Name:

Class:

Date:

Chapter 07: Production and Cost in the Firm

4

36

12

5

42

6

6

46

4

a.

second

b.

third

c.

fourth

d.

fifth

e.

sixth

87. When diminishing marginal returns set in, total product _____.

a.

is negative

b.

decreases at an increasing rate

c.

decreases at a decreasing rate

d.

increases at an increasing rate

e.

increases at a decreasing rate

e

88. When diminishing marginal returns set in, marginal product is _____.

a.

positive and increasing

b.

positive and decreasing

c.

negative and increasing

d.

negative and decreasing

e.

zero

89. In the range of increasing marginal returns, total product is _____.

a.

increasing at a constant rate

b.

increasing at an increasing rate

c.

increasing at a decreasing rate

d.

decreasing at an increasing rate

e.

decreasing at a decreasing rate

90. At the point where diminishing marginal returns set in, the slope of the total product curve is _____.

a.

positive and increasing

b.

positive and decreasing

c.

negative and increasing

d.

negative and decreasing

e.

constant

91. Which of the following is true of marginal product?

a.

When marginal product is negative, total product is increasing.

Name:

Class:

Date:

Chapter 07: Production and Cost in the Firm

b.

When marginal product is increasing, total product is decreasing.

c.

When marginal product is positive and decreasing, total product is decreasing.

d.

When marginal product is positive and decreasing, total product is increasing by increasing amounts.

e.

When marginal product is increasing, total product is increasing by increasing amounts.

92. The marginal product of labor is the _____.

a.

cost of one worker

b.

average output per worker

c.

change in revenue from selling one more unit of output

d.

change in revenue from using one more unit of labor

e.

change in output from using one more unit of labor

93. To a firm facing constant input prices, increasing marginal returns:

a.

mean that each additional unit of output costs more to produce than the previous unit.

b.

mean that the marginal product of the variable input decreases as more of the input is used.

c.

can occur due to the specialization and division of labor.

d.

usually occur at very high rates of output.

e.

can never occur.

94. A variable cost is one that changes _____.

a.

only in the long run

b.

only in the short run

c.

year to year

d.

month to month

e.

as output changes

95. Fixed costs are defined as:

a.

the total costs of a firm’s production.

b.

the additional costs of the last unit produced.

c.

costs that increase proportionately as the quantity produced increases.

d.

costs that do not vary as quantity produced increases.

e.

implicit costs only.

96. Marginal cost eventually increases as output increases due to the effect of _____.

a.

economies of scale

b.

increasing average cost

c.

increasing total cost

d.

diminishing marginal product of inputs

Name:

Class:

Date:

Chapter 07: Production and Cost in the Firm

e.

constant fixed cost

97. The law of diminishing marginal returns explains why:

a.

monopolies have a guaranteed profit margin.

b.

short-run MC and AVC curves are U-shaped.

c.

the production possibilities curve is bowed out.

d.

long-run supply curves are downward sloping.

e.

total product is a straight line.

98. Which of the following is true of marginal cost when marginal returns are increasing?

a.

It is negative and increasing.

b.

It is negative and decreasing.

c.

It is positive and increasing.

d.

It is positive and decreasing.

e.

It is positive and has a constant slope.

99. What is true of marginal cost when marginal returns are decreasing?

a.

It is negative and increasing.

b.

It is negative and decreasing.

c.

It is positive and increasing.

d.

It is positive and decreasing.

e.

It is positive and has a constant slope.

c

100. Which of the following is true of the relationship between marginal cost and marginal product?

a.

Marginal product and marginal cost are not related with each other.

b.

When marginal product increases, marginal cost increases.

c.

When marginal product increases, marginal cost falls.

d.

When marginal product is negative, marginal cost is negative.

e.

When diminishing marginal returns set in, marginal cost falls.

c

101. When a firm is experiencing diminishing marginal returns, its marginal cost _____.

a.

rises

b.

falls

c.

remains constant

d.

first rises and then falls

e.

becomes zero

a

102. As output rises, marginal product eventually diminishes and _____.

Name:

Class:

Date:

Chapter 07: Production and Cost in the Firm

a.

marginal cost increases

b.

average cost falls

c.

total cost falls

d.

fixed cost is increasing

e.

average product is negative

103. If variable cost at each output level doubles, then:

a.

Average Total Cost doubles.

b.

Average Fixed Cost doubles.

c.

Marginal Cost remains unchanged.

d.

Marginal Cost doubles.

e.

Marginal Cost less than doubles.

104. If variable cost rises from $60 to $100 as output increases from 15 to 20 units, the marginal cost of the twentieth unit

is _____.

a.

$100

b.

$5

c.

$40

d.

$8

e.

$58

105. Which of the following statements is true?

a.

If the marginal product of labor diminishes, the average fixed cost rises.

b.

If the marginal product of labor diminishes, the average variable cost is constant.

c.

If the marginal product of labor diminishes, the marginal cost rises.

d.

If the marginal product of labor diminishes, the average total cost rises.

e.

If the marginal product of labor diminishes, the total cost rises at a diminishing rate.

106. If labor is a firm’s only variable input, marginal cost ultimately depends on:

a.

the fixed cost of labor.

b.

how much profit is made.

c.

the price of the good produced.

d.

how much output each worker produces.

e.

the fixed cost per unit.

