Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

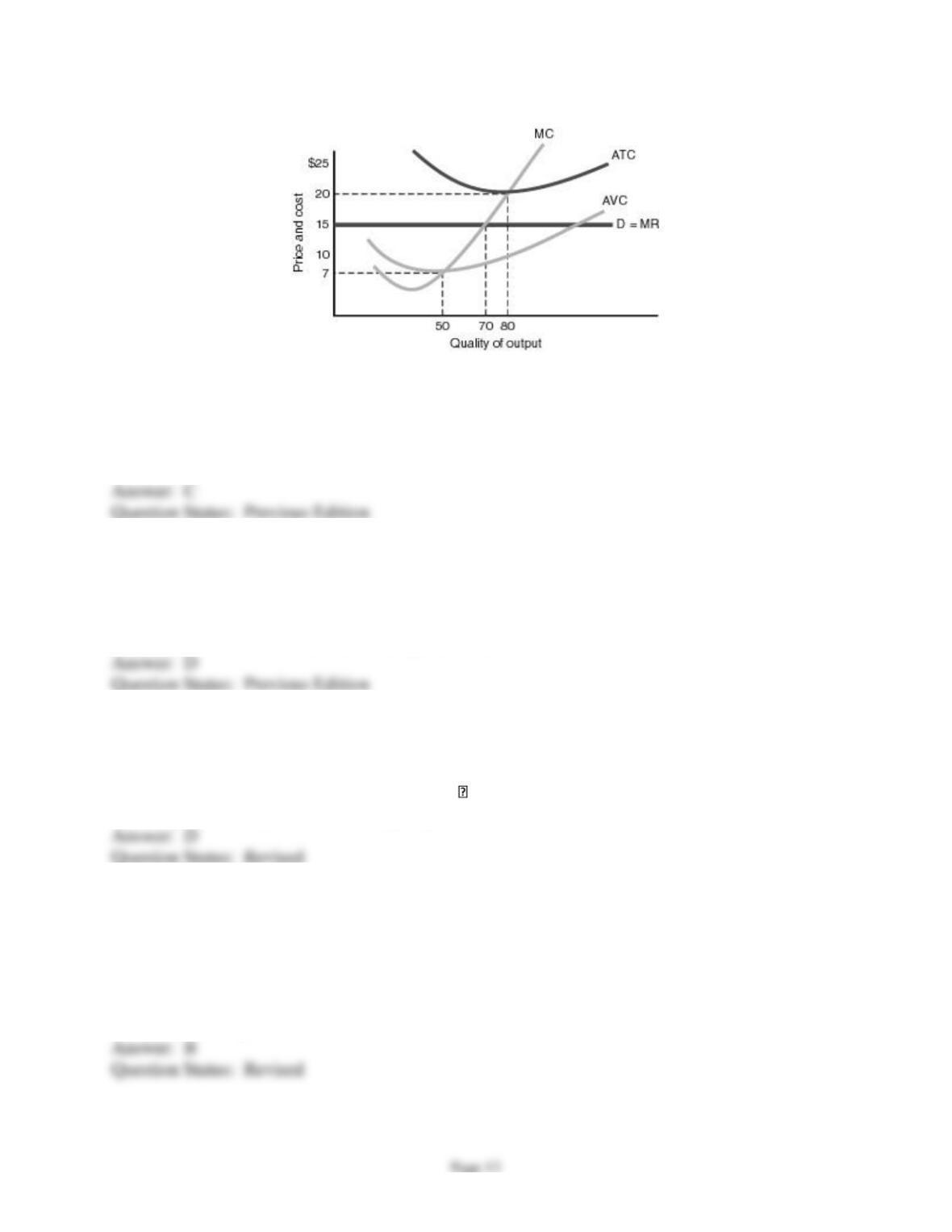

Use the following diagram in answering the following question(s).

12) Based on the figure above, at the prevailing market price of $15, this firm would

A) earn an economic profit.

B) earn a normal profit.

C) incur a loss but continue to operate.

D) shut down.

13) Based on the figure above, long-run equilibrium will be achieved when

A) the entrance of firms reduces the market price to $7.

