Chapter 7/Consumers, Producers, and the Efficiency of Markets ❖ 21

85. Cameron visits a sporting goods store to buy a new set of golf clubs. He is willing to pay $750 for the clubs

but buys them on sale for $575. Cameron’s consumer surplus from the purchase is

a.

$175.

b.

$575.

c.

$750.

d.

$1,325.

86. If the price a consumer pays for a product is equal to a consumer’s willingness to pay, then the consumer sur-

plus relevant to that purchase is

a.

zero.

b.

negative, and the consumer would not purchase the product.

c.

positive, and the consumer would purchase the product.

d.

There is not enough information given to answer this question.

87. Suppose there is an early freeze in California that reduces the size of the lemon crop. What happens to con-

sumer surplus in the market for lemons?

a.

Consumer surplus increases.

b.

Consumer surplus decreases.

c.

Consumer surplus is not affected by this change in market forces.

d.

We would have to know whether the demand for lemons is elastic or inelastic to make this

determination.

88. Suppose your own demand curve for tomatoes slopes downward. Suppose also that, for the last tomato you

bought this week, you paid a price exactly equal to your willingness to pay. Then

a.

you should buy more tomatoes before the end of the week.

b.

you already have bought too many tomatoes this week.

c.

your consumer surplus on the last tomato you bought is zero.

d.

your consumer surplus on all of the tomatoes you have bought this week is zero.

89. Suppose the market demand curve for a good passes through the point (quantity demanded = 100, price =

$25). If there are five buyers in the market, then

a.

the marginal buyer’s willingness to pay for the 100th unit of the good is $25.

b.

the sum of the five buyers’ willingness to pay for the 100th unit of the good is $25.

c.

the average of the five buyers’ willingness to pay for the 100th unit of the good is $25.

d.

all of the five buyers are willing to pay at least $25 for the 100th unit of the good.

22 ❖ Chapter 7/Consumers, Producers, and the Efficiency of Markets

90. If the cost of producing sofas decreases, then consumer surplus in the sofa market will

a.

increase.

b.

decrease.

c.

remain constant.

d.

increase for some buyers and decrease for other buyers.

91. All else equal, what happens to consumer surplus if the price of a good increases?

a.

Consumer surplus increases.

b.

Consumer surplus decreases.

c.

Consumer surplus is unchanged.

d.

Consumer surplus may increase, decrease, or remain unchanged.

92. All else equal, what happens to consumer surplus if the price of a good decreases?

a.

Consumer surplus increases.

b.

Consumer surplus decreases.

c.

Consumer surplus is unchanged.

d.

Consumer surplus may increase, decrease, or remain unchanged.

93. Which of the following will cause an increase in consumer surplus?

a.

an increase in the production cost of the good

b.

a technological improvement in the production of the good

c.

a decrease in the number of sellers of the good

d.

the imposition of a binding price floor in the market

94. Which of the following will cause a decrease in consumer surplus?

a.

an increase in the number of sellers of the good

b.

a decrease in the production cost of the good

c.

sellers expect the price of the good to be lower next month

d.

the imposition of a binding price floor in the market

95. When there is a technological advance in the pork industry, consumer surplus in that market will

a.

increase.

b.

decrease.

c.

not change, since technology affects producers and not consumers.

d.

not change, since consumers’ willingness to pay is unaffected by the technological advance.

Chapter 7/Consumers, Producers, and the Efficiency of Markets ❖ 23

96. If the price of oak lumber increases, what happens to consumer surplus in the market for oak cabinets?

a.

Consumer surplus increases.

b.

Consumer surplus decreases.

c.

Consumer surplus will not change consumer surplus; only producer surplus changes.

d.

Consumer surplus depends on what event led to the increase in the price of oak lumber.

