[Question]

53. The government has bailed out homeowners who are in danger of foreclosure. However,

future homeowners may deduce that the government will again bail them out in the case of future

economic turmoil. The government inadvertently has created what is known as:

A. deleveraging.

B. the law of diminishing control.

C. moral hazard.

D. herding.

54. Which of the following is not an example of moral hazard?

A. Investment banks use 40-1 leverage, knowing that if the market collapses, the government

will come to the rescue.

B. Domestic automobile companies fail to design high-quality fuel-efficient cars, hoping that the

government will save them if oil prices skyrocket.

C. A backcountry skier takes an excessively dangerous run, knowing that local rescue crews will

come to his aid if he gets in an accident.

D. Insurance companies stopped offering insurance policies in New Orleans after a major

hurricane, knowing the government will offer subsidies to draw people back.

55. To offset the moral hazard problem created by the FDIC, government:

A. created securities to spread the risks.

B. created the Federal Reserve Bank.

C. separated banks from other financial institutions.

D. required individuals to pay a portion of the insurance costs.

56. Which is not a measure instituted to offset the moral hazard problem created by the FDIC?

A. Established strict regulations of banks.

B. The creation of the Federal Reserve Bank.

C. Separating banks from other financial institutions.

D. Require financial transactions essential to the economy to remain in banks.

57. The Glass-Steagall Act was set up to:

A. regulate financial institutions after the Savings and Loan Crisis the 1980s.

B. give the federal government the sole responsibility in carrying out fiscal policy to regulate the

economy.

C. establish banking regulations and deposit insurance as a result of the 1930s crisis.

D. regulate the derivatives market as a result of the 2008 crisis.

58. Whenever a regulatory system is set up, individuals or firms being regulated will figure out

ways to get around these regulations. This is referred to as the law of:

A. diminishing returns.

B. unintended consequences.

C. diminishing control.

D. demand.

59. Which of the following describes the law of diminishing marginal control?

A. The Federal Reserve Bank cannot impact excess reserves and the money supply.

B. Financial institutions have few ways to assess the solvency of borrowers.

C. After regulations are enacted, institutions find ways around the regulations.

D. As people engage in leverage, they have less and less control over the price of the asset.

60. Which of the following does not explain why the Glass-Steagall regulations lost their

effectiveness?

A. Over time, non-bank financial firms were able to borrow directly from the public, rather than

having to borrow from commercial banks.

B. The Federal Reserve created regulations that ran counter to what the government was trying

to do.

C. With the advent of new financial instruments, regulated banks lost business to unregulated

institutions, and credit began to flow through unregulated systems.

D. As regulations became too successful, people wanted to eliminate these regulations in order

to pursue the magic of the free market.

61. In the 1970s and 1980s, savings banks invented NOW accounts to get around financial

regulations. This is an example of:

A. a moral hazard problem.

B. deleveraging.

C. the law of diminishing control.

D. quantitative easing.

62. All of the following are examples of the law of diminishing control that followed banking

regulations put in place after the Great Depression except:

A. Banks created new instruments to circumvent the law.

B. Financial business migrated to unregulated institutions.

C. Depositors demanded financial institutions be responsible for their financial decisions.

D. Politicians were pressured to dismantle the regulations.

63. Which of the following did not contribute to the law of diminishing control?

A. New financial institutions and instruments.

B. Political pressure to reduce regulations.

C. New monetary policy tools.

D. Regulations covered fewer financial instruments.

64. If a firm or an industry is considered too big to fail, it is

A. unwise to regulate it because the regulation will slow growth.

B. wise to regulate it because the regulation will make it smaller.

C. wise to regulate it because of the moral hazard problem.

D. unwise to regulate it because it is too big.

65. The recent regulation that was designed to limit risk-taking by banks by requiring them to

report their holdings is called the:

A. The Glass-Steagall Act.

B. Dodd-Frank Wall Street Reform and Consumer Protection Act.

C. Troubled Asset Relief Program.

D. Federal Deposit Insurance Act.

66. The purpose of the Dodd-Frank Wall Street Reform Act was to:

A. encourage banks to engage in more risk-taking.

B. give banks the choice to report their holdings.

C. force banks to limit their risk-taking.

D. limit what stocks and mutual funds that investors could choose.

67. To avoid the law of diminishing control, the government could:

A. treat regulation as a one-time event that is not predictable.

B. leave the regulations the way they are.

C. let the Federal Reserve decide the regulations and implement the regulations.

D. change the regulations when it is appropriate to do so.

68. A general principle of regulation is:

A. do not offset the moral hazard problem.

B. set as few bad precedents as possible.

C. let banks fail regardless of the effect on the economy.

D. the need to reduce regulations over time.

69. Which of the following would not address the moral hazard problem?

A. Establish strict regulations of the banks

B. Design systems so that necessary financial transactions stayed within regulated banks

C. Allow the government to take over the policy-making decisions of the Federal Reserve

D. Separate banks from other financial institutions

70. Buying financial assets from banks and other financial institutions with newly created

money is referred to as:

A. credit easing.

B. operation twist.

C. quantitative easing.

D. precommitment policy.

71. Quantitative easing involves all of the following except:

A. higher long-term interest rates.

B. higher asset prices.

C. Lower long-term interest rates.

D. Purchasing longer-term bonds.

72. Quantitative easing refers to:

A. a gradual reduction in interest rates by the Federal Reserve.

B. looser restrictions on banks’ investments in derivatives.

C. a gradual reduction in marginal tax rates.

D. non-standard monetary policy designed to extend credit in the economy.

73. Which of the following would not fall under the description of unconventional monetary

policy by the Federal Reserve?

A. accepting lower quality assets as collateral for loans

B. opening lending facilities to non-commercial banks

C. directly purchasing short-term bonds from money market mutual funds

D. lowering the reserve requirement for banks

74. A policy of targeting a particular quantity of money by buying financial assets from banks

and other financial institutions with newly created money is called:

A. precommitment policy.

B. operation twist.

C. credit easing.

D. quantitative easing.

75. The aim of unconventional monetary policy tools is to:

A. stimulate the economy in coordination with fiscal policy.

B. slow down liquidity and increase interest rates.

C. support the economy by boosting liquidity and reducing interest rates when credit channels

are clogged.

D. increase the value of the dollar.

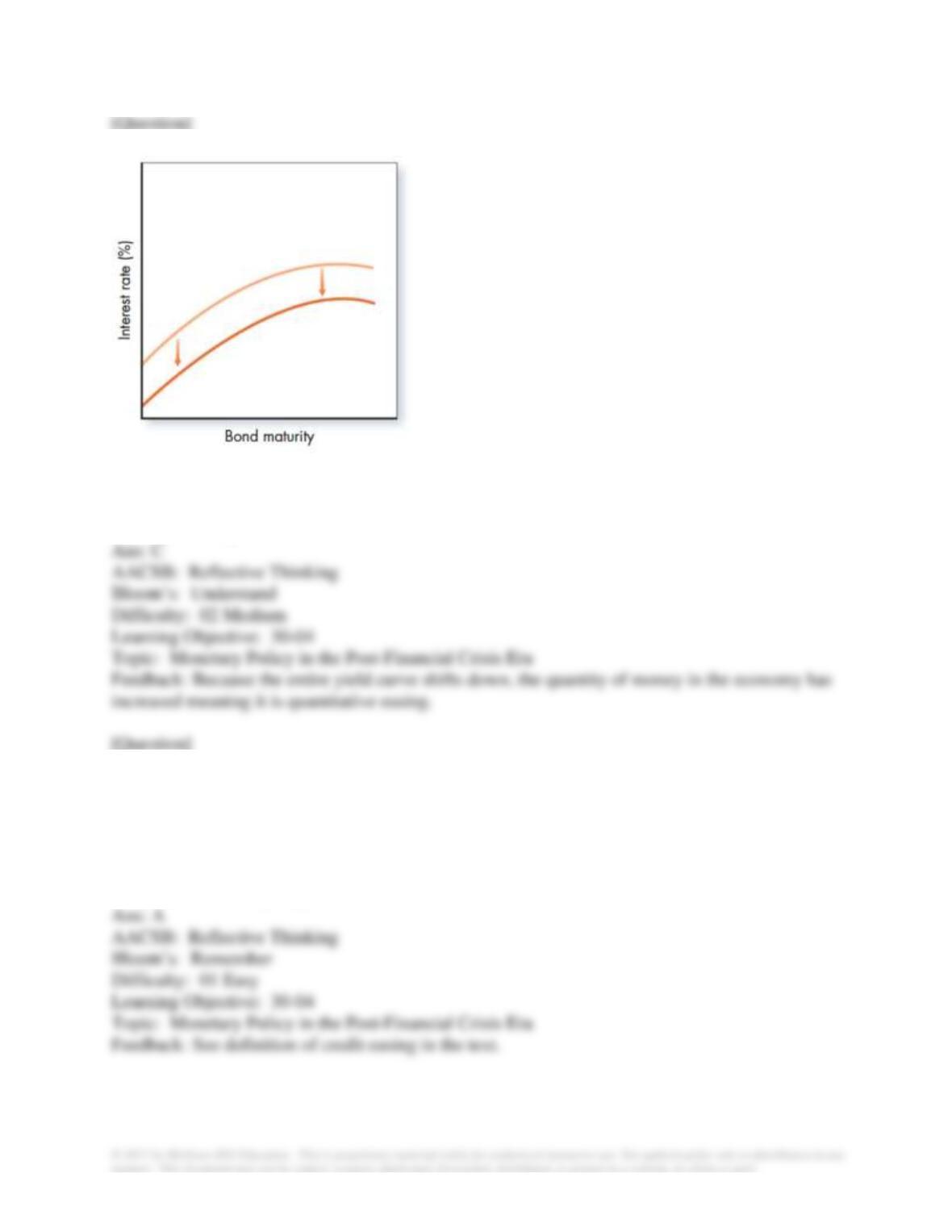

76. Which of the following would have the impact shown in the accompanying graph?

A. Operation twist.

B. Credit easing.

C. Quantitative easing.

D. Credit easing

77. Purchasing long-term government bonds from private financial corporations for the purpose

of changing the mix of securities held by the Fed toward less liquid and more risky assets is

called:

A. credit easing.

B. Operation twist.

C. quantitative easing.

D. precommitment policy.

78. The main difference between quantitative easing and credit easing is that:

A. quantitative easing changes the mix of the Fed’s holdings, credit easing does not.

B. credit easing changes the mix of the Fed’s holdings, quantitative easing does not.

C. credit easing shifts long-term interest rates down while quantitative easing shifts them up.

D. There is no difference since both add credit to the economy.

79. When the Fed is changing the quality of the assets it holds, this is called:

A. quantitative easing.

B. operation twist.

C. credit easing.

D. precommitment policy.

80. Which of the following is not one of the unconventional monetary policy tools used by the

Fed?

