Chapter 7/Consumers, Producers, and the Efficiency of Markets ❖ 41

Figure 7-7

Supply

1 2 3 4 Quantity

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Price

42. Refer to Figure 7-7. If the price of the good is $9.50, then producer surplus is

a.

$2.50.

b.

$6.50.

c.

$8.00.

d.

$10.00.

43. Refer to Figure 7-7. If the price of the good is $14, then producer surplus is

a.

$17.

b.

$22.

c.

$25.

d.

$28.

44. Refer to Figure 7-7. If producer surplus is $14, then the price of the good is

a.

$11.00.

b.

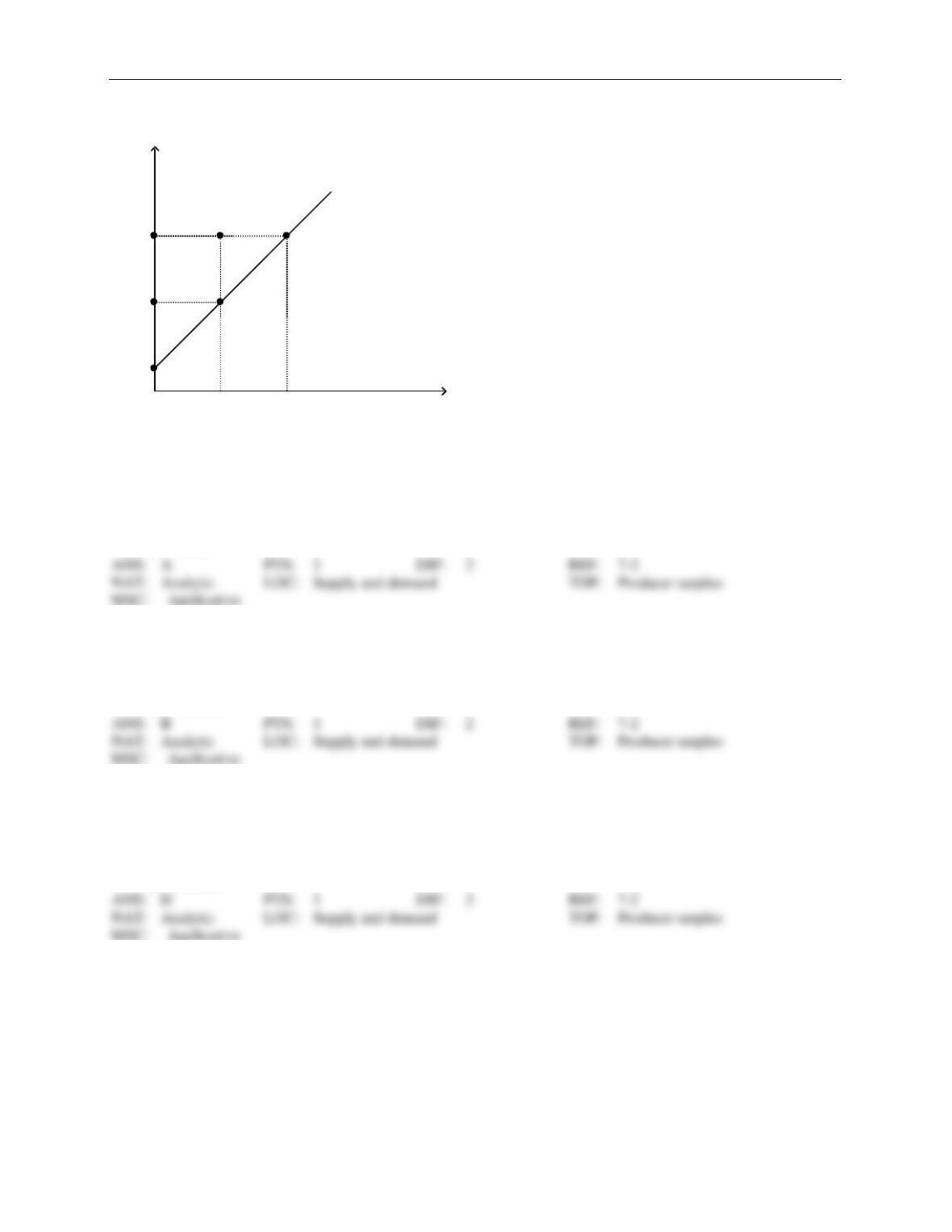

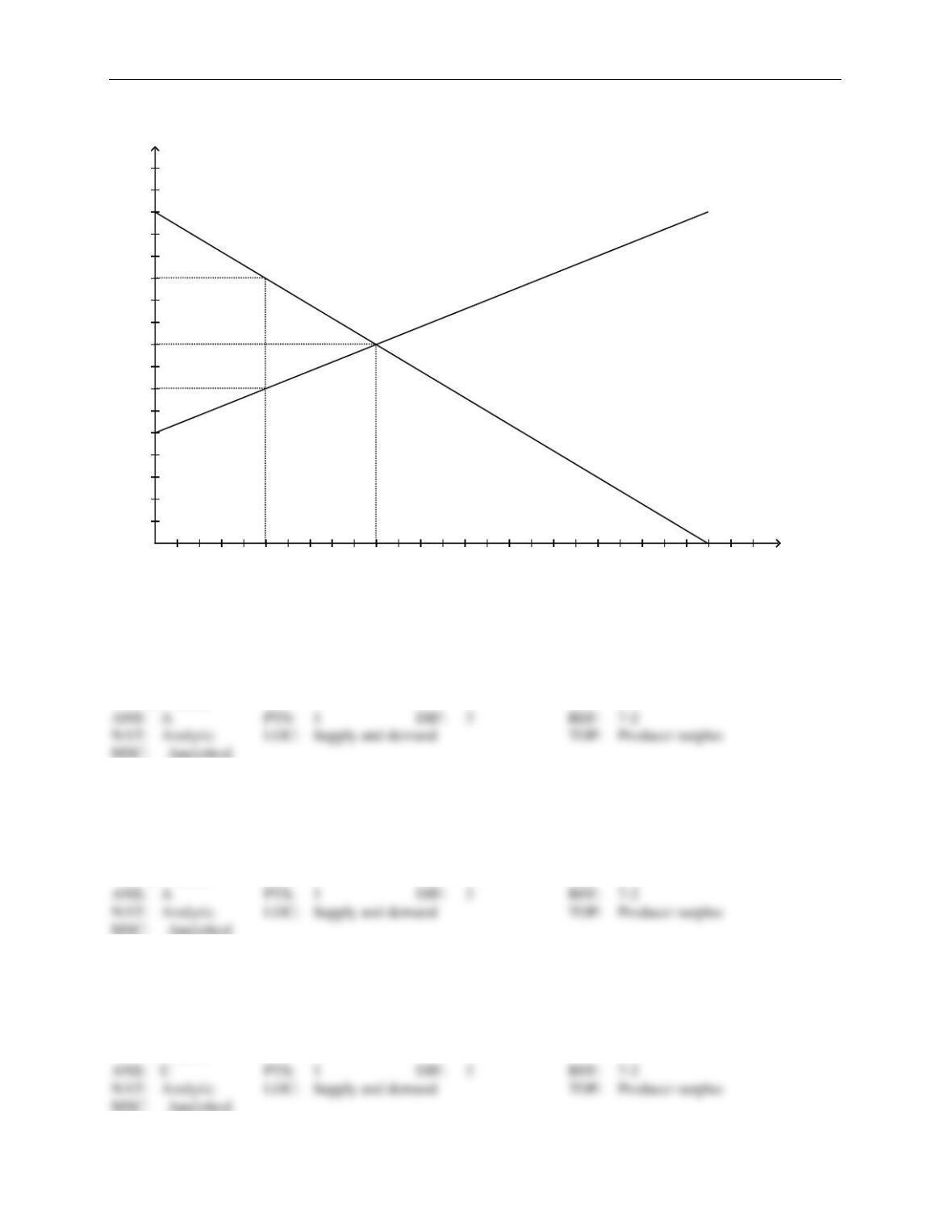

$12.00.

c.

$13.50.

d.

$14.75.