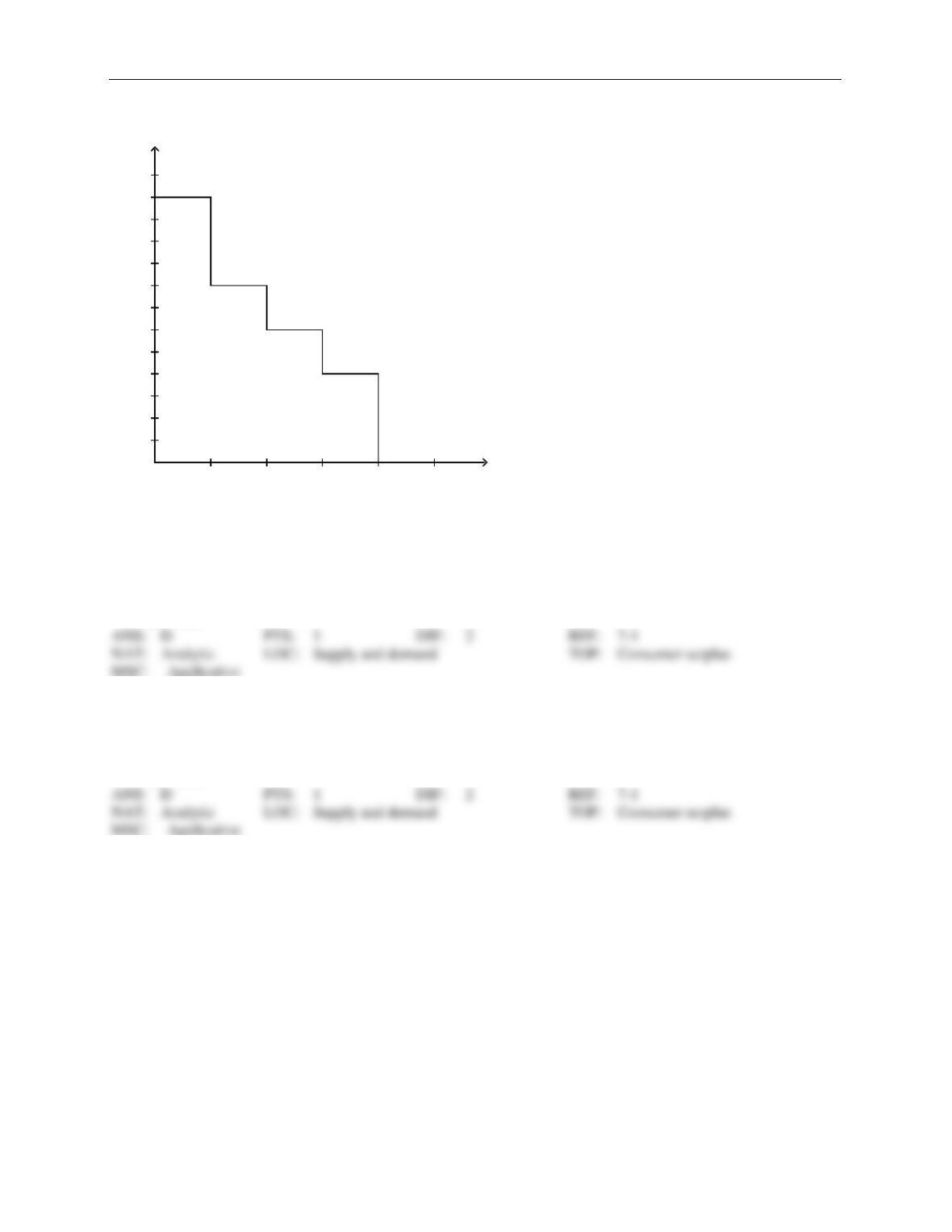

97. Which of the following is not true when the price of a good or service falls?

a.

Buyers who were already buying the good or service are better off.

b.

Some new buyers, who are now willing to buy, enter the market.

c.

The total consumer surplus in the market increases.

d.

The total value of purchases before and after the price change is the same.

98. When the demand for a good increases and the supply of the good remains unchanged, consumer surplus

a.

decreases.

b.

is unchanged.

c.

increases.

d.

may increase, decrease, or remain unchanged.

99. Suppose televisions are a normal good and buyers of televisions experience a decrease in income. As a result,

consumer surplus in the television market

a.

decreases.

b.

is unchanged.

c.

increases.

d.

may increase, decrease, or remain unchanged.

100. Motor oil and gasoline are complements. If the price of motor oil increases, consumer surplus in the gasoline

market

a.

decreases.

b.

is unchanged.

c.

increases.

d.

may increase, decrease, or remain unchanged.

101. Dallas buys strawberries, and he would be willing to pay more than he now pays. Suppose that Dallas has a

change in his tastes such that he values strawberries more than before. If the market price is the same as be-

fore, then

a.

Dallas’s consumer surplus would be unaffected.

b.

Dallas’s consumer surplus would increase.

c.

Dallas’s consumer surplus would decrease.

d.

Dallas would be wise to buy fewer strawberries than before.

24 ❖ Chapter 7/Consumers, Producers, and the Efficiency of Markets

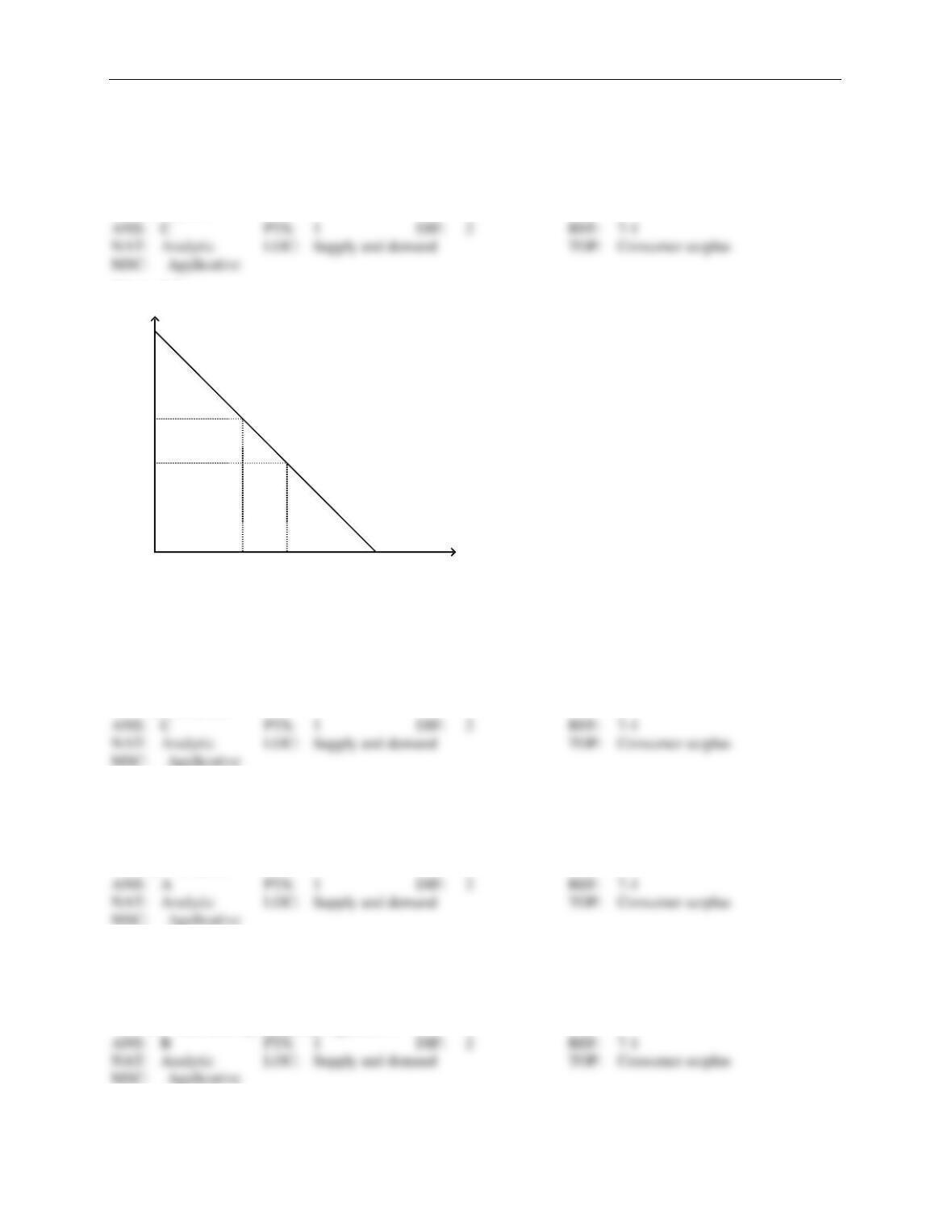

Figure 7-1

Demand

1 2 3 4 5 Q

50

100

150

200

250

300

350

P

102. Refer to Figure 7-1. If the price of the good is $250, then consumer surplus amounts to

a.