A. Precommitment strategy

B. Credit easing

C. Operation twist

D. Dodd-Frank Act

81. The graph shown shows what happens when the Fed implements:

A. operation twist.

B. credit easing.

C. quantitative easing.

D. precommitment policies.

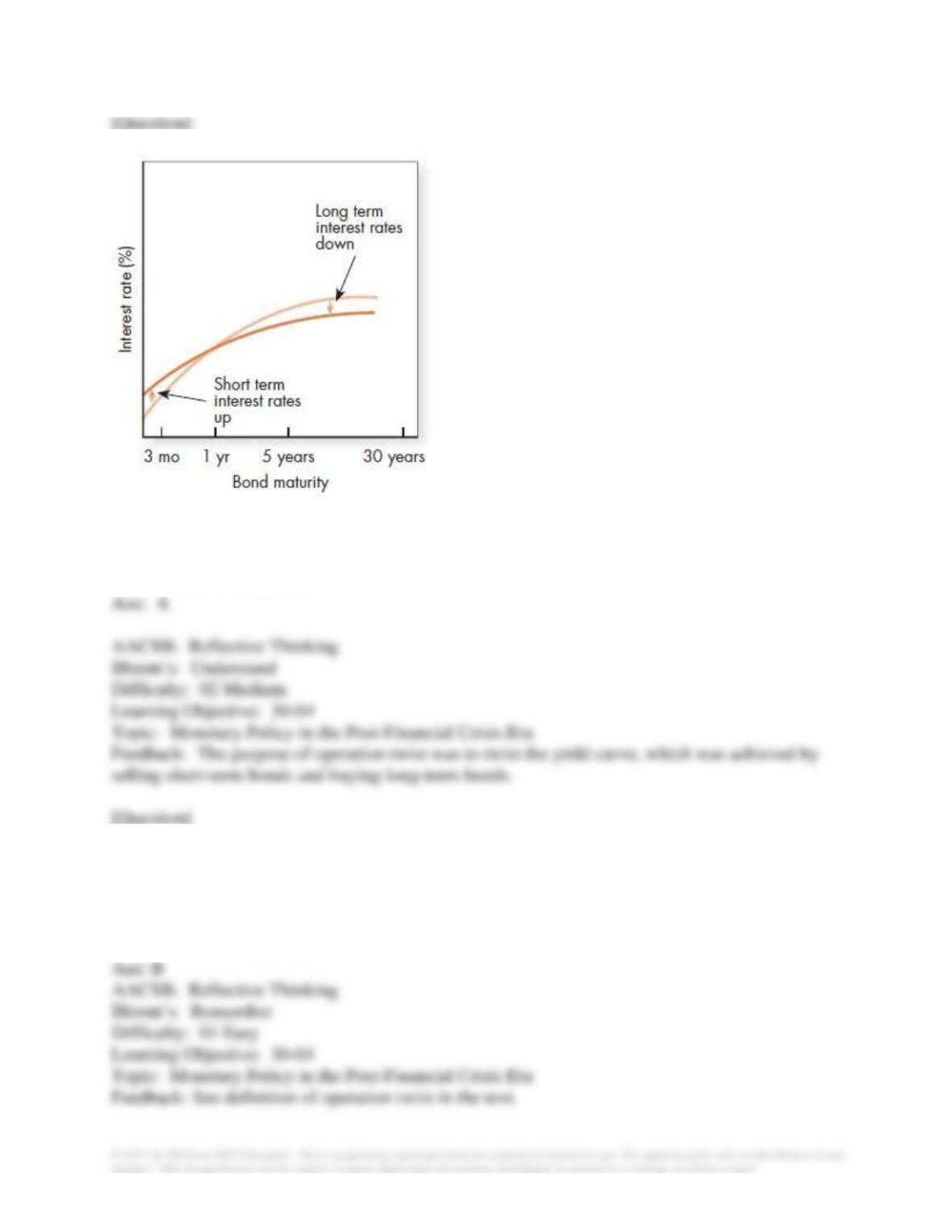

82. Selling short-term treasury bills and buying longer-term treasury bonds without creating

more new money is called:

A. standard monetary policy.

B. operation twist.

C. quantitative easing.

D. precommitment policy.

83. The Fed sells short-term debt and uses the proceeds to buy long-term debt. This represents:

A. precommitment policies.

B. standard monetary policy

C. quantitative easing.

D. operation twist.

84. A problem with a precommitment policy is that it:

A. determines the Fed’s response for a period of time.

B. binds the hands of the Fed from responding to unexpected events.

C. will cause the Fed to lose credibility.

D. locks the Fed into contractionary policy.

85. When the Fed promised to hold the Fed funds rate close to zero until the end of 2014, it was:

A. carrying out what’s known as operation twist.

B. carrying out what is known as credit easing.

C. following a precommitment policy.

D. following a policy that was recommended by Congress.

86. Negative interest rates

A. can only exist if there is inflation

B. are impossible

C. mean that lenders pay borrowers for making a loan

D. mean that borrowers pay lenders for making a loan

87. Higher inflation rates make it technically possible for the Fed to run more:

A. expansionary monetary policy

B. contractionary monetary policy

C. expansionary fiscal policy

D. contractionary fiscal policy

88. Negative interest rates are associated with

A. conventional monetary policy

B. unconventional monetary policy

C. conventional fiscal policy

D. unconventional fiscal policy

89. Negative interest rates

A. can only exist if there is inflation

B. are impossible

C. mean that lenders pay borrowers for making a loan

D. mean that borrowers pay lenders for making a loan

90. Economists now believe that interest rates

A. must be positive

B. can be negative, but only by a small amount

C. can be either negative or positive

D. must be negative

91. One of structural stagnationists’ criticisms of Fed policy after the financial crisis is that it:

A. broke up banks into commercial and noncommercial banks.

B. required workers to take pay cuts so that they would find jobs.

