Chapter 4 The Market Forces of Supply and Demand

MULTIPLE CHOICE

1. The two words most often used by economists are

a.

prices and quantities.

b.

resources and allocation.

c.

supply and demand.

d.

efficiency and equity.

2. The two words economists use most often are

a.

inflation and trade.

b.

supply and demand.

c.

competition and prices.

d.

markets and equilibrium.

3. The forces that make market economies work are

a.

work and leisure.

b.

politics and religion.

c.

supply and demand.

d.

taxes and government spending.

4. In a market economy, supply and demand determine

a.

both the quantity of each good produced and the price at which it is sold.

b.

the quantity of each good produced but not the price at which it is sold.

c.

the price at which each good is sold but not the quantity of each good produced.

d.

neither the quantity of each good produced nor the price at which it is sold.

5. In a market economy, supply and demand are important because they

a.

play a critical role in the allocation of the economy’s scarce resources.

b.

determine how much of each good gets produced.

c.

can be used to predict the impact on the economy of various events and policies.

d.

All of the above are correct.

2 ❖ Chapter 4/The Market Forces of Supply and Demand

6. In a market economy, supply and demand are important because they

a.

are direct policy tools used by government agencies to regulate the economy.

b.

illustrate when an market is in equilibrium, but they are not helpful when a market is out of

equilibrium.

c.

can be used to predict the impact on the economy of various events and policies.

d.

All of the above are correct.

7. In a market economy,

a.

supply determines demand and demand, in turn, determines prices.

b.

demand determines supply and supply, in turn, determines prices.

c.

the allocation of scarce resources determines prices and prices, in turn, determine supply and

demand.

d.

supply and demand determine prices and prices, in turn, allocate the economy’s scarce resources.

MARKETS AND COMPETITION

1. Which of the following statements is correct?

a.

Buyers determine supply, and sellers determine demand.

b.

Buyers determine demand, and sellers determine supply.

c.

Buyers determine both demand and supply.

d.

Sellers determine both demand and supply.

2. The demand for a good or service is determined by

a.

those who buy the good or service.

b.

the government.

c.

those who sell the good or service.

d.

both those who buy and those who sell the good or service.

3. The supply of a good or service is determined by

a.

those who buy the good or service.

b.

the government.

c.

those who sell the good or service.

d.

both those who buy and those who sell the good or service.

Chapter 4/The Market Forces of Supply and Demand ❖ 3

4. A group of buyers and sellers of a particular good or service is called a(n)

a.

coalition.

b.

economy.

c.

market.

d.

competition.

5. For a market for a good or service to exist, there must be a

a.

group of buyers and sellers.

b.

specific time and place at which the good or service is traded.

c.

high degree of organization present.

d.

All of the above are correct.

6. Which of the following is an example of a market?

a.

a gas station

b.

a garage sale

c.

a barber shop

d.

All of the above are examples of markets.

7. The market for ice cream is a

a.

monopolistic market.

b.

highly competitive market.

c.

highly organized market.

d.

Both b) and c) are correct.

8. Most markets in the economy are

a.

markets in which sellers, rather than buyers, control the price of the product.

b.

markets in which buyers, rather than sellers, control the price of the product.

c.

perfectly competitive.

d.

highly competitive.

9. A market includes

a.

buyers only.

b.

sellers only.

c.

both buyers and sellers.

d.

the place where transactions occur but not the people involved.

4 ❖ Chapter 4/The Market Forces of Supply and Demand

10. Which of the following is not an example of a market?

a.

A small town has only one seller of electricity.

b.

In the United States, a sick person cannot legally purchase a kidney.

c.

In Florida, there are many buyers and sellers of key lime pie.

d.

The availability of Internet shopping has expanded the clothing choices for buyers who do not live

near large cities.

11. In a competitive market, the price of a product

a.

is determined by buyers, and the quantity of the product produced is determined by sellers.

b.

is determined by sellers, and the quantity of the product produced is determined by buyers.

c.

and the quantity of the product produced are both determined by sellers.

d.

None of the above is correct.

12. In a competitive market, the quantity of a product produced and the price of the product are determined by

a.

buyers.

b.

sellers.

c.

both buyers and sellers.

d.

None of the above is correct.

13. In a competitive market, the quantity of a product produced and the price of the product are determined by

a.

a single buyer.

b.

a single seller.

c.

one buyer and one seller working together.

d.

all buyers and all sellers.

14. A competitive market is a market in which

a.

an auctioneer helps set prices and arrange sales.

b.

there are only a few sellers.

c.

the forces of supply and demand do not apply.

d.

no individual buyer or seller has any significant impact on the market price.