107. Total fixed cost divided by the level of output yields the _____.

a.

average variable cost per unit

b.

average fixed cost per unit

c.

marginal cost per unit

Name:

Class:

Date:

Chapter 07: Production and Cost in the Firm

d.

average total cost per unit

e.

marginal productivity per unit of fixed resource

108. Total cost is calculated as _____.

a.

average fixed cost plus average variable cost

b.

fixed cost plus variable cost

c.

the additional cost of the last unit produced

d.

marginal cost plus variable cost

e.

marginal cost plus fixed cost

109. Total cost is calculated as _____.

a.

FC + MC

b.

FC/MC

c.

(VC + FC)/MC

d.

VC + FC

e.

VC + output

110. If a firm shuts down in the short run and produces no output, its total cost will be:

a.

equal to zero.

b.

equal to the variable cost.

c.

equal to the fixed cost.

d.

equal to only explicit costs.

e.

equal to the sum of implicit and explicit costs.

c

111. A firm enters into a consent decree to avoid an even greater legal setback. If the terms of the consent decree

effectively double the firm’s fixed costs, then:

a.

marginal cost more than doubles.

b.

marginal cost doubles.

c.

marginal cost remains unchanged.

d.

average total cost remains unchanged.

e.

average variable cost doubles.

c

112. If total cost at Quantity = 0 is $100 and total cost at Quantity = 10 is $500, then average variable cost at Quantity =

10 is _____.

a.

$500

b.

$400

c.

$50

d.

$40

e.

$10

Name:

Class:

Date:

Chapter 07: Production and Cost in the Firm

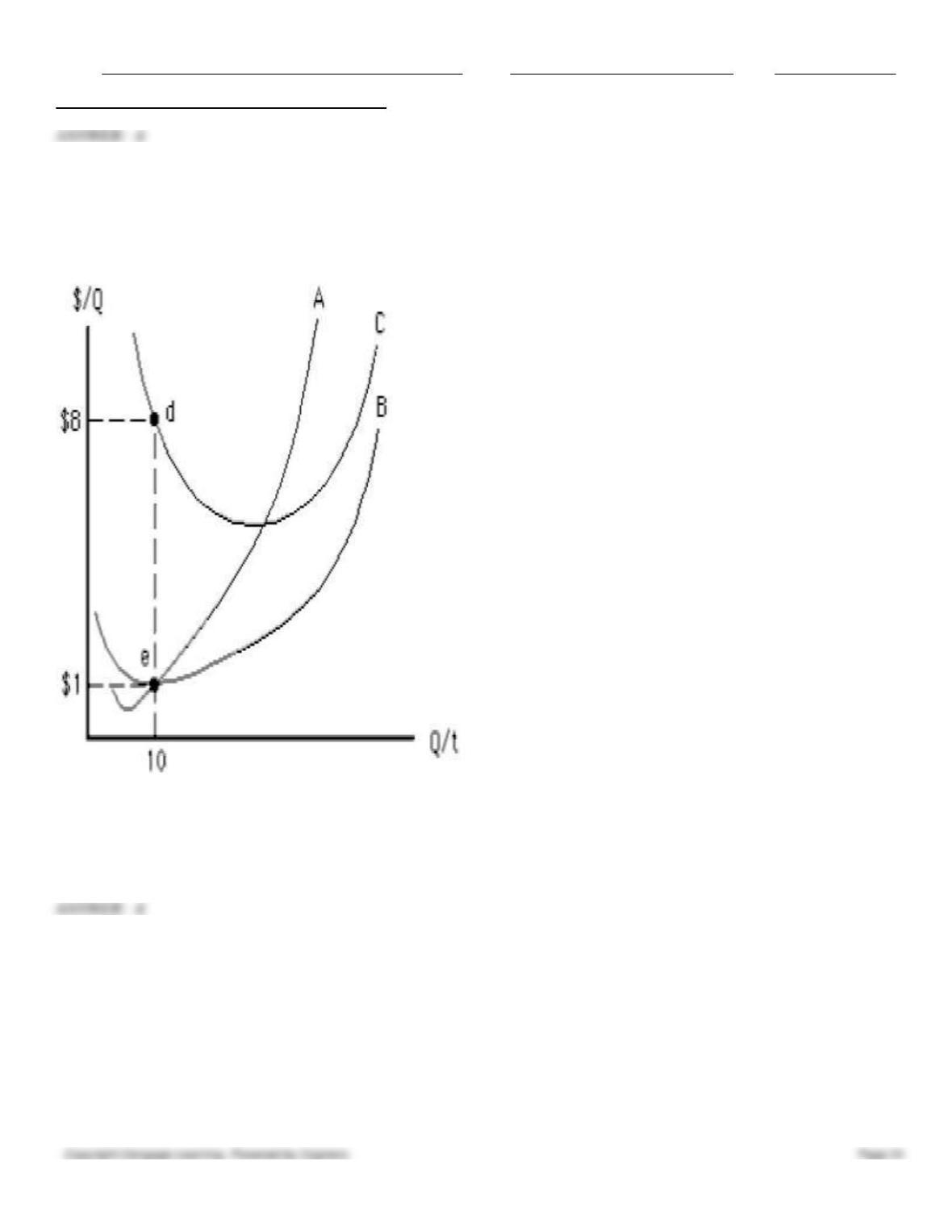

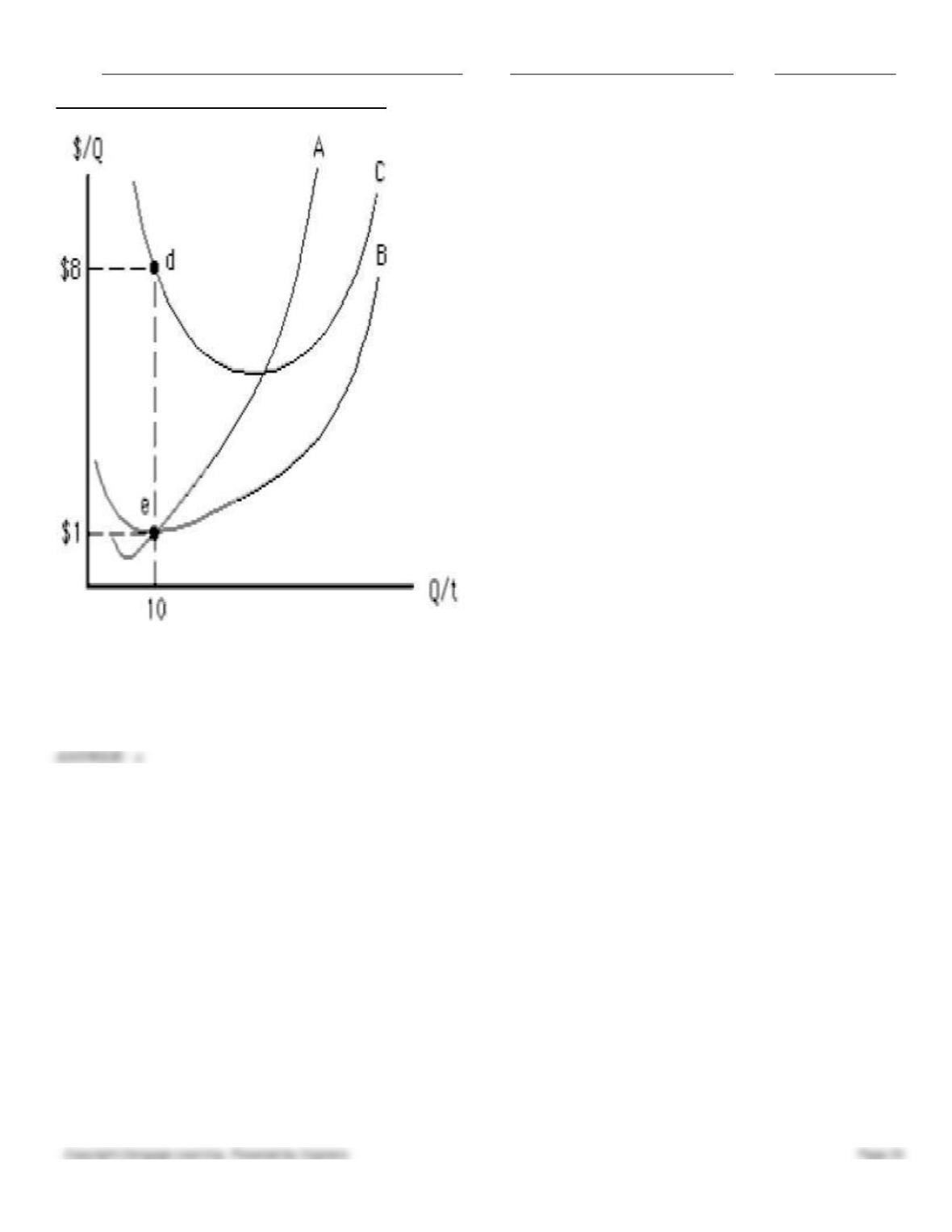

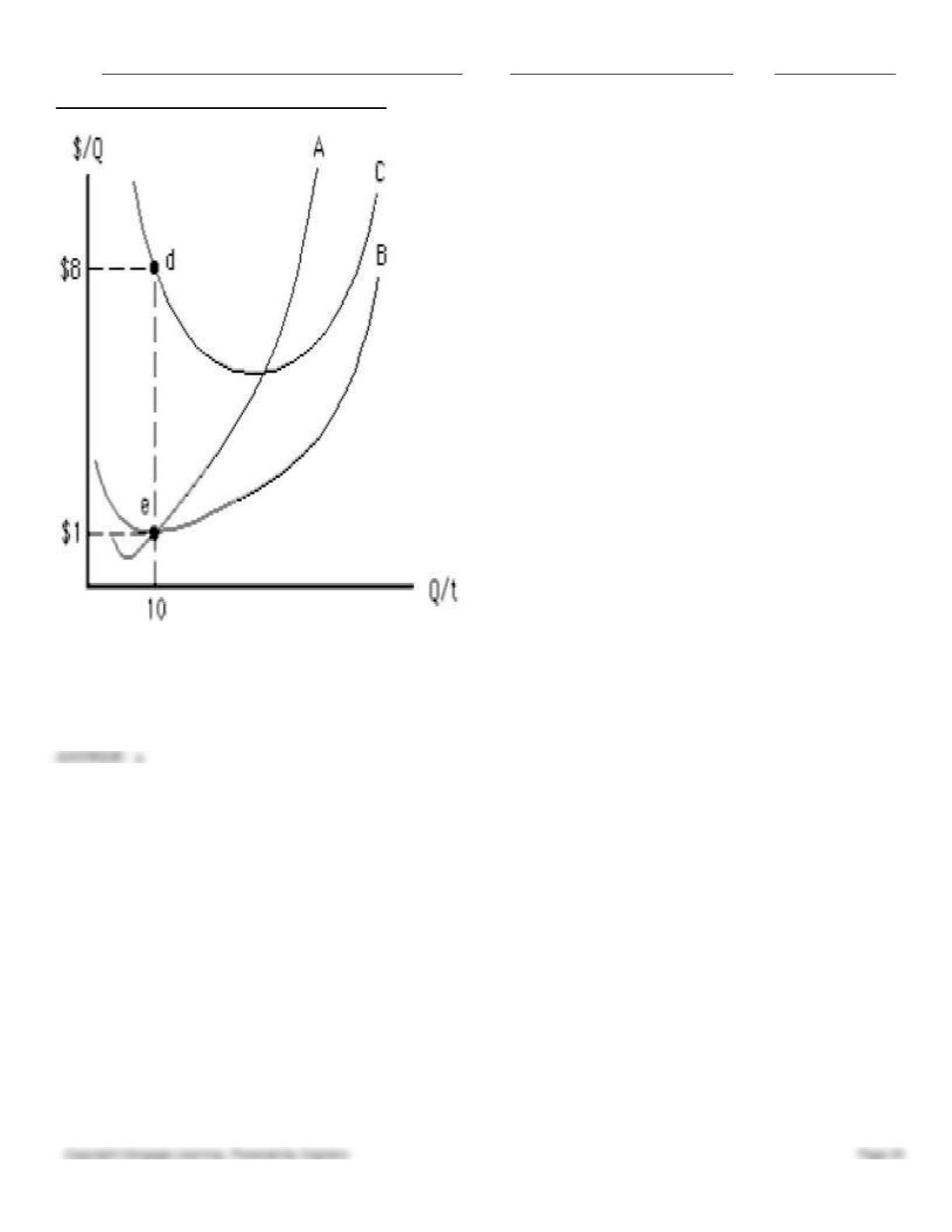

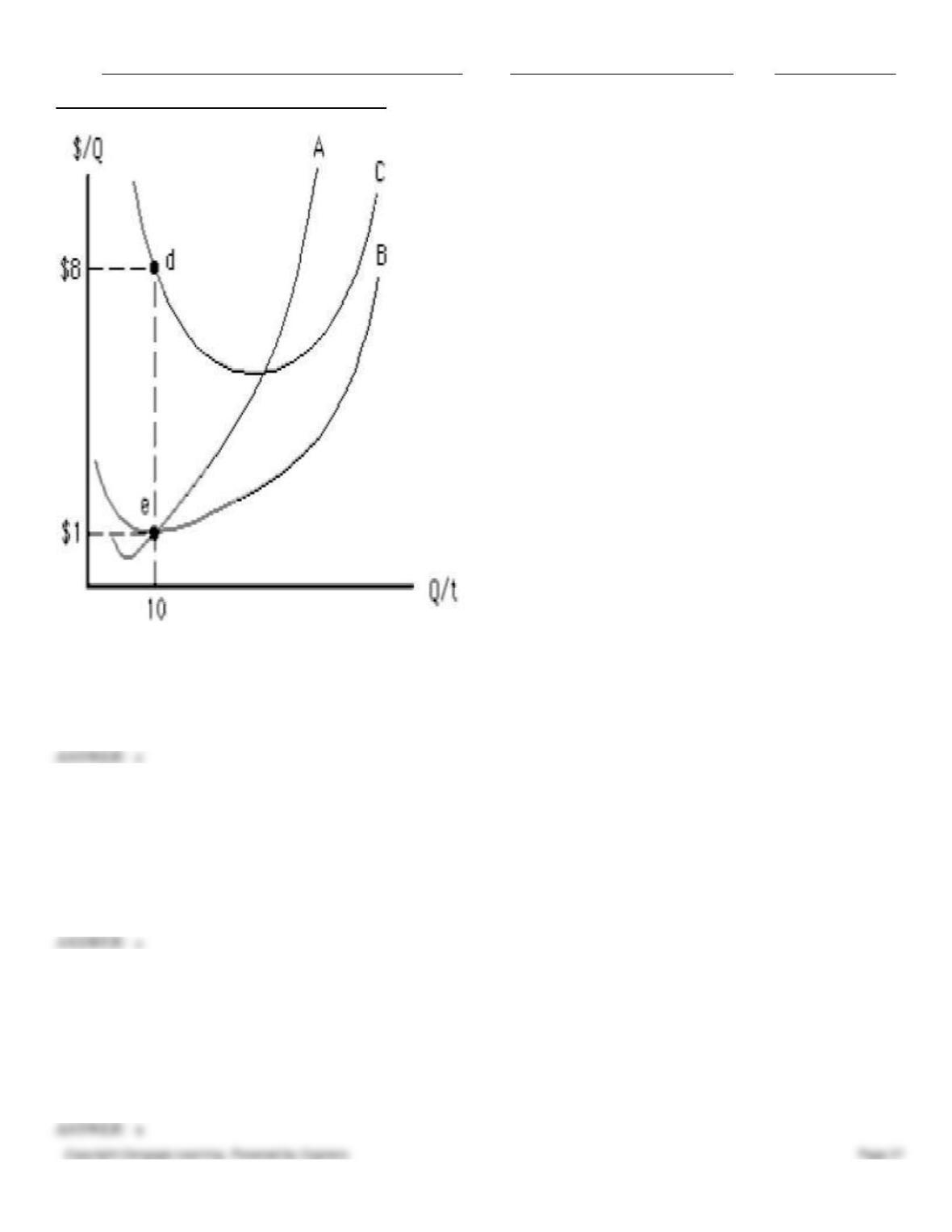

113. Figure 7.1 shows the U-shaped cost curves for a producer. In the figure below, A is the marginal cost curve, B is the

average variable cost curve, and C is the average total cost curve. The vertical distance between lines B and C at any level

of output represents _____.

Figure 7.1

a.

marginal cost

b.

average total cost

c.

average variable cost

d.

average fixed cost

e.

average marginal cost

114. Figure 7.1 shows the U-shaped cost curves for a producer. In the table figure, A is the marginal cost curve, B is the

average variable cost curve, and C is the average total cost curve. At an output of 10, the:

Figure 7.1

Name:

Class:

Date:

Chapter 07: Production and Cost in the Firm

a.

total cost equals $10.

b.

fixed cost equals $1.

c.

variable cost equals $10.

d.

marginal cost equals $10.

e.

fixed cost equals $10.

115. Figure 7.1 shows the U-shaped cost curves for a producer. In the figure below, A is the marginal cost curve, B is the

average variable cost curve, and C is the average total cost curve. When output is 10, then:

Figure 7.1

Name:

Class:

Date:

Chapter 07: Production and Cost in the Firm

a.

total cost equals $80.

b.

fixed cost equals $10.

c.

variable cost equals $70.

d.

marginal cost equals $10.

e.

fixed cost equals $7.

116. Figure 7.1 shows the U-shaped cost curves for a producer. In the figure below, curve B represents _____.