42 ❖ Chapter 7/Consumers, Producers, and the Efficiency of Markets

Figure 7-8

Supply

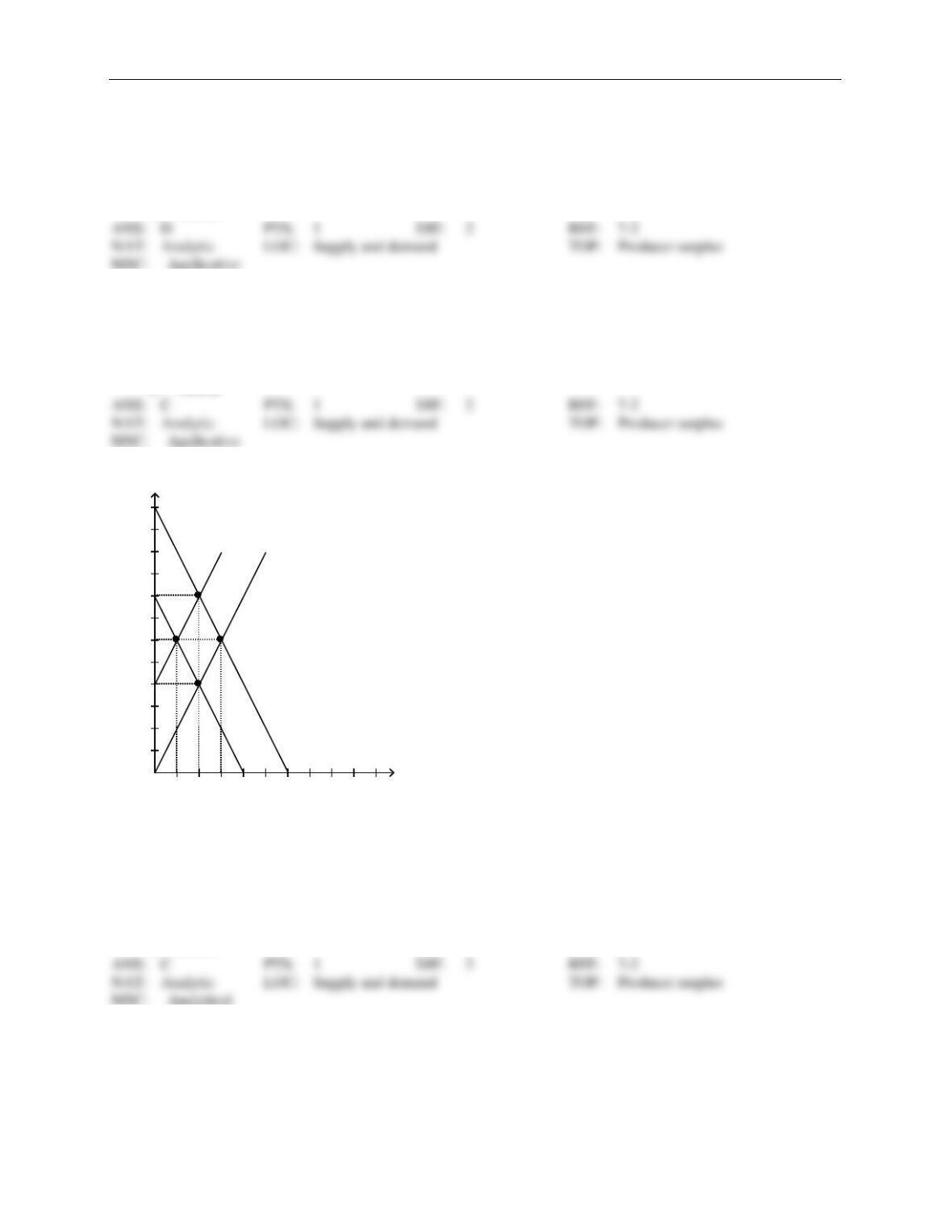

P1

P2

Q1 Q2

A

B

C

D

G

H

Quantity

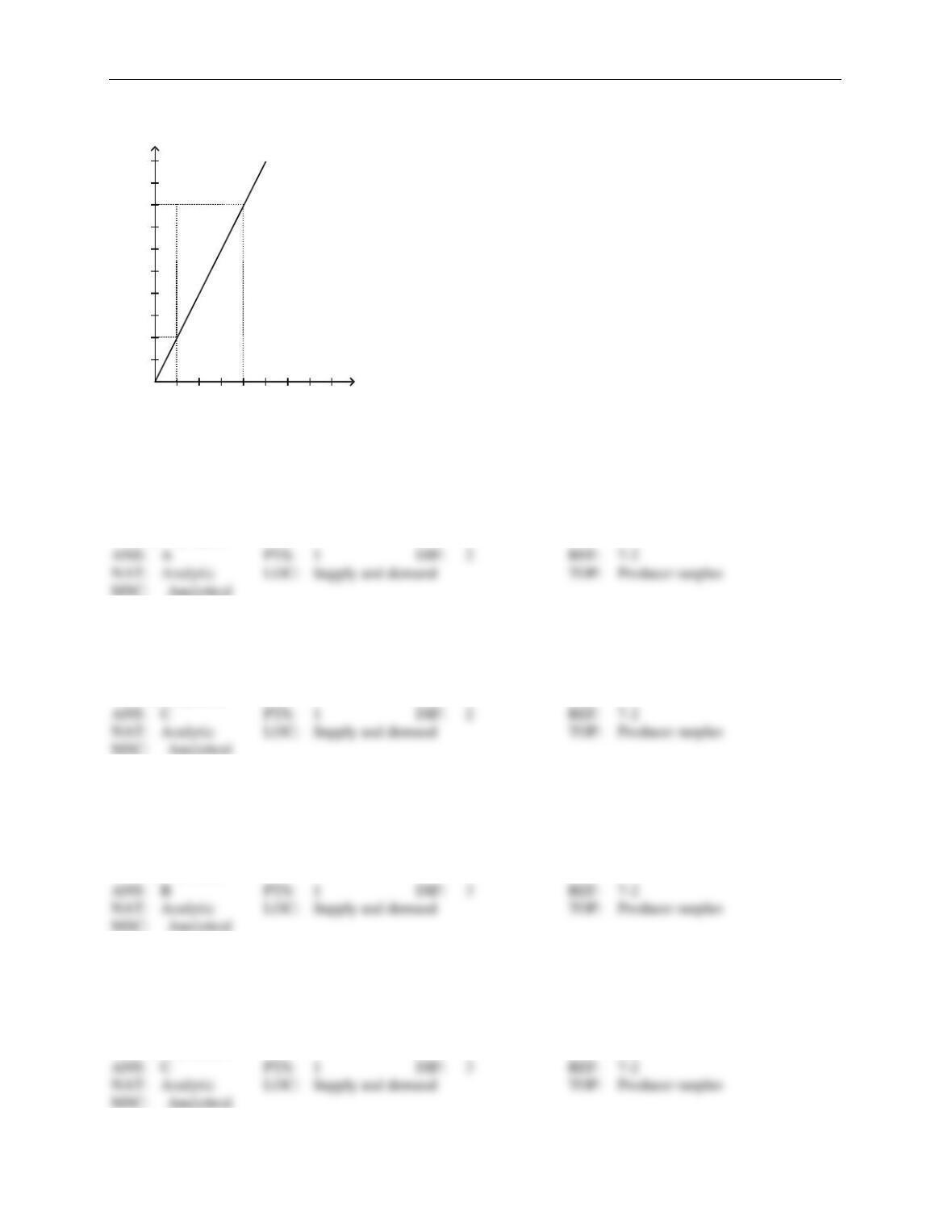

Price

45. Refer to Figure 7-8. Which area represents producer surplus when the price is P1?

a.

BCG

b.

ACH

c.

ABGD

d.

DGH

46. Refer to Figure 7-8. Which area represents producer surplus when the price is P2?

a.