B) the exit of firms reduces the market price to $7.

C) the entrance of firms raises the market price to $20.

D) the exit of the firm raises the market price to $20.

14) Based on the figure above, which of the following is not a true statement?

A) At a price of $20, this firm would produce 80 units and earn zero economic profit.

B) At a price of $10, this firm would produce somewhere between 50 and 70 units.

C) At a price of $6, this firm would shut down produce nothing.

D) At a price of $18, this firm would produce more than 80 units.

15) The Lazy Z Ranch is a purely competitive firm producing hogs. Its owner anticipates that at

the output where MR = MC, the firm's total costs will be $500,000, its total variable costs will be

$300,000, and the firm will earn $250,000 in revenue. This firm should

A) raise the price of its hogs.

B) shut down to minimize its loss.

C) continue to produce the present output to minimize its loss.

D) expand its output.

Page 14

16) If the firms in a competitive industry earn economic profits,

A) additional firms will enter the industry, and the market supply curve will shift to the left.

B) firms will decide to leave the industry, and the market supply curve will shift to the left.

C) additional firms will enter the industry, and the market supply curve will shift to the right.

D) some firms will leave the industry, and the market supply curve will shift to the right.

17) Suppose the firms in a purely competitive industry are in a long-run equilibrium when the

industry experiences a reduction in demand. Which of the following will occur?

A) In the short run, firms will earn profits and will expand output; in the long run, additional

firms will enter the industry until only a normal profit is earned.

B) In the short run, firms will incur losses but will continue to produce the same output; in the

long run, firms will leave the industry until only a normal profit is earned.

C) In the short run, firms will earn profits and will contract output; in the long run, firms will

leave the industry until the remaining firms can earn an economic profit.

D) In the short run, firms will incur losses and will contract output; in the long run, firms will

leave the industry until the remaining firms can earn a normal profit.

18) If the firms in an industry are experiencing short-run losses, they should

A) immediately leave the industry and enter a different, more profitable industry.

B) continue to operate provided that the prevailing market price is higher than the firm's average

variable cost.

C) shut down and wait for market conditions to improve.

D) shut down provided that the prevailing market price is less than the firm's average total cost.

19) Suppose that a firm experienced a doubling of its total fixed costs while prevailing market

price did not change. Under those conditions, the firm would

A) produce less output and experience lower profits or larger losses.

B) produce more output and experience higher profits or smaller losses.

C) produce the same output but experience higher profits or smaller losses.

D) produce the same output but experience lower profits or larger losses.

20) Which of the following would not cause a competitive firm to increase its output?

A) an increase in industry demand

B) a downward shift of the marginal cost curve

C) an increase in the market price

D) a wage hike that shifted the marginal cost curve upward

1) Which of the following is not a characteristic of a purely competitive industry?

A) a large number of sellers

B) similar, but slightly different products

C) no substantial barriers to entry

D) relatively small firms

2) Which of the following industries most closely approximates pure competition?

A) automobile manufacturing

B) the fast-food industry

C) apple orchards

D) computer manufacturing

3) Because all purely competitive firms sell exactly the same thing

A) firms can easily convince consumers to pay a little more for their firm's product.

B) any firm that charges more than the market price will sell nothing.

C) each firm will tend to charge a different price.

D) firms can never earn an economic profit.

4) Because purely competitive industries are composed of a large number of relatively small

firms,

A) these firms can easily alter the market price by withholding their output from the market.

B) these firms can never earn an economic profit.

C) the market price cannot change.

D) these firms are unable to alter the market price by withholding their output from the market.

5) The inability of a purely competitive firm to alter the market price is a result of all of the

following except the assumption that

A) firms sell identical products.

B) there are no substantial barriers to entering the industry.

C) there are a large number of small firms.

D) each firm produces a small fraction of total industry supply.

6) Price takers maximize their profits or minimize their losses by producing

A) as much output as possible.

B) the output level where price (P) is equal to marginal revenue (MR).

C) the output level where the ATC curve is farthest from the demand curve.

D) the output level where MR = MC.