Figure 7.1

Name:

Class:

Date:

Chapter 07: Production and Cost in the Firm

a.

marginal cost

b.

average total cost

c.

average variable cost

d.

average fixed cost

e.

average marginal cost

117. The short-run average variable cost curve:

a.

is always downward sloping.

b.

starts at the origin and always slopes upward.

c.

starts above the origin and always slopes upward.

d.

is a horizontal line intersecting the vertical axis.

e.

slopes downward at low rates of output and then slopes upward at higher rates of output.

118. The average total cost curve and the average variable cost curve:

a.

are closer together as output increases, with average variable cost reaching its minimum level first.

b.

are closer together as output increases, with average total cost reaching its minimum level first.

c.

are farther apart as output increases, with average variable cost reaching its minimum level first.

d.

are farther apart as output increases, with average total cost reaching its minimum level first.

e.

are parallel to each other and reach their minimum levels at the same rate of output.

Name:

Class:

Date:

Chapter 07: Production and Cost in the Firm

119. Which of the following is true in the short run at the output level where average total cost is at its minimum?

a.

Marginal cost equals average total cost.

b.

Average variable cost equals fixed cost.

c.

Marginal cost equals average variable cost.

d.

Average total cost equals average fixed cost.

e.

Average total cost equals average variable cost.