BCG

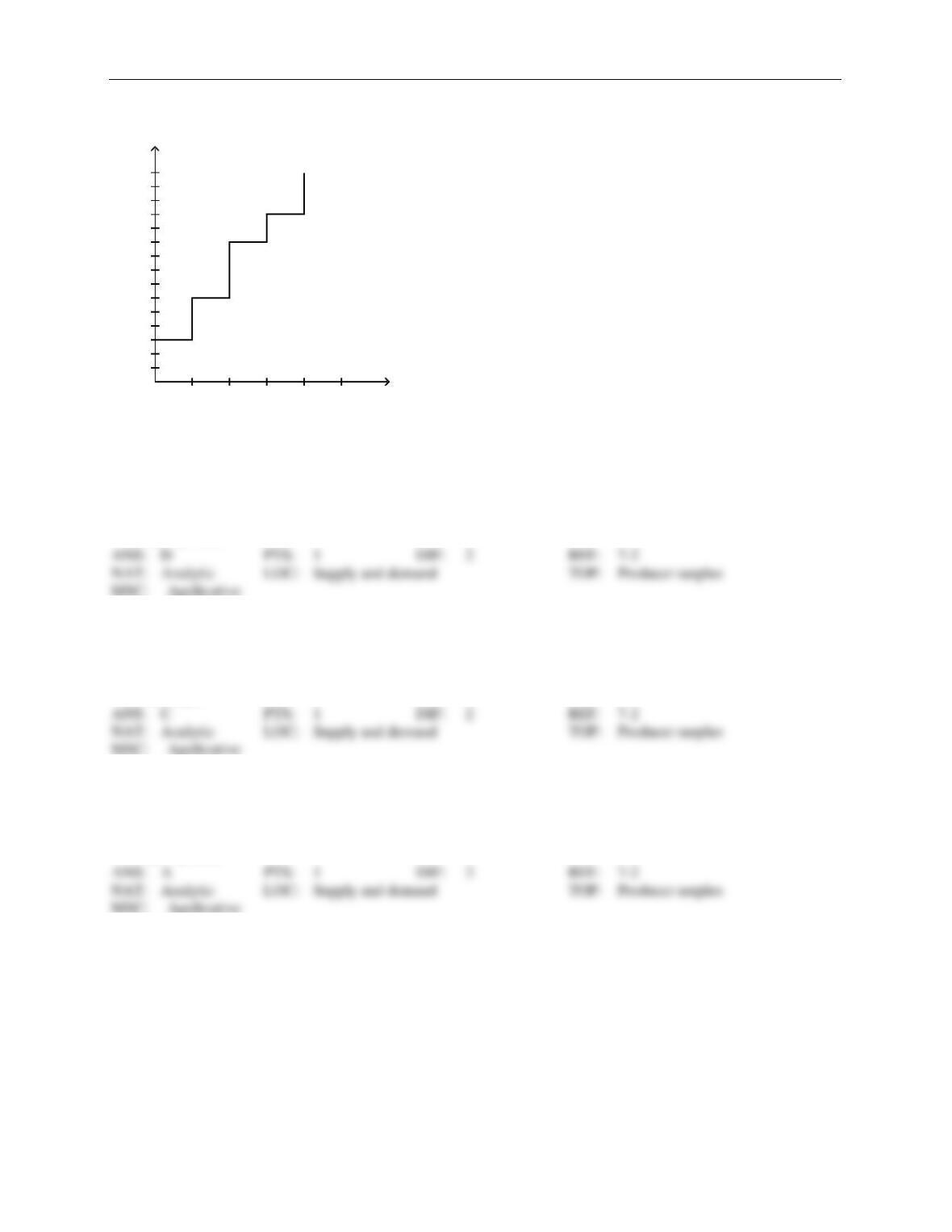

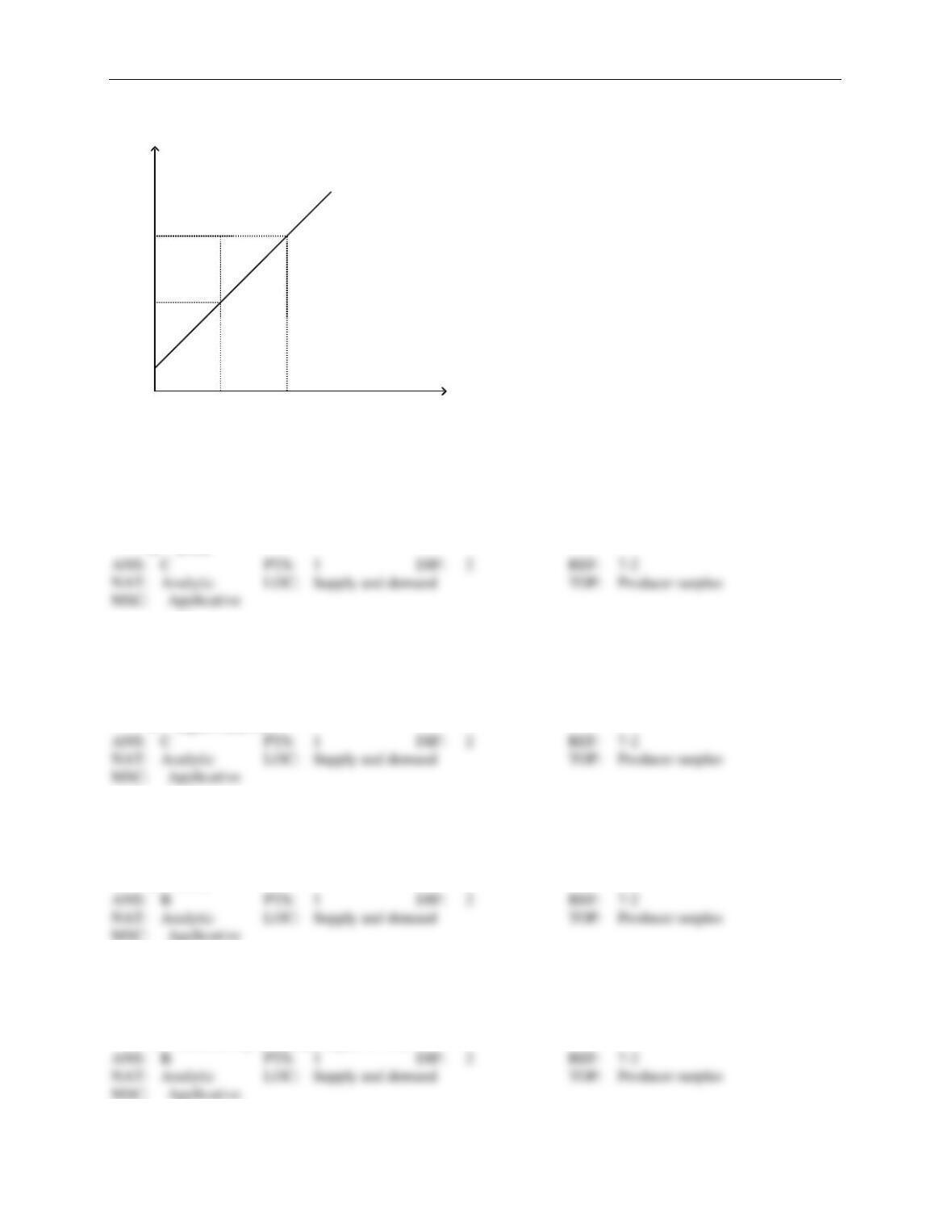

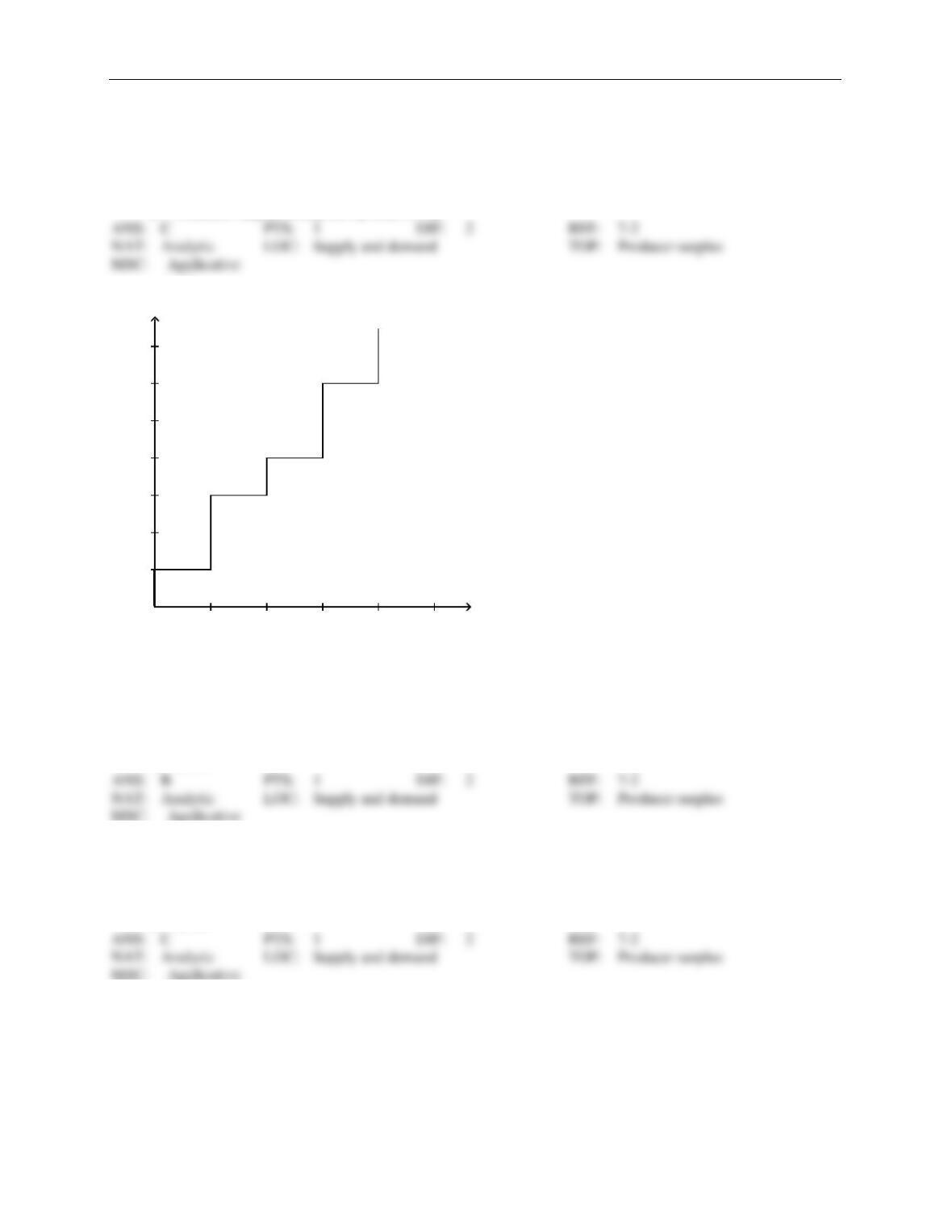

b.

ACH

c.

ABGD

d.

AHGB

47. Refer to Figure 7-8. Which area represents the increase in producer surplus when the price rises from P1 to

P2?

a.

BCG

b.

ACH

c.

ABGD

d.

AHGB

Chapter 7/Consumers, Producers, and the Efficiency of Markets ❖ 43

48. Refer to Figure 7-8. When the price rises from P1 to P2, which area represents the increase in producer sur-

plus to existing producers?

a.

BCG

b.

ACH

c.

DGH

d.

ABGD

49. Refer to Figure 7-8. Which area represents the increase in producer surplus when the price rises from P1 to

P2 due to new producers entering the market?

a.

BCG

b.

ACH

c.

DGH

d.

AHGB

Figure 7-9

D

S’ S

D’

25 50 75 100 125 150 175 200 Quantity

25

50

75

100

125

150

175

200

225

250

275

300 Price

50. Refer to Figure 7-9. If the supply curve is S, the demand curve is D, and the equilibrium price is $100, what

is the producer surplus?

a.

$625

b.

$1,250

c.

$2,500

d.

$5,000

44 ❖ Chapter 7/Consumers, Producers, and the Efficiency of Markets

51. Refer to Figure 7-9. If the supply curve is S’, the demand curve is D, and the equilibrium price is $150, what

is the producer surplus?

a.

$625

b.

$1,250

c.

$2,500

d.

$5,000

52. Refer to Figure 7-9. If the demand curve is D and the supply curve shifts from S’ to S, what is the change in

producer surplus?