C. cause the economy to go through structural adjustments.

D. enabled government to run large deficits through lower interest rates.

92. The problem with the Fed’s exit strategy following the financial crisis is that it:

A. likely involves loosening bank regulations.

B. would increase the trade deficit.

C. didn’t have the support of Congress.

D. didn’t have one.

93. Which of the following is definitely not a valid criticism of the Fed’s unconventional

monetary policy tools?

A. The Fed does not have a reasonable exit strategy.

B. The Fed’s hands are tied when it comes to changing course.

C. It enables the government’s deficit spending.

D. The Fed was not approved by Congress.

94. A structural stagnationist’s criticism of unconventional monetary policy is that it:

A. cannot be unwound.

B. was too little too late.

C. props up asset prices.

D. forces Congress to address the debt.

95. A structural stagnationist’s criticism of unconventional monetary policy is that:

A. it kept the economy from making necessary structural adjustments.

B. the Fed would run out of reserves to infuse in the economy.

C. it would create goods inflation that would only accelerate.

D. it made banks correct their balance sheets too quickly.

96. A criticism of unconventional monetary policy is that it:

A. was not adding sufficient reserves to the economy.

B. kept interest rates higher than they needed to be.

C. meant that the public owed more and more to the Fed.

D. allowed the government to continue to run large deficits.

97. A criticism of unconventional monetary policy is that:

A. it involved the Fed holding too many long-term bonds, which were riskier than short-term

bonds.

B. the economy might have to go on the gold standard.

C. the FOMC would lose its ability to set monetary policy independently.

D. it dismantled too many banks, putting the economy at future risk.

98. Economic theory provides:

A. definitive guidance on monetary policy in conventional monetary policy

B. no guidance on monetary policy in conventional monetary policy

C. some guidance on monetary policy in conventional monetary policy

D. definitive guidance on monetary policy is unconventional monetary policy

99. Those who oppose the use of unconventional monetary policy tend to focus on:

A. the long run

B. the short run

C. both the short run and the long run

D. neither the short run or the long run