120. Which of the following correctly describes the relationship between the marginal cost and average variable cost

curves?

a.

Marginal Cost is always above Average Variable Cost

b.

Average Variable Cost is always above Marginal Cost

c.

Marginal Cost crosses Average Variable Cost at Average Variable Cost’s minimum point

d.

Marginal Cost crosses Average Variable Cost at Marginal Cost’s minimum point

e.

both Average Variable Cost and Marginal Cost first rise and then fall

121. If marginal cost exceeds average variable cost, then:

a.

average variable cost is negative.

b.

average variable cost is increasing.

c.

marginal cost is greater than average total cost.

d.

average variable cost is decreasing.

e.

average fixed cost is increasing.

122. If marginal cost is less than average total cost, then:

a.

marginal cost must be falling.

b.

average total cost must be increasing.

c.

average variable cost must equal average total cost.

d.

average variable cost must be decreasing.

e.

average variable cost may be increasing or decreasing.

123. Which of the following is true of the MC curve?

a.

It intersects the ATC curve at its minimum, but it does not intersect the AVC curve at its minimum.

b.

It intersects the AVC curve at its minimum, but it does not intersect the ATC curve at its minimum.

c.

It intersects both the ATC and the AVC curves at their minimums.

d.

It intersects both the ATC and the AFC curves at their minimums.

e.

It intersects both the AVC and the AFC curves at their minimums.

124. The marginal cost curve intersects the average total cost (ATC) curve:

a.

at the ATC curve’s minimum point.

