Chapter 08: Risk and Rates of Return

5.5% and the market risk premium, (rM – rRF), equals 4%. Which of the following statements is CORRECT?

a.

If the risk-free rate increases but the market risk premium remains unchanged, the required return will increase

for both stocks but the increase will be larger for Nile since it has a higher beta.

b.

If the market risk premium increases but the risk-free rate remains unchanged, Nile’s required return will

increase because it has a beta greater than 1.0 but Elba’s required return will decline because it has a beta less

than 1.0.

c.

Since Nile’s beta is twice that of Elba’s, its required rate of return will also be twice that of Elba’s.

d.

If the risk-free rate increases while the market risk premium remains constant, then the required return on an

average stock will increase.

e.

If the market risk premium decreases but the risk-free rate remains unchanged, Nile’s required return will

decrease because it has a beta greater than 1.0 and Elba’s will also decrease, but by more than Nile’s because it

has a beta less than 1.0.

8-4 The Relationship Between Risk and Rates of Return

Multiple Choice

FOFM.BRIG.17.08.04 – The Relationship Between Risk and Rates of Return

United States – BUSPROG.FOFM.BRIG.17.03 – BUSPROG: Analytic

United States – OH – DISC.FOFM.BRIG.17.07 – Risk and return

Bloom’s: Analysis

6/23/2015 3:25 PM

6/23/2015 3:25 PM

96. Stock X has a beta of 0.6, while Stock Y has a beta of 1.4. Which of the following statements is CORRECT?

a.

A portfolio consisting of $50,000 invested in Stock X and $50,000 invested in Stock Y will have a required

return that exceeds that of the overall market.

b.

Stock Y must have a higher expected return and a higher standard deviation than Stock X.

c.

If expected inflation increases but the market risk premium is unchanged, then the required return on both

stocks will fall by the same amount.

d.

If the market risk premium declines but expected inflation is unchanged, the required return on both stocks

will decrease, but the decrease will be greater for Stock Y.

e.

If expected inflation declines but the market risk premium is unchanged, then the required return on both

stocks will decrease but the decrease will be greater for Stock Y.

8-4 The Relationship Between Risk and Rates of Return

Multiple Choice

FOFM.BRIG.17.08.04 – The Relationship Between Risk and Rates of Return

United States – BUSPROG.FOFM.BRIG.17.03 – BUSPROG: Analytic

United States – OH – DISC.FOFM.BRIG.17.07 – Risk and return

Bloom’s: Analysis

6/23/2015 3:25 PM

6/23/2015 3:25 PM

Chapter 08: Risk and Rates of Return

97. Stock A has a beta of 0.8 and Stock B has a beta of 1.2. 50% of Portfolio P is invested in Stock A and 50% is invested

in Stock B. If the market risk premium (rM – rRF) were to increase but the risk-free rate (rRF) remained constant, which of

the following would occur?

a.

The required return would increase for both stocks but the increase would be greater for Stock B than for

Stock A.

b.

The required return would decrease by the same amount for both Stock A and Stock B.

c.

The required return would increase for Stock A but decrease for Stock B.

d.

The required return on Portfolio P would remain unchanged.

e.

The required return would increase for Stock B but decrease for Stock A.

8-4 The Relationship Between Risk and Rates of Return

Multiple Choice

FOFM.BRIG.17.08.04 – The Relationship Between Risk and Rates of Return

United States – BUSPROG.FOFM.BRIG.17.03 – BUSPROG: Analytic

United States – OH – DISC.FOFM.BRIG.17.07 – Risk and return

Bloom’s: Analysis

6/23/2015 3:25 PM

6/23/2015 3:25 PM

98. Stock A has a beta of 0.7, whereas Stock B has a beta of 1.3. Portfolio P has 50% invested in both A and B. Which of

the following would occur if the market risk premium increased by 1% but the risk-free rate remained constant?

a.

The required return on Portfolio P would increase by 1%.

b.

The required return on both stocks would increase by 1%.

c.

The required return on Portfolio P would remain unchanged.

d.

The required return on Stock A would increase by more than 1%, while the return on Stock B would increase

by less than 1%.

e.

