Introduction to Economic Reasoning, 8e (Rohlf)

Chapter 6: Price Taking: The Purely Competitive Firm

1) Which of the following is not characteristic of a purely competitive industry?

A) a large number of sellers

B) relatively small firms

C) ease of entry into the industry

D) substantial differences in the products of sellers

E) a selling price determined by market forces

2) If a purely competitive firm decided to withhold its entire output from the market,

A) the price of the firm’s product would rise significantly.

B) the price of the firm’s product would fall significantly.

C) the price of the firm’s product would be essentially unchanged.

D) other firms could be counted on to follow the same course of action and drive up price.

E) the price of the firm’s product would fall, but not significantly.

3) The purely competitive firm is a price taker because

A) it produces a very small fraction of total industry output.

B) its product is identical to that offered by other sellers in the industry.

C) there are no substantial barriers to entering the industry.

D) all firms in the industry sell identical products and each firm is too small to significantly alter

total industry output.

E) each firm is large in relation to the total industry.

4) If a purely competitive firm were to raise the price of its product by a small amount, it would

A) lose all of its customers to other sellers in the industry.

B) lose some of its customers but not all of them, since some customers would still prefer its

product.

C) earn a slightly higher profit.

D) force other sellers to raise their prices.

E) earn a much higher profit.

5) Total revenue can be computed by

A) multiplying the selling price of the product by the number of units sold.

B) subtracting total cost from total revenue.

C) multiplying average total cost by the number of units sold.

D) subtracting total variable cost from total revenue.

E) multiplying the profit per unit by the number of units sold.

6) If a firm is earning a normal profit, its owners are

A) earning more than they would have if they had invested in the next best alternative.

B) more than breaking even.

C) also earning an economic profit.

D) breaking even; earning zero economic profit, and earning as much as they would in the next

best alternative investment.

E) breaking even; earning an economic profit, and earning as much as they would in the next

best alternative investment.

7) Suppose George Goforit gives up a $50,000 a year salary and invests $100,000 of his own

money (which had been earning 10 percent a year) to start a business. In order to earn a normal

profit he must make

A) $50,000 a year.

B) at least $50,001.

C) $150,000 a year.

D) $60,000 a year.

E) at least $60,001.

8) In the short run, a purely competitive firm can maximize its profit or minimize its loss by

producing at the level of output where

A) marginal revenue is equal to price.

B) marginal revenue is equal to marginal cost.

C) average total cost is minimized.

D) price exceeds average total cost by the greatest amount.

E) marginal revenue is equal to average variable cost.

9) If, at the present output level, price exceeds marginal cost, the purely competitive firm

A) is maximizing its profit or minimizing its loss.

B) should increase output to maximize its profit or minimize its loss.

C) should reduce output to maximize its profit or minimize its loss.

D) should increase its price to maximize its profit or minimize its loss.

E) is clearly incurring a loss and should leave the industry.