a.

Producer surplus increases by $625.

b.

Producer surplus increases by $1,875.

c.

Producer surplus decreases by $625.

d.

Producer surplus decreases by $1,875.

53. Refer to Figure 7-9. If the supply curve is S and the demand curve shifts from D to D’, what is the change in

producer surplus?

a.

Producer surplus increases by $3,125.

b.

Producer surplus increases by $5,625.

c.

Producer surplus decreases by $3,125.

d.

Producer surplus decreases by $5,625.

54. Refer to Figure 7-9. If the supply curve is S and the demand curve shifts from D to D’, what is the increase

in producer surplus to existing producers?

a.

$625

b.

$2,500

c.

$3,125

d.

$5,625

55. Refer to Figure 7-9. If the supply curve is S and the demand curve shifts from D to D’, what is the increase

in producer surplus due to new producers entering the market?

a.

$625

b.

$2,500

c.

$3,125

d.

$5,625

Chapter 7/Consumers, Producers, and the Efficiency of Markets ❖ 45

Figure 7-10

S

25 50 75 100 125 150 Quantity

25

50

75

100

125

150

175

200

225

250 Price

56. Refer to Figure 7-10. If the equilibrium price is $50, what is the producer surplus?

a.

$625

b.

$3,750

c.

$5,625

d.

$10,000

57. Refer to Figure 7-10. If the equilibrium price is $200, what is the producer surplus?

a.

$625

b.

$3,750

c.

$10,000

d.

$20,000

58. Refer to Figure 7-10. If the equilibrium price rises from $50 to $200, what is the additional producer surplus

