Page 1

1.

When currencies are viewed as assets, the price of a currency is its:

A)

interest rate.

B)

exchange rate.

C)

inflation rate.

D)

growth rate.

2.

Explaining exchange rate behavior in the long run assumes that changes in price levels

and real interest rates affect nominal exchange rates so that interest parity and PPP hold.

Short-run deviations from PPP may be explained by an alternative theory called the:

A)

relative PPP approach.

B)

asset approach to exchange rate determination.

C)

long-run equilibrium approach.

D)

law of one price.

3.

When PPP does not hold in the short run, economists have developed an alternative

short-run explanatory theory based on the idea that:

A)

currency values are different from other prices, since currencies are not considered

assets.

B)

currency values are influenced in the short run because they serve as short-term

assets.

C)

currency values will eventually result in PPP over time, so no short-run theory is

needed.

D)

currency values are set by government entities and the IMF so the value often does

not result in PPP.

4.

Which of the following is NOT an assumption of the behavior of exchange rates in the

short run?

A)

The adjustment period involves weeks rather than years.

B)

Market forces are irrelevant and “do not matter.”

C)

Prices of goods adjust slowly and are therefore “sticky.”

D)

Economic actors behave in their own self-interest.

5.

Using the UIP equation to determine the spot exchange rate requires a knowledge of:

I. expected future exchange rates.

II. observed rates of interest.

III. expected returns on foreign deposits.

A)

I and II only

B)

II and III only

C)

I and III only

D)

I, II, and III

Page 2

6.

A key component of the asset approach to exchange rates is being able to accurately

gauge:

A)

the price level.

B)

the rate of inflation.

C)

expected future exchange rates.

D)

the GDP gap.

7.

If the U.S. interest rate is 5% and the interest rate in Germany is 2%, and the euro is

expected to appreciate by 2% over the next year, then investors would:

A)

sell dollars in the spot market.

B)

buy euros.

C)

seek to invest in the United States.

D)

seek to invest in Germany.

8.

Assume that the U.S. interest rate is 5%, the European interest rate is 2%, and the future

expected exchange rate in one year is $1.224.

If the spot rate is $1.16, then the expected dollar return on euro deposits is:

A)

7.52%

B)

5%

C)

3.2%

D)

2%

9.

Assume that the U.S. interest rate is 5%, the European interest rate is 2%, and the future

expected exchange rate in one year is $1.224.

If the spot rate is $1.24, then the expected dollar return on euro deposits is:

A)

4%.

B)

7.1%.

C)

0.71%.

D)

0.129%.

10.

Assume that the U.S. interest rate is 5%, the European interest rate is 2%, and the future

expected exchange rate in one year is $1.224.

At approximately what exchange rate will the returns between the United States and

Europe be equalized?

A)

$1.20

B)

$1.224

C)

$1.188

D)

$1.98

Page 3

11.

According to UIP, when interest rates are equal, the exchange rate of the country’s home

currency is expected to:

A)

fall.

B)

remain constant.

C)

rise.

D)

Not enough information is provided to answer the question.

12.

If UIP holds, the interest rate at home is 4%, and the exchange rate is expected to

depreciate by 3%, then the foreign interest rate is:

A)

1%.

B)

3%.

C)

7%.

D)

12%.

13.

If UIP holds, the foreign interest rate is 10%, and the home currency is expected to

depreciate by 4%, then the home interest rate is:

A)

4%.

B)

6%.

C)

10%.

D)

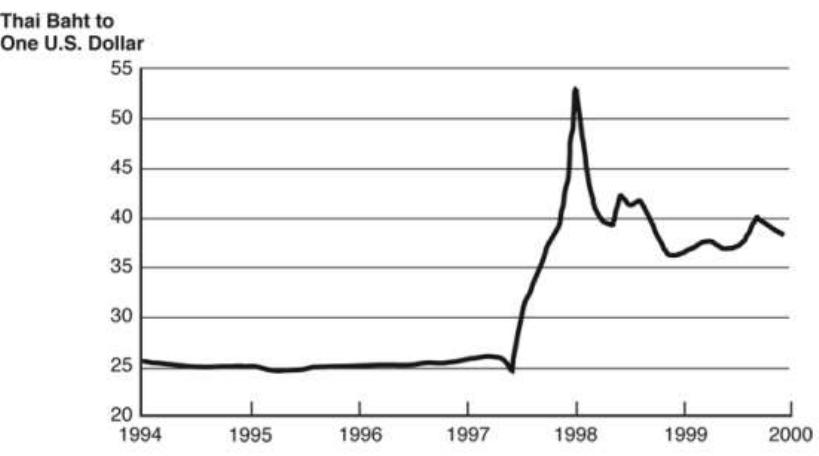

14%.

14.

If UIP holds, the foreign interest rate is 6%, and the home currency is expected to

appreciate by 2%, then the home interest rate is:

A)

10%.

B)

8%.

C)

4%.

D)

3%.

15.

If UIP holds and the home currency is expected to appreciate by 4%, then the home

interest rate is:

A)

6%.

B)

5%.

C)

4%.

D)

Not enough information is provided to answer the question.

Page 4

16.

If UIP holds and if the home currency is expected to depreciate, then:

A)

the home interest rate must be greater than the foreign interest rate.

B)

interest rates cannot be changing.

C)

the home interest rate must be less than the foreign interest rate.

D)

Not enough information is provided to answer the question.

17.

Using the UIP equation to determine the spot exchange rate, assume that the expected

spot rate (after one year) for euros (in terms of dollars) equals $1.50, the current interest

rate on euro deposits is 4.5%, and the current interest rate on dollar deposits is 5.5%.

Which of the following current spot rates would satisfy the equation?

A)

$1.65

B)

$1.50

C)

$1.485

D)

$1.25

18.

If the spot rate for euros depreciates, and all other variables and expected values remain

constant, U.S. investors contemplating European investments would:

A)

get larger returns in terms of dollars.

B)

get smaller returns in terms of dollars.

C)

get very similar returns because of arbitrage.

D)

lose the principal of the investment.

19.

If the domestic dollar return (home nominal interest rate) is 5%, and the foreign nominal

interest rate is 3%, and there is no expected change in future exchange rates, then as the

spot exchange rate depreciates:

A)

the foreign return rises.

B)

the foreign return falls.

C)

the domestic return rises.

D)

the domestic return falls.

20.

When the expected dollar–euro exchange rate rises, the domestic dollar return curve

shifts:

A)

in.