7) Normal profit is

A) the same thing as economic profit.

B) zero economic profit.

C) the most a purely competitive firm can hope to earn in the short run.

D) None of the above.

8) If the firms in a purely competitive industry are earning economic profits in the short run,

A) they may continue to earn that profit in the long run.

B) that profit will be eliminated in the long run as market demand declines.

C) the entrance of additional firms will eliminate that profit in the long run.

D) the exit of firms will eliminate that profit in the long run.

9) In the short run, competitive firms may earn

A) economic profits.

B) economic losses.

C) normal profits.

D) All of the above are possible.

10) When additional firms enter a competitive industry,

A) the industry supply curve shifts left, raising the market price.

B) the industry demand curve shifts right, lowering the market price.

C) the industry supply curve shifts right, lowering the market price.

D) the industry demand curve shifts left, raising the market price.

11) If the firms in a purely competitive industry are incurring losses in the short run,

A) additional firms will tend to enter the industry until those losses are eliminated.

B) the industry demand curve will shift left until those losses are eliminated.

C) firms will raise the price of their product to eliminate the losses.

D) firms will leave the industry, shifting the supply curve to the left and raising the market price.

12) When a firm is earning a normal profit, the firm's total revenue

A) is exactly equal to the sum of its explicit and implicit costs.

B) is exactly equal to its explicit costs.

C) is exactly equal to its implicit costs.

D) is equal to its explicit costs minus its implicit costs.

13) In the purely competitive model, the force that tends to eliminate profits (or losses) in the

long run is

A) adjustments in market demand.

B) adjustments in market supply.

C) adjustments in both market demand and market supply.

D) None of the above.

14) Imagine a purely competitive firm and industry in long-run equilibrium. According to the

competitive model, if industry demand increased

A) the firms in the industry would tend to earn short-run profits.

B) the firms in the industry would tend to produce more output in the short run.

C) additional firms would tend to enter the industry in the long run.

D) All of the above are true.

15) If a purely competitive firm is incurring an economic loss in the short run, it should

A) immediately leave the industry.

B) continue to operate in the short run, provided that the selling price exceeds the firm's average

variable cost.

C) exit the industry in the long run if market conditions do not improve.

D) Both B and C are correct.