Page 3

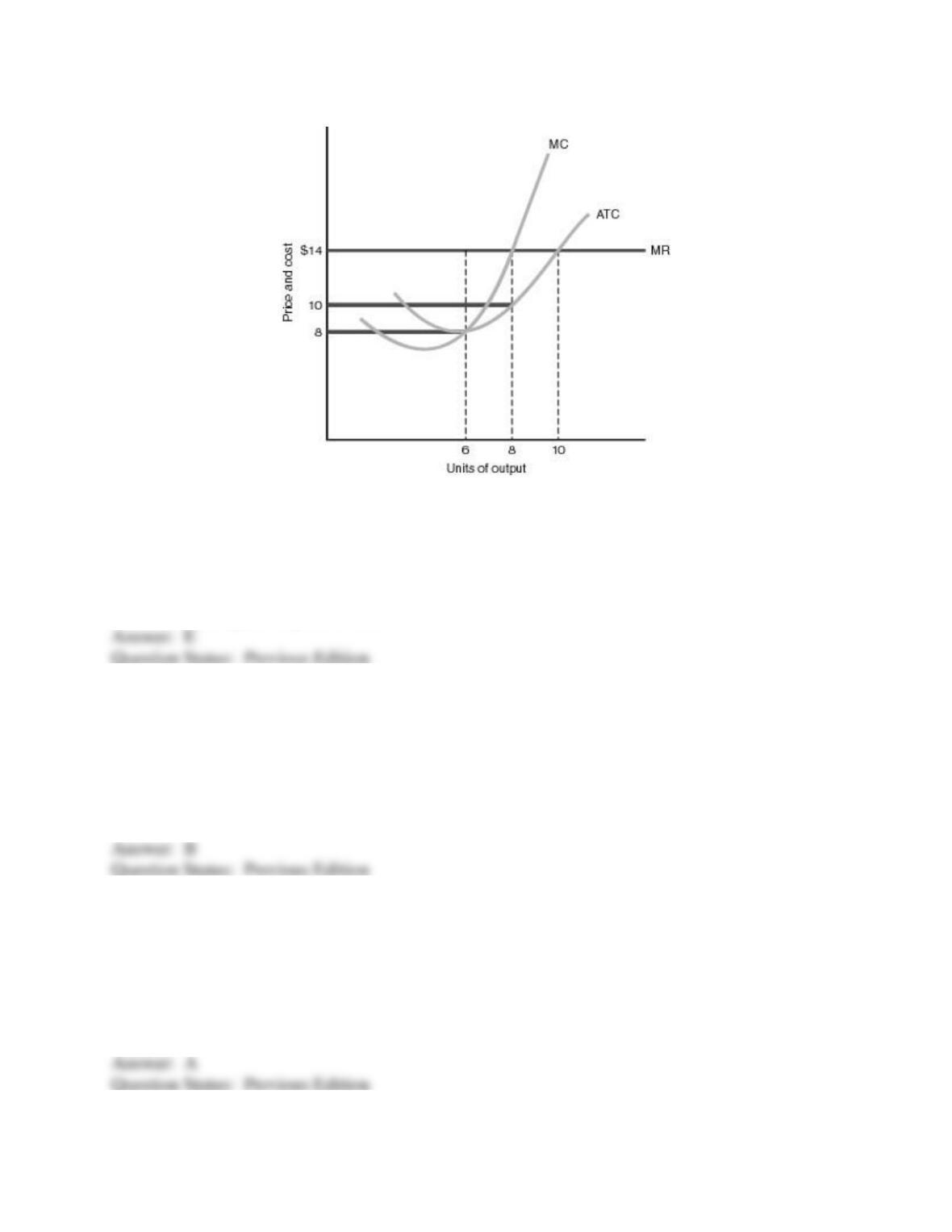

Answer the following question(s) on the basis of the following diagram.

10) Based on the figure above, to maximize its profit or minimize its loss, this firm will produce

A) 6 units of output at a price of $8.

B) 8 units of output at a price of $10.

C) 10 units of output at a price of $14.

D) 6 units of output at a price of $10.

E) 8 units of output at a price of $14.

11) Based on the above figure, at the profit-maximizing (loss-minimizing) output, total revenue

will be

A) $60.

B) $112.

C) $140.

D) $80.

E) $48.

12) Based on the above figure, at the profit-maximizing (loss-minimizing) output, total cost will

be

A) $80.

B) $48.

C) $140.

D) $112.

E) $102.

13) Based on the above figure, this firm will realize

A) a profit of $36.

B) a profit of $32.

C) a profit of $12.

D) a loss of $60.

E) a normal profit.