B)

out.

C)

not at all.

D)

Not enough information is provided to answer the question.

Page 5

21.

When expected dollar–euro exchange rates rise, the foreign expected dollar return curve

shifts:

A)

in.

B)

out.

C)

not at all.

D)

Not enough information is provided to answer the question.

22.

When the European interest rate falls, the foreign expected dollar return curve shifts:

A)

in.

B)

out.

C)

not at all.

D)

Not enough information is provided to answer the question.

23.

When the U.S. interest rate falls, the foreign expected dollar return curve shifts:

A)

in.

B)

out.

C)

not at all.

D)

Not enough information is provided to answer the question.

24.

Using the UIP equation, equilibrium in the short run occurs when:

A)

arbitrage is possible.

B)

the spot rate is such that foreign and domestic investment returns are equalized.

C)

the spot rate is less than the forward rate.

D)

foreign interest rates are higher than domestic rates of interest.

25.

If the spot exchange rate is undervalued, the foreign rate of return is:

A)

equal to the domestic rate of return.

B)

greater than the domestic rate of return.

C)

less than the domestic rate of return.

D)

diverging from the domestic rate of return.

26.

Equilibrium, in the short run, is achieved when:

A)

differences in rates of return cause investors to purchase and sell currency and

thereby change the spot rate of exchange.

B)

the government recognizes a problem and takes action to correct it.

C)

traders adjust their expectations to match reality.

D)

inflation falls to zero.

Page 6

27.

Using the UIP equation, what would happen to the spot rate for euros if the interest rate

on U.S. dollar deposits rises, ceteris paribus?

A)

The spot rate to purchase euros would rise (dollar depreciation).

B)

The spot rate to purchase euros would fall (dollar appreciation).

C)

The spot rate to purchase euros would be unchanged.

D)

The U.S. Federal Reserve would have to raise U.S. short-term interest rates.

28.

Using the UIP equation, what would happen to the spot rate for euros if the interest rate

on euro deposits rises, ceteris paribus?

A)

The spot rate to purchase euros would rise (dollar depreciation).

B)

The spot rate to purchase euros would fall (dollar appreciation).

C)

The spot rate to purchase euros would be unchanged.

D)

The U.S. Federal Reserve would have to raise U.S. short-term interest rates.

29.

When exchange rates are not in alignment, traders see opportunities for _____, which

move the rates _____ equilibrium.

A)

speculation; away from

B)

arbitrage; toward

C)

investments; away from

D)

liquidation; toward

30.

Given expectations of future exchange rates, when foreign returns are greater than

domestic returns, investors will ____ domestic assets, _____ domestic currency, ____

foreign currency, and _____ foreign assets.

A)

sell; sell; buy; buy

B)

sell; buy; sell; buy

C)

buy; sell; buy; sell

D)

buy; buy; sell; sell

31.

The asset approach to short-run exchange rate determination relies on which three

variables?

A)

prices, interest rates, and inflation

B)

the reserve ratio, aggregate wealth, and interest rates

C)

nominal domestic rates, foreign interest rates, and expectations of exchange rate

changes

D)

prices, aggregate wealth, and inflation

Page 7

32.

If the U.S. interest rate is 9% and the Eurozone interest rate is 5%, then in the short run

we would expect:

A)

the dollar to appreciate.

B)

the dollar to depreciate.

C)

the euro to appreciate.

D)

There is no change in the exchange rate.

33.

If domestic returns are greater than foreign returns, then:

A)

the spot rate is too high.

B)

the spot rate is too low.

C)

expectations of future exchange rates will change in the long run.

D)

There is no opportunity for arbitrage.

34.

Using the UIP equation, what would happen to the spot rate for euros if the dollar-euro

exchange rate is expected to appreciate in the future?

A)

The spot rate to purchase euros would rise (dollar depreciation).

B)

The spot rate to purchase euros would fall (dollar appreciation).

C)

The spot rate to purchase euros would remain unchanged.

D)

The spot rate to purchase euros would remain unchanged today, but rise in the

future (dollar depreciation).

Page 8

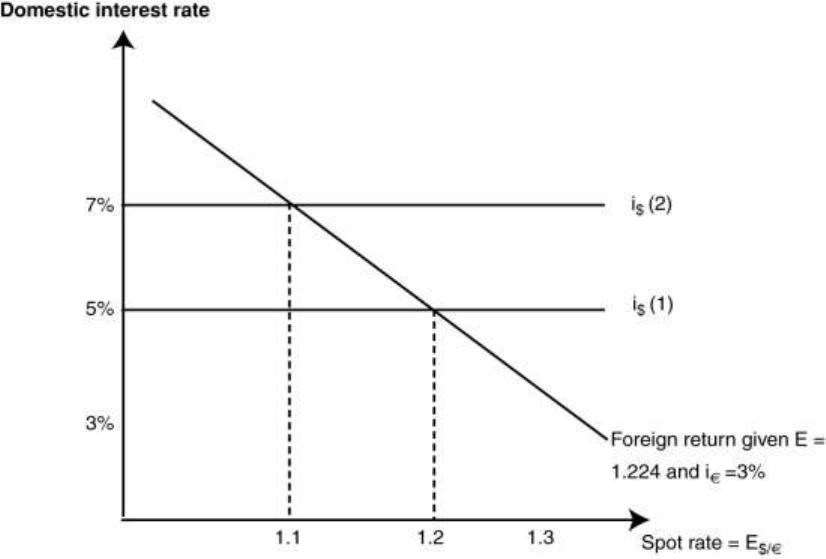

35.

(Figure: The Domestic Interest Rate) Using the graph, if the dollar rate of interest

increases from 5% to 7%, what result will occur in the short run?

A)

Expectations of future exchange rates will change.

B)

U.S. real GDP will fall and the dollar will also fall.

C)

The spot rate for dollars will appreciate to $1.10.

D)

The nominal interest rate on the euro will decrease.