Name:

Class:

Date:

Chapter 07: Production and Cost in the Firm

b.

only when the ATC curve is sloping upward.

c.

at the ATC curve’s maximum point.

d.

only when the ATC curve is sloping downward.

e.

when the ATC curve intersects the fixed cost curve.

a

125. The marginal cost curve intersects the average variable cost (AVC) curve:

a.

only when the AVC curve is rising.

b.

at the AVC curve’s maximum point.

c.

at the AVC curve’s minimum point.

d.

only when the AVC curve is sloping downward.

e.

when the AVC curve intersects the fixed cost curve.

c

126. Which of the following is true of the relationship between average and marginal costs?

a.

If the marginal cost is greater than the average cost, the average cost is increasing.

b.

If the marginal cost is greater than the average cost, the average cost is decreasing

c.

If the marginal cost is greater than the average cost, the marginal cost is increasing

d.

If the marginal cost is greater than the average cost, the marginal cost is decreasing

e.

If the marginal cost is greater than the average cost, the total cost is decreasing

a

127. With respect to the average cost curves, the marginal cost curve:

a.

intersects the average total cost, average fixed cost, and average variable cost curves at their minimum points.

b.

intersects the average total cost, average fixed cost, and average variable cost curves at their maximum points.

c.

intersects both the average total cost and average variable cost curves at their minimum points.

d.

intersects the average total cost curve where it is increasing and the average variable cost curve where it is

decreasing.

e.

intersects only the average total cost curve at its minimum point.

c

128. A firm’s long-run average cost curve is also called its _____.

a.

profit curve

b.

explicit cost curve

c.

opportunity cost curve

d.

production curve

e.

planning curve

e

129. Which of the following is also known as the firm’s planning curve?

a.

The average total cost curve

b.

The total cost curve

c.

The long-run average cost curve

d.

The long-run marginal cost curve

Name:

Class:

Date:

Chapter 07: Production and Cost in the Firm

e.

The fixed cost curve

130. For each size of plant a manufacturer could build, there is a different:

a.

long-run average fixed cost curve.

b.

long-run average variable cost curve.

c.

short-run average total cost curve.

d.

long-run average total cost curve.

e.

long-run marginal cost curve.

131. Empirical studies of production suggest that the long-run average cost curve _____.

a.

is U-shaped

b.

has an inverted L shape

c.

is L-shaped

d.

is horizontal

e.