The required return for Stock A would fall, but the required return for Stock B would increase.

8-4 The Relationship Between Risk and Rates of Return

Multiple Choice

FOFM.BRIG.17.08.04 – The Relationship Between Risk and Rates of Return

United States – BUSPROG.FOFM.BRIG.17.03 – BUSPROG: Analytic

United States – OH – DISC.FOFM.BRIG.17.07 – Risk and return

Bloom’s: Analysis

6/23/2015 3:25 PM

6/23/2015 3:25 PM

99. Assume that the risk-free rate remains constant, but the market risk premium declines. Which of the following is most

likely to occur?

a.

The required return on a stock with beta = 1.0 will not change.

b.

The required return on a stock with beta > 1.0 will increase.

Chapter 08: Risk and Rates of Return

c.

The return on “the market” will remain constant.

d.

The return on “the market” will increase.

e.

The required return on a stock with a positive beta < 1.0 will decline.

8-4 The Relationship Between Risk and Rates of Return

Multiple Choice

FOFM.BRIG.17.08.04 – The Relationship Between Risk and Rates of Return

United States – BUSPROG.FOFM.BRIG.17.03 – BUSPROG: Analytic

United States – OH – DISC.FOFM.BRIG.17.07 – Risk and return

Bloom’s: Comprehension

6/23/2015 3:25 PM

6/23/2015 3:25 PM

100. Which of the following statements is CORRECT?

a.

The slope of the SML is determined by the value of beta.

b.

