CHAPTER 32

Prices and Profits in Perfect Competition

MULTIPLE CHOICE

346. The four types of market structures are

a. perfect competition, monopoly, monopolistic competition, and oligopoly

b. perfect competition, monopoly, monopsony, and duopoly

c. perfect competition, monopolistic competition, monopsony, tripoly

d. perfect competition, monopoly, monopolistic competition, and monopsony

347. Which market structure(s) is characterized by a large number of firms and a large number

of buyers?

a. perfect competition and oligopoly

b. perfect competition and monopoly

c. perfect competition and monopolistic competition

d. perfect competition and duopoly

348.

a. a firm can dictate prices to its customers.

b. a firm must take the price determined in the market.

c. a firm must take the price dictated by its suppliers.

d. the price is different for take away.

349. Atlas Flour finds that the market price for a 5 pound bag of its flour remains $9.00 whether

it sells 1 bag or 1000. This information suggests that Atlas Flour is operating in

a. a perfectly competitive market.

b. an oligopolistic market.

c. a monopolisticaly competitive market.

d. a monopolistic market.

350. Assume that a small firm, Blue Mill Flour Company, enters the perfectly competitive

market for flour. The current market price is $8.40 per 5 pound bag. Blue Mill Flour decides

that $8.75 would be a better price. What will happen if Blue Mill charges a price above the

current market price?

a. Blue Mill will sell more flour.

b. Blue Mill will not sell quite as much flour.

c. Blue Mill will not sell any flour.

d. Blue Mill will sell the same amount of flour.

351. Assume that a small firm, Blue Mill Flour Company, enters the perfectly competitive

market for flour. The current market price is $8.40 per 5 pound bag. Blue Mill Flour decides

that $8.00 would be a better price. What will happen if Blue Mill charges a price below the

current market price?

a. Blue Mill will sell more flour.

b. Blue Mill will not sell quite as much flour.

c. Blue Mill will not sell any flour.

d. Blue Mill will sell the same amount of flour.

352. What is the definition of marginal cost?

a. marginal cost = change in total cost/change in quantity

b. marginal cost = total cost/quantity

c. marginal cost = total cost fixed cost

d. marginal cost = variable cost + fixed cost.

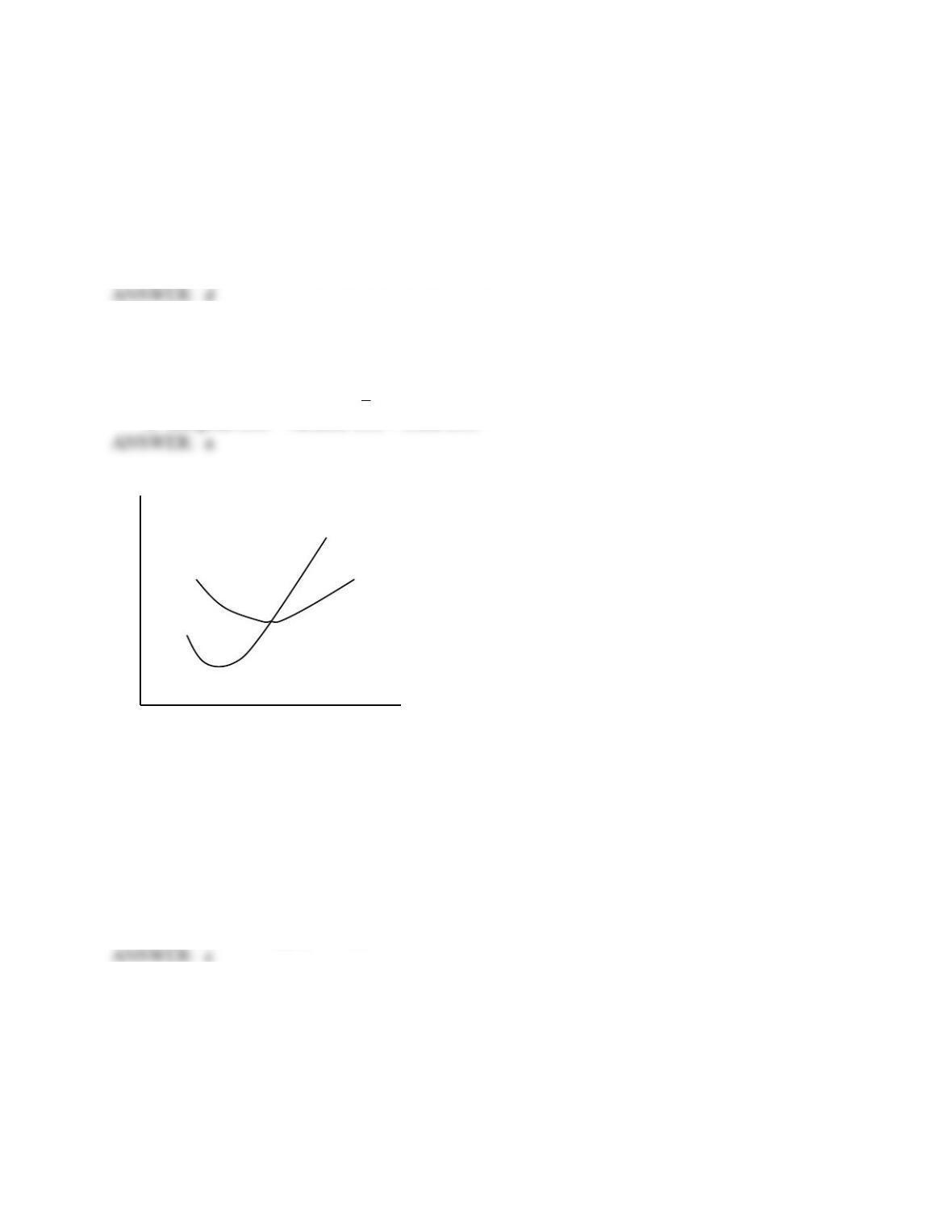

Diagram 32a

353. Identify the curves shown in Diagram 32a

a. line A is the average cost curve; line B is the marginal cost curve.

b. line A is the total cost curve; line B is the average cost curve.

c. line A is the marginal cost curve; line B is the average cost curve.

d. line A is the supply curve; line B is the demand curve.

Q

P line A

line B

APPENDIX 32.1

Long Run Equilibrium for the Firm and the Industry in Perfect Competition

MULTIPLE CHOICE

354. Assume that Dubuque Flour Company is currently selling a 5 pound bag of flour for $8.40.

Marginal cost per 5 pound bag is $8.40, and average cost is $8.00.

a. Dubuque Flour Company is in short term equilibrium and long term equilibrium.

b. Dubuque Flour Company is not in short term equilibrum nor is it in long term

equilibrium.

c. Dubuque Flour Company is in short term equilibrium but not in long term equilibrium.

d. Dubuque Flour Company is not in short term equilibrium but it is in long term

equilibrium.

355. Assume that Boise Flour Company is currently selling a 5 pound bag of flour for $8.00.

Marginal cost per 5 pound bag is $8.00, and average cost is $8.00.

a. Dubuque Flour Company is in short term equilibrium and in long term equilibrium.

b. Dubuque Flour Company is not in short term equilibrum nor is it in long term

equilibrium.

c. Dubuque Flour Company is in short term equilibrium but not in long term equilibrium.

d. Dubuque Flour Company is not in short term equilibrium but it is in long term

equilibrium.

356.