shows diminishing marginal returns

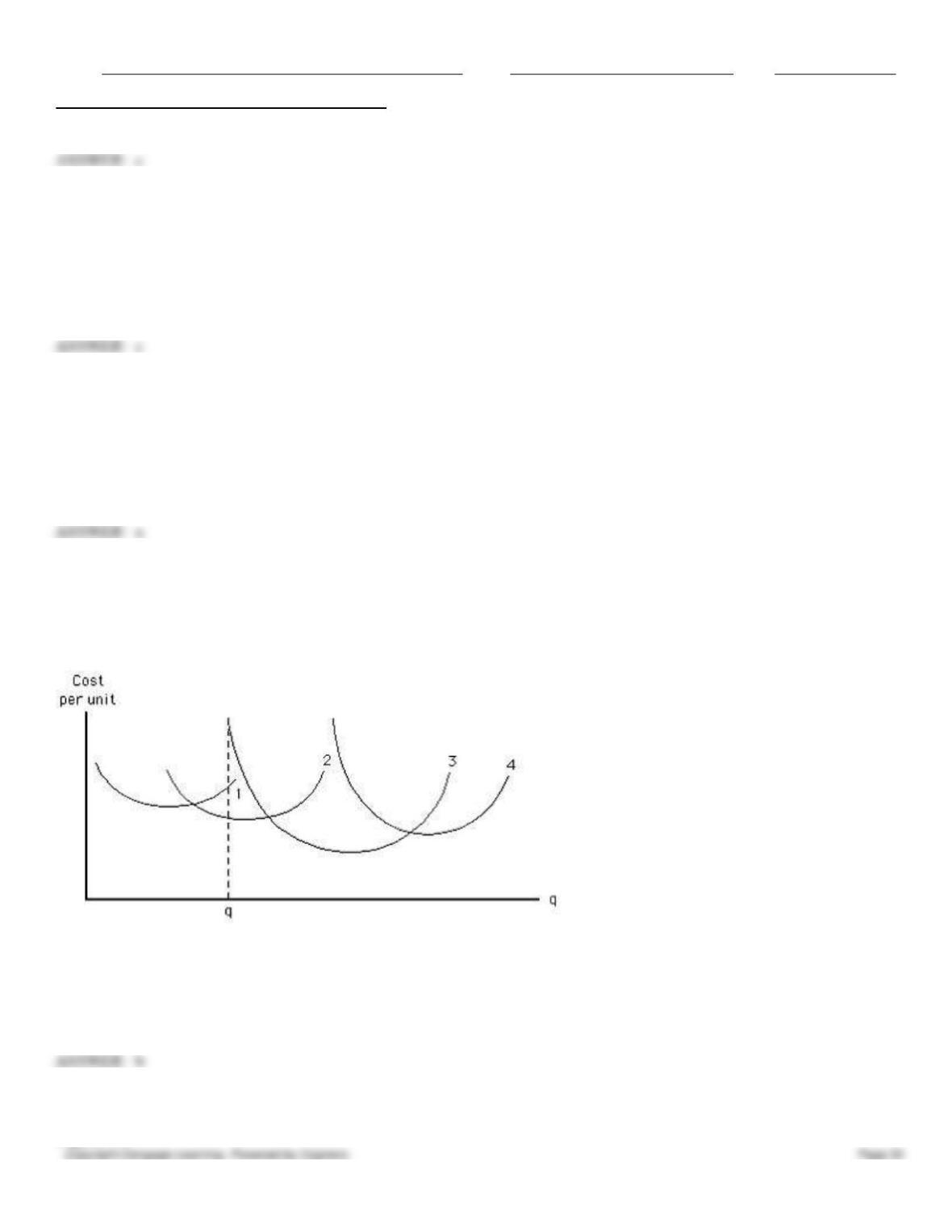

132. Figure 7.2 shows four short-run average cost curves for many possible plant sizes. If the firm represented in the

figure below wants to produce output level q, then, in the long run, it should build a plant size with average total cost

curve of _____.

Figure 7.2

a.

1

b.

2

c.

3

d.

4

e.

either 1 or 3

b

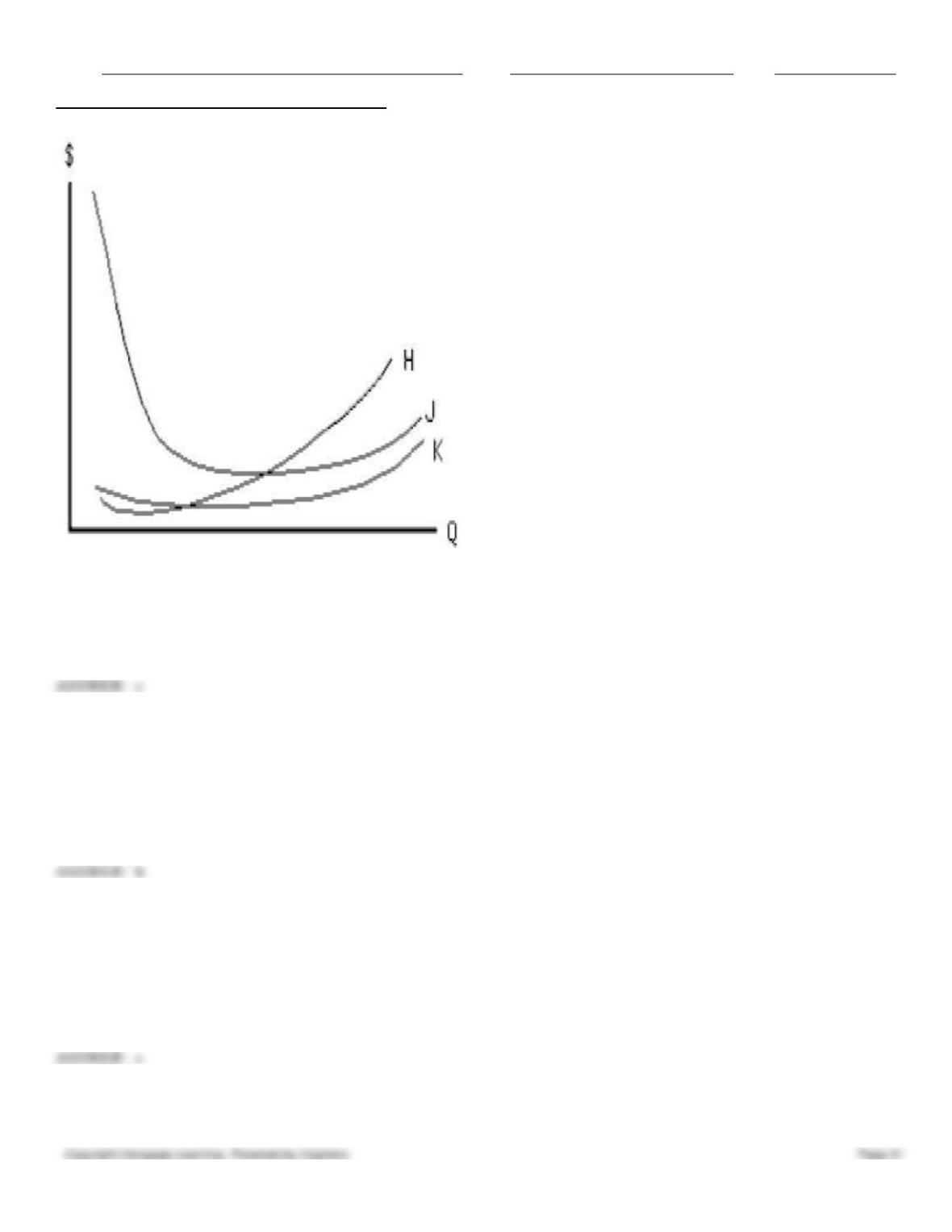

133. Figure 7.3 shows the short-run cost curves for a producer. In the figure below, lines H, J, and K represent:

Figure 7.3

Name:

Class:

Date:

Chapter 07: Production and Cost in the Firm

a.

marginal product, average product, and total product, respectively.

b.

average fixed cost, average total cost, and average variable cost, respectively.

c.

marginal cost, average total cost, and average variable cost, respectively.

d.

average total cost, marginal cost, and average variable cost, respectively.

e.

marginal cost, average product, average total cost, respectively.