15. A competitive market is one in which there

a.

is only one seller, but there are many buyers.

b.

are many sellers, and each seller has the ability to set the price of his product.

c.

are many sellers, and they compete with one another in such a way that some sellers are always

being forced out of the market.

d.

are so many buyers and so many sellers that each has a negligible impact on the price of the

product.

Chapter 4/The Market Forces of Supply and Demand ❖ 5

16. Assume Diana buys computers in a competitive market. It follows that

a.

Diana has a limited number of sellers to turn to when she buys a computer.

b.

Diana will find herself negotiating with sellers whenever she buys a computer.

c.

if Diana buys a large number of computers, the price of computers will rise noticeably.

d.

None of the above is correct.

17. In a competitive market, each seller has limited control over the price of his product because

a.

other sellers are offering similar products.

b.

buyers exert more control over the price than do sellers.

c.

these markets are highly regulated by the government.

d.

sellers usually agree to set a common price that will allow each seller to earn a comfortable profit.

18. For a competitive market,

a.

a seller can always increase her profit by raising the price of her product.

b.

if a seller charges more than the going price, buyers will go elsewhere to make their purchases.

c.

a seller often charges less than the going price to increase sales and profit.

d.

a single buyer can influence the price of the product but only when purchasing from several sellers

in a short period of time.

19. If a seller in a competitive market chooses to charge more than the going price, then

a.

the sellers’ profits must increase.

b.

the owners of the raw materials used in production would raise the prices for the raw materials.

c.

other sellers would also raise their prices.

d.

buyers will make purchases from other sellers.

20. In competitive markets, buyers

a.

are price takers, but sellers are price setters.

b.

are price setters, but sellers are price takers.

c.

and sellers are price takers.

d.

and sellers are price setters.

21. The term price takers refers to buyers and sellers in

a.

perfectly competitive markets.

b.

monopolistic markets.

c.

markets that are regulated by the government.

d.

markets in which buyers cannot buy all they want and/or sellers cannot sell all they want.

6 ❖ Chapter 4/The Market Forces of Supply and Demand

22. In competitive markets,

a.

firms produce identical products.

b.

no individual buyer can influence the market price.

c.

no individual seller can influence the market price.

d.

All of the above are correct.

23. In competitive markets, which of the following is not correct?

a.

Firms produce identical products.

b.

No individual buyer can influence the market price.

c.

Some sellers can set prices.

d.

Buyers are price takers.

24. In competitive markets,

a.

firms produce identical products.

b.

buyers can influence the market price more easily than sellers.

c.

markets are more likely to be in equilibrium.

d.

sellers are price setters.

25. The highest form of competition is called

a.

absolute competition.

b.

cutthroat competition.

c.

perfect competition.

d.

market competition.

26. The highest form of competition is called

a.

arbitrage.

b.

monopolistic competition.

c.

equilibrium.

d.

perfect competition.

27. Which of the following is not a characteristic of a perfectly competitive market?

a.

Different sellers sell identical products.

b.

There are many sellers.

c.

Sellers must accept the price the market determines.

d.

All of the above are characteristics of a perfectly competitive market.

Chapter 4/The Market Forces of Supply and Demand ❖ 7

28. Which of the following is not a characteristic of a perfectly competitive market?

a.

Sellers set the price of the product.

b.

There are many sellers.

c.

Buyers must accept the price the market determines.

d.

All of the above are characteristics of a perfectly competitive market.

29. Buyers and sellers who have no influence on market price are referred to as

a.

market pawns.

b.

monopolists.

c.

price takers.

d.

price setters.

30. When all market participants are price takers who have no influence over prices, the markets have

a.

only a few buyers and sellers.

b.

numerous sellers but only a few buyers.

c.

numerous buyers but only a few sellers.

d.

numerous buyers and sellers.

31. If buyers and sellers in a certain market are price takers, then individually

a.

they have no influence on market price.

b.

they have some influence on market price but that influence is limited.

c.

buyers will be able to find prices lower than those determined in the market.

d.

sellers will find it difficult to sell all they want to sell at the market price.

32. In a perfectly competitive market, at the market price, buyers

a.

cannot buy all they want, and sellers cannot sell all they want.

b.

cannot buy all they want, but sellers can sell all they want.

c.

can buy all they want, but sellers cannot sell all they want.

d.

can buy all they want, and sellers can sell all they want.

33. An example of a perfectly competitive market would be the

a.

cable TV market.

b.

soybean market.

c.

breakfast cereal market.

d.

shampoo market.