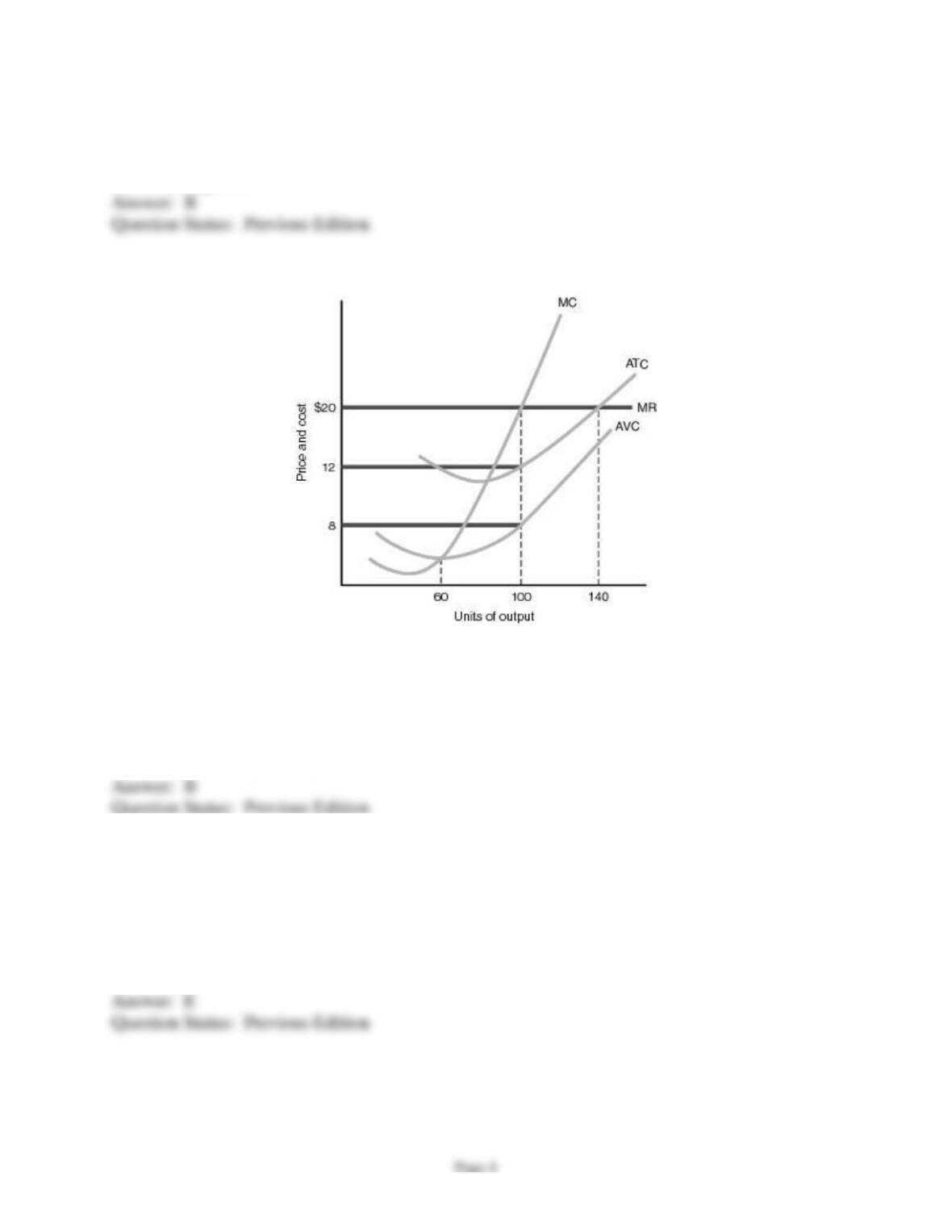

Answer the following question(s) on the basis of the following diagram.

14) Based on the figure above, to maximize its profit or minimize its loss, this firm will produce

A) 60 units of output at a price of $20.

B) 100 units of output at a price of $20.

C) 60 units of output at a price of $12.

D) 140 units of output at a price of $12.

E) 100 units of output at a price of $8.

15) Based on the figure above, at the profit-maximizing (loss-minimizing) output, total revenue

will be

A) $2,800.

B) $800.

C) $1,200.

D) $720.

E) $2,000.

16) Based on the figure above, at the profit-maximizing (loss-minimizing) output, total cost is

equal to

A) $400.

B) $800.

C) $1,200.

D) $2,000.

E) $2,800.

17) Based on the figure above, at the profit-maximizing (loss-minimizing) output, total variable

cost is equal to

A) $400.

B) $800.

C) $1,200.

D) $2,000.

E) $2,800.

