Page 1

1.

An industry with only two firms is generally called:

A)

a monopoly.

B)

monopolistic competition.

C)

a duopoly.

D)

perfect competition.

2.

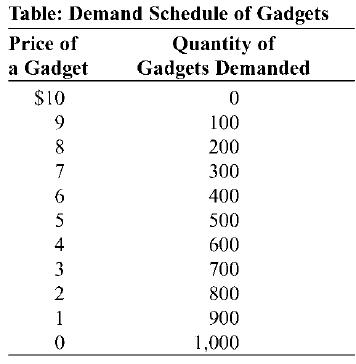

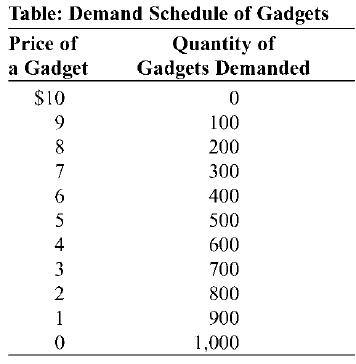

A duopoly is an industry that consists of:

A)

a single firm.

B)

two firms.

C)

three or more firms.

D)

a large number of small firms.

3.

An industry that consists of two firms is:

A)

a duopoly.

B)

a monopoly.

C)

a monopsony.

D)

monopolistic competition.

4.

_____ occurs when the only two firms in an industry agree to fix the price at a given

level.

A)

Collusion

B)

The ability to satisfy demand

C)

Price extortion

D)

Price leadership

5.

An extreme case of oligopoly in which firms collude to raise joint profits is known as a:

A)

duopoly.

B)

cartel.

C)

dominant producer.

D)

price war.

6.

If there are two gas stations in a very small town, then the gas station business there is

probably best characterized as:

A)

perfectly competitive.

B)

monopolistically competitive.

C)

monopolistic.

D)

oligopolistic.

Page 2

7.

Collusive agreements are typically difficult for cartels to maintain because each firm can

increase profits by:

A)

producing more than the quantity that maximizes joint profits.

B)

producing less than the quantity that maximizes joint profits.

C)

charging more than the price that maximizes joint cartel profits.

D)

advertising less than will maximize joint cartel profits.

8.

The owners of the gas stations in a town are trying to set up a cartel that will raise the

price of gasoline. Which scenario will increase the chances that the cartel will fail

because of cheating by the owners?

A)

All of the gas stations face the same costs.

B)

There are only a few gas stations.

C)

The gas stations are producing as much as they can.

D)

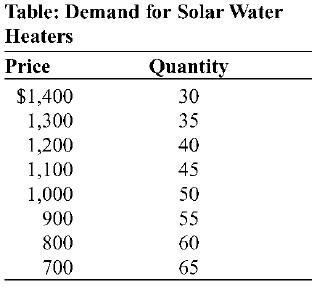

The gas stations vary in terms of the services that they provide.

9.

In an oligopoly market, collusion between firms usually leads to higher profits than does

noncooperative behavior. However, formal, overt collusion doesn’t usually occur in the

United States because:

I. it is illegal.

II. there is an incentive for each firm to cheat on a collusive agreement.

III. an oligopolistic firm will typically prefer lower profits for itself if the only way to

make higher collective profits in the industry is to improve the profit position of its

rivals.

A)

I only

B)

II only

C)

I and II

D)

II and III

10.

Gary’s Gas and Frank’s Fuel are the only two providers of gasoline in their small town.

Gary and Frank decide to form a cartel to raise the price of gasoline. The total industry

profits are highest when _____ cheat(s) on the agreement, and Gary’s profits are highest

when _____.

A)

neither firm; neither firm cheats on the agreement

B)

neither firm; Gary cheats but Frank does not

C)

both firms; Gary cheats but Frank does not

D)

both Gary and Frank; both Gary and Frank cheat

Page 3

11.

In which situation does overt collusion take place?

A)

Smaller firms in an industry have an unspoken agreement to charge the same price

as the largest firm.

B)

Firms in an industry agree openly on price and output, and they jointly make other

decisions aimed at achieving monopoly profits.

C)

Competition among a large number of small firms generates similar but slightly

different prices.

D)

Competition among a large number of small firms generates a stable market price.

Use the following to answer questions 12-38:

12.

(Ref 30-1 Table: Demand Schedule of Gadgets) Use Table 30-1: Demand Schedule of

Gadgets. The market for gadgets consists of two producers, Margaret and Ray. Each

firm can produce gadgets with no marginal cost or fixed cost. If these two producers

formed a cartel and acted to maximize total industry profits, total industry output would

be _____, and the price would be _____.

A)

1,000; $10

B)

100; $9

C)

400; $6

D)

500; $5

Page 4

13.

(Ref 30-1 Table: Demand Schedule of Gadgets) Use Table 30-1: Demand Schedule of

Gadgets. The market for gadgets consists of two producers, Margaret and Ray. Each

firm can produce gadgets with no marginal cost or fixed cost. If these two producers

formed a cartel and acted to maximize total industry profits, total industry profit would

be:

A)

$10,000.

B)

$5,000.

C)

$2,500.

D)

$1,250.

14.

(Ref 30-1 Table: Demand Schedule of Gadgets) Use Table 30-1: Demand Schedule of

Gadgets. The market for gadgets consists of two producers, Margaret and Ray. Each

firm can produce gadgets with no marginal cost or fixed cost. If these two producers

formed a cartel, split the production of output equally, and acted to maximize total

industry profits, each firm’s output would be _____, and each firm’s profit would be

_____.

A)

500; $2,500

B)

250; $1,250

C)

1,000; $500

D)

1,000; $10,000

15.