8 ❖ Chapter 4/The Market Forces of Supply and Demand

34. An example of a perfectly competitive market would be the market for

a.

tennis racquets.

b.

pizza.

c.

garbage collection.

d.

wheat.

35. An example of a perfectly competitive market would be the market for

a.

electricity.

b.

soybeans.

c.

coffee shops.

d.

restaurants.

36. Which of the following is the least likely to be a competitive market?

a.

ice cream

b.

soybeans

c.

cable television

d.

new houses

37. Assume the market for tennis balls is perfectly competitive. When one tennis ball producer exits the market,

a.

the price of tennis balls increases.

b.

the price of tennis balls decreases.

c.

the price of tennis balls does not change.

d.

there is no longer a market for tennis balls.

38. Assume the market for pork is perfectly competitive. When one pork buyer exits the market,

a.

the price of pork increases.

b.

the price of pork decreases.

c.

the price of pork does not change.

d.

there is no longer a market for pork.

Chapter 4/The Market Forces of Supply and Demand ❖ 9

39. Which of the following is not a reason perfect competition is a useful simplification, despite the diversity of

market types we find in the world?

a.

Perfectly competitive markets are the easiest to analyze because everyone participating in the

market takes the price as given by market conditions.

b.

Some degree of competition is present in most markets.

c.

There are many buyers and many sellers in all types of markets.

d.

Many of the lessons that we learn by studying supply and demand under perfect competition apply

in more complicated markets as well.

40. If a firm is a price taker, it operates in a

a.

competitive market.

b.

monopoly market.

c.

oligopoly market.

d.

monopolistically competitive market.

41. A monopoly is a market with one

a.

seller, and that seller is a price taker.

b.

seller, and that seller sets the price.

c.

buyer, and that buyer is a price taker.

d.

buyer, and that buyer sets the price.

42. Which of the following would most likely serve as an example of a monopoly?

a.

a bakery in a large city

b.

a bank in a large city

c.

a local cable television company

d.

a small group of corn farmers

43. Which of the following would most likely serve as an example of a monopoly?

a.

a restaurant in a large city

b.

a dry cleaners in a large city

c.

a local gas station

d.

a local electrical company

DEMAND

1. The quantity demanded of a good is the amount that buyers are

a.

willing to purchase.

b.

willing and able to purchase.

c.

willing, able, and need to purchase.

d.

able to purchase.

10 ❖ Chapter 4/The Market Forces of Supply and Demand

2. An increase in quantity demanded

a.

results in a movement downward and to the right along a demand curve.

b.

results in a movement upward and to the left along a demand curve.

c.

shifts the demand curve to the left.

d.

shifts the demand curve to the right.

3. A decrease in quantity demanded

a.

results in a movement downward and to the right along a demand curve.

b.

results in a movement upward and to the left along a demand curve.

c.

shifts the demand curve to the left.

d.

shifts the demand curve to the right.

4. A movement upward and to the left along a demand curve is called a(n)

a.

increase in demand.

b.

decrease in demand.

c.

decrease in quantity demanded.

d.

increase in quantity demanded.

5. A movement downward and to the right along a demand curve is called a(n)

a.

increase in demand.

b.

decrease in demand.

c.

decrease in quantity demanded.

d.

increase in quantity demanded.

6. An increase in the price of a good will

a.

increase demand.

b.

decrease demand.

c.

increase quantity demanded.

d.

decrease quantity demanded.

7. A decrease in the price of a good will

a.

increase demand.

b.

decrease demand.

c.

increase quantity demanded.

d.

decrease quantity demanded.

Chapter 4/The Market Forces of Supply and Demand ❖ 11

8. When the price of a good or service changes,

a.

the supply curve shifts in the opposite direction.

b.

the demand curve shifts in the opposite direction.

c.

the demand curve shifts in the same direction.

d.

there is a movement along a given demand curve.

9. A decrease in the price of a good would

a.

increase the supply of the good.

b.

increase the quantity demanded of the good.

c.

give producers an incentive to produce more to keep profits from falling.

d.

shift the supply curve for the good to the left.