Page 9

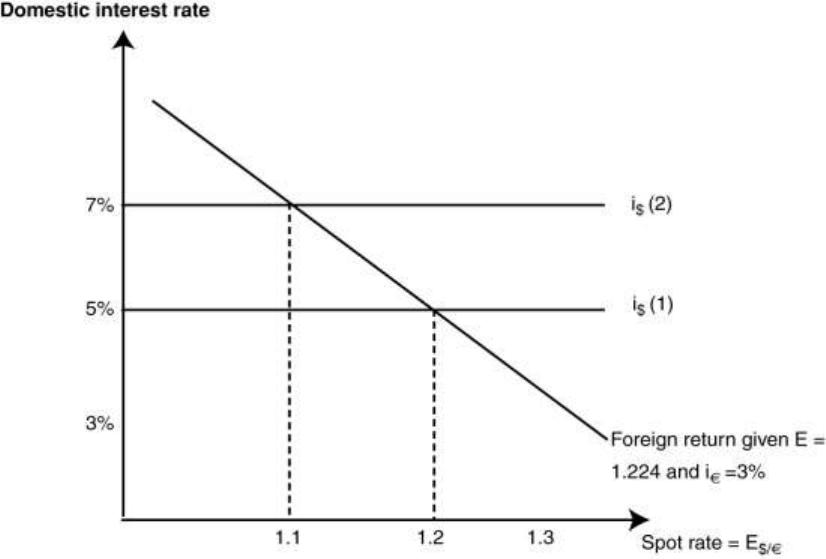

36.

(Figure: The Domestic Interest Rate) Using the graph, if i€ falls, the result is:

A)

the dollar interest rate line shifts up and the spot rate rises.

B)

the dollar interest rate line shifts down and the spot rate rises.

C)

the foreign return line shifts up and to the right and the spot rate rises.

D)

the foreign return line shifts down and to the left and the spot rate falls.

Page 10

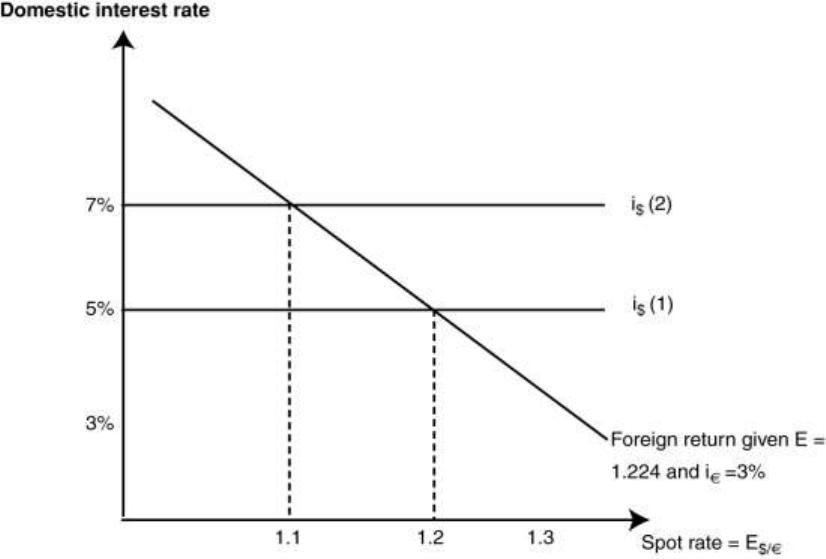

37.

(Figure: The Domestic Interest Rate) Using the graph, if the expected future exchange

rate falls from $1.224 to $1.15:

A)

the dollar interest rate line shifts up and the spot rate rises.

B)

the dollar interest rate line shifts down and the spot rate rises.

C)

the foreign return line shifts up and to the right and the spot rate rises.

D)

the foreign return line shifts down and to the left and the spot rate falls.

38.

What assumptions are made to create a model to determine short-run changes in

exchange rates using the asset approach?

A)

Prices are completely flexible.

B)

In the long run, money is neutral.

C)

Prices are sticky, yet nominal interest rates are flexible.

D)

Prices and nominal interest rates are sticky.

39.

We assume flexible prices in the long run, but whenever it is costly to change prices

(menu costs) or when there are long-term contracts for labor or capital:

A)

short-run prices tend to be flexible.

B)

short-run prices tend to be sticky.

C)

long-run prices tend to be sticky.

D)

firms have to pay higher costs and therefore have to raise prices.

Page 11

40.

The money market (short-run) equilibrium equation states that the demand for real

balances, (L(i)Y) is always equal to the supply of real balances (M/P) because ____

adjust(s) to ensure that people are willing to hold the entire stock.

A)

nominal interest rates

B)

real interest rates

C)

the price level

D)

nominal GDP

41.

Nominal interest rates are considered to be _____ in the short-run model.

A)

flexible

B)

rigid

C)

zero

D)

set by the central bank

42.

In the money market, equilibrium is achieved:

A)

in the long run by the adjustment of interest rates.

B)

in the short run by the adjustment of prices.

C)

in the long run by the adjustment of prices.

D)

in the short run by changes in the money supply.

43.

Nominal rigidity is another term for:

A)

sticky prices.

B)

fixed exchange rates.

C)

menu prices.

D)

the trilemma.

44.

Menu costs are the:

A)

cost of changing interest rates.

B)

cost of converting currencies.

C)

cost of changing prices.

D)

cost of changing exchange rates.

45.

Which of the following are explanations for sticky prices?

A)

long-term labor contracts

B)

fixed exchange rates

C)

flexible exchange rates

D)

fixed money supply

Page 12

46.

A rise in real income will have which of the following effects on money demand?

A)

The money demand curve will shift out.

B)

The money demand curve will not shift at all.

C)

The money demand curve will shift in.

D)

Real income has no effect on money demand.

47.

The demand for real money balances is a function of:

A)

the supply of real money balances.

B)

the nominal GDP.

C)

the nominal rate of interest on alternative assets and the level of real GDP.

D)

policy decisions by the central bank.

48.

In the short run, when the central bank increases the quantity of money, what happens to

real balances?

A)

They do not change, since prices will rise by the same proportion.

B)

They will fall, since prices will rise by a greater proportion.

C)

They will rise, since prices overall will fall.

D)

They will rise, since prices will not change in the short run.

49.

At higher nominal rates of interest, the demand for real balances is:

A)

higher because savers can earn higher returns.

B)

lower because the opportunity cost of holding those funds is higher.

C)

invariant with respect to the nominal interest rate.

D)

inversely related to the price level.

50.

Whenever there is excess demand for real balances, short-run adjustment occurs

because:

A)

savers and investors buy bonds and drive up their prices (drive down nominal rates

of interest).

B)

investors and borrowers sell bonds (convert to cash) and drive down their prices

(drive up nominal rates of interest).

C)

the price level falls to restore real balances.

D)

aggregate demand is decreased to restore equilibrium.

Page 13

51.