$50.

b.

$100.

c.

$150.

d.

$200.

103. Refer to Figure 7-1. If the price of the good is $150, then consumer surplus amounts to

a.

$150.

b.

$200.

c.

$250.

d.

$300.

104. Refer to Figure 7-1. If the price of the good is $50, then consumer surplus amounts to

a.

$400.

b.

$500.

c.

$600.

d.

$750.

105. Refer to Figure 7-1. If the price of the good is $200, then

a.

consumer surplus is $150.

b.

consumer surplus is $650.

c.

producer surplus is $650.

d.

producer surplus is $750.

Chapter 7/Consumers, Producers, and the Efficiency of Markets ❖ 25

106. Refer to Figure 7-1. The value of the good to consumers minus the cost of the good to consumers amounts to

$325 if the price of the good is

a.

$200.

b.

$150.

c.

$125.

d.

$100.

Figure 7-2

P2

P1

Q2 Q1

Demand

A

BC

D F

Quantity

Price

107. Refer to Figure 7-2. When the price is P1, consumer surplus is

a.

A.

b.

A+B.

c.

A+B+C.

d.

A+B+D.

108. Refer to Figure 7-2. When the price is P2, consumer surplus is

a.

A.

b.

B.

c.

A+B.

d.

A+B+C.

109. Refer to Figure 7-2. When the price rises from P1 to P2, consumer surplus

a.

increases by an amount equal to A.

b.

decreases by an amount equal to B+C.

c.

increases by an amount equal to B+C.

d.

decreases by an amount equal to C.

26 ❖ Chapter 7/Consumers, Producers, and the Efficiency of Markets

110. Refer to Figure 7-2. Area C represents the

a.

decrease in consumer surplus that results from a downward-sloping demand curve.

b.

consumer surplus to new consumers who enter the market when the price falls from P2 to P1.

c.

increase in producer surplus when quantity sold increases from Q2 to Q1.

d.

decrease in consumer surplus to each consumer in the market when the price increases from P1 to

P2.

111. Refer to Figure 7-2. When the price rises from P1 to P2, which of the following statements is not true?

a.

The buyers who still buy the good are worse off because they now pay more.

b.

Some buyers leave the market because they are not willing to buy the good at the higher price.

c.

Buyers place a higher value on the good after the price increase.

d.

Consumer surplus in the market falls.

Figure 7-3

Demand

P1

P2

Q1 Q2

A

B

C

D

F G

Quantity

Price

112. Refer to Figure 7-3. Which area represents consumer surplus at a price of P1?

a.

ABD

b.

ACG

c.

BCDF

d.

DFG

113. Refer to Figure 7-3. Which area represents consumer surplus at a price of P2?

a.

ABD

b.

ACG

c.

BCDF

d.

DFG

Chapter 7/Consumers, Producers, and the Efficiency of Markets ❖ 27

114. Refer to Figure 7-3. Which area represents the increase in consumer surplus when the price falls from P1 to

P2?

a.

ABD

b.

ACG

c.

DFG

d.

BCGD

115. Refer to Figure 7-3. When the price falls from P1 to P2, which area represents the increase in consumer sur-

plus to existing buyers?

a.

ABD

b.

ACG

c.

BCFD

d.

DFG

116. Refer to Figure 7-3. When the price falls from P1 to P2, which area represents the increase in consumer sur-

plus to new buyers entering the market?

a.

ABD

b.

ACG

c.

BCDF

d.

DFG

28 ❖ Chapter 7/Consumers, Producers, and the Efficiency of Markets

Figure 7-4

1 2 3 4 Quantity

2

4

6

8

10

12

14

16

18

20

22

24

26

Price

117. Refer to Figure 7-4. If the price of the good is $6, then consumer surplus is

a.

$16.

b.

$24.

c.

$30.

d.

$36.

118. Refer to Figure 7-4. If the price of the good is $12, then consumer surplus is

a.

$9.

b.

$11.

c.

$13.

d.

$16.