18) Based on the figure above, at the profit-maximizing (loss-minimizing) output, average total

cost is equal to

A) $2,000.

B) $1,200.

C) $20.

D) $12.

E) $8.

19) Based on the figure above, at the profit-maximizing (loss-minimizing) output, total fixed cost

is equal to

A) $400.

B) $800.

C) $1,200.

D) $2,000.

E) $2,800.

20) Based on the figure above, this firm will realize

A) a profit of $400.

B) a loss of $400.

C) a profit of $800.

D) a profit of $1,200.

E) a normal profit.

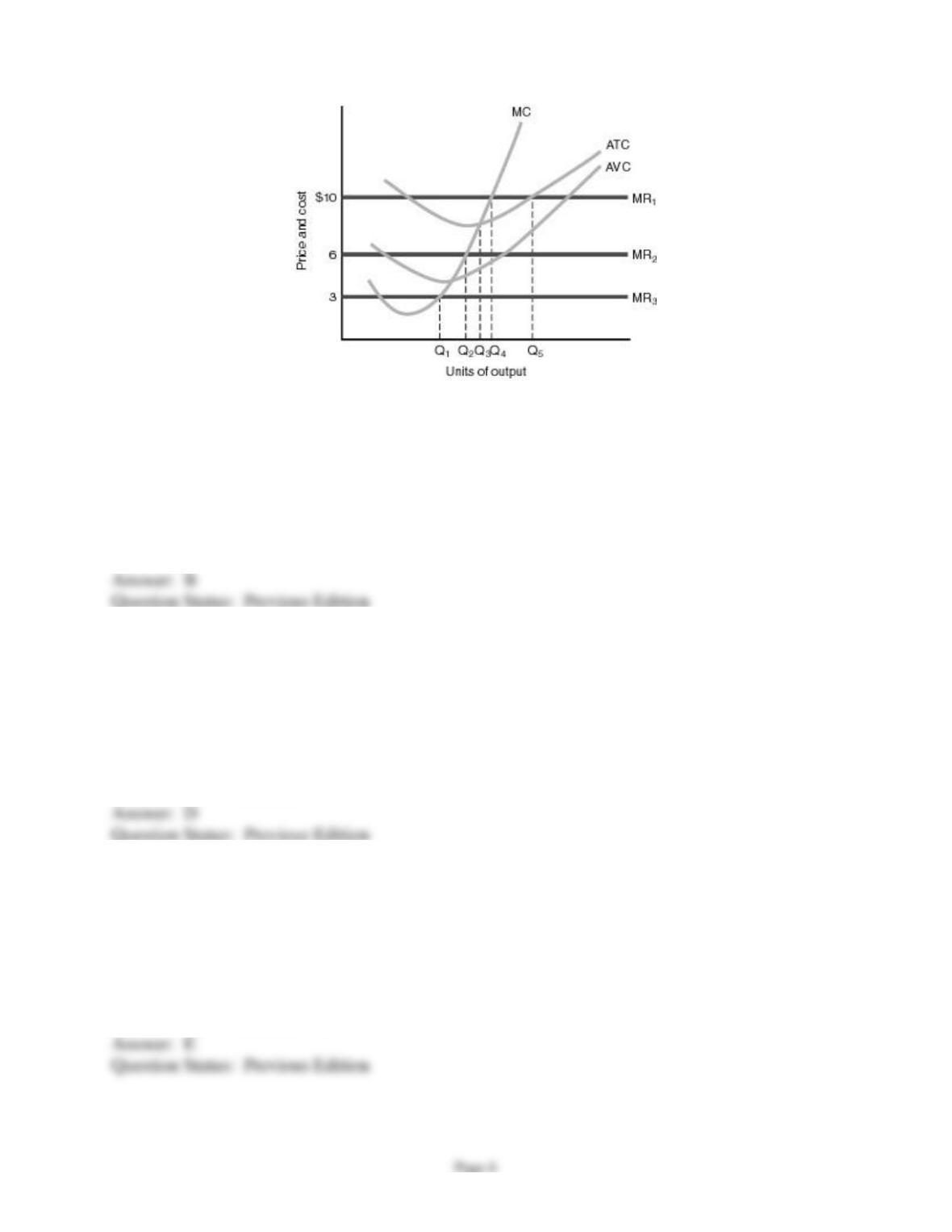

21) Based on the figure above, if the prevailing market price is $10, this purely competitive firm

will

A) produce Q5 units and earn an economic profit.