The money market clears as people with excess real balances:

A)

buy bonds and drive down nominal rates of interest until the demand for real

balances equals supply.

B)

sell bonds and drive up nominal rates of interest until the demand for real balances

equals supply.

C)

increase spending, driving up nominal GDP and raising nominal rates of interest.

D)

sell financial assets such as stocks to increase the total supply of real balances.

52.

With sticky prices increasing, the supply of money results in:

A)

an increase in the nominal rate of interest.

B)

an increase in the U.S. dollar exchange rate.

C)

a decrease in the nominal rate of interest.

D)

increased price and wage flexibility.

53.

Assuming short-run sticky prices, the same monetary policy result may be achieved by

targeting the money supply or the nominal rate of interest whenever:

A)

the demand for money is stable.

B)

interest income is not taxable.

C)

changes in the supply of money are small and predictable.

D)

real income is constant.

54.

An increase in nominal GDP (with inflexible prices) results in:

A)

an increase in the nominal rate of interest.

B)

an increase in the U.S. dollar exchange rate.

C)

a decrease in the nominal rate of interest.

D)

increased price and wage flexibility.

55.

Normally, whenever the central bank lowers the rate it charges banks for overnight

loans, market rates of interest:

A)

are not affected.

B)

fall at the same rate.

C)

increase.

D)

are unstable.

56.

During the financial crisis of 2007–08, the U.S. central bank lowered its policy rate

from 5.25% to 0%. What was the effect on market rates of interest?

A)

Market rates increased by 5%.

B)

Market rates fell by 5%.

C)

Market rates fell below zero.

D)

Market rates barely moved at all.

Page 14

57.

What are options for monetary easing using interest rate policy instruments when the

rate has hit the zero lower bound?

A)

At that point, interest rate policy cannot be used.

B)

Monetary easing can still occur whenever interest rates are greater than zero at the

retail level.

C)

The central bank can increase the money supply, and interest rates can be less than

zero.

D)

Borrowing can be stimulated in ways other than lower rates of interest.

58.

To move quickly to turn around the crisis during 2007–08, the U.S. Federal Reserve

relied on:

A)

lowering taxes.

B)

removing restrictions on collateral, adding more categories of securities purchased

by the Federal Reserve, and expanding its operations with nonbank dealers.

C)

tightening up credit rules and keeping banks out of trouble.

D)

admonishing the administration for its excessive debt situation.

59.

What happened to the measure of money, M0, which includes only cash, bank reserves,

and deposits at the Federal Reserve during the crisis?

A)

It shrank measurably.

B)

It expanded slightly.

C)

It more than doubled.

D)

There was no change in M0.

60.

Aggressive policy measures taken by the monetary authority during the 2007–08

financial crisis in the United States resulted in:

A)

avoidance of a recession caused by a tight credit market.

B)

almost no transmission of the monetary stimulus to market rates of interest,

increased lending, and expansion of GDP.

C)

lower rates of interest and increased investment activity.

D)

an increase of real GDP and a fall in the core unemployment rate.

61.

An increase in real income _____ the demand for real money balances and thereby

causes a ____ in the nominal rate of interest.

A)

lowers; rise

B)

lowers; fall

C)

raises; rise

D)

raises; fall

Page 15

62.

In the short run, ceteris paribus, an expanded money supply leads to:

A)

a higher nominal interest rate.

B)

no change in the nominal interest rate.

C)

a lower nominal interest rate.

D)

an increase in the exchange rate.

63.

In the short run/long run, a strong currency goes with:

A)

a low interest rate/a high interest rate.

B)

a high interest rate/a high interest rate.

C)

a high interest rate/a low interest rate.

D)

a low interest rate/a low interest rate.

64.

An increase in the money supply in the short run changes ____, whereas in the long run,

____ change.

A)

exchange rates; nominal interest rates

B)

price levels; interest rates

C)

interest rates; interest rates

D)

interest rates; inflation rates

65.

A perceived permanent rise in the rate of money growth will cause what long-run effects

in the economy?

A)

a rise in the nominal rate of interest and a rise in inflation by the same percentage

B)

a rise in the nominal rate of interest and a rise in real GDP by the same percentage

C)

a fall in the nominal rate of interest and a rise in inflation by the same percentage

D)

a fall in the nominal rate of interest and a fall in real GDP by the same percentage

66.

When the public perceives that a monetary expansion will be temporary, what happens

to nominal interest rates in the short run?

A)

They will rise.

B)

They will overshoot their target.

C)

They will fall.

D)

They will be unchanged.

67.

The dependent variable (vertical axis) in standard graphical treatments of the money

market is:

A)

the exchange rate.

B)

the real rate of interest.

C)

real GDP.

D)

the nominal rate of interest.

Page 16

68.

A key assumption to ensure that domestic returns and foreign returns are in equilibrium

is:

A)

there are perfectly flexible prices.

B)

the quantity of money is fixed.

C)

there are no capital controls preventing the movement of capital.

D)

trade is not subject to any restrictions.

69.

Combining the home money market and the uncovered interest parity relationship, we

can see how changes in variables determine:

A)

real GDP.

B)

the exchange rate.

C)

the price level.

D)

the quantity of money.

70.

When policy changes are temporary, then:

A)

exchange rates do not change.

B)

expectations do not change.

C)

interest rates do not change.

D)

expectations can change based on results.

71.

The returns from the home country and foreign country capital markets are equalized if:

A)

the home country interest rates are higher.

B)

the foreign country interest rates are higher.

C)

the foreign country has a higher price level.

D)

both countries have no capital controls.

72.

Using the asset model of short-run exchange rate determination, once the domestic rate

of return is determined by MS and MD, the short-run equilibrium _____ can be

determined if prices are inflexible and expectations are given.

A)

interest rate

B)

exchange rate

C)

price level

D)

income level

Page 17

73.

Assume sticky prices and given expectations of future exchange rates, what is the

immediate effect on the exchange rate of the U.S. dollar if there is a temporary increase

in the quantity of U.S. dollars?

A)

U.S. nominal and real returns rates decline while euro rates hold steady, and the

U.S. dollar depreciates against the euro.

B)

U.S. nominal returns rise, U.S. real returns fall, euro rates rise, and the U.S. dollar

appreciates against the euro.

C)

U.S. nominal returns fall, U.S. real returns rise, euro rates fall, and the U.S. dollar

appreciates against the euro.

D)

U.S. dollar returns and euro returns both rise, leaving the exchange rate unchanged.

74.