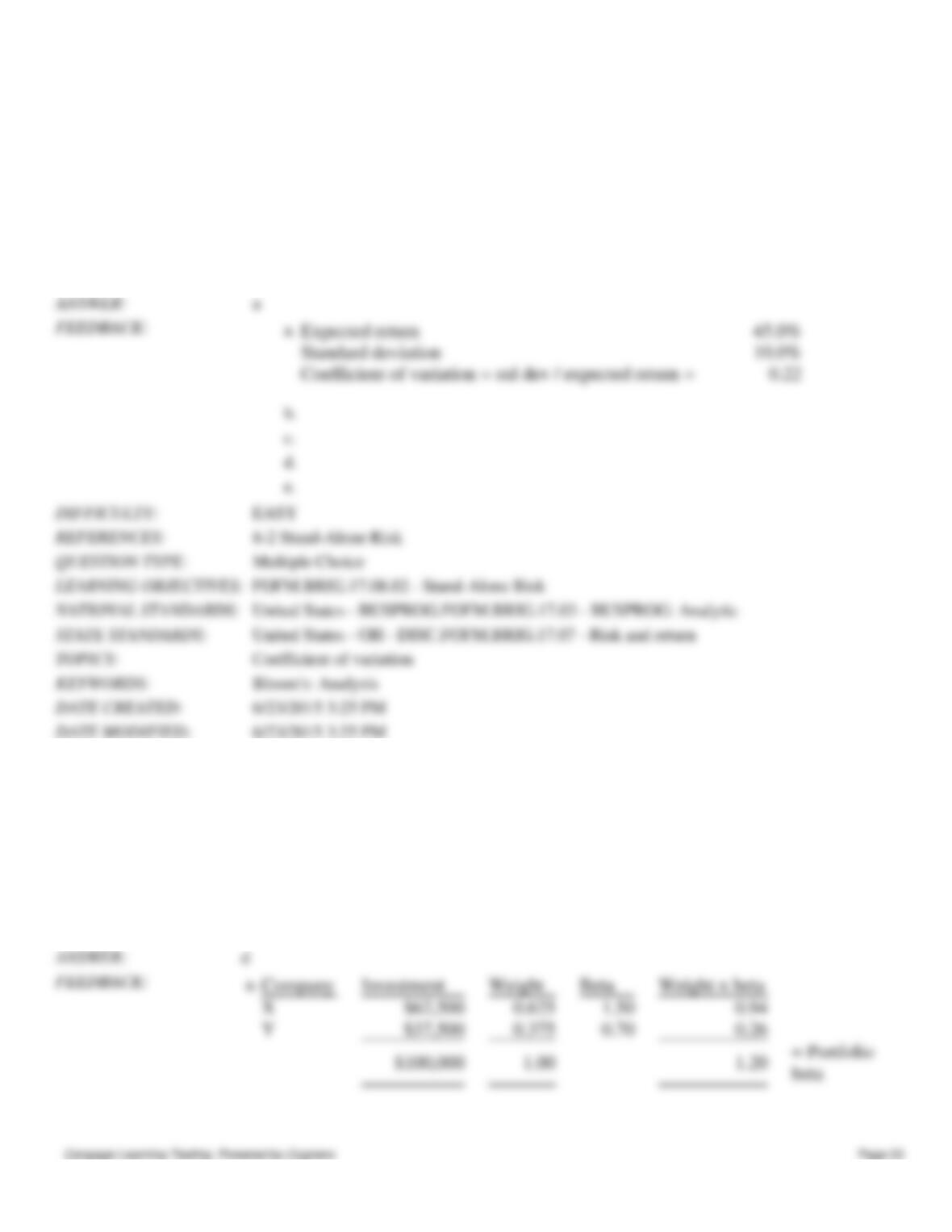

The SML shows the relationship between companies’ required returns and their diversifiable risks. The slope

and intercept of this line cannot be influenced by a firm’s managers, but the position of the company on the

line can be influenced by its managers.

c.

Suppose you plotted the returns of a given stock against those of the market, and you found that the slope of

the regression line was negative. The CAPM would indicate that the required rate of return on the stock should

be less than the risk-free rate for a well diversified investor, assuming investors expect the observed

relationship to continue on into the future.

d.

If investors become less risk averse, the slope of the Security Market Line will increase.

e.

If a company increases its use of debt, this is likely to cause the slope of its SML to increase, indicating a

higher required return on the stock.

8-4 The Relationship Between Risk and Rates of Return

Multiple Choice

FOFM.BRIG.17.08.04 – The Relationship Between Risk and Rates of Return

United States – BUSPROG.FOFM.BRIG.17.03 – BUSPROG: Analytic

United States – OH – DISC.FOFM.BRIG.17.07 – Risk and return

Bloom’s: Comprehension

6/23/2015 3:25 PM

8/13/2015 1:27 PM

101. Other things held constant, if the expected inflation rate decreases and investors also become more risk averse, the

Security Market Line would be affected as follows:

a.

The y-axis intercept would decline, and the slope would increase.

b.

The x-axis intercept would decline, and the slope would increase.

c.

The y-axis intercept would increase, and the slope would decline.

Chapter 08: Risk and Rates of Return

d.

The SML would be affected only if betas changed.

e.

Both the y-axis intercept and the slope would increase, leading to higher required returns.

8-4 The Relationship Between Risk and Rates of Return

Multiple Choice

FOFM.BRIG.17.08.04 – The Relationship Between Risk and Rates of Return

United States – BUSPROG.FOFM.BRIG.17.03 – BUSPROG: Analytic

United States – OH – DISC.FOFM.BRIG.17.07 – Risk and return

Bloom’s: Comprehension

6/23/2015 3:25 PM

6/23/2015 3:25 PM

102. Assume that the risk-free rate, rRF, increases but the market risk premium, (rM – rRF), declines with the net effect

being that the overall required return on the market, rM, remains constant. Which of the following statements is

CORRECT?

a.

The required return of all stocks will increase by the amount of the increase in the risk-free rate.

b.

The required return will decline for stocks that have a beta less than 1.0 but will increase for stocks that have a

beta greater than 1.0.

c.

Since the overall return on the market stays constant, the required return on each individual stock will also

remain constant.

d.

The required return will increase for stocks that have a beta less than 1.0 but decline for stocks that have a beta

greater than 1.0.

e.

The required return of all stocks will fall by the amount of the decline in the market risk premium.