B) produce Q4 units and earn an economic profit.

C) produce Q3 units and earn a normal profit.

D) produce Q2 units and incur a loss.

E) shut down to minimize its loss.

22) Based on the figure above, if the prevailing market price is $6, this purely competitive firm

will

A) produce Q4 units and earn an economic profit.

B) produce Q3 units and earn an economic profit.

C) produce Q3 units and incur a loss.

D) produce Q2 units and incur a loss.

E) shut down to minimize its loss.

23) Based on the figure above, if the prevailing market price is $3, this purely competitive firm

will

A) produce Q3 units and incur a loss.

B) produce Q1 units and earn a profit.

C) produce Q2 units and incur a loss.

D) produce Q1 units and incur a loss.

E) shut down to minimize its loss.

Page 7

24) If the representative firm in a purely competitive industry earns a profit in the short run, in

the long run

A) industry demand will tend to decline, reducing the market price and eliminating all economic

profit.

B) additional firms will tend to enter the industry, forcing up the market price.

C) additional firms will tend to enter the industry, reducing the market price.

D) firms will tend to leave the industry, increasing the market price.

E) it will continue to earn an economic profit.

25) In pure competition, the representative firm

A) tends to just “break even” in long-run equilibrium.

B) may realize an economic profit, a normal profit, or an economic loss in the long run.

C) will produce at the output where price equals average total cost.

D) will always produce at the output where ATC is minimized.

E) will shut down if it cannot cover all costs of production.

26) Which of the following is false?

A) A normal profit is equivalent to a zero economic profit.

B) If a firm is earning exactly a zero economic profit, its owners are doing as well as they could

have if they had put their money in the next best alternative investment.

C) If a firm is “breaking even,” it is earning an economic profit.

D) If a firm is earning an economic profit, its owners are earning more than they could have

expected to earn in the next best alternative investment.

E) An economic profit exceeds a normal profit.

27) Allocative efficiency requires that production continue up to the point where

A) marginal revenue equals marginal cost.

B) average total cost is at a minimum.

C) marginal social benefit equals marginal social cost.

D) marginal social cost is at a minimum.

E) Both C and D are correct.

28) Under conditions of pure competition, the firm’s supply curve is

A) its average variable cost curve.

B) its average total cost curve.

C) the segment of the marginal cost curve above average variable cost.

D) the segment of the marginal cost curve above average total cost.

E) its average fixed cost curve.

29) Production efficiency has been achieved if the firm is producing at the output where

Page 8

A) MR = MC.

B) P = MC.

C) P = ATC.

D) MR = ATC.

E) ATC is at a minimum.

30) The essence of allocative efficiency is

A) the production of the most-desired products in the proper quantities.

B) production at the lowest average total cost.

C) achieving an economic profit.

D) production at the lowest average variable cost.

E) distributing society’s limited output in the fairest manner possible.

31) Production efficiency is an important goal because

A) it results in long-run economic profits for the competitive firm.

B) it means that the firm is producing the optimal amount of its product.

C) it makes it possible to satisfy more of society’s unlimited wants.

D) it indicates that output is being distributed in a fair or just manner.

E) it ensures that all of society’s wants will be satisfied.

32) When there are no externalities, a purely competitive industry will achieve allocative

efficiency because production occurs up to the point where

A) the market supply and demand curves intersect.

B) marginal social cost equals marginal social benefit.

C) the price of the product is equal to its marginal cost.

D) All of the above.

E) None of the above.

33) Which of the following is true under conditions of pure competition?

A) If the representative firm is incurring a loss in the short run, firms will tend to leave the

industry, pushing price to a lower level.

B) The representative firm must always earn exactly an economic profit in short-run equilibrium.