to initial producers?

a.

$625

b.

$3,750

c.

$5,625

d.

$10,000

59. Refer to Figure 7-10. If the equilibrium price rises from $50 to $200, what is the producer surplus to new

producers?

a.

$625

b.

$3,750

c.

$5,625

d.

$10,000

46 ❖ Chapter 7/Consumers, Producers, and the Efficiency of Markets

Figure 7-11

S

D

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 Quantity

10

20

30

40

50

60

70

80

90

100

110

120

130

140

150

160

170

Price

60. Refer to Figure 7-11. At the equilibrium price, producer surplus is

a.

$200.

b.

$400.

c.

$450.

d.

$900.

61. Refer to Figure 7-11. If the government imposes a price ceiling of $70 in this market, then the new producer

surplus will be

a.

$50.

b.

$100.

c.

$175.

d.

$350.

62. Refer to Figure 7-11. If the government imposes a price ceiling of $70 in this market, then producer surplus

will decrease by

a.

$50.

b.

$125.

c.

$150.

d.

$200.

Chapter 7/Consumers, Producers, and the Efficiency of Markets ❖ 47

Figure 7-12

Supply

P1

P2

Q1 Q2

A

C

B

D

G

Quantity

Price

63. Refer to Figure 7-12. When the price is P2, producer surplus is

a.

A.

b.

A+C.

c.

A+B+C.

d.

D+G.

64. Refer to Figure 7-12. Suppose producer surplus is larger than C but smaller than A+B+C. The price of the

good must be

a.

lower than P1.

b.

P1.

c.

between P1 and P2.

d.

higher than P2.

65. Refer to Figure 7-12. When the price is P1, producer surplus is

a.

A.

b.

C.

c.