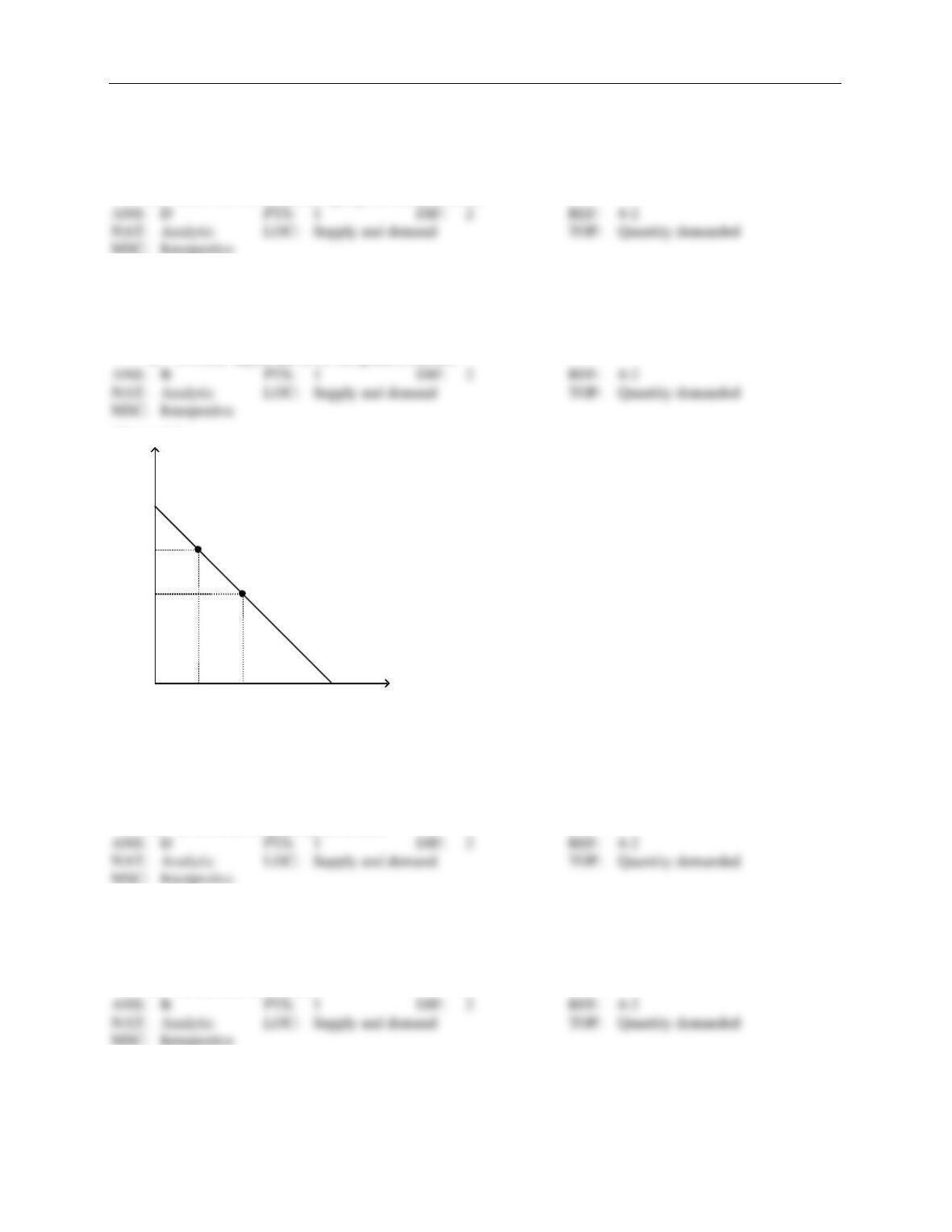

Figure 4-1

D

P

P’

QQ’

A

B

quantity

price

10. Refer to Figure 4-1. The movement from point A to point B on the graph shows

a.

a decrease in demand.

b.

an increase in demand.

c.

a decrease in quantity demanded.

d.

an increase in quantity demanded.

11. Refer to Figure 4-1. The movement from point A to point B on the graph is caused by

a.

an increase in price.

b.

a decrease in price.

c.

a decrease in the price of a substitute good.

d.

an increase in income.

12 ❖ Chapter 4/The Market Forces of Supply and Demand

12. Refer to Figure 4-1. It is apparent from the figure that the

a.

good is inferior.

b.

demand for the good decreases as income increases.

c.

demand for the good conforms to the law of demand.

d.

All of the above are correct.

13. “Other things equal, when the price of a good rises, the quantity demanded of the good falls, and

when the price falls, the quantity demanded rises.” This relationship between price and quantity demanded

a.

applies to most goods in the economy.

b.

is represented by a downward-sloping demand curve.

c.

is referred to as the law of demand.

d.

All of the above are correct.