Chapter 7/Consumers, Producers, and the Efficiency of Markets ❖ 29

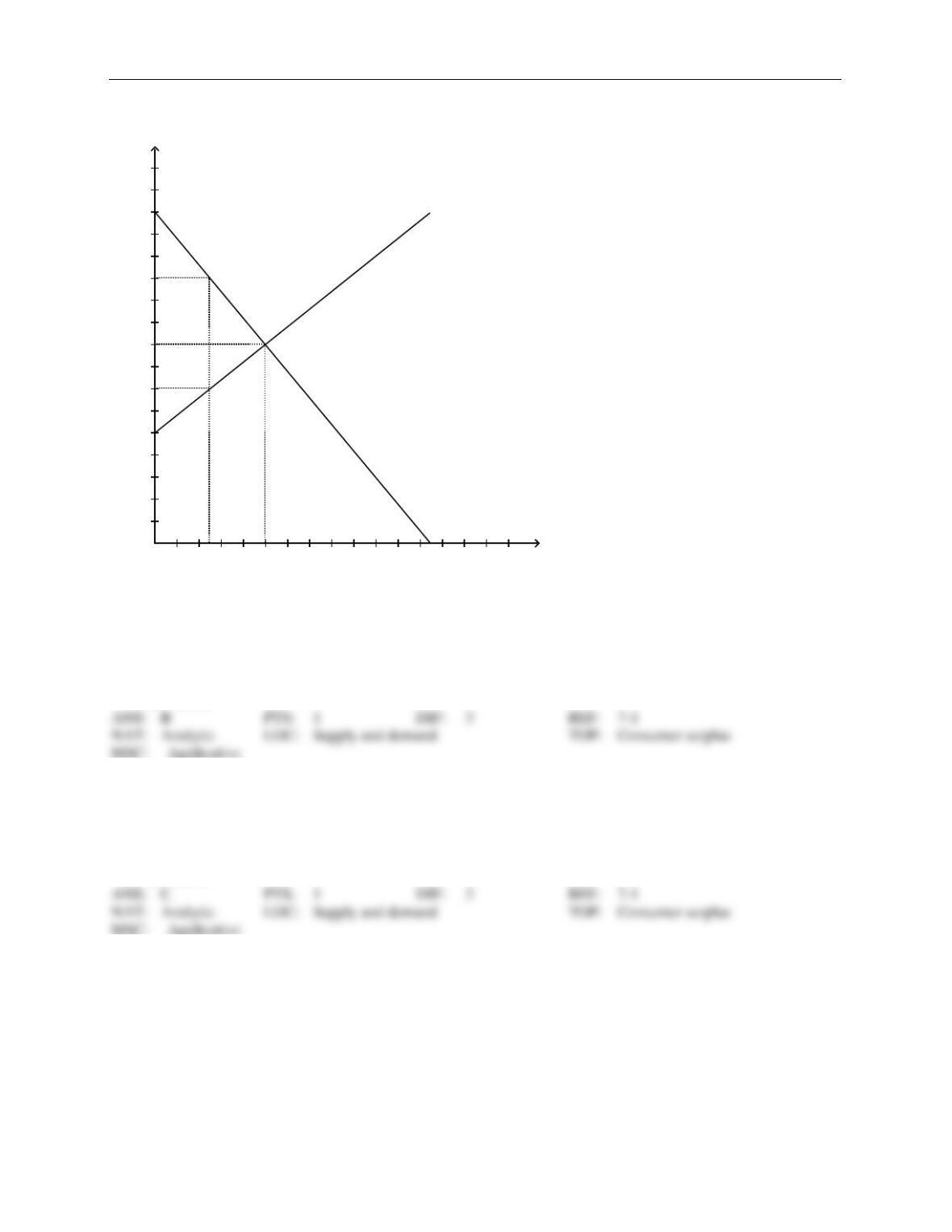

Figure 7-5

5

Supply

Demand

25

2 4 6 8 10 12 14 16 18 20 22 24 26 28 Quantity

10

20

30

40

50

60

70

80

90

100

110

120

130

140

150

160

170

Price

119. Refer to Figure 7-5. At the equilibrium price, consumer surplus is

a.

$200.

b.

$300.

c.

$500.

d.

$600.

120. Refer to Figure 7-5. If the government imposes a price floor of $120 in this market, then consumer surplus

will decrease by

a.

$75.

b.

$125.

c.

$225.

d.

$300.