8-4 The Relationship Between Risk and Rates of Return

Multiple Choice

FOFM.BRIG.17.08.04 – The Relationship Between Risk and Rates of Return

United States – BUSPROG.FOFM.BRIG.17.03 – BUSPROG: Analytic

United States – OH – DISC.FOFM.BRIG.17.07 – Risk and return

Bloom’s: Comprehension

6/23/2015 3:25 PM

6/23/2015 3:25 PM

103. Assume that to cool off the economy and decrease expectations for inflation, the Federal Reserve tightened the

money supply, causing an increase in the risk-free rate, rRF. Investors also became concerned that the Fed’s actions would

lead to a recession, and that led to an increase in the market risk premium, (rM – rRF). Under these conditions, with other

things held constant, which of the following statements is most correct?

a.

The required return on all stocks would increase by the same amount.

b.

The required return on all stocks would increase, but the increase would be greatest for stocks with betas of

less than 1.0.

c.

Stocks’ required returns would change, but so would expected returns, and the result would be no change in

Chapter 08: Risk and Rates of Return

stocks’ prices.

d.

The prices of all stocks would decline, but the decline would be greatest for high-beta stocks.

e.

The prices of all stocks would increase, but the increase would be greatest for high-beta stocks.

8-4 The Relationship Between Risk and Rates of Return

Multiple Choice

FOFM.BRIG.17.08.04 – The Relationship Between Risk and Rates of Return

United States – BUSPROG.FOFM.BRIG.17.03 – BUSPROG: Analytic

United States – OH – DISC.FOFM.BRIG.17.07 – Risk and return

Bloom’s: Application

6/23/2015 3:25 PM

6/23/2015 3:25 PM

104. Which of the following statements is CORRECT?

a.

If a stock has a beta of to 1.0, its required rate of return will be unaffected by changes in the market risk

premium.

b.

The slope of the Security Market Line is beta.

c.

Any stock with a negative beta must in theory have a negative required rate of return, provided rRF is positive.

d.

If a stock’s beta doubles, its required rate of return must also double.

e.

If a stock’s returns are negatively correlated with returns on most other stocks, the stock’s beta will be

negative.

8-4 The Relationship Between Risk and Rates of Return

Multiple Choice

FOFM.BRIG.17.08.04 – The Relationship Between Risk and Rates of Return

United States – BUSPROG.FOFM.BRIG.17.03 – BUSPROG: Analytic

United States – OH – DISC.FOFM.BRIG.17.07 – Risk and return

Bloom’s: Comprehension

6/23/2015 3:25 PM

6/23/2015 3:25 PM

105. Assume that investors have recently become more risk averse, so the market risk premium has increased. Also,

assume that the risk-free rate and expected inflation have not changed. Which of the following is most likely to occur?

a.

The required rate of return for an average stock will increase by an amount equal to the increase in the market

risk premium.

b.

The required rate of return will decline for stocks whose betas are less than 1.0.

c.

The required rate of return on the market, rM, will not change as a result of these changes.

d.

The required rate of return for each individual stock in the market will increase by an amount equal to the

increase in the market risk premium.

e.

The required rate of return on a riskless bond will decline.

Chapter 08: Risk and Rates of Return

8-4 The Relationship Between Risk and Rates of Return

Multiple Choice

FOFM.BRIG.17.08.04 – The Relationship Between Risk and Rates of Return

United States – BUSPROG.FOFM.BRIG.17.03 – BUSPROG: Analytic

United States – OH – DISC.FOFM.BRIG.17.07 – Risk and return

Bloom’s: Application

6/23/2015 3:25 PM

6/23/2015 3:25 PM

106. Which of the following statements is CORRECT?

a.

A graph of the SML as applied to individual stocks would show required rates of return on the vertical axis

and standard deviations of returns on the horizontal axis.

b.

The CAPM has been thoroughly tested, and the theory has been confirmed beyond any reasonable doubt.

c.

If two “normal” or “typical” stocks were combined to form a 2-stock portfolio, the portfolio’s expected return

would be a weighted average of the stocks’ expected returns, but the portfolio’s standard deviation would

probably be greater than the average of the stocks’ standard deviations.

d.

If investors become more risk averse, then (1) the slope of the SML would increase and (2) the required rate of

return on low-beta stocks would increase by more than the required return on high-beta stocks.

e.