14. “Other things equal, when the price of a good rises, the quantity demanded of the good falls, and

when the price falls, the quantity demanded rises.” This relationship between price and quantity demanded is

referred to as

a.

equilibrium.

b.

the law of demand.

c.

the relationship between supply and demand.

d.

the definition of an inferior good.

15. The law of demand states that, other things equal, when the price of a good

a.

falls, the demand for the good rises.

b.

rises, the quantity demanded of the good rises.

c.

rises, the demand for the good falls.

d.

falls, the quantity demanded of the good rises.

16. The law of demand states that, other things equal, an increase in

a.

price causes quantity demanded to increase.

b.

price causes quantity demanded to decrease.

c.

quantity demanded causes price to increase.

d.

quantity demanded causes price to decrease.

17. Which of these statements best represents the law of demand?

a.

When buyers’ tastes for a good increase, they purchase more of the good.

b.

When income levels increase, buyers purchase more of most goods.

c.

When the price of a good decreases, buyers purchase more of the good.

d.

When buyers’ demands for a good increase, the price of the good increases.

Chapter 4/The Market Forces of Supply and Demand ❖ 13

18. A downward-sloping demand curve illustrates

a.

that demand decreases over time.

b.

that prices fall over time.

c.

the relationship between income and quantity demanded.

d.

the law of demand.

19. Nemo rents 5 movies per month when the price is $3.00 per rental and 7 movies per month when the price is

$2.50 per rental. Nemo’s demand demonstrates the law of

a.

price.

b.

supply.

c.

demand.

d.

income.

20. Which of the following demonstrates the law of demand?

a.

After Jon got a raise at work, he bought more pretzels at $1.50 per pretzel than he did before his

raise.

b.

Melissa buys fewer muffins at $0.75 per muffin than at $1 per muffin, other things equal.

c.

Dave buys more donuts at $0.25 per donut than at $0.50 per donut, other things equal.

d.

Kendra buys fewer Snickers at $0.60 per Snickers after the price of Milky Ways falls to $0.50 per

Milky Way.

21. The following table contains a demand schedule for a good.

Price

Quantity Demanded

$10

100

$20

Q1

If the law of demand applies to this good, then Q1 could be

a.

0.

b.

100.

c.

200.

d.

400.

22. If the price of apple pies rose to $100 per pie, consumers would purchase fewer pies than if the price were $5

per pie. If the price of ice cream fell to $0.30 per scoop, consumers would purchase more ice cream than if the

price were $5 per scoop. These relationships illustrate the

a.

law of demand.

b.

law of supply.

c.

difference between normal and inferior goods.

d.

difference between substitute and complement goods.

14 ❖ Chapter 4/The Market Forces of Supply and Demand

23. A table that shows the relationship between the price of a good and the quantity demanded of that good is

called a

a.

price-quantity schedule.

b.

buyer schedule.

c.

demand schedule.

d.

demand curve.

24. A demand schedule is a table that shows the relationship between

a.

quantity demanded and quantity supplied.

b.

income and quantity demanded.

c.

price and quantity demanded.

d.

price and income.

25. Which of the following is not held constant in a demand schedule?

a.

income

b.

tastes

c.

price

d.

expectations

26. The demand curve for a good is a line that relates

a.

price and quantity demanded.

b.

income and quantity demanded.

c.

quantity demanded and quantity supplied.

d.

price and income.

27. The line that relates the price of a good and the quantity demanded of that good is called the demand

a.

schedule, and it usually slopes upward.

b.

schedule, and it usually slopes downward.

c.

curve, and it usually slopes upward.

d.

curve, and it usually slopes downward.

Chapter 4/The Market Forces of Supply and Demand ❖ 15

28. When drawing a demand curve,

a.

demand is measured along the vertical axis, and price is measured along the horizontal axis.

b.

quantity demanded is measured along the vertical axis, and price is measured along the horizontal

axis.

c.

price is measured along the vertical axis, and demand is measured along the horizontal axis.

d.

price is measured along the vertical axis, and quantity demanded is measured along the horizontal

axis.

29. When we move along a given demand curve,

a.

only price is held constant.

b.

income and price are held constant.

c.

all nonprice determinants of demand are held constant.

d.

all determinants of quantity demanded are held constant.

30. Once the demand curve for a product or service is drawn, it

a.

remains stable over time.

b.

can shift either rightward or leftward.

c.

is possible to move along the curve, but the curve will not shift.

d.

tends to become steeper over time.

31. If something happens to alter the quantity demanded at any given price, then

a.

the demand curve becomes steeper.

b.

the demand curve becomes flatter.

c.

the demand curve shifts.

d.

we move along the demand curve.