If there is a temporary increase in the money supply in the Eurozone, ceteris paribus,

what is the result for the United States?

A)

The money supply in the United States must decrease by the same proportion.

B)

The U.S. dollar nominal interest rate will increase, as the euro rate is unchanged.

C)

Long-run expectations shift to expect a stronger euro.

D)

The dollar appreciates against the euro.

75.

Assuming sticky prices and given expectations of future exchange rates, what is the

short-run effect on the exchange rate of the U.S. dollar (purchasing euros) and on

domestic and foreign rates of return if there is a temporary increase in the quantity of

U.S. dollars?

A)

Rates of return on domestic and foreign assets diverge, as the dollar appreciates.

B)

Domestic and foreign rates of return both fall, as the dollar depreciates.

C)

Domestic and foreign rates of return converge, as the dollar depreciation lowers

returns for U.S. investors who purchase euro-based assets.

D)

Rates of return on euro assets fall, causing investors to switch into U.S. assets and,

therefore, the U.S. dollar appreciates against the euro.

76.

Assuming sticky prices and given expectations of future exchange rates, what is the

short-run effect on the exchange rate of the U.S. dollar (purchasing euros) and on

domestic and foreign rates of return if there is a temporary increase in the quantity of

euros?

A)

Rates of return on domestic and foreign assets diverge, as the dollar appreciates.

B)

Domestic and foreign rates of return both fall, as the dollar depreciates.

C)

Domestic and foreign rates of return converge, as depreciation of the euro raises

returns for U.S. investors who purchase euro-based assets.

D)

Rates of return on dollar assets fall, causing investors to switch into euro assets

and, therefore, the U.S. dollar depreciates against the euro.

Page 18

77.

A short-run depreciation of the British pound would be consistent with:

A)

a temporary fall in the British money supply.

B)

a temporary fall in the European money supply.

C)

a temporary rise in the European money supply.

D)

either a temporary fall in the British money supply or a temporary rise in the

European money supply.

78.

A short-run appreciation of the British pound would be consistent with:

A)

a temporary fall in the British money supply.

B)

a temporary fall in the European money supply.

C)

a permanent rise in the European money supply.

D)

either a temporary fall in the British money supply or a temporary rise in the

European money supply.

79.

When a country’s central bank temporarily switches from an expansionary to a more

conservative monetary policy, one would expect the exchange rate to:

A)

depreciate in the short run, then return to its initial value.

B)

appreciate in the short run, then return to its initial value.

C)

depreciate in the short run and then stay higher.

D)

appreciate in the short run and then stay lower.

80.

During the period 2001–04, the U.S. Federal Reserve lowered nominal interest rates on

the dollar by more than the European Central Bank (ECB) did on the euro, a move that

most market participants viewed as temporary. What was the effect on the dollar–euro

exchange rate?

A)

The dollar depreciated against the euro.

B)

The dollar appreciated against the euro.

C)

There was no change in the dollar–euro rate because expectations adjusted.

D)

There was no change in the dollar–euro rate because real interest rates were

unchanged.

81.

From 1999–01, the U.S. Federal Reserve _____ nominal interest rates, and it _____ the

policy in 2001 because of concerns over _____.

A)

lowered; continued; recession

B)

raised; reversed; inflation

C)

raised; reversed; recession

D)

lowered; continued; inflation

Page 19

82.

Interest rates set by the European central bank during the period 1999–2004 resulted in

what situation compared with the United States?

A)

European rates were exactly the same as those in the United States, resulting in

uncovered interest parity.

B)

European rates were consistently higher than U.S. rates.

C)

European rates were consistently lower than U.S. rates.

D)

At first the European rates were much higher, but then the ECB acted aggressively

to lower them.

83.

The behavior of exchange rates during the period 1999–2004 ____ predictable based on

the short run asset model if we assume that changes in the money supply were assumed

to be _________.

A)

was not; temporary

B)

was; temporary

C)

was not; permanent

D)

was; permanent

84.

To arrive at a complete theory of exchange rate determination, we use:

A)

the short-run monetary approach, the long-run monetary approach, and a good dose

of common sense.

B)

the short-run asset approach, the long-run monetary approach, and real interest

parity.

C)

real-world phenomena such as sticky prices, government inefficiency, and

imperfect markets.

D)

information on financial markets, political realities, and the large government debt.

85.

Which of the following is NOT a method of forecasting exchange rates?

A)

technical methods

B)

animal methods

C)

economic fundamental methods

D)

All of these are methods.

86.

To complete the theory of exchange rates, a model should be created that:

A)

accommodates short-run changes in variables.

B)

accommodates long-run changes in variables.

C)

accommodates changes in expectations.

D)

accommodates short-run and long-run changes in variables and changes in

expectations.

Page 20

87.

The asset approach basically looks at ____ as the fundamental variable affecting _____

exchange rates.

A)

interest rates; short-run

B)

interest rates; long-run

C)

the price level; short-run

D)

the price level; long-run

88.

The monetary approach basically looks at ____ as the fundamental variable affecting

_____ exchange rates.

A)

interest rates; short-run

B)

interest rates; long-run

C)

the price level; short-run

D)

the price level; long-run

89.

Survey evidence from forex traders indicates support for the economic fundamental’s

impact on exchange rates:

A)

in the short run.

B)

in the moderate run.

C)

only in the long run.

D)

not at all.

90.

Which of the following is true in the short run?

A)

Short-term interest rates are fixed.

B)

Prices are flexible.

C)

Long-run expectations of the exchange rate are unchanged.

D)

Monetary shocks are deemed permanent.

91.

When analyzing the complete model, which can predict short-run and long-run changes

in the exchange rate, one must:

A)

start with short-run changes and move toward long-run changes, and thereby

determine expectations.

B)

use only the long-run model because the short-run model is largely irrelevant.

C)

start with the long-run equilibrium positions where expectations of future exchange

rates can be determined and use those expectations to feed into the short-run

model.

D)

use the short-run model only, because the long run is only a theoretical concept.

Page 21

92.

From full long-run equilibrium, expectations of future exchange rates can only change

when there is a:

A)

political change.

B)

permanent change in the quantity of money.

C)

change in short-run interest rates.

D)

temporary decrease in the quantity of money.

93.

The overriding factor in analyzing long-run changes in the exchange rate is:

A)

the exchange rate in the period t – 1.

B)

how a permanent change in the supply of money is transmitted to prices and

interest rates.

C)

the reaction of traders as they conduct arbitrage and speculation.

