161. Assuming the Fed is following the Taylor Rule, if inflation is 3 percent, target inflation is 2

percent, and output is 1 percent above potential, what would you predict would be the Fed funds

rate target?

A. 4 percent.

B. 5 percent.

C. 5.5 percent.

D. 6 percent.

162. If inflation is one percentage point above the Fed’s target, the Taylor rule predicts that the

Fed should:

A. raise the federal funds rate by 0.5 percentage points.

B. raise the federal funds rate by 1.0 percentage points.

C. reduce the federal funds rate by 1.5 percentage points.

D. reduce the federal funds rate by 1.0 percentage points.

163. If output falls one percentage point below its potential, the Taylor rule predicts that the Fed

should:

A. reduce the federal funds rate by 0.5 percentage points.

B. reduce the federal funds rate by 1.0 percentage points.

C. raise the federal funds rate by 1.5 percentage points.

D. raise the federal funds rate by 1.0 percentage points.

164. Suppose the federal funds rate rises by 0.5 percent. If the Taylor rule is correct, this might

be because output is:

A. 1 percentage point below potential output.

B. 0.5 percentage points below potential output.

C. 0.5 percentage points above potential output.

D. 1 percentage point above potential output.

165. Assume that the federal funds rate is at its target, 2 percent, output is about 1 percent

beneath potential, and inflation is roughly 1.5 percent. If the Taylor rule is accurate, the Fed’s

desired rate of inflation at this time would be:

A. 1 percent.

B. 2.5 percent.

C. 3.5 percent.

D. 5 percent.

166. Using the Taylor rule, if inflation is 3 percent, desired inflation is 2 percent, and output is 2

percentage points above potential, the Fed should target a federal funds rate of:

A. 6.5.

B. 4.5.

C. 3.5.

D. 3.0.

167. Using the Taylor rule, if inflation is 1 percent, desired inflation is 2 percent, and output is 2

percentage points above potential, the Fed should target a federal funds rate of:

A. 6.5.

B. 4.5.

C. 3.5.

D. 3.0.

168. Using the Taylor rule, if inflation is 3 percent, desired inflation is 2 percent, and output is 2

percentage points below potential, the Fed should target a federal funds rate of:

A. 6.5.

B. 4.5.

C. 3.5.

D. 3.0.

169. Using the Taylor rule, if inflation is 1 percent, desired inflation is 2 percent, and output is 2

percentage points below potential, the Fed should target a federal funds rate of:

A. 6.5.

B. 4.5.

C. 2.5.

D. 1.5.

170. If the federal funds rate is at its target 3.5 percent, inflation is 1.5 percent, and target

inflation is 2.5 percent. If the Taylor rule is accurate, the output was:

A. 1 percent below potential.

B. 1 percent above potential.

C. 1.5 percent below potential.

D. 1.5 percent above potential.

0.5) / 0.5 = 1 percent.

171. The Federal Reserve kept interest rates low from 2002 through 2016 because:

A. they wanted to reduce the value of the dollar and help domestic exporters.

B. they were worried about inflation creeping into the economy.

C. they wanted to avoid deflation and the resulting recession.

D. they wanted to follow the Taylor Rule.

172. Between from 2002 through 2016 the Federal Reserve:

A. raised rates in order to follow the Taylor Rule.

B. left rates unchanged in order to follow the Taylor Rule.

C. lowered rates and went against the Taylor Rule.

D. abandoned the Taylor Rule in favor of the Greenspan Rule.

173. Some experts have argued that the Fed contributed to the housing bubble by:

A. approving the purchase of high-risk assets by banks, even though there was a risk of them

defaulting.

B. lowering interest rates, despite the fact that the Taylor rule indicated keeping them high.

C. not regulating non-bank financial institutions who were coming up with innovative

mortgages.

D. following the Taylor Rule, which during the 2000s indicated that rates should be kept low.

174. In general, the yield curve is:

A. flat.

B. upward sloping.

C. downward sloping.

D. shaped like a mountain.

175. If short-term and long-term interest rates are currently equal and the Fed contracts the

money supply, the yield curve would be expected to:

A. become downward sloping.

B. become upward sloping.

C. become vertical.

D. be unaffected.

176. If inflation becomes expected, and all other things remain as they were, the yield curve

would most likely become:

A. steeper.

B. flatter

C. flat.

D. vertical.

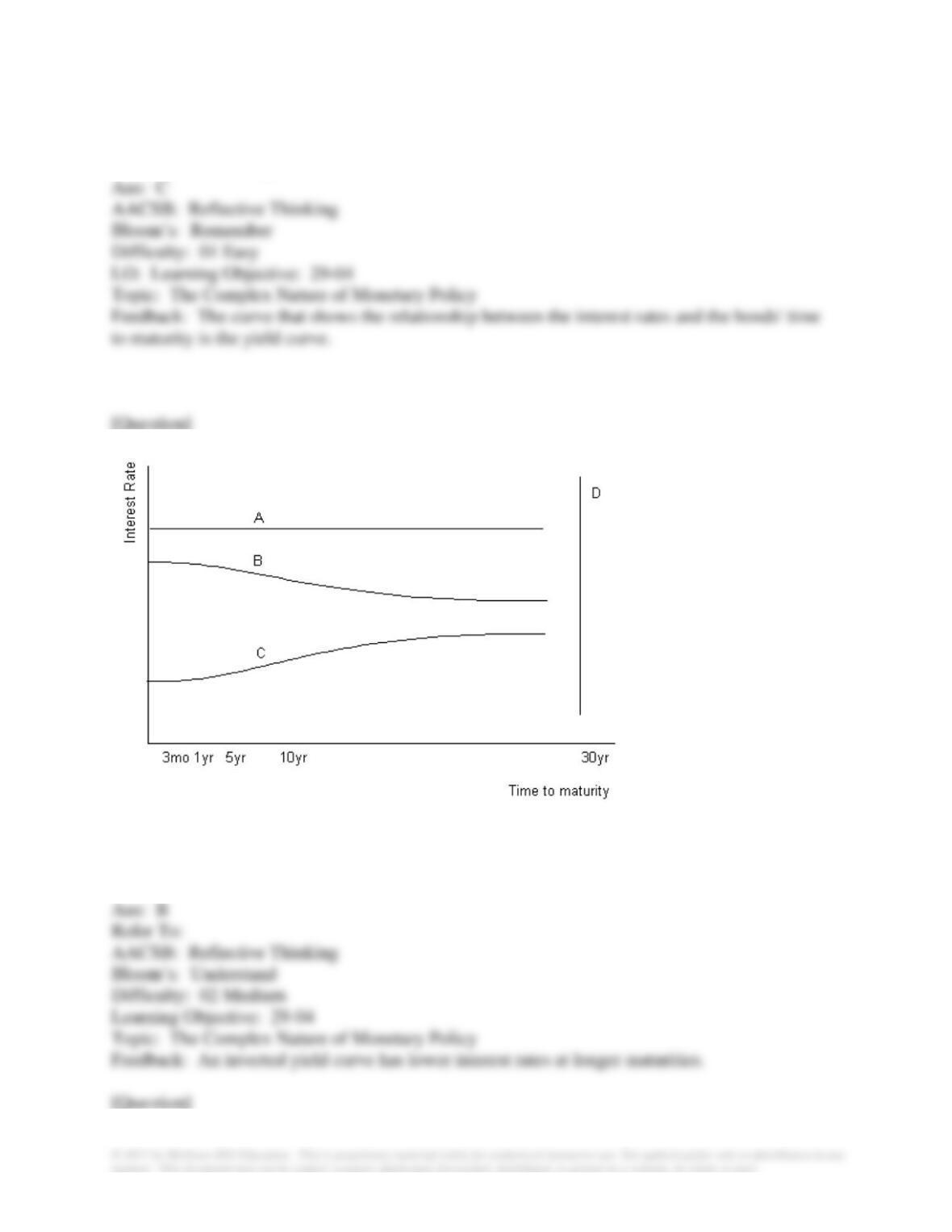

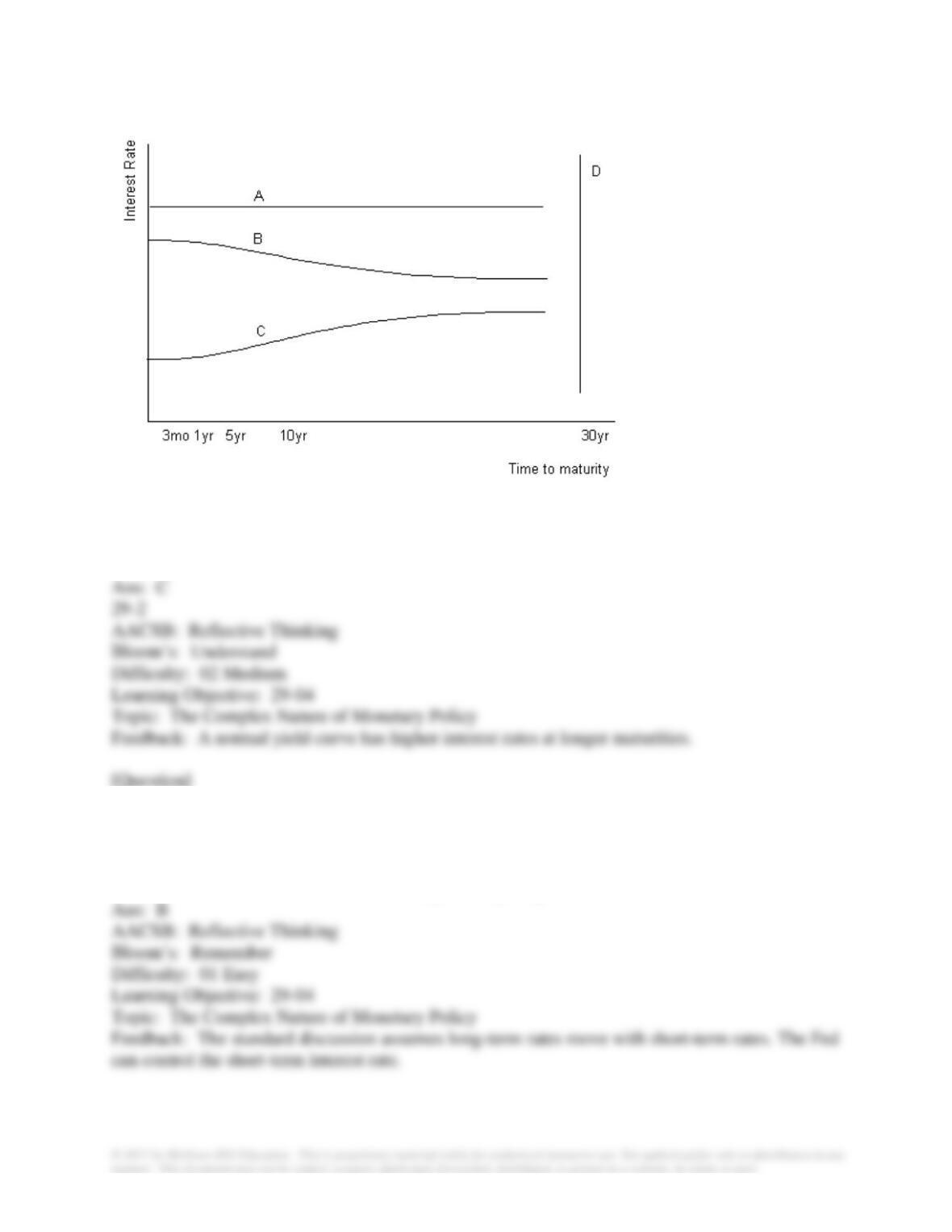

177. The curve most economists use to follow the relationship between the interest rates and

bonds’ time to maturity is the:

A. effective supply of money curve.

B. aggregate demand curve.

C. yield curve.

D. demand of money curve.

178. Refer to the graph shown. Which of the curves represents an inverted yield curve?

A. A

B. B

C. C

D. D

179. Refer to the graph shown. Which of the curves represents a normal yield curve?

A. A

B. B

C. C

D. D

180. The standard discussion of monetary policy is based on the assumption that:

A. long-term rates will fall when the Fed pushes up short-term interest rates.

B. long-term rates will rise when the Fed pushes up short-term interest rates.

C. short-term rates will fall when the Fed pushes up long-term interest rates.

D. short-term rates will rise when the Fed pushes up long-term interest rates.

181. The standard discussion of monetary policy is based on the assumption that the:

A. entire yield curve shifts up when the Fed sells government bonds.

B. entire yield curve shifts down when the Fed sells government bonds.

C. yield curve becomes inverted when the Fed buys government bonds.

D. yield curve becomes steeper when the Fed buys government bonds.

182. When an economy faces an inverted yield curve, compared to short-term bonds the long-

term bonds:

A. are riskier.

B. pay lower interest rates.

C. pay higher interest rates.

D. are a safe investment.

183. Which of the following gives the correct relationship between nominal and real interest

rates?