(Ref 30-1 Table: Demand Schedule of Gadgets) Use Table 30-1: Demand Schedule of

Gadgets. The market for gadgets consists of two producers, Margaret and Ray. Each

firm can produce gadgets with no marginal cost or fixed cost. Suppose that these two

producers have formed a cartel and are maximizing total industry profits and splitting

the production of output evenly between themselves. If Margaret decides to cheat on the

agreement and sell 100 more gadgets, how many gadgets will she sell?

A)

0

B)

250

C)

350

D)

600

16.

(Ref 30-1 Table: Demand Schedule of Gadgets) Use Table 30-1: Demand Schedule of

Gadgets. The market for gadgets consists of two producers, Margaret and Ray. Each

firm can produce gadgets with no marginal cost or fixed cost. Suppose that these two

producers have formed a cartel, agreed to split production of output evenly, and are

maximizing total industry profits. If Margaret decides to cheat on the agreement and sell

100 more gadgets, the market price of gadgets will be:

A)

$4.

B)

$5.

C)

$6.

D)

$7.

Page 5

17.

(Ref 30-1 Table: Demand Schedule of Gadgets) Use Table 30-1: Demand Schedule of

Gadgets. The market for gadgets consists of two producers, Margaret and Ray. Each

firm can produce gadgets with no marginal cost or fixed cost. Suppose that these two

producers have formed a cartel, agreed to split production of output evenly, and are

maximizing total industry profits. If Margaret decides to cheat on the agreement and sell

100 more gadgets, Margaret’s profit will be _____, and Ray’s profit will be _____.

A)

$1,250; $1,250

B)

$500; $500

C)

$1,400; $1,000

D)

$1,000; $1,400

18.

(Ref 30-1 Table: Demand Schedule of Gadgets) Use Table 30-1: Demand Schedule of

Gadgets. The market for gadgets consists of two producers, Margaret and Ray. Each

firm can produce gadgets with no marginal cost or fixed cost. Suppose that these two

producers have formed a cartel, agreed to split production of output evenly, and are

maximizing total industry profits. If Margaret decides to cheat on the agreement and sell

100 more gadgets, Margaret’s quantity effect will be a(n) _____ in profit of _____.

A)

decrease; $250

B)

increase; $150

C)

increase; $400

D)

decrease; $400

19.

(Ref 30-1 Table: Demand Schedule of Gadgets) Use Table 30-1: Demand Schedule of

Gadgets. The market for gadgets consists of two producers, Margaret and Ray. Each

firm can produce gadgets with no marginal cost or fixed cost. Suppose that these two

producers have formed a cartel, agreed to split production of output evenly, and are

maximizing total industry profits. If Margaret decides to cheat on the agreement and sell

100 more gadgets, Margaret’s price effect will be a(n) _____ in profit of _____.

A)

decrease; $400

B)

increase; $400

C)

increase; $250

D)

decrease; $250

Page 6

20.

(Ref 30-1 Table: Demand Schedule of Gadgets) Use Table 30-1: Demand Schedule of

Gadgets. The market for gadgets consists of two producers, Margaret and Ray. Each

firm can produce gadgets with no marginal cost or fixed cost. Suppose that these two

producers have formed a cartel, agreed to split production of output evenly, and are

maximizing total industry profits. If Margaret decides to cheat on the agreement and sell

100 more gadgets but Ray continues to sell 250 gadgets, Ray’s profits will be:

A)

$1,400.

B)

$1,250.

C)

$1,000.

D)

$400.

21.

(Ref 30-1 Table: Demand Schedule of Gadgets) Use Table 30-1: Demand Schedule of

Gadgets. The market for gadgets consists of two producers, Margaret and Ray. Each

firm can produce gadgets with no marginal cost or fixed cost. If industry output is 350

gadgets produced by Margaret and 250 gadgets produced by Ray and if Ray decides to

increase output by an additional 100 gadgets, industry output will be:

A)

700.

B)

600.

C)

500.

D)

400.

22.

(Ref 30-1 Table: Demand Schedule of Gadgets) Use Table 30-1: Demand Schedule of

Gadgets. The market for gadgets consists of two producers, Margaret and Ray. Each

firm can produce gadgets with no marginal cost or fixed cost. If industry output is 350

gadgets produced by Margaret and 250 gadgets produced by Ray and if Ray decides to

increase output by an additional 100 gadgets, industry price will be:

A)

$3.

B)

$2.

C)

$1.

D)

$0.

23.

(Ref 30-1 Table: Demand Schedule of Gadgets) Use Table 30-1: Demand Schedule of

Gadgets. The market for gadgets consists of two producers, Margaret and Ray. Each

firm can produce gadgets with no marginal cost or fixed cost. If industry output is 350

gadgets produced by Margaret and 250 gadgets produced by Ray and if Ray decides to

increase output by an additional 100 gadgets, Margaret’s profit will be _____, and Ray’s

profit will be _____.

A)

$1,750; $1,250

B)

$1,250; $1,250

C)

$1,400; $1,000

D)

$1,050; $1,050

Page 7

24.

(Ref 30-1 Table: Demand Schedule of Gadgets) Use Table 30-1: Demand Schedule of

Gadgets. The market for gadgets consists of two producers, Margaret and Ray. Each

firm can produce gadgets with no marginal cost or fixed cost. If industry output is 700,

each firm’s profits will be _____ than they would be at the output of 500, which

maximizes industry profit.

A)

$150 less

B)

$150 more

C)

$200 more

D)

$200 less

25.

(Ref 30-1 Table: Demand Schedule of Gadgets) Use Table 30-1: Demand Schedule of

Gadgets. The market for gadgets consists of two producers, Margaret and Ray. Each

firm can produce gadgets with no marginal cost or fixed cost. Suppose that these two

producers have formed a cartel, agreed to split production of output evenly, and are

maximizing total industry profits. Total industry output would be _____ gadgets.

A)

10

B)

5

C)

50

D)

500

26.