30 ❖ Chapter 7/Consumers, Producers, and the Efficiency of Markets

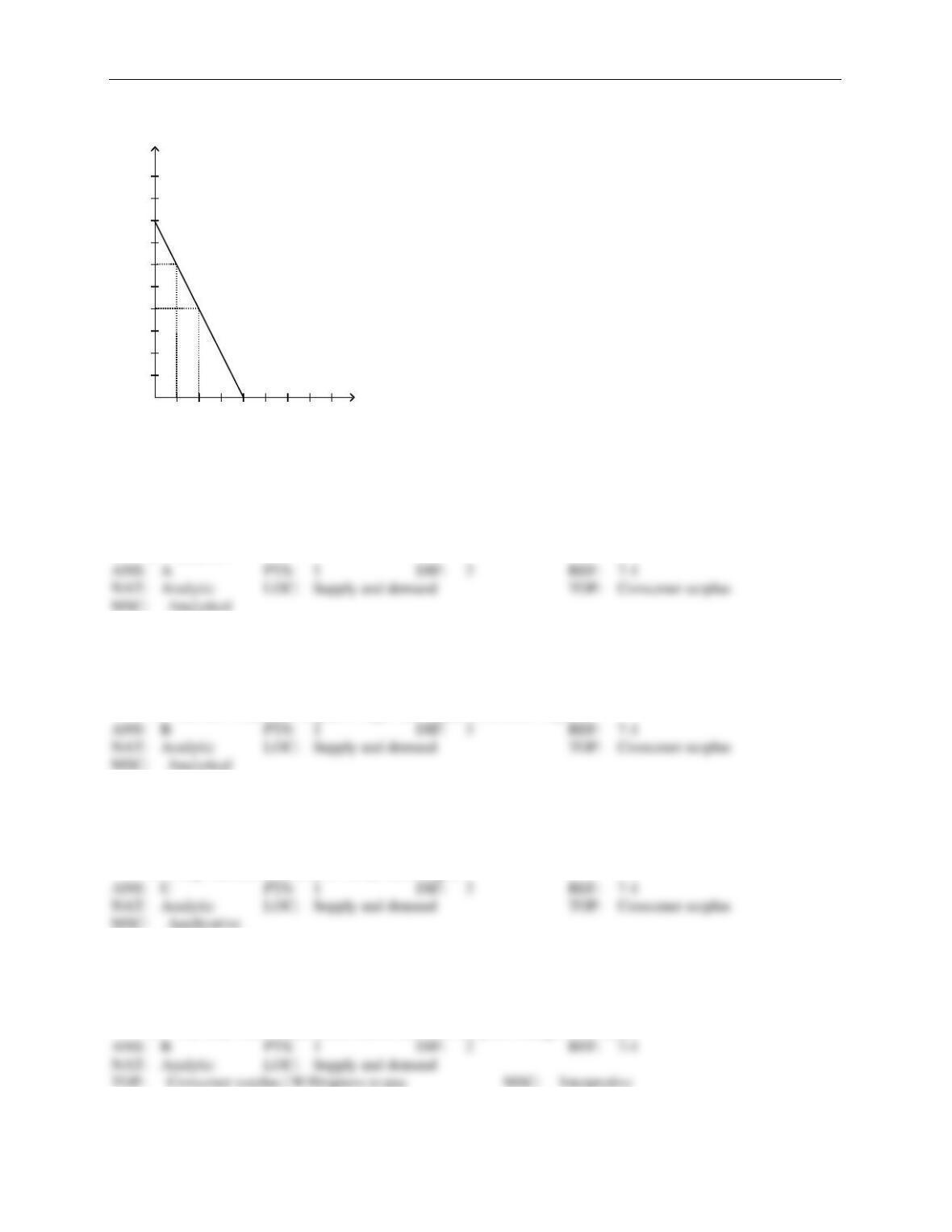

Figure 7-6

Demand

25 50 75 100 125 150 Quantity

25

50

75

100

125

150

175

200

225

250

Price

121. Refer to Figure 7-6. What is the consumer surplus if the price is $100?

a.

$2,500

b.

$5,000

c.

$10,000

d.

$20,000

122. Refer to Figure 7-6. What happens to the consumer surplus if the price rises from $100 to $150?

a.

The new consumer surplus is half of the original consumer surplus.

b.

The new consumer surplus is 25 percent of the original consumer surplus.

c.

The new consumer surplus is double the original consumer surplus.

d.

The new consumer surplus is triple the original consumer surplus.

123. When the supply of a good increases and the demand for the good remains unchanged, consumer surplus

a.

decreases.

b.

is unchanged.

c.

increases.

d.

may increase, decrease, or remain unchanged.

124. Which of the following is true when the price of a good or service rises?

a.

Buyers who were already buying the good or service are better off.

b.

Some buyers exit the market.

c.

The total consumer surplus in the market increases.

d.

The total value of purchases before and after the price change is the same.

Chapter 7/Consumers, Producers, and the Efficiency of Markets ❖ 31

125. Motor oil and gasoline are complements. If the price of motor oil decreases, consumer surplus in the gasoline

market

a.

decreases.

b.

is unchanged.

c.

increases.

d.

may increase, decrease, or remain unchanged.

126. What happens to consumer surplus in the iPod market if iPods are normal goods and buyers of iPods experi-

ence an increase in income?

a.

Consumer surplus decreases.

b.

Consumer surplus remains unchanged.

c.

Consumer surplus increases.

d.

Consumer surplus may increase, decrease, or remain unchanged.

127. As a result of a decrease in price,

a.

new buyers enter the market, increasing consumer surplus.

b.

new buyers enter the market, decreasing consumer surplus.

c.

existing buyers exit the market, increasing consumer surplus.

d.

existing buyers exit the market, decreasing consumer surplus.

128. Economists normally assume people’s preferences should be

a.

respected.

b.

adjusted.

c.

overruled.

d.

ignored.

129. Consumer surplus is a good measure of economic welfare if policymakers want to

a.

maximize total benefit.

b.

minimize deadweight loss.

c.

respect the preferences of sellers.

d.

respect the preferences of buyers.

130. When policymakers are considering a particular action, they can use consumer surplus as a(n)

a.

objective measure of the benefits to buyers as determined by policymakers.

b.

measure of the benefits to buyers as the buyers perceive them.

c.

potentially flawed measure of the benefits to buyers if the buyers are not rational.

d.

Both b) and c) are correct.

32 ❖ Chapter 7/Consumers, Producers, and the Efficiency of Markets

PRODUCER SURPLUS

1. A seller’s opportunity cost measures the

a.

value of everything she must give up to produce a good.

b.

amount she is paid for a good minus her cost of providing it.

c.

consumer surplus.

d.

out of pocket expenses to produce a good but not the value of her time.

2. Cost is a measure of the

a.

seller’s willingness to sell.

b.

seller’s producer surplus.

c.

producer shortage.

d.

seller’s willingness to buy.

3. Justin builds fences for a living. Justin’s out–of-pocket expenses (for wood, paint, etc.) plus the value that he

places on his own time amount to his

a.

producer surplus.

b.

producer deficit.

c.

cost of building fences.

d.

profit.

4. A supply curve can be used to measure producer surplus because it reflects

a.

the actions of sellers.

b.

quantity supplied.

c.

sellers’ costs.

d.

the amount that will be purchased by consumers in the market.

5. A seller is willing to sell a product only if the seller receives a price that is at least as great as the

a.

seller’s producer surplus.

b.

seller’s cost of production.

c.

seller’s profit.

d.

average willingness to pay of buyers of the product.

6. Producer surplus is

a.

measured using the demand curve for a good.

b.

always a negative number for sellers in a competitive market.

c.

the amount a seller is paid minus the cost of production.

d.

the opportunity cost of production minus the cost of producing goods that go unsold.

Chapter 7/Consumers, Producers, and the Efficiency of Markets ❖ 33

7. Producer surplus measures the

a.

benefits to sellers of participating in a market.

b.

costs to sellers of participating in a market.

c.

price that buyers are willing to pay for sellers’ output of a good or service.

d.

benefit to sellers of producing a greater quantity of a good or service than buyers demand.

8. A seller’s willingness to sell is

a.

measured by the seller’s cost of production.

b.

related to her supply curve, just as a buyer’s willingness to buy is related to his demand curve.

c.

less than the price received if producer surplus is a positive number.

d.

All of the above are correct.

9. Caroline sharpens knives in her spare time for extra income. Buyers of her service are willing to pay $2.95 per

knife for as many knives as Caroline is willing to sharpen. On a particular day, she is willing to sharpen the

first knife for $2.00, the second knife for $2.25, the third knife for $2.75, and the fourth knife for $3.50. As-

sume Caroline is rational in deciding how many knives to sharpen. Her producer surplus is

a.

$0.95.

b.

$1.15.

c.

$1.30.

d.

$1.85.