An increase in expected inflation, combined with a constant real risk-free rate and a constant market risk

premium, would lead to identical increases in the required returns on a riskless asset and on an average stock,

other things held constant.

8-4 The Relationship Between Risk and Rates of Return

Multiple Choice

FOFM.BRIG.17.08.04 – The Relationship Between Risk and Rates of Return

United States – BUSPROG.FOFM.BRIG.17.03 – BUSPROG: Analytic

United States – OH – DISC.FOFM.BRIG.17.07 – Risk and return

Bloom’s: Comprehension

6/23/2015 3:25 PM

6/23/2015 3:25 PM

107. For markets to be in equilibrium, that is, for there to be no strong pressure for prices to depart from their current

levels,

a.

The expected rate of return must be equal to the required rate of return; that is, = .

b.

The past realized rate of return must be equal to the expected future rate of return; that is, = .

c.

The required rate of return must equal the past realized rate of return; that is, = .

d.

All three of the above statements must hold for equilibrium to exist; that is = = .

e.

None of the above statements is correct.

Chapter 08: Risk and Rates of Return

108. Which of the following statements is CORRECT?

a.

When diversifiable risk has been diversified away, the inherent risk that remains is market risk, which is

constant for all stocks in the market.

b.

Portfolio diversification reduces the variability of returns on an individual stock.

c.

Risk refers to the chance that some unfavorable event will occur, and a probability distribution is completely

described by a listing of the likelihoods of unfavorable events.

d.

The SML relates a stock’s required return to its market risk. The slope and intercept of this line cannot be

controlled by the firms’ managers, but managers can influence their firms’ positions on the line by such actions

as changing the firm’s capital structure or the type of assets it employs.

e.

A stock with a beta of -1.0 has zero market risk if held in a 1-stock portfolio.

Multiple Choice

FOFM.BRIG.17.08.00 – Comprehensive

United States – BUSPROG.FOFM.BRIG.17.03 – BUSPROG: Analytic

United States – OH – DISC.FOFM.BRIG.17.07 – Risk and return

Risk concepts

Bloom’s: Comprehension

6/23/2015 3:25 PM

6/23/2015 3:25 PM

109. You observe the following information regarding Companies X and Y:

—Company X has a higher expected return than Company Y.

—Company X has a lower standard deviation of returns than Company Y.

—Company X has a higher beta than Company Y.

Given this information, which of the following statements is CORRECT?

a.

Company X has more diversifiable risk than Company Y.

b.

Company X has a lower coefficient of variation than Company Y.

c.

Company X has less market risk than Company Y.

d.

Company X’s returns will be negative when Y’s returns are positive.

e.

Company X’s stock is a better buy than Company Y’s stock.

8-4 The Relationship Between Risk and Rates of Return

Multiple Choice

FOFM.BRIG.17.08.04 – The Relationship Between Risk and Rates of Return

United States – BUSPROG.FOFM.BRIG.17.03 – BUSPROG: Analytic

United States – OH – DISC.FOFM.BRIG.17.07 – Risk and return

Market equilibrium

Bloom’s: Comprehension

6/23/2015 3:25 PM

8/13/2015 1:42 PM

Chapter 08: Risk and Rates of Return

110. Stocks A and B both have an expected return of 10% and a standard deviation of returns of 25%. Stock A has a beta

of 0.8 and Stock B has a beta of 1.2. The correlation coefficient, r, between the two stocks is +0.6. Portfolio P has 50%

invested in Stock A and 50% invested in B. Which of the following statements is CORRECT?

a.

Portfolio P has a standard deviation of 25% and a beta of 1.0.

b.

Based on the information we are given, and assuming those are the views of the marginal investor, it is

apparent that the two stocks are in equilibrium.

c.

Portfolio P has more market risk than Stock A but less market risk than B.

d.

Stock A should have a higher expected return than Stock B as viewed by the marginal investor.

e.

Portfolio P has a coefficient of variation equal to 2.5.