A+B.

d.

C+D.

66. Refer to Figure 7-12. When the price falls from P2 to P1, producer surplus

a.

decreases by an amount equal to C.

b.

decreases by an amount equal to A+B.

c.

decreases by an amount equal to A+C.

d.

increases by an amount equal to A+B.

48 ❖ Chapter 7/Consumers, Producers, and the Efficiency of Markets

67. Refer to Figure 7-12. When the price rises from P1 to P2, what area represents the increase in producer sur-

plus?

a.

A

b.

A+B

c.

A+B+C

d.

G

68. Refer to Figure 7-12. When the price rises from P1 to P2, which area represents the increase in producer sur-

plus to existing producers?

a.

A

b.

A+B

c.

A+B+C

d.

G

69. Refer to Figure 7-12. When the price rises from P1 to P2, which area represents the increase in producer sur-

plus due to new producers entering the market?

a.

A

b.

B

c.

A+B

d.

G

70. Refer to Figure 7-12. Area A represents

a.

producer surplus to new producers entering the market as the result of an increase in price from P1

to P2.

b.

the increase in consumer surplus that results from an upward-sloping supply curve.

c.

the increase in total surplus when sellers are willing and able to increase supply from Q1 to Q2.

d.

the increase in producer surplus to those producers already in the market when the price increases

from P1 to P2.

71. Refer to Figure 7-12. Area B represents

a.

the combined profits of all producers when the price is P2.

b.

the increase in producer surplus to all producers as the result of an increase in the price from P1 to

P2.

c.

producer surplus to new producers entering the market as the result of an increase in the price from

P1 to P2.

d.

that portion of the increase in producer surplus that is offset by a loss in consumer surplus when the

price increases from P1 to P2.

Chapter 7/Consumers, Producers, and the Efficiency of Markets ❖ 49

72. Refer to Figure 7-12. When the price falls from P2 to P1, which of the following would not be true?

a.

The sellers who still sell the good are worse off because they now receive less.

b.

Some sellers leave the market because they are not willing to sell the good at the lower price.

c.

The total cost of what is now sold by sellers is actually higher than it was before the decrease in the

price.

d.

Producer surplus would fall by area A + B.

Figure 7-13

Supply

1 2 3 4 5 Q

100

200

300

400

500

600

700

P

73. Refer to Figure 7-13. If the price of the good is $300, then producer surplus amounts to

a.

$100.

b.

$200.

c.

$300.

d.

$400.

74. Refer to Figure 7-13. If the price of the good is $500, then producer surplus amounts to

a.

$450.

b.

$575.

c.

$700.

d.

$800.

50 ❖ Chapter 7/Consumers, Producers, and the Efficiency of Markets

75. Refer to Figure 7-13. If the price of the good is $600, then producer surplus amounts to

a.

$650.

b.

$800.

c.

$900.

d.

$1,000.

76. Refer to Figure 7-13. If the price of the good is $600, then

a.

consumer surplus is $800.

b.

consumer surplus is $900.

c.

producer surplus is $900.

d.

producer surplus is $1,000.

77. Refer to Figure 7-13. Suppose the price of the good is $400. Then, on the first unit of the good that is sold,

producer surplus amounts to

a.

$200.

b.

$300.

c.

$400.

d.

$450.

78. Refer to Figure 7-13. Suppose the price of the good is $450. Then, on the first unit of the good that is sold,

producer surplus is

a.

$250, and on the second unit of the good that is sold, producer surplus is $100.

b.

$250, and on the second unit of the good that is sold, producer surplus is $150.

c.

$350, and on the second unit of the good that is sold, producer surplus is $100.

d.

$350, and on the second unit of the good that is sold, producer surplus is $150.

79. Refer to Figure 7-13. Producer surplus amounts to $300 if the price of the good is

a.

$300.

b.

$350.

c.

$400.

d.

$450.

80. Refer to Figure 7-13. Sellers will be unwilling to sell more than

a.

1 unit of the good if its price is below $200.

b.

2 units of the good if its price is below $450.

c.

3 units of the good if its price is below $700.

d.

All of the above are correct.

Chapter 7/Consumers, Producers, and the Efficiency of Markets ❖ 51

81. Producer surplus equals

a.

Value to buyers – Amount paid by buyers.

b.

Amount received by sellers – Costs of sellers.

c.

Value to buyers – Costs of sellers.

d.

Value to buyers – Amount paid by buyers + Amount received by sellers – Costs of sellers.

82. Producer surplus is the

a.

area under the supply curve to the left of the amount sold.

b.

amount a seller is paid minus the cost of production.

c.

area between the supply and demand curves, above the equilibrium price.

d.

cost to sellers of participating in a market.

83. Producer surplus is the area

a.

under the supply curve.

b.

between the supply and demand curves.

c.

below the price and above the supply curve.

d.

under the demand curve and above the price.

84. Producer surplus is

a.

represented on a graph by the area below the demand curve and above the supply curve.

b.

the amount a seller is paid minus the cost of production.

c.

also referred to as excess supply.

d.

All of the above are correct.

85. Producer surplus directly measures

a.

the well-being of society as a whole.

b.

the well-being of buyers and sellers.

c.

the well-being of sellers.

d.

sellers’ willingness to sell.

86. Producer surplus directly measures

a.

the well-being of sellers.

b.

production costs.

c.

excess demand.

d.

unsold inventories.

52 ❖ Chapter 7/Consumers, Producers, and the Efficiency of Markets

87. The marginal seller is the seller who

a.

cannot compete with the other sellers in the market.

b.

would leave the market first if the price were any lower.

c.

can produce at the lowest cost.

d.

has the largest producer surplus.

88. The marginal seller is the seller

a.

for whom the marginal cost of producing one more unit of output is the lowest among all sellers,

and the marginal buyer is the buyer for whom the marginal benefit of one more unit of the good is

the highest among all buyers.

b.

who supplies the smallest quantity of the good among all sellers, and the marginal buyer is the

buyer who demands the smallest quantity of the good among all buyers.

c.

who would leave the market first if the price were any lower, and the marginal buyer is the buyer

who would leave the market first if the price were any higher.

d.

who has the largest producer surplus, and the marginal buyer is the buyer who has the largest

consumer surplus.

89. Another way to think of the marginal seller is the seller who

a.

will accept the lowest price of any seller in the market.

b.

requires the highest price of any potential seller in the market.

c.

would leave the market first if the price were any lower.

d.

would leave the market last if the price falls.