32. When quantity demanded decreases at every possible price, the demand curve has

a.

shifted to the left.

b.

shifted to the right.

c.

not shifted; rather, we have moved along the demand curve to a new point on the same curve.

d.

not shifted; rather, the demand curve has become flatter.

33. When quantity demanded increases at every possible price, the demand curve has

a.

shifted to the left.

b.

shifted to the right.

c.

not shifted; rather, we have moved along the demand curve to a new point on the same curve.

d.

not shifted; rather, the demand curve has become steeper.

16 ❖ Chapter 4/The Market Forces of Supply and Demand

34. The market demand curve

a.

is found by vertically adding the individual demand curves.

b.

slopes upward.

c.

represents the sum of the prices that all the buyers are willing to pay for a given quantity of the

good.

d.

represents the sum of the quantities demanded by all the buyers at each price of the good.

35. The market demand curve

a.

is the sum of all individual demand curves.

b.

is the demand curve for every product in an industry.

c.

shows the average quantity demanded by individual demanders at each price.

d.

is always flatter than an individual demand curve.

36. To obtain the market demand curve for a product, sum the individual demand curves

a.

vertically.

b.

diagonally.

c.

horizontally.

d.

and then average them.

37. A market demand curve shows

a.

the relationship between price and the number of buyers in a market.

b.

how quantity demanded changes when the number of sellers changes.

c.

the sum of all prices that individual buyers are willing and able to pay for each possible quantity of

the good.

d.

how much of a good all buyers are willing and able to buy at each possible price.

38. A market demand curve shows how the total quantity demanded of a good varies as

a.

income varies.

b.

price varies.

c.

price of the nearest substitute good varies.

d.

supply varies.