(Ref 30-1 Table: Demand Schedule of Gadgets) Use Table 30-1: Demand Schedule of

Gadgets. The market for gadgets consists of two producers, Margaret and Ray. Each

firm can produce gadgets at a marginal cost of $2 and no fixed cost. If these two

producers formed a cartel, agreed to split production of output evenly, and acted to

maximize total industry profits, total industry output would be _____, and the price

would be _____.

A)

1,000; $10

B)

100; $9

C)

400; $6

D)

500; $5

27.

(Ref 30-1 Table: Demand Schedule of Gadgets) Use Table 30-1: Demand Schedule of

Gadgets. The market for gadgets consists of two producers, Margaret and Ray. Each

firm can produce gadgets at a marginal cost of $2 and no fixed cost. If these two

producers formed a cartel, agreed to split production of output evenly, and acted to

maximize total industry profits, total industry profit would be:

A)

$10,000.

B)

$5,000.

C)

$2,500.

D)

$1,600.

Page 8

28.

(Ref 30-1 Table: Demand Schedule of Gadgets) Use Table 30-1: Demand Schedule of

Gadgets. The market for gadgets consists of two producers, Margaret and Ray. Each

firm can produce gadgets at a marginal cost of $2 and no fixed cost. Suppose that these

two producers have formed a cartel, agreed to split production of output evenly, and are

maximizing total industry profits. Each firm’s output would be _____, and each firm’s

profit would be _____.

A)

500; $2,500

B)

200; $800

C)

1,000; $500

D)

1,000; $10,000

29.

(Ref 30-1 Table: Demand Schedule of Gadgets) Use Table 30-1: Demand Schedule of

Gadgets. The market for gadgets consists of two producers, Margaret and Ray. Each

firm can produce gadgets at a marginal cost of $2 and no fixed cost. Suppose that these

two producers have formed a cartel, agreed to split production of output evenly, and are

maximizing total industry profits. If Margaret decides to cheat on the agreement and sell

100 more gadgets, how many gadgets will Margaret sell?

A)

500

B)

200

C)

300

D)

600

30.

(Ref 30-1 Table: Demand Schedule of Gadgets) Use Table 30-1: Demand Schedule of

Gadgets. The market for gadgets consists of two producers, Margaret and Ray. Each

firm can produce gadgets at a marginal cost of $2 and no fixed cost. Suppose that these

two producers have formed a cartel, agreed to split production of output evenly, and are

maximizing total industry profits. If Margaret decides to cheat on the agreement and sell

100 more gadgets, the market price of gadgets will be:

A)

$4.

B)

$5.

C)

$6.

D)

$7.

Page 9

31.

(Ref 30-1 Table: Demand Schedule of Gadgets) Use Table 30-1: Demand Schedule of

Gadgets. The market for gadgets consists of two producers, Margaret and Ray. Each

firm can produce gadgets at a marginal cost of $2 and no fixed cost. Suppose that these

two producers have formed a cartel, agreed to split production of output evenly, and are

maximizing total industry profits. If Margaret decides to cheat on the agreement and sell

100 more gadgets, Margaret’s profit will be _____, and Ray’s profit will be _____.

A)

$1500; $1,000

B)

$900; $600

C)

$1,400; $1,000

D)

$1,000; $1,400

32.

(Ref 30-1 Table: Demand Schedule of Gadgets) Use Table 30-1: Demand Schedule of

Gadgets. The market for gadgets consists of two producers, Margaret and Ray. Each

firm can produce gadgets at a marginal cost of $2 and no fixed cost. Suppose that these

two producers have formed a cartel, agreed to split production of output evenly, and are

maximizing total industry profits. If Margaret decides to cheat on the agreement and sell

100 more gadgets, Margaret’s quantity effect will be a(n) _____ in profit of _____.

A)

decrease; $100

B)

increase; $100

C)

increase; $300

D)

decrease; $300

33.

(Ref 30-1 Table: Demand Schedule of Gadgets) Use Table 30-1: Demand Schedule of

Gadgets. The market for gadgets consists of two producers, Margaret and Ray. Each

firm can produce gadgets at a marginal cost of $2 and no fixed cost. Suppose that these

two producers have formed a cartel, agreed to split production of output evenly, and are

maximizing total industry profits. If Margaret decides to cheat on the agreement and sell

100 more gadgets, Margaret’s price effect will be a(n) _____ in profit of _____.

A)

decrease; $400

B)

increase; $400

C)

increase; $200

D)

decrease; $200

Page 10

34.

(Ref 30-1 Table: Demand Schedule of Gadgets) Use Table 30-1: Demand Schedule of

Gadgets. The market for gadgets consists of two producers, Margaret and Ray. Each

firm can produce gadgets at a marginal cost of $2 and no fixed cost. Suppose that these

two producers have formed a cartel, agreed to split production of output evenly, and are

maximizing total industry profits. If Margaret decides to cheat on the agreement and sell

100 more gadgets but Ray continues to sell 200 gadgets, Ray’s profits will be:

A)

$1,400.

B)

$1,250.

C)

$600.

D)

$400.

35.

(Ref 30-1 Table: Demand Schedule of Gadgets) Use Table 30-1: Demand Schedule of

Gadgets. The market for gadgets consists of two producers, Margaret and Ray. Each

firm can produce gadgets at a marginal cost of $2 and no fixed cost. If industry output is

300 gadgets produced by Margaret and 200 gadgets produced by Ray and if Ray decides

to increase output by an additional 100 gadgets, industry output will be:

A)

700.

B)

600.

C)

500.

D)

400.

36.

(Ref 30-1 Table: Demand Schedule of Gadgets) Use Table 30-1: Demand Schedule of

Gadgets. The market for gadgets consists of two producers, Margaret and Ray. Each

firm can produce gadgets at a marginal cost of $2 and no fixed cost. If industry output is

300 gadgets produced by Margaret and 200 gadgets produced by Ray and if Ray decides

to increase output by an additional 100 gadgets, industry price will be:

A)

$4.

B)

$3.

