downward

e.

is vertical

134. Suppose a perfectly competitive increasing-cost industry is in long-run equilibrium when market demand increases.

Which of the following statements is true in this case?

a.

Existing firms will earn economic profits in the new long-run equilibrium.

b.

Existing firms will decrease output in the short run.

c.

New firms will enter the industry in the short run.

Name:

Class:

Date:

Chapter 08: Perfect Competition

d.

Some resource suppliers to the industry will earn higher income.

e.

The new long-run equilibrium price will be lower than the original equilibrium price.

135. Suppose a perfectly competitive, increasing-cost industry is in long-run equilibrium when market demand increases.

In the long run, a typical firm _____.

a.

will stop production as total revenue no longer covers the average variable cost of production

b.

experiences a higher average total cost and equilibrium price

c.

experiences a lower average total cost and equilibrium price

d.

experiences the same equilibrium price but a greater average total cost

e.

experiences the same equilibrium price but a lower average total cost

136. Firms achieve productive efficiency by:

a.

striving to minimize their fixed cost.

b.

striving to maximize their total revenue.

c.

producing at their minimum long-run average cost.

d.

producing at their minimum long-run marginal cost.

e.

producing the products that have no substitute.

137. The term productive efficiency refers to:

a.

the short-run equilibrium for a competitive firm.

b.

the production of all goods and services that consumers want.

c.

the production of a good at the lowest long-run average cost.

d.

the equality between average total and average variable cost.

e.

satisfying the condition of equality between marginal cost and marginal revenue.

138. A firm said to be is productively efficient if, _____.

a.

it produces its output at the lowest possible cost

b.

it sells its product at the lowest possible price

c.

it earns a positive economic profit

d.

it produces what consumers demand

e.

it earns a normal profit in the short run

139. Resources are efficiently allocated when production occurs at that point at which:

a.

the marginal cost curve intersects the average variable cost curve.

b.

price is equal to average revenue.

c.

price is equal to marginal cost.

d.

the marginal revenue curve intersects the average variable cost curve.

e.

price is equal to average variable cost.

Name:

Class:

Date:

Chapter 08: Perfect Competition

140. To achieve allocative efficiency, firms:

a.

strive to minimize their fixed costs.

b.

strive to maximize their profits.

c.

produce at their minimum long-run average cost.

d.

produce at their minimum long-run marginal cost.

e.

produce the output consumers value most.

141. If a market is allocatively efficient, _____.

a.

firms produce at the minimum point of their marginal cost curve

b.

firms produce at the minimum point of their total cost curve

c.

consumers minimize their expenditures

d.

total utility cannot be increased through a reallocation of resources

e.

total output cannot be decreased through a reallocation of resources

142. Allocative efficiency occurs in markets when:

a.

the marginal benefit that consumers attach to the last unit purchased equals the opportunity cost of the

resources employed to produce that unit.

b.

the marginal benefit that consumers attach to the last unit purchased exceeds the opportunity cost of the

resources employed to produce that unit.

c.

goods are produced at the minimum of average total cost.

d.

goods are distributed evenly among consumers.

e.

government establishes price ceilings below the market price.

143. If, at the equilibrium quantity in a market, the benefit of the last unit produced just equals its marginal cost, _____.

a.

each firm earns a positive economic profit

b.

the market is said to have achieved productive efficiency

c.

the market is said to have achieved allocative efficiency

d.

the firms in the market are said to have achieved economies of scale

e.

each firm in the market incurs an economic loss

144. In the short run, producers derive surplus from market exchange because:

a.

the price they receive is greater than the minimum amount they require to sell a good.

b.

the price they receive is equal to the minimum amount they require to sell a good.

c.

the price they receive is less than the minimum amount they require to sell a good.

d.

market price equals average total cost.

e.

they can charge higher prices for their products by restricting supply.

145. In the short run, producer surplus equals _____.

Name:

Class:

Date:

Chapter 08: Perfect Competition

a.

Total revenue (TR) − Variable cost (VC)

b.

Total revenue (TR) − Average variable cost (AVC)

c.

Total revenue (TR) + Variable cost (VC)

d.

Total revenue (TR) − Average fixed cost (AFC)

e.

Total revenue (TR) + Total cost (TC)

a

146. If MC’s Hammers, a perfectly competitive firm, finds that its total revenue is $45,000, its fixed cost is $20,000, and

its total cost is $50,000, its producer surplus is _____.

a.

zero

b.

−$5,000

c.

$25,000

d.

$15,000

e.

−$25,000

147. When market exchange occurs voluntarily in a competitive market, _____.

a.

consumer choice does not involve any opportunity cost

b.

the sum of consumer surplus and producer surplus is maximized

c.

both consumer surplus and producer surplus are eliminated

d.

buyers benefit at the expense of producers

e.

the exchange confers no net benefit to the participants

148. We say that equilibrium in a perfectly competitive market is allocatively efficient because:

a.

the sum of consumer and producer surplus is maximized.

b.

the sum of consumer and producer surplus is minimized.

c.

the sum of consumer and producer surplus is zero.

d.

a consumer can attain the highest possible indifference curve, given his or her budget constraint.

e.

producer surplus is zero.

a

149. The combination of producer and consumer surplus shows the:

a.

gains from voluntary exchange.

b.

maximum price that sellers can charge.

c.

maximum price that buyers are willing to pay for a good.

d.

minimum price below which sellers will not sell.

e.

minimum price buyers are willing to pay for a good.

a

150. Which of the following is true of social welfare?

a.

It is a government program through which society takes care of low-income people.

b.

It refers to the overall well-being of people in an economy.

c.

It is measured in terms of spending on social welfare programs.

Name:

Class:

Date:

Chapter 08: Perfect Competition

d.

It applies to sociology, not economics.

e.

It solely depends on the income earned by people.