Chapter 4/The Market Forces of Supply and Demand ❖ 17

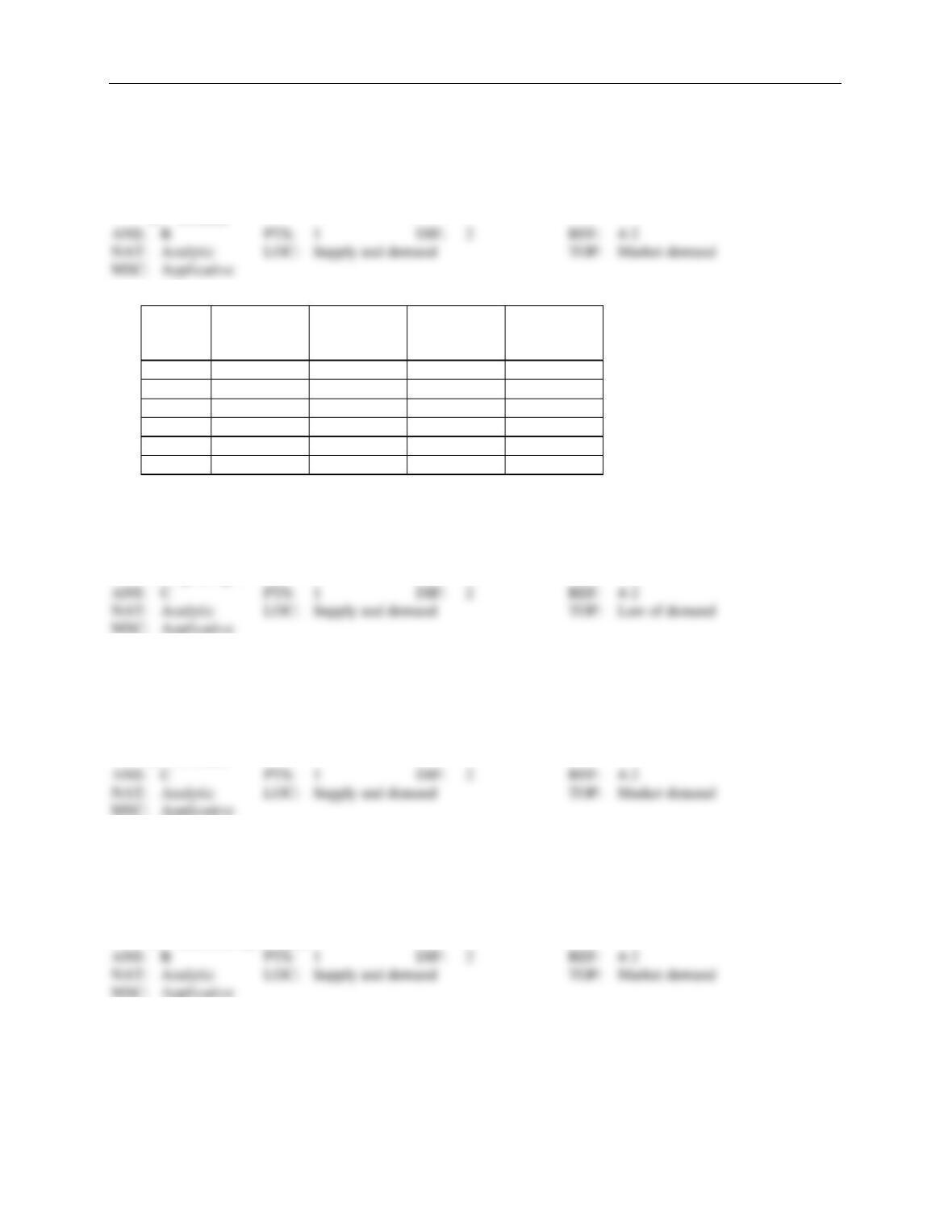

Table 4-1

Price

Quantity Demanded

by Michelle

Quantity Demanded

by Laura

Quantity Demanded

by Hillary

$5

5

4

11

$4

6

6

13

$3

7

8

15

$2

8

10

17

$1

9

12

19

$0

10

14

21

39. Refer to Table 4-1. If the market consists of Michelle, Laura, and Hillary and the price falls by $1, the quan-

tity demanded in the market increases by

a.

2 units.

b.

3 units.

c.

4 units.

d.

5 units.

40. Refer to Table 4-1. If the market consists of Michelle and Laura only and the price falls by $1, the quantity

demanded in the market increases by

a.

2 units.

b.

3 units.

c.

4 units.

d.

5 units.

41. Refer to Table 4-1. If the market consists of Michelle and Hillary only and the price falls by $1, the quantity

demanded in the market increases by

a.

2 units.

b.

3 units.

c.

4 units.

d.

5 units.

42. Refer to Table 4-1. If the market consists of Laura and Hillary only and the price falls by $1, the quantity

demanded in the market increases by

a.

2 units.

b.

3 units.

c.

4 units.

d.

5 units.