10. Anita sharpens knives in her spare time for extra income. Buyers of her service are willing to pay $3.50 per

knife for as many knives as Anita is willing to sharpen. On a particular day, she is willing to sharpen the first

knife for $2.00, the second knife for $2.50, the third knife for $3.00, and the fourth knife for $3.50. Assume

Anita is rational in deciding how many knives to sharpen. Her producer surplus is

a.

$3.50.

b.

$3.00.

c.

$2.00.

d.

$0.50.

11. Tom tunes pianos in his spare time for extra income. Buyers of his service are willing to pay $155 per tuning.

One particular week, Tom is willing to tune the first piano for $120, the second piano for $125, the third piano

for $140, and the fourth piano for $160. Assume Tom is rational in deciding how many pianos to tune. His

producer surplus is

a.

$95.

b.

$80.

c.

$75.

d.

$60.

12. David tunes pianos in his spare time for extra income. Buyers of his service are willing to pay $135 per tuning.

One particular week, David is willing to tune the first piano for $115, the second piano for $125, the third pi-

34 ❖ Chapter 7/Consumers, Producers, and the Efficiency of Markets

ano for $140, and the fourth piano for $175. Assume David is rational in deciding how many pianos to tune.

His producer surplus is

a.

$-15.

b.

$20.

c.

$30.

d.

$75.

13. Ivana produces cookies. Her production cost is $6 per dozen. She sells the cookies for $8 per dozen. Her pro-

ducer surplus per dozen cookies is

a.

$2.

b.

$6.

c.

$8.

d.

$14.

14. Donald produces nails at a cost of $200 per ton. If he sells the nails for $350 per ton, his producer surplus per

ton is

a.

$150.

b.

$200.

c.

$350.

d.

$550.

15. If Gina sells a shirt for $40, and her producer surplus from the sale is $32, her cost must have been

a.

$72.

b.

$32.

c.

$8.

d.

We would have to know the consumer surplus in order to make this determination.

16. Ronnie operates a lawn-care service. On each day, the cost of mowing the first lawn is $10, the cost of mow-

ing the second lawn is $12, and the cost of mowing the third lawn is $15. His producer surplus on the first

three lawns of the day is $53. If Ronnie charges all customers the same price for lawn mowing, that price is

a.

$25.

b.

$30.

c.

$36.

d.

$45.

Chapter 7/Consumers, Producers, and the Efficiency of Markets ❖ 35

17. At Nick’s Bakery, the cost to make homemade chocolate cake is $3 per cake. As a result of selling three cakes,

Nick experiences a producer surplus in the amount of $19.50. Nick must be selling his cakes for

a.

$6.50 each.

b.

$7.50 each.

c.

$9.50 each.

d.

$10.50 each.

18. Kristi and Rebecca sell lemonade on the corner. It costs them 9 cents to make each cup. On a certain day, they

sell 40 cups, and their producer surplus for that day amounts to $12.40. Kristi and Rebecca sold each cup for

a.

36 cents.

b.

40 cents.

c.

45 cents.

d.

52 cents.

Table 7-7

The following table represents the costs of five possible sellers.

Seller

Cost

Abby

$1,500

Bobby

$1,200

Carlos

$1,000

Dianne

$750

Evalina

$500

19. Refer to Table 7-7. If the market price is $1,000, the producer surplus in the market is

a.

$700.

b.

$750.

c.

$2,250.

d.

$3,700.

20. Refer to Table 7-7. If the market price is $900, the producer surplus in the market is

a.

$350.

b.

$550.

c.

$750.

d.

$1,000.

21. Refer to Table 7-7. If the market price is $1,100, the combined total cost of all participating sellers is

a.

$3,700.

b.

$2,700.

c.

$2,250.

d.

$1,250.

36 ❖ Chapter 7/Consumers, Producers, and the Efficiency of Markets

22. Refer to Table 7-7. If the market price is $900, the combined total cost of all participating sellers is

a.

$3,700.

b.

$2,700.

c.

$2,250.

d.

$1,250.

23. Refer to Table 7-7. If the price is $1,000,

a.

Bobby is an eager supplier.

b.

Dianne is an eager supplier.

c.

Abby’s producer surplus is $500.

d.

All of the above are correct.

24. Refer to Table 7-7. If the price is $775, who would be willing to supply the product?

a.

Abby and Bobby

b.

Abby, Bobby, and Carlos

c.

Carlos, Dianne, and Evalina

d.

Dianne and Evalina

25. Refer to Table 7-7. Suppose each of the five sellers can supply at most one unit of the good. The market

quantity supplied is exactly 3 if the price is

a.

$670.

b.

$770.

c.

$970.

d.

$1,170.

26. Refer to Table 7-7. Suppose each of the five sellers can supply at most one unit of the good. The market

quantity supplied is exactly 4 if the price is

a.

$770.

b.

$970.

c.

$1,170.

d.

$1,370.

27. Refer to Table 7-7. Who is a marginal seller when the price is $1,200?

a.

Bobby

b.

Bobby and Abby

c.

Carlos, Dianne, and Evalina

d.

Carlos, Dianne, Evalina, and Bobby

Chapter 7/Consumers, Producers, and the Efficiency of Markets ❖ 37

Table 7-8

The only four producers in a market have the following costs:

Seller

Cost

Evan

$50

Selena

$100

Angie

$150

Kris

$200

28. Refer to Table 7-8. If the sellers bid against each other for the right to sell the good to a consumer, then the

good will sell for

a.

$50 or slightly more.

b.

$100 or slightly less.

c.

$150 or slightly less.

d.

$200 or slightly more.

29. Refer to Table 7-8. If the sellers bid against each other for the right to sell the good to a consumer, then the

producer surplus will be

a.

$0 or slightly more.

b.

$50 or slightly less.

c.

$150 or slightly less.

d.

$200 or slightly more.

30. Refer to Table 7-8. If Evan, Selena, and Angie sell the good, and the resulting producer surplus is $300, then

the price must have been

a.

$200.

b.

$300.

c.

$450.

d.

$600.

31. Refer to Table 7-8. If Evan, Selena, Angie, and Kris sell the good, and the resulting producer surplus is $700,

then the price must have been

a.