8-3 Risk in a Portfolio Context: The CAPM

Multiple Choice

FOFM.BRIG.17.08.03 – Risk in a Portfolio Context: The CAPM

United States – BUSPROG.FOFM.BRIG.17.03 – BUSPROG: Analytic

United States – OH – DISC.FOFM.BRIG.17.07 – Risk and return

Portfolio risk

Bloom’s: Analysis

6/23/2015 3:25 PM

6/23/2015 3:25 PM

111. The risk-free rate is 6% and the market risk premium is 5%. Your $1 million portfolio consists of $700,000 invested

in a stock that has a beta of 1.2 and $300,000 invested in a stock that has a beta of 0.8. Which of the following statements

is CORRECT?

a.

If the stock market is efficient, your portfolio’s expected return should equal the expected return on the market,

which is 11%.

b.

The required return on the market is 10%.

c.

The portfolio’s required return is less than 11%.

d.

If the risk-free rate remains unchanged but the market risk premium increases by 2%, your portfolio’s required

return will increase by more than 2%.

e.

If the market risk premium remains unchanged but expected inflation increases by 2%, your portfolio’s

required return will increase by more than 2%.

d is correct. The portfolio’s beta is 1.08. Therefore, if the market risk premium increases by

Multiple Choice

FOFM.BRIG.17.08.00 – Comprehensive

United States – BUSPROG.FOFM.BRIG.17.03 – BUSPROG: Analytic

United States – OH – DISC.FOFM.BRIG.17.07 – Risk and return

Risk measures

Bloom’s: Evaluation

6/23/2015 3:25 PM

6/23/2015 3:25 PM

Chapter 08: Risk and Rates of Return

112. Stock A has an expected return of 10% and a standard deviation of 20%. Stock B has an expected return of 13% and

a standard deviation of 30%. The risk-free rate is 5% and the market risk premium, rM – rRF, is 6%. Assume that the

market is in equilibrium. Portfolio AB has 50% invested in Stock A and 50% invested in Stock B. The returns of Stock A

and Stock B are independent of one another, i.e., the correlation coefficient between them is zero. Which of the following

statements is CORRECT?

a.

Stock A’s beta is 0.8333.

b.

Since the two stocks have zero correlation, Portfolio AB is riskless.

c.

Stock B’s beta is 1.0000.

d.

Portfolio AB’s required return is 11%.

e.

Portfolio AB’s standard deviation is 25%.

a is correct. Stock A’s required return is 10% = 5% + b(6%), so b = 5%/6% = 0.83333.

8-4 The Relationship Between Risk and Rates of Return

Multiple Choice

FOFM.BRIG.17.08.04 – The Relationship Between Risk and Rates of Return

United States – BUSPROG.FOFM.BRIG.17.03 – BUSPROG: Analytic

United States – OH – DISC.FOFM.BRIG.17.07 – Risk and return

Port. risk and ret. relationships

Bloom’s: Analysis

6/23/2015 3:25 PM

6/23/2015 3:25 PM

113. Stock A has a beta of 1.2 and a standard deviation of 25%. Stock B has a beta of 1.4 and a standard deviation of 20%.

Portfolio AB was created by investing in a combination of Stocks A and B. Portfolio AB has a beta of 1.25 and a standard

deviation of 18%. Which of the following statements is CORRECT?

a.

Stock A has more market risk than Portfolio AB.

b.

Stock A has more market risk than Stock B but less stand-alone risk.

c.

Portfolio AB has more money invested in Stock A than in Stock B.

d.

Portfolio AB has the same amount of money invested in each of the two stocks.

e.

Portfolio AB has more money invested in Stock B than in Stock A.

2.0% the portfolio’s required return will increase by 2.16%

8-4 The Relationship Between Risk and Rates of Return

Multiple Choice

FOFM.BRIG.17.08.04 – The Relationship Between Risk and Rates of Return

United States – BUSPROG.FOFM.BRIG.17.03 – BUSPROG: Analytic

United States – OH – DISC.FOFM.BRIG.17.07 – Risk and return

Port. risk and ret. relationships

Bloom’s: Analysis

6/23/2015 3:25 PM

6/23/2015 3:25 PM

Chapter 08: Risk and Rates of Return

114. Which of the following statements is CORRECT?

a.