D)

the notion that there is no long run, only a series of short-run measurements.

94.

When there is a permanent fall in the domestic money supply, the exchange rate:

A)

falls in the short run and rises slightly in the long run.

B)

falls in the short run and falls more in the long run.

C)

rises in the short run and falls slightly in the long run.

D)

rises in the short run and rises more in the long run.

95.

When there is a permanent fall in the foreign money supply, the exchange rate:

A)

falls in the short run and rises slightly in the long run.

B)

falls in the short run and falls more in the long run.

C)

rises in the short run and falls slightly in the long run.

D)

rises in the short run and rises more in the long run.

96.

When traders perceive a permanent money supply adjustment, long-term nominal

interest rates ___ affected, the expected exchange rate ____ affected, and the spot

exchange rate _____ affected.

A)

are not; is; is

B)

are; is; is not

C)

are not; is not; is not

D)

are; is not; is

Page 22

97.

When traders perceive a permanent money supply adjustment, short-term nominal

interest rates ___ affected, the expected exchange rate ____ affected, and the spot

exchange rate _____ affected.

A)

are; is; is

B)

are; is; is not

C)

are not; is not; is not

D)

are; is not; is

98.

If you observe that the dollar is appreciating because of a permanent change in the U.S.

monetary supply, then the money supply must have:

A)

fallen.

B)

stayed the same.

C)

risen.

D)

Not enough information is provided to answer the question.

99.

Which of the following conditions do NOT exist in long-run equilibrium?

A)

Domestic nominal interest rates are such that the supply of real balances is equal to

demand.

B)

The domestic real return is equal to the foreign real return through the equilibrium

exchange rate.

C)

There are no price level or exchange rate changes and therefore the expected future

exchange rate is equal to the actual exchange rate.

D)

Domestic nominal interest rates are such that the supply of real balances is greater

than demand.

100.

When the U.S–foreign exchange rate appreciates in the short run and then depreciates

slightly in the long run, it implies that the foreign money supply has:

A)

temporarily risen.

B)

permanently risen.

C)

temporarily fallen.

D)

permanently fallen.

101.

In the short run, the nominal interest rate is affected by changes in the money supply

perceived to be temporary, but once ____ adjust(s), the nominal interest rate ____ in the

long run.

A)

the supply of money; rises

B)

the price level; will revert to its former level

C)

expectations of interest rates; falls

D)

real GDP; does not change

Page 23

102.

When the exchange rate appreciates in the short run and then depreciates to its original

level in the long run, it implies that the foreign money supply has:

A)

temporarily risen.

B)

permanently risen.

C)

temporarily fallen.

D)

permanently fallen.

103.

When the exchange rate depreciates in the short run and then depreciates slightly in the

long run, it implies that the domestic money supply has:

A)

temporarily risen.

B)

permanently risen.

C)

temporarily fallen.

D)

permanently fallen.

104.

When the exchange rate depreciates in the short run and then appreciates to its original

level in the long run, it implies that the domestic money supply has:

A)

temporarily risen.

B)

permanently risen.

C)

temporarily fallen.

D)

permanently fallen.

105.

When the exchange rate appreciates in the short run and then depreciates slightly in the

long run, it implies that the domestic money supply has:

A)

temporarily risen.

B)

permanently risen.

C)

temporarily fallen.

D)

permanently fallen.

106.

When the exchange rate appreciates in the short run and then depreciates to its original

level in the long run, it implies that the domestic money supply has:

A)

temporarily risen.

B)

permanently risen.

C)

temporarily fallen.

D)

permanently fallen.

Page 24

107.

When the exchange rate depreciates in the short run and then appreciates slightly in the

long run, it implies that the foreign money supply has:

A)

temporarily risen.

B)

permanently risen.

C)

temporarily fallen.

D)

permanently fallen.

108.

When the exchange rate depreciates in the short run and then appreciates to its original

level in the long run, it implies that the foreign money supply has:

A)

temporarily risen.

B)

permanently risen.

C)

temporarily fallen.

D)

permanently fallen.

109.

If there is a permanent increase in the domestic money supply, then in the short run,

which of the following will be true?

A)

The prices will adjust lower.

B)

Domestic interest rates will increase.

C)

Real money supply will increase.

D)

Domestic money demand will permanently increase.

110.

If there is a permanent increase of 8% in the domestic money supply, then which of the

following will be true in the long run?

A)

Prices will decrease by 8%.

B)

Prices will increase by 4%.

C)

The home country currency will depreciate by 8%.

D)

The home country currency will appreciate by 4%.

111.

If the Bank of Japan permanently increases its money supply, then which of the

following is most likely to take place in the short run?

A)

Japanese prices will immediately decrease.

B)

Japanese prices will immediately increase.

C)

Japanese interest rates will increase.

D)

Japanese interest rates will decrease.

Page 25

112.

When an increase in the quantity of money is considered to be permanent and prices are

sticky, then in the short run the exchange rate depreciates and overshoots because:

A)

domestic nominal returns fall relative to foreign returns, and traders expect a

permanent depreciation in future exchange rates.

B)

traders do not change their expectations of the exchange rate, and lower domestic

rates make it easier to borrow.

C)

inflationary expectations eventually cause a rise in domestic real returns.

D)

traders quickly realize that their expectations of future exchange rates are incorrect

and eventually prices will become unstuck.

113.

In the United States, where there is a permanent increase in the money supply, exchange

rate overshooting is caused in part by:

A)

higher domestic interest rates.

B)

an appreciation of the dollar.

C)

lower foreign interest rates.

D)

a depreciation of the dollar.

114.

Overshooting occurs because:

A)

expectations adjust slower than prices.

B)

expectations adjust at the same rate as prices.

C)

expectations adjust faster than prices.

D)

expectations do not adjust.

115.

Overshooting is when exchange rates:

A)

adjust more in the short run than they need to for long-run equilibrium.

B)

adjust less in the short run than they need to for long-run equilibrium.

C)

are unable to adjust because of fixed exchange rates.

D)

adjust at the same rate as prices.

116.

A nominal anchor is a commitment to keep nominal variables within limits, often tied to

an external value or price. When nations do not incorporate such discipline into their

monetary policy, exchange rates are often:

A)

irrelevant to economic activity.

B)

extremely volatile, because traders consider monetary shocks to be permanent.

C)

less dependent on monetary variables.

D)

determined by political considerations rather than economic fundamentals.

Page 26

117.