$200.

b.

$300.

c.

$500.

d.

$700.

38 ❖ Chapter 7/Consumers, Producers, and the Efficiency of Markets

Table 7-9

The numbers reveal the opportunity costs of providing 10 piano lessons of equal quality.

Seller

Cost

Marcia

$200

Jan

$250

Cindy

$350

Greg

$400

Peter

$700

Bobby

$800

32. Refer to Table 7-9. You wish to purchase 10 piano lessons, so you take bids from each of the sellers. You

will not accept a bid below a seller’s cost because you are concerned that the seller will not provide all 10 les-

sons. What bid will you accept?

a.

$351

b.

$251

c.

$249

d.

$199

33. Refer to Table 7-9. You wish to purchase 10 piano lessons for yourself and for your brother, so you take bids

from each of the sellers. You will take lessons at the same time, so one teacher cannot provide lessons to both

of you. You must pay the same price for both sets of lessons, and you will not accept a bid below a seller’s

cost because you are concerned that the seller will not provide all 10 lessons. What bid will you accept?

a.

$351

b.

$349

c.

$201

d.

$199

34. Refer to Table 7-9. The equilibrium market price for 10 piano lessons is $400. What is the total producer

surplus in the market?

a.

$0

b.

$300

c.

$400

d.

$700

35. Refer to Table 7-9. The equilibrium market price for 10 piano lessons is $300. What is the total producer

surplus in the market?

a.

$50

b.

$150

c.

$1,050

d.

$1,500

36. Refer to Table 7-9. You wish to purchase 10 piano lessons, so you take bids from each of the sellers. The

bids are required to be rounded to the nearest dollar. You will not accept a bid below a seller’s cost because

you are concerned that the seller will not provide all 10 lessons. Your parents have given you $450 to spend

Chapter 7/Consumers, Producers, and the Efficiency of Markets ❖ 39

on piano lessons. You believe that the sellers with higher opportunity costs offer higher quality lessons. You

want the highest quality lessons that you can afford, but you can spend any remaining money on dinner with

friends. From whom will you take lessons, and how much money will you spend?

a.

Peter; $450

b.

Cindy; $450

c.

Greg; $401

d.

Cindy; $401

Table 7-10

Seller

Cost

LeBron

$700

Kobe

$600

Kevin

$450

Steve

$400

37. Refer to Table 7-10. You want to hire a professional photographer to take pictures of your fami-

ly. The table shows the costs of the four potential sellers in the local photography market. You take bids from

the sellers. Who offers the winning bid, and what does he offer to charge for the photography session?

a.

Steve; more than $400 but less than $450

b.

Steve; $399

c.

LeBron; more than $700

d.

LeBron; more than $600 but less than $700

38. Refer to Table 7-10. You and your best friend want to hire a professional photographer to take pictures of

your two families. The table shows the costs of the four potential sellers in the local photography market.

You and your friend take bids from the sellers. Who offers the two winning bids, and what do they offer to

charge for the photography sessions?

a.

LeBron and Kobe; more than $450 but less than $600

b.

Kevin and Steve; more than $450 but less than $600

c.

LeBron and Kobe; more than $700

d.

Kevin and Steve; less than $400

39. Refer to Table 7-10. You want to hire a professional photographer to take pictures of your family. The table

shows the costs of the four potential sellers in the local photography market. You hire Kevin for a price of

$500. What is his producer surplus?

a.

$500

b.

$150

c.

$100

d.

$50

40 ❖ Chapter 7/Consumers, Producers, and the Efficiency of Markets

40. Refer to Table 7-10. You and your best friend want to hire a professional photographer to take pictures of

your two families. The table shows the costs of the four potential sellers in the local photography market.

You and your friend agree to offer $500 for each session. Who accepts the offer, and what is the total produc-

er surplus in the market?

a.

LeBron and Kobe; $500

b.

Kevin and Steve; $500

c.

LeBron and Kobe; $300

d.