If Mutual Fund A held equal amounts of 100 stocks, each of which had a beta of 1.0, and Mutual Fund B held

equal amounts of 10 stocks with betas of 1.0, then the two mutual funds would both have betas of 1.0. Thus,

they would be equally risky from an investor’s standpoint, assuming the investor’s only asset is one or the other

of the mutual funds.

b.

If investors become more risk averse but rRF does not change, then the required rate of return on high-beta

stocks will rise and the required return on low-beta stocks will decline, but the required return on an average-

risk stock will not change.

c.

An investor who holds just one stock will generally be exposed to more risk than an investor who holds a

portfolio of stocks, assuming the stocks are all equally risky. Since the holder of the 1-stock portfolio is

exposed to more risk, he or she can expect to earn a higher rate of return to compensate for the greater risk.

d.

There is no reason to think that the slope of the yield curve would have any effect on the slope of the SML.

e.

Assume that the required rate of return on the market, rM, is given and fixed at 10%. If the yield curve were

upward sloping, then the Security Market Line (SML) would have a steeper slope if 1-year Treasury securities

were used as the risk-free rate than if 30-year Treasury bonds were used for rRF.

e

CHALLENGING

8-4 The Relationship Between Risk and Rates of Return

Multiple Choice

FOFM.BRIG.17.08.04 – The Relationship Between Risk and Rates of Return

United States – BUSPROG.FOFM.BRIG.17.03 – BUSPROG: Analytic

United States – OH – DISC.FOFM.BRIG.17.07 – Risk and return

Bloom’s: Analysis

6/23/2015 3:25 PM

6/23/2015 3:25 PM

115. Taggart Inc.’s stock has a 50% chance of producing a 36% return, a 30% chance of producing a 10% return, and a

20% chance of producing a –28% return. What is the firm’s expected rate of return? Do not round your intermediate

calculations.

a.

15.86%

= 0.5(1.2) + 0.5(1.4) = 1.3. But < 1.3, so more money must be invested in the low-beta

CHALLENGING

8-4 The Relationship Between Risk and Rates of Return

Multiple Choice

FOFM.BRIG.17.08.04 – The Relationship Between Risk and Rates of Return

United States – BUSPROG.FOFM.BRIG.17.03 – BUSPROG: Analytic

United States – OH – DISC.FOFM.BRIG.17.07 – Risk and return

Port. risk and ret. relationships

Bloom’s: Analysis

6/23/2015 3:25 PM

6/23/2015 3:25 PM

Chapter 08: Risk and Rates of Return

b.

15.71%

c.

15.40%

d.

12.01%

e.

14.01%

c

b.

c.

d.

e.

EASY

116. Dothan Inc.’s stock has a 25% chance of producing a 16% return, a 50% chance of producing a 12% return, and a

25% chance of producing a –18% return. What is the firm’s expected rate of return? Do not round your intermediate

calculations.

a.

4.51%

b.

5.50%

c.

4.68%

d.

4.29%

e.

6.38%

Chapter 08: Risk and Rates of Return

b.

c.

d.

e.

EASY

117. Cheng Inc. is considering a capital budgeting project that has an expected return of 24% and a standard deviation of

30%. What is the project’s coefficient of variation? Do not round your intermediate calculations. Round the final answer

to 2 decimal places.

a.

1.08

b.

1.40

c.

1.03

d.

1.25

e.

0.99

b.

c.

d.

e.

EASY

Chapter 08: Risk and Rates of Return

118. Bae Inc. is considering an investment that has an expected return of 45% and a standard deviation of 10%. What is

the investment’s coefficient of variation? Do not round your intermediate calculations. Round the final answer to 2

decimal places.

a.

0.22

b.

0.27

c.

0.20

d.

0.26

e.

0.23

a

b.

c.

d.

e.

EASY

119. Bill Dukes has $100,000 invested in a 2-stock portfolio. $62,500 is invested in Stock X and the remainder is invested

in Stock Y. X’s beta is 1.50 and Y’s beta is 0.70. What is the portfolio’s beta? Do not round your intermediate

calculations. Round the final answer to 2 decimal places.

a.