Page 18

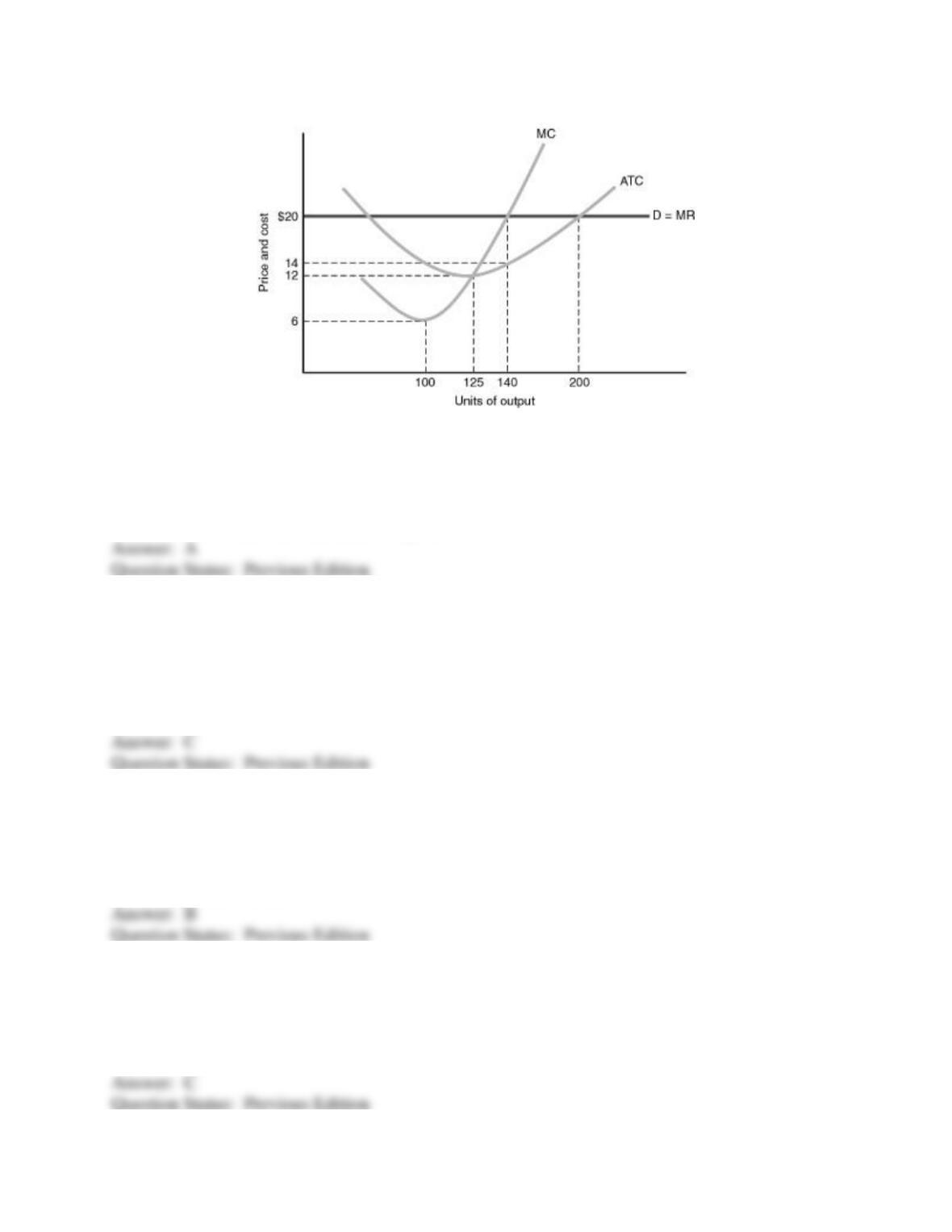

Use the following diagram in answering the following question(s).

16) Based on the figure above, the firm depicted should

A) produce 140 units and maximize its profit.

B) produce 125 units and maximize its profit.

C) produce 140 units and minimize its loss.

D) produce 200 units and maximize its profit.

17) Based on the figure above, if this firm produces the optimal level of output, its total revenue

will be

A) $1,960.

B) $4,000.

C) $2,800.

D) $1,500.

18) Based on the figure above, if this firm produces the optimal level of output, it will

A) incur a loss of $460.

B) earn a profit of $840.

C) earn a normal profit.

D) earn a profit of $1,300.

19) Based on the figure above, in long-run equilibrium, this firm's product will sell for

A) between $14 and $20.

B) $14.

C) $12.

D) $6.

20) Based on the figure above, in long-run equilibrium, this firm will produce

A) more than 140 units of output.

B) 140 units of output.

C) 125 units of output.

D) 100 units of output.

21) Based on the figure above, long-run equilibrium will be achieved when

A) additional firms enter this industry, lowering the equilibrium price and eliminating all

economic profit.

B) some firms leave this industry, raising the equilibrium price and eliminating the economic

loss.

C) the firm raises its price to eliminate the loss.

D) industry demand falls, eliminating the economic profit.