Nominal anchors limit overshooting by:

A)

fixing exchange rates.

B)

distinguishing between permanent and temporary changes.

C)

slowing down expectations formation.

D)

limiting temporary changes to exchange rates.

118.

In general, which of the following statements is NOT a characteristic of a fixed

exchange rate regime as defined by the text?

A)

Capital is mobile.

B)

Exchange rates are determined by the market in the short run.

C)

Arbitrage is free to operate.

D)

Government takes an active role in foreign currency market intervention.

119.

Central banks control exchange rates by intervention. If a nation such as Japan wished

to peg its market rate at a certain level, such as ¥100 = $1, what should it do if the actual

market rate begins to depreciate to ¥125 = $1?

A)

It should purchase dollars with its own currency.

B)

It should sell dollars from its treasury and retire its own currency.

C)

It should increase its GDP to increase exports.

D)

It should petition the IMF for a rate change.

120.

Exchange rate interventions occur when a government:

A)

buys and sells its own currency on forex markets.

B)

buys and sells other currencies on forex markets.

C)

increases its interest rate.

D)

buys and sells its own currency and other currencies on forex markets.

121.

Which of the following describes the role of the government in a fixed exchange rate

regime?

A)

establishing capital controls

B)

controlling budget deficits

C)

the buying and selling of currency by the central bank

D)

expanding the money supply

122.

With fixed exchange rates and capital mobility:

A)

interest rates in the home country and in foreign countries are equalized.

B)

interest rates in the home country are higher.

C)

interest rates in foreign countries are higher.

D)

monetary policy maintains its autonomy.

Page 27

123.

In the short run, the chain of causality between monetary policy and the exchange rate

under fixed rates differs from a floating rate. How?

A)

In a fixed rate regime, the money supply is determined first, then interest rates,

then the short-run exchange rate.

B)

In a fixed rate regime, interest rates are determined first, then the money supply,

and then the short-run exchange rate.

C)

In a floating rate regime, exchange rates are determined first, then the nominal

interest rate (according to uncovered interest parity), and then the money supply.

D)

In a fixed rate regime, exchange rates are determined first, then the nominal

interest rate (according to uncovered interest parity), and then the money supply.

124.

If Bulgaria, for instance, wished to keep its exchange rate with the dollar fixed, what

monetary policy options are available to lower unemployment in the short run?

A)

Bulgaria has all the options available to it, because domestic monetary policy is

conducted inside the nation and has no bearing on its international variables.

B)

Traders would realize that any monetary policy actions taken inside a nation would

improve economic conditions without affecting international variables.

C)

Bulgaria cannot use any monetary policy that would cause its short-run exchange

rate to depreciate against the dollar.

D)

Bulgaria’s monetary action would restore confidence and help keep its currency

stable.

125.

Why would lowering its own interest rates affect a nation’s exchange rate?

A)

International interest arbitrage (the ability to borrow in low-rate markets and

deposit in higher-rate markets) would cause investors to sell domestic currency

assets and purchase foreign assets based in other currencies.

B)

A nation’s central bank controls both interest rates and exchange rates.

Unfortunately, they do not have sufficient funds to take care of both at the same

time.

C)

When interest rates fall, borrowing is cheaper, spending and GDP rise and so do

exports, thus causing the exchange rate to appreciate.

D)

In the short run, exchange rates have to adhere to PPP; otherwise, traders will make

profits by purchasing in the cheap market and selling in the more expensive

market, thus aligning exchange rates at the proper level.

Page 28

126.

Why would making a permanent change in a monetary aggregate have an effect on

exchange rates in a nation?

A)

Permanent rates are mostly set by short-run fluctuations in the rate of interest

caused by monetary instability.

B)

A permanent change is never quite as permanent as policy makers claim—people

form expectations on past performance rather than declarations.

C)

The central bank is always aware of the effect on exchange rates as it formulates

policy, so it is very careful to make small permanent changes that have no effect on

exchange rates.

D)

Traders form expectations of future exchange rates based on the anticipated

long-run effects of monetary operations.

127.

Which of the following is correct?

A)

If a nation changes its money supply, it disrupts the long-run PPP equilibrium,

which causes traders to purchase in the cheaper markets and sell in the pricier

markets, which, in turn, causes demand for the domestic currency (vis-à-vis the

international currency) to be lower.

B)

The peg changes the long-run expectation of exchange rates, and this is a

determinant of short-run rates which, in turn, affect deposit rates of return.

C)

The Federal Reserve has complete control of monetary policy; it is independent of

political control, so, in the United States at least, monetary policy can coexist with

an exchange rate peg.

D)

Pegging its own currency causes a nation to lose political control, and it is then

forced to sell its own resources at world prices.

128.

If Japan seeks to control its exchange rates so that ¥100 = $1, which of the following

policies should it NOT maintain?

A)

interest rates that provide the same return as alternative international rates

B)

a stable rate of price level changes that will not cause currency depreciation or

appreciation

C)

a willingness to raise interest rates when its currency begins to depreciate

D)

a willingness to raise price levels

129.

A country with a fixed exchange rate faces:

A)

no monetary policy constraints in the long run.

B)

no monetary policy constraints in the short run.

C)

no monetary policy constraints in the long run and the short run.

D)

monetary policy constraints in the long run and the short run.

Page 29

130.

Which of the following explains why a monetary policy in a nation with an exchange

rate peg, such as Denmark, would NOT be possible?

A)

The nation must keep its import tariffs in sync with the import tariffs of the nation

to which it pegs.

B)

The nation must keep its price level and nominal interest rate equal to the price

level and nominal interest rate in the nation to which it pegs.

C)

The nation must keep its taxes and budget deficit in sync with taxes and budget

deficit in the nation to which it pegs.

D)

The nation is no longer able to print its own money, since it is using the currency of

the nation to which it pegs.

131.

The trilemma refers to all the following, EXCEPT:

A)

a fixed exchange rate.

B)

international capital mobility.

C)

monetary policy autonomy.

D)

price controls.

132.

If an economy wants to maintain monetary policy autonomy, then:

A)

it can maintain a fixed exchange rate and international capital mobility.

B)

it can impose strict capital controls and maintain a fixed exchange rate.

C)

it can maintain capital mobility but not a fixed exchange rate.

D)

it can impose strict capital controls and maintain a fixed exchange rate or it can

maintain capital mobility but not a fixed exchange rate.

133.