C)

$2.

D)

$1.

37.

(Ref 30-1 Table: Demand Schedule of Gadgets) Use Table 30-1: Demand Schedule of

Gadgets. The market for gadgets consists of two producers, Margaret and Ray. Each

firm can produce gadgets at a marginal cost of $2 and no fixed cost. If industry output is

300 gadgets produced by Margaret and 200 gadgets produced by Ray and if Ray decides

to increase output by an additional 100 gadgets, Margaret’s profit will be _____, and

Ray’s profit will be _____.

A)

$1,750; $1,250

B)

$1,250; $1,250

C)

$1,400; $1,000

D)

$600; $600

Page 11

38.

(Ref 30-1 Table: Demand Schedule of Gadgets) Use Table 30-1: Demand Schedule of

Gadgets. The market for gadgets consists of two producers, Margaret and Ray. Each

firm can produce gadgets at a marginal cost of $2 and no fixed cost. If the industry were

actually perfectly competitive, the output would be _____ gadgets, and the price would

be _____.

A)

0; $10

B)

500; $5

C)

600; $4

D)

800; $2

Use the following to answer questions 39-49:

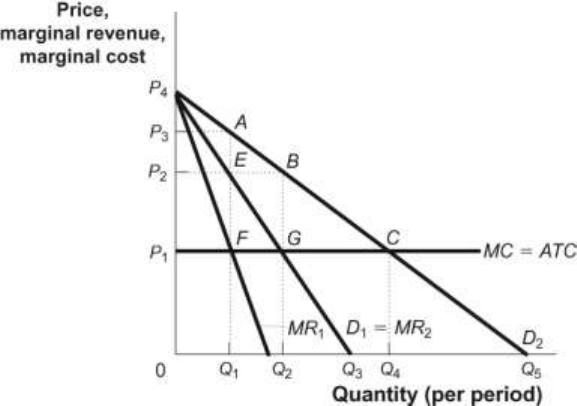

Figure: Monopoly Profits in Duopoly

39.

(Ref 30-2 Figure: Monopoly Profits in Duopoly) Use Figure 30-2: Monopoly Profits in

Duopoly. If there were two firms in this industry, they could engage in _____ and reap

monopoly profits.

A)

game theory

B)

the prisoners’ dilemma

C)

collusive behavior

D)

measuring the four-firm concentration ratio

Page 12

40.

(Ref 30-2 Figure: Monopoly Profits in Duopoly) Use Figure 30-2: Monopoly Profits in

Duopoly. Suppose there are two firms in this industry. Each firm faces an identical

demand curve, D1, and the market demand curve is D2. The figure illustrates how firms

can reap monopoly profits, even in an industry with:

A)

free entry and exit.

B)

two firms.

C)

monopolistic competition.

D)

a four-firm concentration ratio of 50.

41.

(Ref 30-2 Figure: Monopoly Profits in Duopoly) Use Figure 30-2: Monopoly Profits in

Duopoly. The figure shows how an industry consisting of two firms that face identical

demand curves (D1) can collude to increase profits. Which assumption is not a part of

the analysis illustrated by the model?

A)

The two firms are identical.

B)

The two firms sell identical products.

C)

While the firms face the same MC curves, their respective TC curves have unequal

slopes.

D)

Each firm has a horizontal marginal cost curve.

42.

(Ref 30-2 Figure: Monopoly Profits in Duopoly) Use Figure 30-2: Monopoly Profits in

Duopoly. The figure shows how an industry consisting of two firms that face identical

demand curves (D1) can collude to increase profits. The market demand curve is D2.

Which assumption is part of the analysis illustrated by the model?

A)

The two firms have identical marginal cost but different average total cost.

B)

The two firms sell differentiated products.

C)

The MR curve is not relevant to either firm’s choices.

D)

The firms can act as a cartel and maximize their combined economic profit.

43.

(Ref 30-2 Figure: Monopoly Profits in Duopoly) Use Figure 30-2: Monopoly Profits in

Duopoly. The figure shows how an industry consisting of two firms that face identical

demand curves (D1) can collude to increase profits. The market demand curve is D2. If

the firms collude to share the market demand equally, then each firm will act as if its

demand curve is given by:

A)

D1.

B)

D2.

C)

MR1.

D)

2 *D1.

Page 13

44.

(Ref 30-2 Figure: Monopoly Profits in Duopoly) Use Figure 30-2: Monopoly Profits in

Duopoly. The figure shows how an industry consisting of two firms that face identical

demand curves (D1) can collude to increase profits. If the firms collude to share the

market demand equally, then each firm will act as if its marginal revenue curve is given

by:

A)

MR1.

B)

2 * MR1.

C)

MR2.

D)

MC.

45.

(Ref 30-2 Figure: Monopoly Profits in Duopoly) Use Figure 30-2: Monopoly Profits in

Duopoly. The figure shows how an industry consisting of two firms that face identical

demand curves (D1) can collude to increase profits. If the firms collude to share the

market demand equally, then each firm will act as if its demand curve is given by

_____, while the market demand curve is given by _____.

A)

D1; MR2

B)

D2; D1

C)

D1; D2

D)

MR1; MR2

46.

(Ref 30-2 Figure: Monopoly Profits in Duopoly) Use Figure 30-2: Monopoly Profits in

Duopoly. Given the duopoly industry illustrated in the figure, if each firm acted on the

belief that it faced demand curve D2 and acted without consideration of the other, each

firm would attempt to maximize economic profits by producing quantity _____ and

setting price equal to _____.

A)

Q4; P1

B)

Q4; P2

C)

Q1; P4

D)

Q2; P2

47.

(Ref 30-2 Figure: Monopoly Profits in Duopoly) Use Figure 30-2: Monopoly Profits in

Duopoly. Firms in the duopoly industry illustrated in the figure have zero fixed costs.