90. Suppose the demand for peanuts increases. What will happen to producer surplus in the market for peanuts?

a.

It increases.

b.

It decreases.

c.

It remains unchanged.

d.

It may increase, decrease, or remain unchanged.

91. Suppose the demand for peaches decreases. What will happen to producer surplus in the market for peaches?

a.

It increases.

b.

It decreases.

c.

It remains unchanged.

d.

It may increase, decrease, or remain unchanged.

Chapter 7/Consumers, Producers, and the Efficiency of Markets ❖ 53

92. Which of the following will cause an increase in producer surplus?

a.

the imposition of a binding price ceiling in the market

b.

buyers expect the price of the good to be lower next month

c.

the price of a substitute increases

d.

income increases and buyers consider the good to be inferior

93. If the demand for leather decreases, producer surplus in the leather market

a.

increases.

b.

decreases.

c.

remains the same.

d.

may increase, decrease, or remain the same.

94. If the demand for light bulbs increases, producer surplus in the market for light bulbs

a.

increases.

b.

decreases.

c.

remains the same.

d.

may increase, decrease, or remain the same.

95. The Surgeon General announces that eating chocolate increases tooth decay. As a result, the equilibrium price

of chocolate

a.

increases, and producer surplus increases.

b.

increases, and producer surplus decreases.

c.

decreases, and producer surplus increases.

d.

decreases, and producer surplus decreases.

96. Suppose consumer income increases. If grass seed is a normal good, the equilibrium price of grass seed will

a.

decrease, and producer surplus in the industry will decrease.

b.

increase, and producer surplus in the industry will increase.

c.

decrease, and producer surplus in the industry will increase.

d.

increase, and producer surplus in the industry will decrease.

97. Which of the following statements is not correct?

a.

A seller would be eager to sell her product at a price higher than her cost.

b.

A seller would refuse to sell her product at a price lower than her cost.

c.

A seller would be indifferent about selling her product at a price equal to her cost.

d.

Since sellers cannot set the price for their product, they must be willing to sell their product at any

price.

54 ❖ Chapter 7/Consumers, Producers, and the Efficiency of Markets

98. Which of the following events would increase producer surplus?

a.

Sellers’ costs stay the same and the price of the good increases.

b.

Sellers’ costs increase and the price of the good stays the same.

c.

Sellers’ costs increase and the price of the good decreases.

d.

All of the above are correct.

99. Which of the following will cause a decrease in producer surplus?

a.

the imposition of a binding price ceiling in the market

b.

an increase in the number of buyers of the good

c.

income increases and buyers consider the good to be normal

d.

the price of a complement decreases

100. ABC Company incurs a cost of 50 cents to produce a dozen eggs, while XYZ Company incurs a cost of 70

cents to produce a dozen eggs. Which of the following price increases would cause both companies to experi-

ence an increase in producer surplus?

a.

The price of a dozen eggs increases from 40 cents to 55 cents.

b.

The price of a dozen eggs increases from 55 cents to 70 cents.

c.

The price of a dozen eggs increases from 55 cents to 75 cents.

d.

All of these price increases would cause both companies to experience a loss in producer surplus.

101. The welfare of sellers is measured by

a.

consumer surplus.

b.

producer surplus.

c.

total surplus.

d.

price.

102. The Surgeon General announces that eating apples promotes healthy teeth. As a result, the equilibrium price of

apples

a.

increases, and producer surplus increases.

b.

increases, and producer surplus decreases.

c.

decreases, and producer surplus increases.

d.

decreases, and producer surplus decreases.

103. Kristi and Rebecca sell lemonade on the corner. It costs them 7 cents to make each cup. On a certain day, they

sell 40 cups. Their producer surplus for that day amounts to $19.20. Kristi & Rebecca sold each cup for

a.

31 cents.

b.

38 cents.

c.

45 cents.

d.

55 cents.

Chapter 7/Consumers, Producers, and the Efficiency of Markets ❖ 55

104. Bill created a new software program he is willing to sell for $200. He sells his first copy and enjoys a producer

surplus of $150. What is the price paid for the software?

a.

$50.

b.

$150.

c.

$200.

d.

$350.

105. Bill created a new software program he is willing to sell for $300. He sells his first copy and enjoys a producer

surplus of $250. What is the price paid for the software?

a.

$50.

b.

$250.

c.

$300.

d.

$550.

106. Donald produces nails at a cost of $350 per ton. If he sells the nails for $500 per ton, his producer surplus is

a.

$150.

b.

$350.

c.

$500.

d.

$850.

107. At Nick’s Bakery, the cost to make homemade chocolate cake is $4 per cake. As a result of selling five cakes,

Nick experiences a producer surplus in the amount of $17.50. Nick must be selling his cakes for

a.

$6.50 each.

b.

$7.50 each.

c.

$9.50 each.

d.

$10.50 each.

108. Which of the following will cause a decrease in producer surplus?

a.

the imposition of a nonbinding price ceiling in the market

b.

buyers expect the price of a good to be higher next month

c.

the price of a substitute increases

d.

income increases and buyers consider the good to be inferior

109. Which of the following will cause no change in producer surplus?

a.

the imposition of a nonbinding price ceiling in the market

b.

buyers expect the price of a good to be higher next month

c.

the price of a substitute increases

d.

income increases and buyers consider the good to be inferior

56 ❖ Chapter 7/Consumers, Producers, and the Efficiency of Markets

110. Suppose that the market price for pizzas increases. The increase in producer surplus comes from the benefit of

the higher prices to

a.

only existing sellers who now receive higher prices on the pizzas they were already selling.

b.

only new sellers who enter the market because of the higher prices.

c.

both existing sellers who now receive higher prices on the pizzas they were already selling and new

sellers who enter the market because of the higher prices.

d.

Producer surplus does not increase; it decreases.

MARKET EFFICIENCY

1. Which tools allow economists to determine if the allocation of resources determined by free markets is desira-

ble?

a.

profits and costs to firms

b.

consumer and producer surplus

c.

the equilibrium price and quantity

d.

incomes of and prices paid by buyers

2. Economists typically measure efficiency using

a.

the price paid by buyers.

b.

the quantity supplied by sellers.

c.

total surplus.

d.

profits to firms.

3. Consumer surplus equals the

a.

value to buyers minus the amount paid by buyers.

b.

value to buyers minus the cost to sellers.

c.

amount received by sellers minus the cost to sellers.

d.

amount received by sellers minus the amount paid by buyers.