134. The shape of the long-run average cost curve reflects _____.

a.

market demand

b.

economies and diseconomies of scale

c.

increasing and diminishing marginal returns

d.

productivity of fixed inputs

e.

the law of diminishing returns

135. Economies of scale occur where:

a.

long-run average cost falls as new firms enter the industry.

b.

short-run average cost falls as new firms enter the industry.

c.

long-run average cost falls as one firm expands plant size.

d.

short-run average cost falls as one firm expands plant size.

e.

long-run average cost rises as one firm expands plant size.

136. Which economic concept explains why a large drugstore chain can produce at a lower average cost than Whoville

Pharmacy, an individually owned drugstore?

Name:

Class:

Date:

Chapter 07: Production and Cost in the Firm

a.

Increasing marginal returns

b.

Diminishing marginal returns

c.

Economies of scale

d.

Diseconomies of scale

e.

Constant returns to scale

137. Doubling the circumference of an oil pipeline more than doubles the volume of oil that can be pumped through. This

strategy is chosen only by large firms because it results in _____.

a.

production inefficiency

b.

diminishing marginal returns

c.

diseconomies of scale

d.

constant returns to scale

e.

economies of scale

138. To achieve the minimum efficient scale in the long run, a firm must:

a.

charge the highest price possible.

b.

produce where demand is unit elastic.

c.

sell the most output possible.

d.

minimize the cost of producing any given amount of output.

e.

produce at minimum long-run average cost.

139. Economies of scale can be caused by:

a.

a decrease in plant size.

b.

short-run increases in marginal productivity.

c.

the use of larger, more specialized machines.

d.

higher information costs as a firm expands.

e.

bureaucratic red tape as a firm expands.

140. The minimum efficient scale for a firm is the:

a.

lowest rate of output at which long-run average cost is at a minimum.

b.

lowest rate of output at which short-run average total cost is at a minimum.

c.

lowest rate of output at which short-run average variable cost is at a minimum.

d.

average of the rates of output at which long-run average cost is at a minimum.

e.

average of the rates of output at which short-run average total cost is at a minimum.

141. Someone once said that Chevrolet is so large that if it shakes its tail, its takes two years for its head to notice it. This

is an example of _____.

a.

profit centers

b.

economies of scale

Name:

Class:

Date:

Chapter 07: Production and Cost in the Firm

c.

diseconomies of scale

d.

diminishing marginal returns

e.

diminishing marginal cost

142. In recent years, the number of farms has fallen while the average farm size has increased. Which of the following

concept may explain this phenomenon?

a.

Diminishing marginal returns

b.

Declining productivity

c.

Diseconomies of scale

d.

Economies of scale

e.

Poor economic reforms

143. Which of the following reflects diseconomies of scale?

a.

Marginal product decreasing as output increases

b.

Short-run marginal cost increasing as output increases

c.

Long-run marginal cost increasing as output increases.

d.

Short-run average cost increasing as output increases.

e.

Long-run total cost increasing by more than double as output doubles

144. If General Electric finds that doubling both its plant size and the amount of associated inputs does not double its

output level, then:

a.

the law of diminishing returns is in effect.

b.

long-run average costs must be decreasing.

c.

the firm is experiencing diseconomies of scale.

d.

the firm should increase production.

e.

the firm is experiencing constant returns to scale.

145. As output increases, diseconomies of scale:

a.

lead to rising long-run average costs.

b.

lead to declining long-run average costs.

c.

lead to rising short-run average total costs.

d.

lead to declining short-run total cost.

e.

mean the law of diminishing marginal returns is affecting production.

146. If a firm triples all of its inputs and its output doubles, it is said to be experiencing:

a.

diminishing marginal returns.

b.

increasing marginal returns.

c.

diseconomies of scale.

d.

economies of scale.

Name:

Class:

Date:

Chapter 07: Production and Cost in the Firm

e.

constant average costs.

147. Diseconomies of scale are pictured on a graph by the upward-sloping portion of the _____.

a.

marginal product curve

b.

short-run marginal cost curve

c.

long-run marginal cost curve

d.

short-run average cost curve

e.

long-run average cost curve

148. _____ is an example of an uncontrollable resource that contributes to diseconomies of scale for a movie theater.

a.

A Concession stand staff

b.

A public road congested with traffic

c.

A discount from movie distributors

d.

A single lobby in the theater

e.

A bigger, more noticeable newspaper advertisement

149. Minimum efficient scale is the level of output at which:

a.

short-run average total cost stops decreasing.

b.

short-run average total cost stops increasing.

c.

long-run average cost stops decreasing.

d.

long-run average cost stops increasing.

e.

profit stops increasing.

150. At a given rate of output, marginal cost equals the slope of the _____.

a.

long-run average cost curve

b.

short-run average total cost curve

c.

planning curve

d.

total cost curve

e.

average variable cost curve

151. The least-cost way of producing each particular rate of output is represented by the tangency points between the

short-run average cost curves and the _____.

a.

total cost curve

b.

short-run average total cost curve

c.

average variable cost curve

d.

long-run average cost curve

e.

marginal cost curve

Name:

Class:

Date:

Chapter 07: Production and Cost in the Firm