C) If the representative firm is earning a profit in the short run, market demand will tend to drop,

reducing the industry price.

D) If the representative firm is incurring a loss in the short run, firms will tend to leave the

industry pushing price to a higher level.

E) In the short run, the firm will maximize its profit or minimize its loss by producing at the

output level where average total cost is at a minimum.

34) Under conditions of pure competition, if the representative firm is earning a short-run profit

Page 9

A) additional firms will tend to enter the industry in the long run, shifting the industry supply

curve to the left.

B) firms will tend to leave the industry in the long run, shifting the industry supply curve to the

left.

C) additional firms will tend to enter the industry in the long run, depressing the equilibrium

price.

D) industry demand will tend to decline in the long run until all economic profits have been

eliminated.

E) firms will tend to leave the industry in the long run, increasing the equilibrium price.

35) In the short run, if there is an increase in industry demand in a purely competitive industry

A) additional firms will enter the industry and industry output will expand.

B) the market price will tend to rise, causing the representative firm to expand its output.

C) the demand curve facing the representative firm will shift upward, causing it to cut back on

output.

D) the market price will tend to fall, causing the representative firm to reduce its output.

E) the market price will be unchanged, but the representative firm will tend to expand its output.

36) In the short run, a firm should shut down rather than produce output

A) whenever it cannot cover all of its costs, fixed and variable.

B) whenever it is incurring a loss.

C) if the price it receives for its product is less than average variable cost.

D) if the price it receives for its product is less than average total cost.

E) whenever the firm is unable to cover its fixed costs.

37) In the short run, a firm should shut down rather than produce output

A) whenever total revenue is less than total cost.

B) whenever price is less than average total cost.

C) whenever the loss it incurs by shutting down is less than its total fixed costs.

D) whenever industry demand declines.

E) if it cannot cover all of its costs, fixed and variable.

1) Which of the following statements was made by a person in a purely competitive industry?

A) “We can charge more than our rivals because our product is so much better.”

B) “I think we can count on earning those profits at least until our patent expires.”

C) “If we cut back on our output, we should be able to drive the price up significantly.”

D) “If we don’t charge the same price as everyone else, we’re not going to sell anything.”

2) Is the average pizza restaurant in a large metropolitan area a price taker?

A) Yes; there are a large number of sellers and they all sell the same thing so they must be price

takers

B) No; there are a large number of sellers but they each sell somewhat different products so they

can charge different prices

C) Yes; there are a large number of sellers so it must be easy to enter this industry.

D) No; we can’t live without pizza so these restaurants can charge any price they want.

3) Purely competitive firms are price takers because

A) they are too small to significantly alter market price through their output decisions.

B) they produce identical products and therefore cannot charge a premium for their product.

C) there are no barriers to entering a purely competitive industry.

D) All of the above.

E) Both A and B are correct.

4) Suppose we discover that most dry-cleaning establishments earn something approximating a

normal profit. Economists would attribute this finding to the fact that

A) all dry cleaners provide essentially the same service.

B) it’s relatively easy and inexpensive to start these businesses.

C) there are a large number of these firms.

D) all of the above

5) In pure competition, which of the following is true?

A) The firm’s demand curve is described as perfectly inelastic.

B) The firm’s marginal revenue is equal to the prevailing market price.

C) Firms always earn an economic profit when they are in long-run equilibrium.

D) All of the above.

E) Both B and C and correct.