4. Producer surplus equals the

a.

value to buyers minus the amount paid by buyers.

b.

value to buyers minus the cost to sellers.

c.

amount received by sellers minus the cost to sellers.

d.

amount received by sellers minus the amount paid by buyers.

Chapter 7/Consumers, Producers, and the Efficiency of Markets ❖ 57

5. Total surplus

a.

can be used to measure a market’s efficiency.

b.

is the sum of consumer and producer surplus.

c.

is the to value to buyers minus the cost to sellers.

d.

All of the above are correct.

6. Total surplus is

a.

the total cost to sellers of providing the good minus the total value of the good to buyers.

b.

the total value of the good to buyers minus the cost to sellers of providing the good.

c.

the difference between consumer surplus and sellers’ cost.

d.

always smaller than producer surplus.

7. Total surplus is

a.

equal to producer surplus plus consumer surplus.

b.

equal to the total cost to sellers minus the total value to buyers.

c.

equal to consumers’ willingness to pay plus producers’ cost.

d.

greater than the sum of consumer surplus plus producer surplus.

8. Total surplus is equal to

a.

value to buyers – profit to sellers.

b.

value to buyers – cost to sellers.

c.

consumer surplus x producer surplus.

d.

(consumer surplus + producer surplus) x equilibrium quantity.

9. Total surplus in a market is equal to

a.

value to buyers – amount paid by buyers.

b.

amount received by sellers – costs of sellers.

c.

value to buyers – costs of sellers.

d.

amount received by sellers – amount paid by buyers.

10. Total surplus in a market is equal to

a.

consumer surplus + producer surplus.

b.

value to buyers – amount paid by buyers.

c.

amount received by sellers – costs of sellers.

d.

producer surplus – consumer surplus.

58 ❖ Chapter 7/Consumers, Producers, and the Efficiency of Markets

11. Total surplus is represented by the area

a.

under the demand curve and above the price.

b.

above the supply curve and up to the price.

c.

under the supply curve and up to the price.

d.

between the demand and supply curves up to the point of equilibrium.

12. Which of the following equations is not valid?

a.

Consumer surplus = Value to buyers – Amount paid by buyers

b.

Producer surplus = Amount received by sellers – Cost to sellers

c.

Total surplus = Value to buyers – Amount paid by buyers + Amount received by sellers – Costs of

sellers

d.

Total surplus = Value to sellers – Cost to sellers

13. Which of the following equations is valid?

a.

Consumer surplus = Total surplus – Cost to sellers

b.

Producer surplus = Total surplus – Consumer surplus

c.

Total surplus = Value to buyers – Amount paid by buyers

d.

Total surplus = Amount received by sellers – Cost to sellers

14. Total surplus is represented by the area below the

a.

demand curve and above the price.

b.

price and up to the point of equilibrium.

c.

demand curve and above the supply curve, up to the equilibrium quantity.

d.

demand curve and above the horizontal axis, up to the equilibrium quantity.

15. Which of the following is correct?

a.

Consumer surplus refers to a situation in which there are more buyers than sellers in a market.

b.

Producer surplus refers to a situation in which there are more sellers than buyers in a market.

c.

Total surplus is measured as the area below the demand curve and above the supply curve, up to the

equilibrium quantity.

d.

All of the above are correct.

16. We can say that the allocation of resources is efficient if

a.

producer surplus is maximized.

b.

consumer surplus is maximized.

c.

total surplus is maximized.

d.

sellers’ costs are minimized.

Chapter 7/Consumers, Producers, and the Efficiency of Markets ❖ 59

17. Efficiency in a market is achieved when

a.

a social planner intervenes and sets the quantity of output after evaluating buyers’ willingness to

pay and sellers’ costs.

b.

the sum of producer surplus and consumer surplus is maximized.

c.

all firms are producing the good at the same low cost per unit.

d.

no buyer is willing to pay more than the equilibrium price for any unit of the good.

18. At the equilibrium price of a good, the good will be purchased by those buyers who

a.

value the good more than price.

b.

value the good less than price.

c.

have the money to buy the good.

d.

consider the good a necessity.

19. Which of the following statements is not correct about a market in equilibrium?

a.

The price determines which buyers and which sellers participate in the market.

b.

Those buyers who value the good more than the price choose to buy the good.

c.

Those sellers whose costs are less than the price choose to produce and sell the good.

d.

Consumer surplus will be equal to producer surplus.

20. Efficiency is attained when

a.

total surplus is maximized.

b.

producer surplus is maximized.

c.

all resources are being used.

d.

consumer surplus is maximized and producer surplus is minimized.

21. The distinction between efficiency and equality can be described as follows:

a.

Efficiency refers to maximizing the number of trades among buyers and sellers; equality refers to

maximizing the gains from trade among buyers and sellers.

b.

Efficiency refers to minimizing the price paid by buyers; equality refers to maximizing the gains

from trade among buyers and sellers.

c.

Efficiency refers to maximizing the size of the pie; equality refers to producing a pie of a given size

at the least possible cost.

d.

Efficiency refers to maximizing the size of the pie; equality refers to distributing the pie fairly

among members of society.

60 ❖ Chapter 7/Consumers, Producers, and the Efficiency of Markets

22. If an allocation of resources is efficient, then

a.

consumer surplus is maximized.

b.

producer surplus is maximized.

c.

all potential gains from trade among buyers are sellers are being realized.

d.

the allocation achieves equality as well.

23. Moving production from a high-cost producer to a low-cost producer will

a.

lower total surplus.

b.

raise total surplus.

c.

lower producer surplus.

d.

raise producer surplus but lower consumer surplus.

24. Which of the following is correct?

a.

Efficiency deals with the size of the economic pie, and equality deals with how fairly the pie is

sliced.

b.

Equality can be judged on positive grounds whereas efficiency requires normative judgments.

c.

Efficiency is more difficult to evaluate than equality.

d.

Equality and efficiency are both maximized in a society when total surplus is maximized.

Table 7-11

Price

Quantity

Demanded

Quantity

Supplied

$12.00

0

36

$10.00

3

30

$ 8.00

6

24

$ 6.00

9

18

$ 4.00

12

12

$ 2.00

15

6

$ 0.00

18

0

25. Refer to Table 7-11. The equilibrium price is

a.

$10.00.

b.

$8.00.

c.

$6.00.

d.

$4.00.