The market demand curve is D2. If the two firms colluded to maximize their combined

economic profits, they would set the market price at _____, and combined economic

profits of the firms would be _____.

A)

P1; given by the area of the rectangle 0P1CQ4

B)

P1; zero

C)

P3; given by the area of the rectangle 0P3AQ1

D)

P2; given by the area of the rectangle P1P2BG

Page 14

48.

(Ref 30-2 Figure: Monopoly Profits in Duopoly) Use Figure 30-2: Monopoly Profits in

Duopoly. The efficient solution in the figure is found where price is _____ and quantity

is _____.

A)

P1; Q4

B)

P2; Q2

C)

P2; Q1

D)

P3; Q1

49.

(Ref 30-2 Figure: Monopoly Profits in Duopoly) Use Figure 30-2: Monopoly Profits in

Duopoly. If the two firms in the figure colluded to split production evenly and to

maximize their joint profits, the market price they set would be _____, and each firm’s

economic profit would be _____. (Assume that the market demand curve is D2.)

A)

P2; given by the area of the rectangle bounded by P1P2EF = FEBG

B)

P1; P1P3AF

C)

P3; given by the area of the rectangle bounded by 0P3AQ1

D)

P2; given by the area of the rectangle bounded by P1P2BG

Use the following to answer questions 50-51:

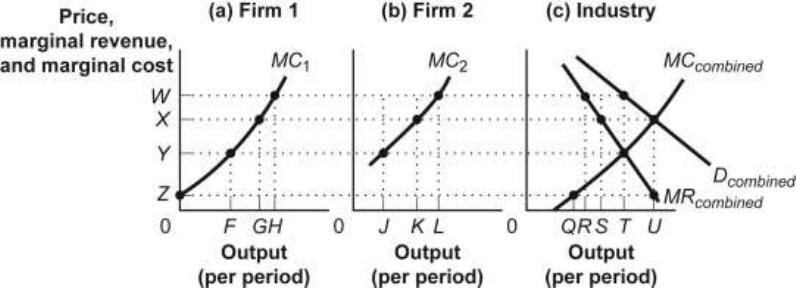

Figure: Collusion

50.

(Ref 30-3 Figure: Collusion) Use Figure 30-3: Collusion. The quantity of output

produced by the industry with collusion is shown by:

A)

Q.

B)

R.

C)

S.

D)

T.

Page 15

51.

(Ref 30-3 Figure: Collusion) Use Figure 30-3: Collusion. The price charged by the

industry with collusion is shown by:

A)

W.

B)

X.

C)

Y.

D)

Z.

Use the following to answer questions 52-61:

52.

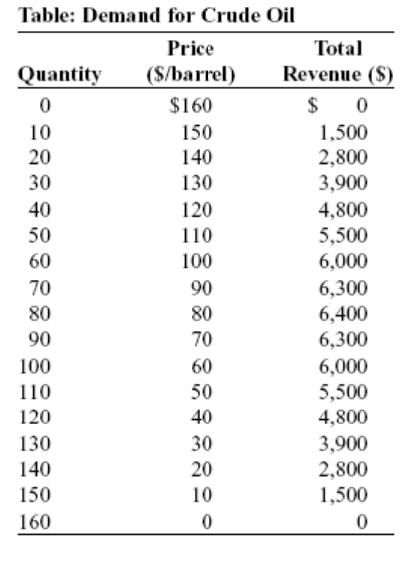

(Ref 30-4 Table: Demand for Crude Oil) Use Table 30-4: Demand for Crude Oil.

Assume that the crude oil industry is a duopoly and the marginal cost of producing

crude oil is zero. If the two firms collude to share the market equally, the price of crude

oil will be _____, firm 1 will produce _____ barrels, firm 2 will produce _____ barrels,

and each firm will earn revenue equal to _____.

A)

$80; 80; 80; $6,400

B)

$80; 40; 40; $3,200

C)

$60; 50; 50; $3,000

D)

$40; 60; 60; $2,400

Page 16

53.

(Ref 30-4 Table: Demand for Crude Oil) Use Table 30-4: Demand for Crude Oil. The

marginal cost of producing crude oil is zero. If the crude oil industry is a monopoly, the

price of crude oil will be _____, the total quantity of crude oil produced by the

monopoly will be _____ barrels, and the monopoly will earn revenue equal to _____.

A)

$80; 80; $6,400

B)

$80; 80; $0

C)

$160; 0; $0

D)

$60; 100; $6,000

54.

(Ref 30-4 Table: Demand for Crude Oil) Use Table 30-4: Demand for Crude Oil.

Assume that the crude oil industry is a duopoly and the marginal cost of producing

crude oil is zero. Suppose that the two firms are maximizing industry profit and splitting

the profit evenly. If firm 1 decides to cheat and increase production by 10 more barrels,

total industry output will be _____ barrels.

A)

160

B)

100

C)

90

D)

80

55.

(Ref 30-4 Table: Demand for Crude Oil) Use Table 30-4: Demand for Crude Oil.

Assume that the crude oil industry is a duopoly and the marginal cost of producing

crude oil is zero. Suppose that the two firms are maximizing industry profit and splitting

the profit evenly. If firm 1 decides to cheat and increase production by 10 more barrels,

the price of crude oil will be:

A)

$0.

B)

$70.

C)

$80.

D)

$160.

56.

(Ref 30-4 Table: Demand for Crude Oil) Use Table 30-4: Demand for Crude Oil.

Assume that the crude oil industry is a duopoly and the marginal and fixed cost of

producing crude oil equals zero. Suppose that the two firms are maximizing industry

profit and splitting the profit evenly. If firm 1 decides to cheat and increase production

by 10 more barrels, it will earn profits of:

A)

$6,400.

B)

$6,300.

C)

$3,500.

D)

$2,800.

Page 17

57.

(Ref 30-4 Table: Demand for Crude Oil) Use Table 30-4: Demand for Crude Oil.