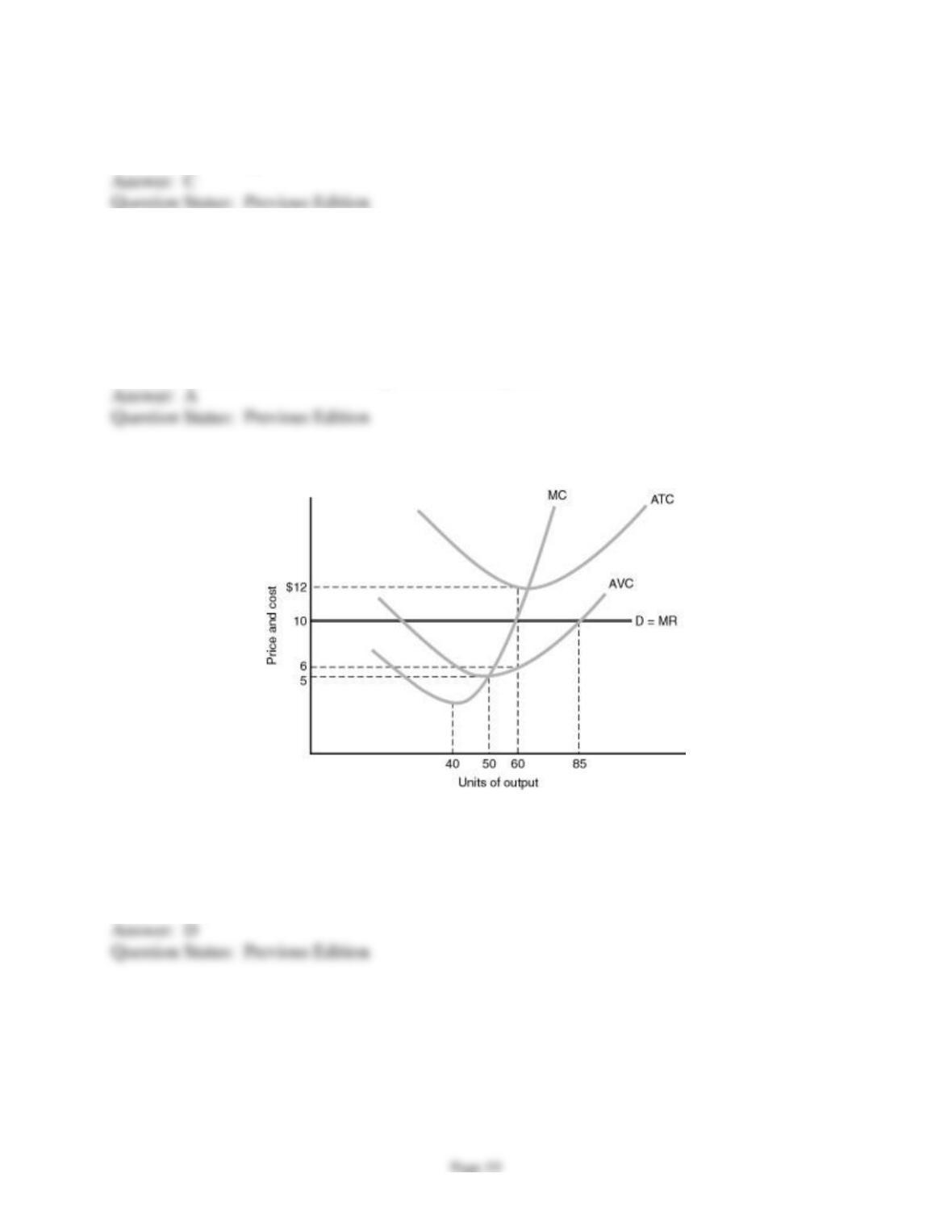

Use the diagram found below in answering the following question(s).

22) Based on the figure above, this firm should

A) shut down in order to minimize its loss.

B) produce 40 units in order to minimize its loss.

C) produce 50 units in order to minimize its loss.

D) produce 60 units in order to minimize its loss.

Page 20

23) Based on the figure above, if this firms shuts down, it will lose

A) $720.

B) $360.

C) $250.

D) $120.

24) Based on the figure above, if this firm continues to produce, it will lose

A) $720.

B) $360.

C) $250.

D) $120.

25) Based on the figure above, if the firm's average variable cost curve were above the demand

curve,

A) it would be in long-run equilibrium.

B) it would be earning a normal profit.

C) it would be incurring a loss, but should continue to operate.

D) it should shut down to minimize its loss.

26) Based on the figure above, according to the competitive model, long-run equilibrium will be

achieved when

A) the market demand increases, raising the selling price.

B) the firms raise the price of their product enough to cover their total costs.

C) firms exit the industry, reducing market supply.

D) the market price falls to $5.

1) Firms in purely competitive industries sell similar, but not necessarily identical products.

2) There are substantial barriers to prevent new firms from entering purely competitive

industries.