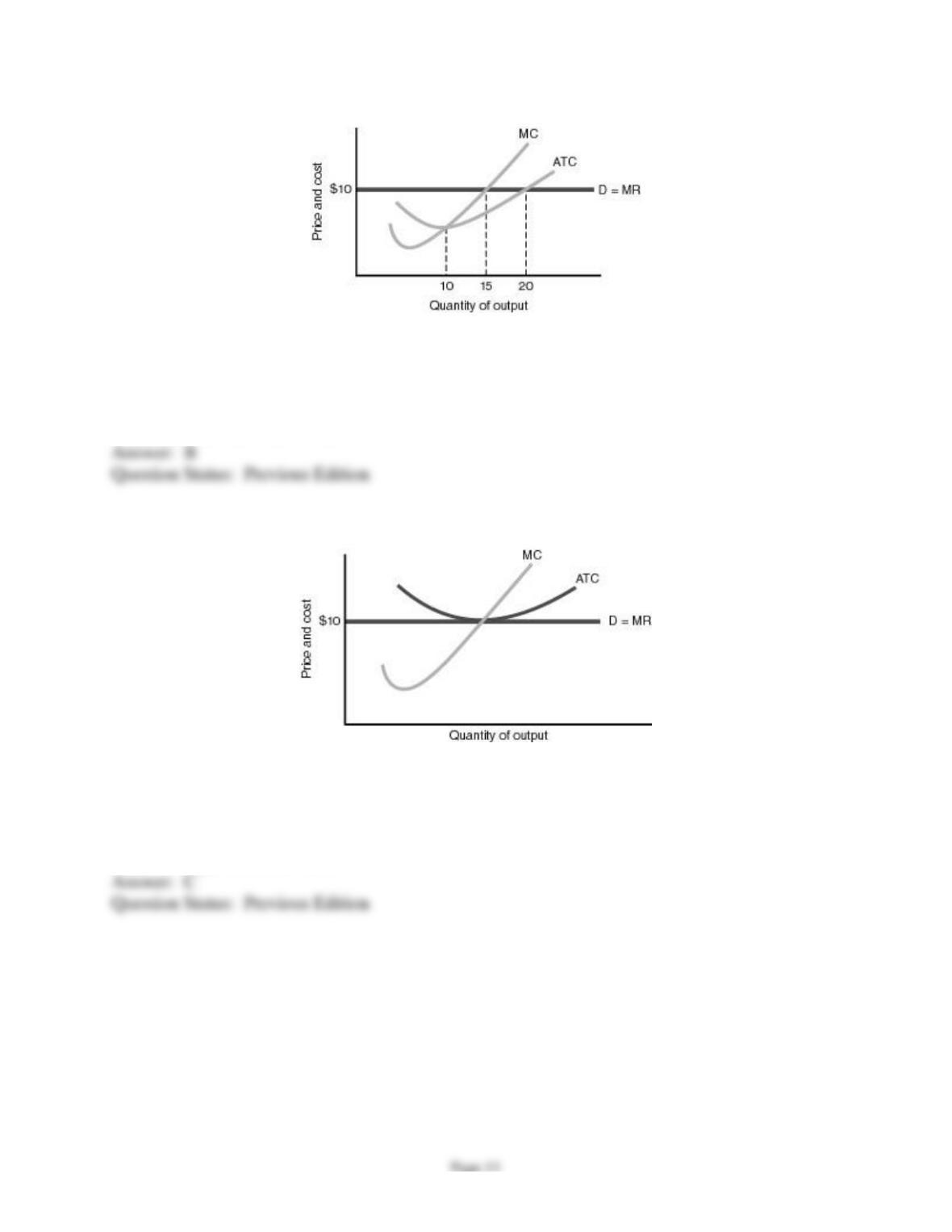

Refer to the following diagram in answering this question.

6) Based on the figure above, the firm depicted should

A) produce 10 units and maximize its profit.

B) produce 15 units and maximize its profit.

C) produce 10 units and minimize its loss.

D) produce 20 units and break even.

Refer to the following diagram in answering this question.

7) Based on the figure above, the firm depicted is

A) facing a loss.

B) making an economic profit.

C) making a normal profit.

D) about to go out of business.