18 ❖ Chapter 4/The Market Forces of Supply and Demand

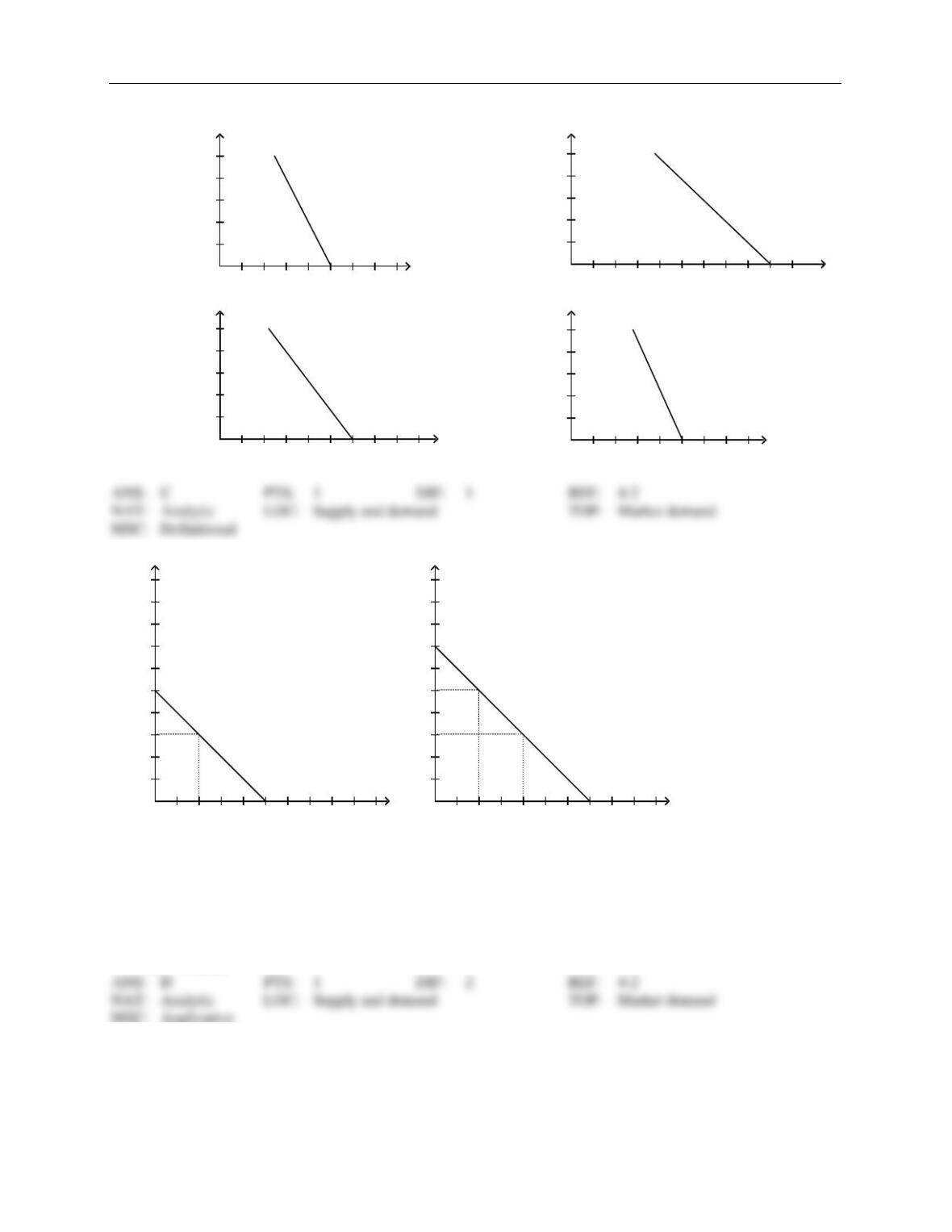

43. Refer to Table 4-1. Which of the following illustrates the market demand curve?

a.

Demand A

2 4 6 8 10 12 Quantity

1

2

3

4

5

Price

c.

Demand C

510 15 20 25 30 35 40 45 Quantity

1

2

3

4

5

Price

b.

Demand B

4 8 12 16 20 24 28 Quantity

1

2

3

4

5

Price

d.

Demand D

510 15 20 25 30 Quantity

1

2

3

4

5

Price

Figure 4-2

D1

Consumer A

246810 12 14 16 Quantity

2

4

6

8

10

12

14

16

18

20 Price

D2

Consumer B

246810 12 14 16 Quantity

2

4

6

8

10

12

14

16

18

20 Price

44. Refer to Figure 4-2. If Consumer A and Consumer B are the only consumers in the market, then the market

quantity demanded when the price is $6 is

a.

4 units.

b.

6 units.

c.

8 units.

d.

12 units.

Chapter 4/The Market Forces of Supply and Demand ❖ 19

45. Refer to Figure 4-2. If Consumer A and Consumer B are the only consumers in the market, then the market

quantity demanded when the price is $10 is

a.

0 units.

b.

4 units.

c.

10 units.

d.

12 units.

Table 4-2

Price

William’s

Quantity

Demanded

Fergie’s

Quantity

Demanded

Taboo’s

Quantity

Demanded

apl.de.ap’s

Quantity

Demanded

$12

2

1

3

4

$10

4

4

4

5

$8

6

7

5

6

$6

8

8

4

7

$4

10

9

3

8

$2

12

10

2

9

46. Refer to Table 4-2. Whose demand does not obey the law of demand?

a.

William’s

b.

Fergie’s

c.

Taboo’s

d.

apl.de.ap’s

47. Refer to Table 4-2. If these are the only four buyers in the market, then the market quantity demanded at a

price of $8 is

a.

4 units.

b.

6 units.

c.

24 units.

d.

32 units.

48. Refer to Table 4-2. If these are the only four buyers in the market, then when the price decreases from $6 to

$4, the market quantity demanded

a.

increases by 0.75 units.

b.

increases by 3 units.

c.

increases by 8 units.

d.

decreases by 27 units.

20 ❖ Chapter 4/The Market Forces of Supply and Demand

Figure 4-3

Consumer 1

Consumer 2

D

246810 12 14 16 quantity

2

4

6

8

10

12

14

16

18

20 price

D

510 15 20 25 30 35 40 quantity

3

6

9

12

15

18

21

24

27

30 price

49. Refer to Figure 4-3. If these are the only two consumers in the market, then the market quantity demanded at

a price of $15 is

a.

0 units.

b.

10 units.

c.

15 units.

d.

25 units.

50. Refer to Figure 4-3. If these are the only two consumers in the market, then the market quantity demanded at

a price of $10 is

a.

0 units.

b.

5 units.

c.

8.33 units.

d.

25 units.

51. Refer to Figure 4-3. If these are the only two consumers in the market, then the market quantity demanded at

a price of $6 is

a.

12 units.

b.

14 units.

c.

19 units.

d.

21 units.