Assume that the crude oil industry is a duopoly and the marginal cost and fixed cost of

producing crude oil equals zero. Suppose that the two firms are maximizing industry

profit and splitting the profit evenly. If firm 1 decides to cheat and increase production

by 10 more barrels and firm 2 continues to produce 40 barrels, firm 2 will earn profits

of:

A)

$6,400.

B)

$6,300.

C)

$3,500.

D)

$2,800.

58.

(Ref 30-4 Table: Demand for Crude Oil) Use Table 30-4: Demand for Crude Oil.

Assume that the crude oil industry is a duopoly and the marginal cost and fixed cost of

producing crude oil equal zero. Suppose that the two firms are maximizing industry

profit and splitting the profit evenly. If both firms decide to cheat and produce 10 more

barrels each, industry output will be _____ barrels.

A)

100

B)

120

C)

110

D)

160

59.

(Ref 30-4 Table: Demand for Crude Oil) Use Table 30-4: Demand for Crude Oil.

Assume that the crude oil industry is a duopoly and the marginal cost and fixed cost of

producing crude oil equal zero. Suppose that the two firms are maximizing industry

profit and splitting the profit evenly. If both firms decide to cheat and produce 10 more

barrels each, the price of crude oil will be:

A)

$160.

B)

$80.

C)

$70.

D)

$60.

60.

(Ref 30-4 Table: Demand for Crude Oil) Use Table 30-4: Demand for Crude Oil.

Assume that the crude oil industry is a duopoly and the marginal and fixed cost of

producing crude oil equals zero. Suppose that the two firms are maximizing industry

profit and splitting the profit evenly. If both firms decide to cheat and produce 10 more

barrels each, firm 1’s profit will be _____, and firm 2’s profit will be _____.

A)

$3,200; $3,200

B)

$3,200; $3,000

C)

$3,000; $3,200

D)

$3,000; $3,000

Page 18

61.

(Ref 30-4 Table: Demand for Crude Oil) Use Table 30-4: Demand for Crude Oil.

Assume that the crude oil industry is a duopoly and the marginal and fixed costs of

producing crude oil equal zero. Suppose that the two firms are maximizing industry

profit and splitting the profit evenly. If both firms engage in noncooperative behavior,

the industry output will be _____ barrels, and the price of crude oil will be _____.

A)

0; $160

B)

80; $80

C)

100; $60

D)

160; $0

62.

Market power in the United States was often gained in the latter part of the nineteenth

century by:

A)

forming trusts.

B)

the growth of competition.

C)

international arrangements with Russian and Japanese firms.

D)

opening up more industries to international trade.

63.

Attempts by the federal government to prevent the exercise of monopoly power in the

United States are known as _____ policy.

A)

stabilization

B)

antitrust

C)

fiscal

D)

government

64.

Antitrust policy refers to government:

A)

attempts to prevent the acquisition of monopoly power.

B)

attempts to encourage the exercise of monopoly power.

C)

encouragement of collusion in the marketplace.

D)

attempts to limit private enterprise.

65.

The FIRST law designed to curb monopoly power in the United States was the _____

Act.

A)

Sherman Antitrust

B)

Clayton

C)

Federal Trade Commission

D)

Robinson-Patman

Page 19

66.

A major application of the Sherman Antitrust Act was in _____ against _____.

A)

1880; the Ford Motor Company

B)

1889; Bell

C)

1911; Standard Oil

D)

1889; Bell and Standard Oil

67.

The field of law that attempts to limit the ability of oligopolists to collude and restrict

competition is called:

A)

antitrust policy.

B)

product safety policy.

C)

fuel-efficiency standards.

D)

excise tax policy.

68.

One of the earliest actions of antitrust policy was the breakup of:

A)

the Standard Oil Company.

B)

Bell Telephone.

C)

Microsoft.

D)

IBM.

69.

Oligopoly first became an issue in the United States when:

A)

the Sons of Liberty dumped the East India Company’s tea into Boston Harbor in

1773.

B)

the Emancipation Proclamation was issued in 1863.

C)

the growth of railroads made possible a national market for goods in the second

half of the nineteenth century.

D)

Google purchased Motorola Mobility in 2011.

70.

A formal agreement to limit production and raise prices leads to:

A)

a cartel.

B)

perfect competition.

C)

monopolistic competition.

D)

oligopoly.

71.

Cartels became illegal in the United States in:

A)

1776.

B)

1890.

C)

1929.

D)

1982.

Page 20

72.

A trust:

A)

is a government agency that regulates natural monopolies.

B)

is the new organization that is formed when two firms merge.

C)

occurs when shareholders of the major companies in an industry turn over their

shares to a board of trustees who then control all of the companies.

D)

is another name for a large insurance company.

73.

The FIRST trust in the United States was established by _____ in the _____ industry.

A)

AT&T; communications

B)

Walt Disney; entertainment

C)

Amtrak; transportation

D)

Standard Oil; petroleum

74.

The purpose of the trusts established in the United States in the late 1800s was to:

A)

engage in monopoly pricing.

B)

promote international trade.

C)

promote competition in the transportation industry.

D)

limit the involvement of government in providing health care.

75.

The purpose of antitrust policy is to:

A)

limit pollution.

B)

provide access to affordable health care for uninsured Americans.

C)

prevent the exercise of monopoly power.

D)

control inflation and interest rates.

76.

The 1890 law intended to prevent the establishment of more monopolies and to break up

existing ones in the United States was the _____ Act.

A)

Taft-Hartley

B)

Sherman Antitrust

C)

Affordable Care

D)

Federal Trade Commission

77.

The government agency in the United States that reviews proposed mergers of firms in

the same industry and prohibits mergers that it believes will reduce competition is the:

A)

Commerce Department.

B)

Federal Reserve.

C)

Labor Department

D)

Department of Justice.

Page 21

78.

Which factor would make it difficult for oligopolists to collude?