Kevin and Steve; $150

41. Refer to Table 7-10. You want to hire a professional photographer to take pictures of your family. The table

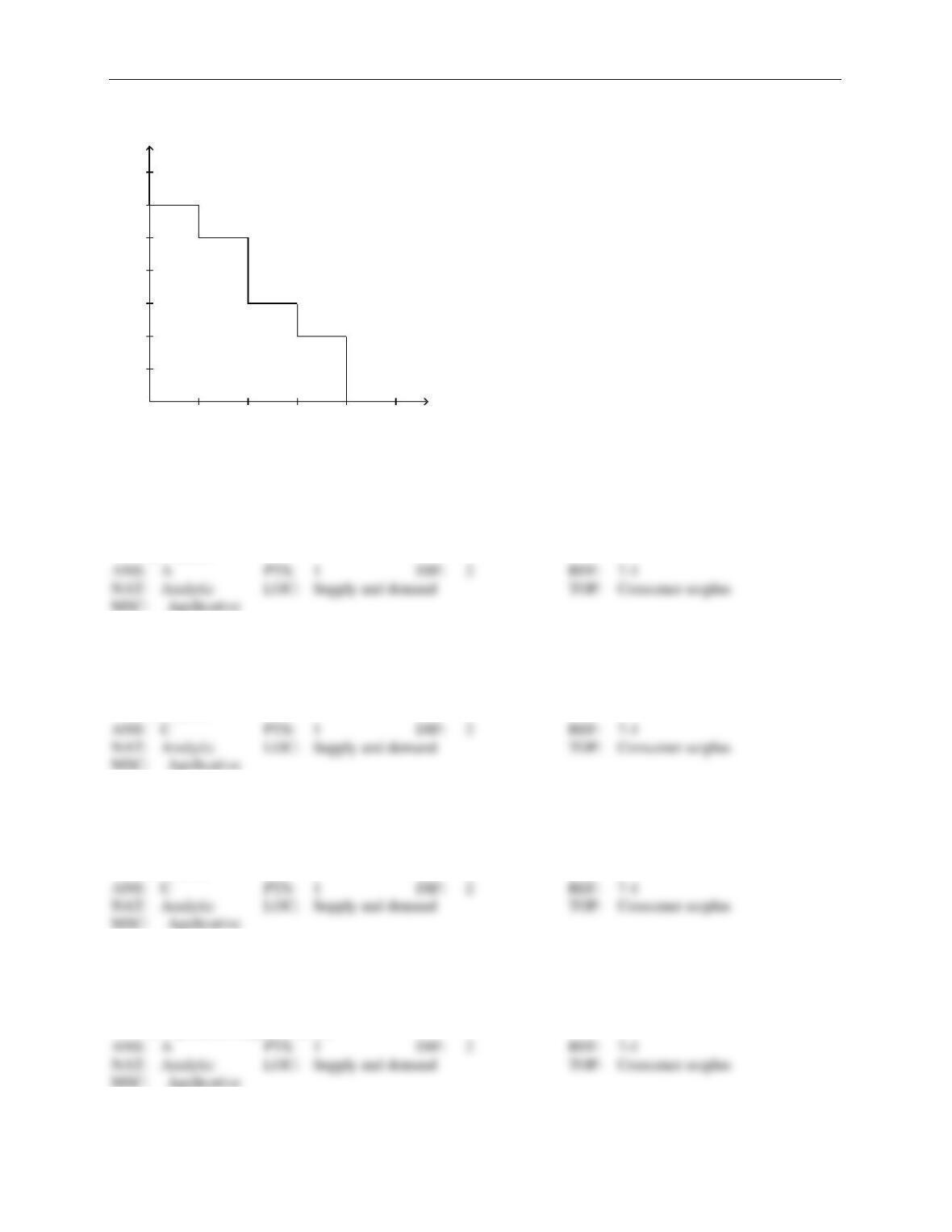

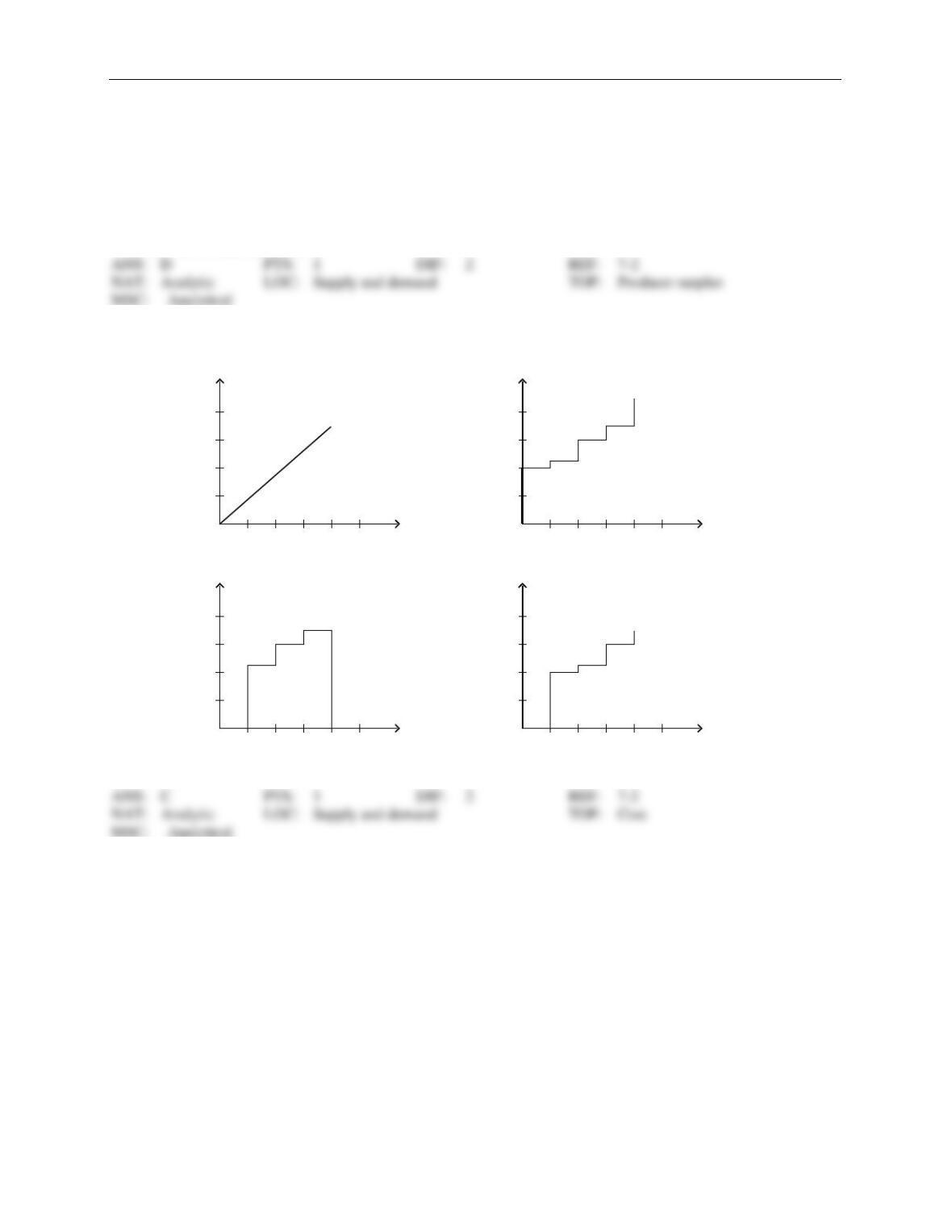

shows the costs of the four potential sellers in the local photography market. Which of the following graphs

represents the market supply curve?

a.

Supply

$200

$400

$450

$600

$700

$800

1 2 3 4 Quantity

Price

c.

$200

$400

$450

$600

$700

$800

Supply

1 2 3 4 Quantity

Price

b.

$200

$400

$450

$600

$700

$800

Supply

1 2 3 4 Quantity

Price

d.

$200

$400

$450

$600

$700

$800 Supply

1 2 3 4 Quantity

Price