1.14

b.

0.90

c.

1.44

d.

1.20

e.

1.56

Chapter 08: Risk and Rates of Return

120. Tom O’Brien has a 2-stock portfolio with a total value of $100,000. $47,500 is invested in Stock A with a beta of

0.75 and the remainder is invested in Stock B with a beta of 1.42. What is his portfolio’s beta? Do not round your

intermediate calculations. Round your final answer to 2 decimal places.

a.

1.04

b.

1.10

c.

1.09

d.

1.06

e.

1.05

EASY

Chapter 08: Risk and Rates of Return

121. Assume that you hold a well-diversified portfolio that has an expected return of 11.0% and a beta of 1.20. You are in

the process of buying 1,000 shares of Alpha Corp at $10 a share and adding it to your portfolio. Alpha has an expected

return of 21.5% and a beta of 1.70. The total value of your current portfolio is $90,000. What will the expected return and

beta on the portfolio be after the purchase of the Alpha stock? Do not round your intermediate calculations.

a.

13.98%; 1.28

b.

12.29%; 1.48

c.

12.41%; 1.56

d.

12.05%; 1.25

e.

9.40%; 1.34

b.

c.

d.

e.

8-3 Risk in a Portfolio Context: The CAPM

Multiple Choice

FOFM.BRIG.17.08.03 – Risk in a Portfolio Context: The CAPM

United States – BUSPROG.FOFM.BRIG.17.03 – BUSPROG: Analytic

United States – OH – DISC.FOFM.BRIG.17.07 – Risk and return

Portfolio beta

8-3 Risk in a Portfolio Context: The CAPM

Multiple Choice

United States – OH – DISC.FOFM.BRIG.17.07 – Risk and return

Portfolio beta

Bloom’s: Analysis

6/23/2015 3:25 PM

6/23/2015 3:25 PM

Chapter 08: Risk and Rates of Return

122. Calculate the required rate of return for Climax Inc., assuming that (1) investors expect a 4.0% rate of inflation in the

future, (2) the real risk-free rate is 3.0%, (3) the market risk premium is 5.0%, (4) the firm has a beta of 2.30, and (5) its

realized rate of return has averaged 15.0% over the last 5 years. Do not round your intermediate calculations.

a.

20.91%

b.

18.87%

c.

16.28%

d.

17.76%

e.

18.50%

e

b.

c.

d.

e.

EASY

123. Cooley Company’s stock has a beta of 1.28, the risk-free rate is 2.25%, and the market risk premium is 5.50%. What

is the firm’s required rate of return? Do not round your intermediate calculations.

a.

9.29%

b.

9.94%

c.

10.96%

d.

8.55%

e.

11.52%

a

Chapter 08: Risk and Rates of Return

124. Porter Inc’s stock has an expected return of 12.50%, a beta of 1.25, and is in equilibrium. If the risk-free rate is

2.00%, what is the market risk premium? Do not round your intermediate calculations.

a.

10.50%

b.

8.48%

c.

7.98%

d.

8.40%

e.

6.80%

b.

c.

d.

e.

EASY

c.

d.

e.

EASY

Chapter 08: Risk and Rates of Return

125. Roenfeld Corp believes the following probability distribution exists for its stock. What is the coefficient of variation

on the company’s stock? Do not round your intermediate calculations.

State of

the

Economy

Probability

of State

Occurring

Stock’s

Expected

Return

Boom

0.19

25%

Normal

0.50

15%

Recession

0.31

5%

a.

0.6565

b.

0.6060

c.

0.5050

d.

0.4545

e.

0.4292

c

b

d

MODERATE

Chapter 08: Risk and Rates of Return

126. Jim Angel holds a $200,000 portfolio consisting of the following stocks:

Stock

Investment

Beta

A

$50,000

1.20

B

$50,000

0.80

C

$50,000

1.00

D

$50,000

1.20

Total

$200,000

What is the portfolio’s beta? Do not round your intermediate calculations.

a.

1.239

b.

1.040

c.

0.861

d.

0.809

e.

1.050

e

b.

c.

d.

e.

MODERATE