A. Real interest rate = nominal interest rate + expected inflation rate

B. Nominal interest rate = real interest rate + expected inflation rate

C. Nominal interest rate + real interest rate = expected inflation rate

D. Nominal interest rate = real interest rate – expected inflation

184. Suppose you are a lender and you expect inflation to be 4 percent over the next year

because inflation was 4 percent in the last year. If you want to earn a real return of 2 percent on

any loans you make, you will set the interest rate on your loans equal to:

A. 2 percent.

B. 4 percent.

C. 6 percent.

D. 10 percent.

185. Suppose you are a borrower and you expect inflation to be 6 percent over the next year

because inflation was 6 percent in the last year. If you do not want to pay more than 2 percent in

real terms for any loan you take out, you will not borrow if the interest rate is greater than:

A. 2 percent.

B. 6 percent.

C. 8 percent.

D. 30 percent.

186. If nominal interest rates increase:

A. the expected inflation rate must have gone up.

B. the real interest rate must have gone up.

C. either the expected inflation rate went up, the real interest rate went up, or both.

D. either the expected inflation rate went down, the real interest rate went down, or both.

187. Suppose the nominal interest rate in Brazil is 40 percent and the expected inflation rate is

150 percent. The real interest rate is:

A. -110 percent.

B. -190 percent.

C. 110 percent.

D. 190 percent.

188. Suppose the real interest rate in Brazil is 40 percent, actual inflation is 20 percent, and

expected inflation is 20 percent. The nominal interest must then be:

A. 20 percent.

B. 40 percent.

C. 60 percent.

D. 80 percent.

189. When people expect higher inflation, usually nominal interest rates will:

A. fall.

B. rise.

C. remain unchanged.

D. move erratically.

190. Suppose a contractionary monetary policy raises nominal interest rates. If this is the case,

it follows that the contractionary monetary policy must have:

A. reduced expected inflation.

B. increased expected inflation.

C. increased expected inflation more than it reduced real interest rates.

D. increased real interest rates more than it reduced expected inflation.

191. Suppose an expansionary monetary policy reduces nominal interest rates. If this is the

case, it follows that the expansionary monetary policy must have:

A. reduced expected inflation.

B. increased expected inflation.

C. increased expected inflation less than it reduced real interest rates.

D. reduced real interest rates less than it increased expected inflation.

192. The distinction between real and nominal interest rates:

A. makes it easier to assess the impact of monetary policy.

B. makes it harder to assess the impact of monetary policy.

C. does not affect the assessment of monetary policy since nominal interest rates are observable.

D. does not affect the assessment of monetary policy since real interest rates are observable.

193. As financial markets develop new and complex financial instruments, the Fed has:

A. more control over the long-term interest rate.

B. less control over the long-term interest rate.

C. no control over the short-term interest rate.

D. full control over the short-term interest rate.

194. A difference between a monetary regime and monetary policy is that a monetary regime:

A. is a pre-determined response while a monetary policy has more flexibility.

B. has more flexibility while monetary policy is a pre-determined response.

C. depends on the economic conditions while the monetary policy does not.

D. is not favored while monetary policy is.

195. Monetary regimes:

A. do not set policy on the basis of a predetermined framework.

B. rely on the discretion of monetary policy officials.

C. use predetermined rules to set monetary policy.

D. produce greater variation in expected inflation than individual monetary policies.

196. Monetary regimes

A. involve feedback rules.

B. allow the greatest policy flexibility.

C. follow the Taylor rule.

D. are created to undermine expectations.

197. The AS/AD model implies that monetary policy should be used to:

A. make adjustments so that savings equal investment.

B. keep the money supply growing at a constant rate.

C. keep the interest rate constant.

D. keep the price level constant.

198. According to the AS/AD model, a contractionary monetary policy is appropriate:

A. when saving is less than investment.

B. when saving is greater than investment.

C. when saving equals investment.

D. whatever the level of saving and investment.

199. According to the AS/AD model, a reduction in the money supply is appropriate:

A. when saving is less than investment.

B. when saving is greater than investment.

C. when saving equals investment.

D. whatever the level of saving and investment.

200. If saving is less than investment, the appropriate countercyclical monetary policy would be:

A. a cut in the reserve requirement.

B. a cut in the discount rate.

C. an open market sale of government bonds.

D. a cut in the federal funds rate.

201. If saving exceeds investment, the appropriate countercyclical monetary policy would be:

A. an increase in the reserve requirement.

B. a cut in the discount rate.

C. an open market sale of government bonds.

D. an increase in the federal funds rate.