A)

few firms

B)

few buyers

C)

similar costs of production

D)

a homogeneous product

79.

Which factor would make it difficult for Georgia peach suppliers to collude?

A)

only a few suppliers

B)

each supplier having the same costs

C)

buyers of peaches having very little bargaining power since peaches are

homogeneous

D)

only a few buyers of peaches

80.

The airline industry often engages in price wars. This means that firms often _____

prices until profits _____.

A)

raise; are maximized

B)

lower; are maximized

C)

lower; approach zero

D)

raise; approach zero

81.

Airlines are prone to price wars because:

A)

most fliers choose airlines on the basis of schedule and price.

B)

airline pricing is easy to understand.

C)

airlines have the same costs.

D)

airlines operate close to capacity.

82.

Tacit collusion is difficult if:

A)

there are many firms in the industry.

B)

the firms in the industry are producing differentiated products.

C)

firms have common interests.

D)

the oligopolists are selling to many small firms.

83.

Tacit collusion is relatively easy for oligopolists if:

A)

they are producing many different products.

B)

there are only a few firms in the industry.

C)

they are selling their product to only a few large buyers.

D)

barriers to entry into the industry are low.

Page 22

84.

As the number of firms in an oligopoly decreases:

A)

barriers to entry are likely to shrink.

B)

firms are less likely to engage in tacit collusion.

C)

firms are more likely to engage in tacit collusion.

D)

it becomes more difficult for the oligopoly to restrict output.

85.

If the several companies in the tobacco industry produce similar products but have very

different marginal costs:

A)

they are less likely to engage in tacit collusion than firms with similar costs.

B)

they are more likely to engage in tacit collusion than firms with similar costs.

C)

prices for tobacco products are more likely to be near the monopoly level than in

an industry whose firms have similar costs.

D)

output of tobacco products is more likely to be near the monopoly level than in an

industry whose firms have similar costs.

Use the following to answer questions 86-90:

86.

(Ref 30-5 Table: Demand for Solar Water Heaters) Use Table 30-5: Demand for Solar

Water Heaters. The marginal cost of producing solar water heaters is zero, and only two

firms, Rheem and Calefi, produce them. Suppose they agree to produce only 25 water

heaters each. By how much does Rheem’s profit rise if it cheats on the agreement and

produces 30 water heaters?

A)

$3,000

B)

$2,700

C)

$2,000

D)

$5,000

Page 23

87.

(Ref 30-5 Table: Demand for Solar Water Heaters) Use Table 30-5: Demand for Solar

Water Heaters. The marginal cost of producing solar water heaters is zero, and only two

firms, Rheem and Calefi, produce them. Suppose they agree to produce only 25 water

heaters each. If Rheem cheats on the agreement and produces 30 water heaters, what is

the price effect for Rheem?

A)

-$1,000

B)

-$2,500

C)

$2,000

D)

$1,000

88.

(Ref 30-5 Table: Demand for Solar Water Heaters) Use Table 30-5: Demand for Solar

Water Heaters. The marginal cost of producing solar water heaters is zero, and only two

firms, Rheem and Calefi, produce them. Suppose they agree to produce only 25 water

heaters each. If Rheem cheats on the agreement and produces 30 water heaters, what is

the quantity effect for Rheem?

A)

$1,000

B)

$4,500

C)

$2,000

D)

$9,000

89.

(Ref 30-5 Table: Demand for Solar Water Heaters) Use Table 30-5: Demand for Solar

Water Heaters. The marginal cost of producing solar water heaters is zero, and only two

firms, Rheem and Calefi, produce them. If Rheem and Calefi get into a price war, the

equilibrium price in the market will be:

A)

$0.

B)

$700.

C)

$800.

D)

$1,000.

90.

(Ref 30-5 Table: Demand for Solar Water Heaters) Use Table 30-5: Demand for Solar

Water Heaters. The marginal cost of producing solar water heaters is zero, and only two

firms, Rheem and Calefi, produce them. If they agree to collude, what price will the

cartel charge and how many water heaters will the cartel sell?

A)

$1,000; 50

B)

$1,100; 45

C)

$900; 55

D)

$800; 60

91.

Cartels are illegal in the United States.

A)

True

B)

False

Page 24

92.

One of the most inefficient ways for duopolists to earn a profit is to engage in collusion

or form a cartel.

A)

True

B)

False

93.

The fact that the price effect for an oligopolist is less than the price effect for a

monopolist helps explain why firms are likely to cheat on a cartel agreement.

A)

True

B)

False

94.

Suppose all of the firms in an industry form a cartel and succeed in raising the price to

the monopoly level by reducing output. Any single firm will find that it can increase its

profits by cheating on the cartel agreement.

A)

True

B)

False

95.

Oligopolists will earn zero profits unless they can collude.

A)

True

B)

False

96.

Each firm in a cartel has an incentive to break its word and produce more than the

agreed quantity.

A)

True

B)

False

97.

Until 1890, trusts in which firms in an industry agreed to limit production and raise

prices were legal in the United States.

A)

True

B)

False

98.

Antitrust legislation was first passed in the United States in 1776.

A)

True

B)

False

Page 25

99.

Oligopoly first became an issue in the United States in the second half of the nineteenth

century, when the growth of railroads allowed for a national market for goods.

A)

True

B)

False

100.

Cartels were legal in the United States until 1890.

A)

True

B)

False

101.

The purpose of the nineteenth-century cartels was to increase production and encourage

price competition.

A)

True

B)

False

102.

A trust is a government agency that enforces laws limiting the power of oligopolies.

A)

True

B)

False

103.

A trust is the organization that is formed when two large companies merge.

A)

True

B)

False

104.

A trust is formed when shareholders of the major companies in an industry place their

shares in the hands of a board of trustees who control the companies and act as a single

firm that can engage in monopoly pricing.

A)

True

B)

False

105.

The first trust in the United States was established in 1881 by lawyers at John D.