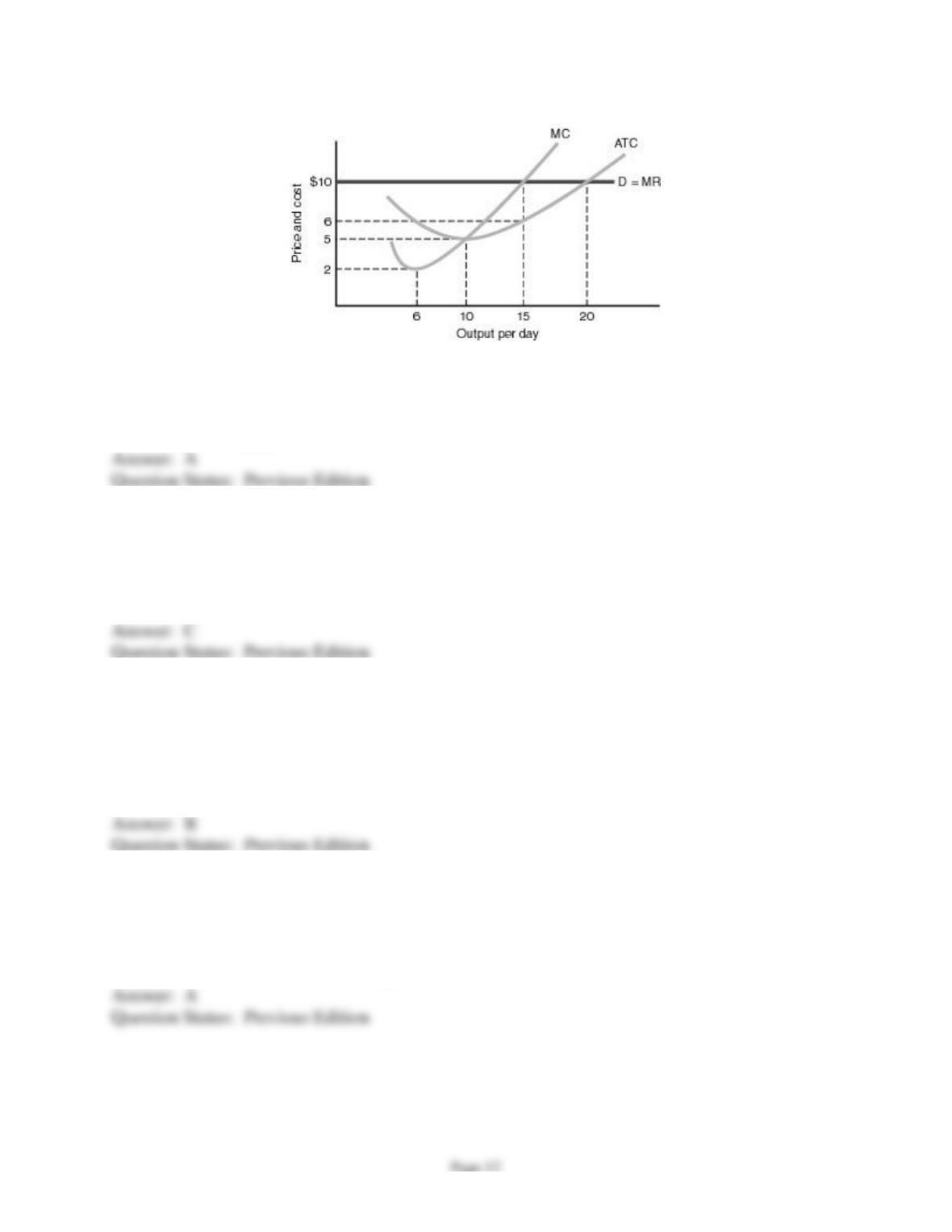

Use the following diagram in answering the following question(s).

8) Based on the figure above, the firm depicted is

A) earning an economic profit.

B) incurring a loss.

C) earning a normal profit.

9) Based on the figure above, the firm’s profit-maximizing (loss-minimizing) output is

A) 6 units.

B) 10 units.

C) 15 units.

D) 20 units.

10) Based on the figure above, by producing the optimal output, this firm will

A) earn a profit of $50.

B) earn a profit of $60.

C) earn of profit of $100.

D) earn a normal profit.

E) incur a loss a $50.

11) Based on the figure above, in the long-run,

A) price will be driven down to $5 by the entrance of additional firms.

B) the price will remain $10 but the firm will earn only a normal profit.

C) firms will exit this industry until the remaining firms earn a normal profit.

D) price will be driven down to $2 by the entrance of additional firms.