International variables are linked through trade and financial flows. Therefore, what

trilemma is faced by a nation that wishes to keep its exchange rates with other nations

fixed?

A)

It can have fixed exchange rates only when it allows free flows of capital and

maintains control of its interest rates.

B)

If it wants to control its own monetary policy under fixed exchange rates, then it

must restrict foreign investment.

C)

Fixed exchange rates are not possible if the nation allows free flows of capital both

into and out of the nation.

D)

Fixed exchange rates are not possible if the nation also wants to control its

monetary policy.

Page 30

134.

What are the consequences for a nation that keeps its exchange rate fixed, holds its own

domestic interest rates below market to encourage domestic spending, and allows free

foreign investment?

A)

Foreign investors will not invest, so the only consequence will be a decline in the

inflow of foreign investment.

B)

Domestic and foreign investors will invest in other nations, causing a sell-off of the

domestic currency and, to maintain fixed rates, the central bank will have to buy its

own currency, depleting its treasury reserves.

C)

There will be upward pressure on the rate of interest as more borrowing occurs, so

the central bank will have to increase the stock of money.

D)

Interest rates in other nations will also fall as banks and other firms have to

compete for international borrowers.

135.

Comparing the examples of Denmark and the United Kingdom in relationship to the

European Monetary Union, the krone is pegged to the euro, whereas the British pound is

not. What can be predicted then about their interest rates?

A)

The United Kingdom has the ability to set its own interest rates and pursue an

independent monetary policy, whereas Denmark’s rates are virtually the same as

those of the euro.

B)

Denmark gets the benefits of having fixed exchange rates as well as having an

independent monetary policy and the ability to set its own rates of interest.

C)

Denmark’s price level in the long run will be much higher than the Eurozone

because it has to keep exchange rates fixed.

D)

The United Kingdom will discover that it cannot lower its own interest rates after

all, or the pound will depreciate so far that no investors will make investments in

the United Kingdom.

136.

During the U.S. Civil War (1861–1865), the Confederate States printed their own

currency. Events occurred during the war that affected the exchange value of the

Confederate dollars. What evidence was there that supports the theory of long- and

short-run exchange rate determination?

A)

The Union soldiers burned Confederate dollars at every opportunity, making them

more valuable than the Union dollar.

B)

The Confederate dollar became worth more as it became clear that the South would

lose, because the Confederacy’s dollars would become collectibles.

C)

The Confederate dollar’s value was closely linked to the difference in the deposit

rates in southern states’ banks.

D)

Speculators traded for profit and based their valuation on the long-run expectation

of the exchange rate, which tracked closely the probability of a victory for the

South.

Page 31

137.

The outcome of the Civil War in the United States was that:

A)

the Confederates were allowed to keep their currency.

B)

the value of the Confederate dollar increased at the end of the war.

C)

the Confederate dollar became worthless.

D)

the North’s currency declined in value.

138.

Two currencies existed in Iraq before the U.S. invasion and subsequent conflict. What

lessons are there for students of exchange rates?

A)

Exchange rate values are influenced not only by economic fundamentals but by

political events that change long-run expectations of future currency values.

B)

Iraq did not back its currency with gold and, therefore, it was worth much less than

the U.S. dollar.

C)

Eventually each Iraqi sect developed its own currency and payments system.

D)

Exchange rate values are solely influenced by economic policy.

139.

In 2003, which of the following currencies was used in Iraq?

A)

Swiss dinar

B)

Saddam (or print) dinar

C)

American dinar

D)

Swiss dinar and Saddam (or print) dinar

140.

After the United States dropped an atomic bomb on Japan, what do you expect

happened to the yen?

A)

The yen appreciated.

B)

The yen was unaffected.

C)

The yen depreciated.

D)

There is no way to predict the effect on the yen.

141.

What happens, ceteris paribus, to the foreign return on assets, as the spot exchange rate

increases (depreciates).

142.

Explain why an increase in the European interest rate increases the dollar–euro

exchange rate.

143.

Suppose domestic interest rates are at 4.55%, while foreign returns are bringing 6.38%.

According to the asset approach, if the expected future exchange rate is three dollars per

unit of foreign currency, what can we say about the current spot rate if UIP holds?

Page 32

144.

Explain the intuition for the fact that short-run nominal interest rates fall in response to

an increase in the money supply.

145.

Explain the fact that short-run nominal interest rates rise in response to an increase in

the real income.

146.

On the outlined graphs that follow, label each axis and each linear relationship. If the

money supply in the United States is temporarily increased from M1 to M2, and prices

are sticky, trace the effects of the change and predict the effect on the dollar, assuming

other variables remain constant.

147.

Briefly describe the three elements of a complete theory of exchange rate determination.

List the variables in each element, and explain whether the theory addresses short-run

exchange rate changes or long-run exchange rates.

148.

Evaluate the following statement: Higher nominal interest rates are associated with an

appreciating exchange rate. Do you agree, disagree, or both? Explain.

149.

The U.S. Federal Reserve has recently been engaged in quantitative easing in which it is

essentially expanding the money supply. What are the likely short-run and long-run

implications of this?

150.

Describe the effect of a permanent increase in the quantity of money on exchange rates

in both the long and short run.

151.

Describe the effect of a permanent increase in the foreign quantity of money on

exchange rates in both the long run and short run.

Page 33

152.

The dollar–pound exchange rate has increased (the dollar has depreciated). What could

have happened? Choose one possible determinant and how it caused this phenomenon.

153.

What exactly is overshooting and why does it happen?

154.

What role does the Fisher effect play in overshooting?

155.

(Figure: Thailand–U.S. Foreign Exchange Rate) Look at the following graph. How

would you explain the behavior of the exchange rate after the pegged exchange rate

broke?

Figure: Thailand–U.S. Exchange Rate

156.

The case of Denmark illustrates the effects on a nation of a fixed exchange rate regime.

Briefly discuss the trade-offs from a fixed exchange rate and the ability to conduct

monetary policy.

157.

Suppose a country has decided to peg to the euro. Explain what will need to happen if

the European Central Bank engages in a temporary increase in money supply.

158.

Suppose Japan wishes to maintain its exchange rate with the U.S. dollar at ¥100 = $1. It

would also like to attract foreign investors to provide funds to build its aircraft sector,

and it would like to keep inflation low. Is it capable of doing that?

Page 34

159.

In your own words, explain the essence of the trilemma. Why can’t a country with fixed

exchange rates and capital mobility maintain autonomy?

Page 36

Page 37

Page 38