Rockefeller’s Standard Oil Company.

A)

True

B)

False

106.

The purpose of the trusts established in the United States in the late 1800s was to

decrease government spending and the size of the federal budget deficit.

A)

True

B)

False

Page 26

107.

The purpose of antitrust policy is to prevent the exercise of monopoly power.

A)

True

B)

False

108.

The law enacted in 1890 to break up existing monopolies and prevent the formation of

new ones was the Glass-Steagall Act.

A)

True

B)

False

109.

The law enacted in 1890 to break up existing monopolies and prevent the formation of

new ones was the Sherman Antitrust Act.

A)

True

B)

False

110.

The government agency in the United States that reviews proposed mergers of firms in

the same industry and prohibits mergers that it believes will reduce competition is the

Office of Management and Budget.

A)

True

B)

False

111.

The government agency in the United States that reviews proposed mergers of firms in

the same industry and prohibits mergers that it believes will reduce competition is the

Department of Justice.

A)

True

B)

False

112.

Until recently, most advanced countries except the United States did not have policies

against price fixing.

A)

True

B)

False

113.

The breakup of Microsoft in 2005 was one of the first applications of antitrust policy in

the United States.

A)

True

B)

False

Page 27

114.

The breakup of Standard Oil in 1911 was one of the first applications of antitrust policy

in the United States.

A)

True

B)

False

115.

For approximately the past 20 years, the European Union has enforced antitrust policies

for its member countries.

A)

True

B)

False

116.

The purpose of the Sherman Antitrust Act was to encourage the establishment of

monopolies to replace trusts.

A)

True

B)

False

117.

Suppose that Walmart buys fresh roses from several hundred small backyard gardeners

in California. These gardeners are very likely to be able to engage successfully in tacit

collusion.

A)

True

B)

False

118.

Tacit collusion is most likely to occur if there are only a few firms in the industry.

A)

True

B)

False

119.

Tacit collusion is relatively less likely to occur in an industry with 3 firms than it is in an

industry with 10 firms.

A)

True

B)

False

120.

If there are many firms in an industry, there is little incentive for firms to engage in tacit

collusion because a smaller proportion of the units of the product sold are affected by

the price effect if a firm increases output.

A)

True

B)

False

Page 28

121.

Oligopoly firms that produce only cement are less likely to collude than firms in a cell

phone oligopoly.

A)

True

B)

False

122.

Tacit collusion is likely to occur when firms have different market shares.

A)

True

B)

False

123.

Suppose an oligopoly is composed of four firms. One firm has a 50% market share;

another firm, 35%; another, 10%; and the fourth, 5%. It will be easier for this industry to

engage in tacit collusion than it would for an oligopoly each of whose four firms has

25% of the market.

A)

True

B)

False

124.

Until recently, most other advanced countries did not have policies that prohibited price

fixing.

A)

True

B)

False

125.

A price war occurs when tacit collusion breaks down and aggressive price competition

causes prices to collapse.

A)

True

B)

False

126.

In a price war, firms in an oligopoly often push prices up to the monopoly level.

A)

True

B)

False

Page 29

Use the following to answer question 127:

127.

(Ref 30-6 Table: Demand Schedule of Gadgets) Use Table 30-1: The Market for

Gadgets. Two producers, Margaret and Ray, dominate the market. Each firm can

produce gadgets at marginal costs of zero and without fixed costs.

A) If these firms form a cartel to maximize joint profits, what output level will be

produced and at what price? If the output is shared evenly, how much profit will each

firm earn?

B) Suppose that Margaret decides to increase production by 100 gadgets and Ray

leaves output constant. What will be the new market price and output? How much profit

will each firm earn?

128.

Why do the United States and many other countries have antitrust laws? What’s so

harmful about oligopoly that it warrants an entire body of law?

129.

Maximization of joint profits is MOST likely when firms are:

A)

perfect competitors.

B)

monopolistic competitors.

C)

duopolists who collude.

D)

natural monopolists.

130.

Cartels made up of a large number of firms are unstable because each firm in the cartel:

A)

has an incentive to cheat.

B)

is producing a relatively homogeneous product in which entry barriers are low.

C)

does not have to worry about losses.

D)

recognizes that the market size is relatively stable.

Page 30

131.

Both monopolists and cartel members will find that a drop-in price leads to:

A)

a quantity effect that reduces total revenue.

B)

a price effect that reduces total revenue.

C)

a quantity effect that has no effect on total revenue.

D)

neither a price nor a quantity effect.

132.

Given the large amount of interdependence among them, cooperation with one’s

competitors is the most profitable strategy for:

A)

perfect competitors.

B)

monopolistic competitors.

C)

oligopolists.

D)

monopolists.

133.

(Scenario: Two Identical Firms) Use Scenario: Two Identical Firms. Suppose the two

firms decide to cooperate and collude, resulting in the same amount of production for

each firm. What is the profit-maximizing price and output for the industry?

Scenario: Two Identical Firms

Two identical firms make up an industry in which the market demand curve is

represented by Q = 5,000 – 4P, where Q is the quantity demanded and P is price per

unit. The marginal cost of producing the good in this industry is constant and equal to

$650. Fixed cost is zero.

A)

P = $400, Q = 5,000

B)

P = $950, Q = 1,200

C)

P = $600, Q = 1,500

D)

P = $300, Q = 2,000

134.

The Sherman Antitrust Act:

A)

was aimed at preventing the establishment of more monopolies and was the

beginning of antitrust policy.

B)

introduced the HHI measure to industries.

C)

initially allowed firms to collude legally.

D)

allowed the establishment of trusts.

135.

A customer with significant buying power in an industry would:

A)

make a tacit price agreement more difficult to achieve.

B)

make a tacit price agreement easier to achieve.

C)

have no effect on tacit pricing agreement negotiations.

D)

result in a kinked demand curve.

Page 31

Page 33

Page 34