3) Purely competitive industries are composed of many small firms selling identical products.

4) Purely competitive firms are described as price takers because they must charge the price

dictated by the government.

Page 21

5) The demand curve facing a purely competitive firm is a horizontal straight line.

6) The demand curve facing a purely competitive firm is perfectly inelastic.

7) Marginal revenue is equal to price for a purely competitive firm.

8) If a purely competitive firm produces at the output where marginal revenue is equal to

marginal cost, it will always earn a profit.

9) If a firm earns zero economic profit it is earning a normal profit.

10) Firms may continue to produce output in the short run even if they are incurring losses.

11) If price is less than average total cost, a firm will incur a loss and should always shut down in

the short run.

12) If price is less than average total cost but greater than average variable cost, the firm should

continue to produce output rather than shutting down.

13) If a purely competitive industry is in long-run equilibrium, an increase in demand will cause

the firms in the industry to reduce their output.

14) If a price taker's demand curve is everywhere below its average total cost curve, it will

always minimize its loss by shutting down and producing no output.

15) If the firms in a purely competitive industry are earning economic profits, additional firms

will enter the industry.

16) In the long run, firms will leave an industry if they cannot earn an economic profit.

17) In the long run, firms will leave an industry if price does not at least cover average total cost.

18) If price falls in a purely competitive industry, the short-run response of the firms in that

industry will be to reduce output or shut down.

19) In the short run, firms will continue to operate at a loss as long as price exceeds average total

cost.

20) If firms in a purely competitive industry are incurring short-run losses, some firms will exit

the industry.

21) When a purely competitive industry is in long-run equilibrium, price will equal average

variable cost for a representative firm.

22) Production efficiency requires that firms produce at the minimum point on marginal cost

curve.

23) Production efficiency occurs when firms produce at minimum average total cost.

24) Achieving allocative efficiency is important because it enables a society to satisfy more

wants.

25) Allocative efficiency means producing each product at minimum average total cost.

26) Allocative efficiency occurs when production continues up to the point where marginal

social benefit equals marginal social cost.

27) If firms produce each produce using as few scarce resources as possible, they are achieving

allocative efficiency.

28) If producers provide us with the proper quantities of the products we desire the most,

allocative efficiency is being achieved.

29) If firms produce each product at minimum cost, but fail to produce the mix of products that

consumers desire they most, they are achieving allocative efficiency but not production

efficiency.

30) A purely competitive industry is composed of a large number relatively small firms selling

identical products and protected by substantial barriers to entry.

31) The price in a purely competitive industry can never change.

32) If the firms in a purely competitive industry are incurring losses, they often respond by

raising the selling price of their product.

33) In the short run, purely competitive firms cannot expand output.

34) The entrance of additional firms into a purely competitive industry is shown by shifting the

industry supply curve to the left.

35) If firms in a purely competitive industry are incurring short-run losses, the long-run

adjustment process will involve the industry supply curve shifting to the right.

1) Suppose that a purely competitive firm chose to operate at the output level where its average

cost (ATC) was at a minimum. Carefully explain why this output is generally not the profit-

maximizing (loss-minimizing) level.

2) Draw the diagrams necessary to show a purely competitive industry and a representative firm

in long-run equilibrium. Use these diagrams to show

(a) the short-run response to an increase in the demand for the industry's product

(b) the process by which long-run equilibrium will be restored.

Fully explain your diagrams.

3) In some instances, firms that are incurring losses decide not to produce any output; in others,

they continue to produce. How do you explain this difference in behavior? Supplement your

answer with the appropriate graphs.

4) Many manufacturing industries are now international, with producers spread throughout the

world. Suppose that computer chip manufacturing is an example of such an industry and that it is

accurately described as purely competitive. Why would U.S. producers be upset if the Chinese

government decided to subsidize its chip producers? What do you think would be the long run

impact of such a policy? (Assume that transportation costs are insignificant for computer chips.)

5) Under conditions of pure competition, when long-run equilibrium is attained P = MC =

Minimum ATC. Explain why this equality is socially desirable.