Page 1

1.

The short-run industry supply curve:

A)

shows the total quantity supplied by all firms in an industry for each possible price

when the number of producers is fixed.

B)

is drawn on the assumption that the number of firms in the industry doesn’t

increase, but it allows for a decrease in the number of firms due to bankrupt firms

leaving the industry.

C)

is a meaningful concept only if all firms in the industry are identical.

D)

is of limited usefulness since it is not relevant when markets are perfectly

competitive.

2.

The supply curve found by taking the horizontal summation of the short-run supply

curves of all of the firms in a perfectly competitive industry is called the _____ curve.

A)

marginal cost

B)

short-run market supply

C)

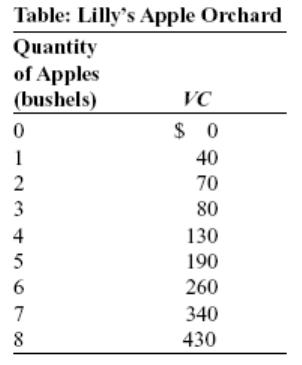

interim market supply

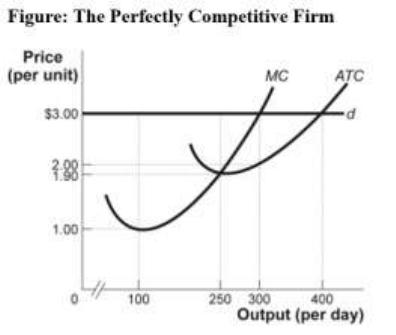

D)

competitive

3.

In perfect competition, the assumption of easy entry and exit implies that, in the _____

run, all firms in the industry will earn _____ economic profits.

A)

long; zero

B)

short; positive

C)

short; zero

D)

long; positive

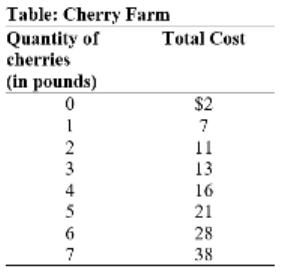

4.

If firms are making positive economic profits in the short run, then in the long run:

A)

the short-run industry supply curve will shift leftward.

B)

new firms will enter the industry.

C)

industry output will rise and the price will rise.

D)

firms will leave the industry.

5.

The market for beef is in long-run equilibrium at $3.25 per pound. The announcement

that mad cow disease has been discovered in the United States reduces the demand for

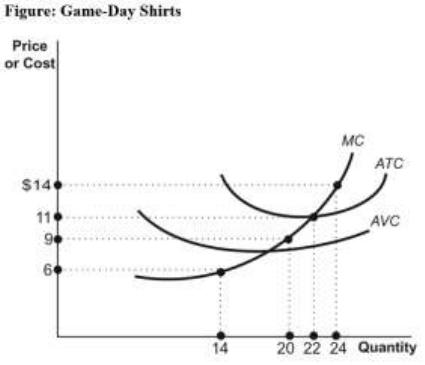

beef sharply, and the price falls to $2.00 per pound. If the long-run supply curve is

horizontal, when the long-run equilibrium is reestablished, the price will be:

A)

$3.25 per pound.

B)

$2.00 per pound.

C)

greater than $2.00 per pound but less than $3.25 per pound.

D)

More information is needed to answer this question.

Page 2

6.

Suppose economic profits exist in perfect competition in the short run. Firms will enter

in the long run because of easy entry, the short-run market _____ curve will shift to the

right, and _____ will _____.

A)

supply; output; increase

B)

demand; supply; fall

C)

supply; demand; also shift to the right

D)

demand; price; increase

7.

Short-run economic profits in a perfectly competitive industry encourage firms to _____

the industry, and short-run losses encourage firms to _____ the industry.

A)

exit; enter

B)

enter; enter

C)

enter; exit

D)

exit; exit

8.

Suppose that some firms in a perfectly competitive industry earn negative economic

profits in the short run. In the long run, the:

A)

short-run industry supply curve will not shift.

B)

short-run industry supply curve will shift to the left.

C)

number of firms in the industry will not change.

D)

number of firms in the industry will increase.

9.

If firms are taking economic losses in the short run, then in the long run, firms will leave

the industry, industry output will _____, and economic losses will _____.

A)

fall; decrease

B)

rise; decrease

C)

rise; increase

D)

fall; increase

10.

Suppose that the market for candy canes operates under conditions of perfect

competition, that it is initially in long-run equilibrium, that the price of each candy cane

is $0.10, and that the market demand curve is downward sloping. The price of sugar

rises, increasing the marginal and average total costs of producing candy canes by

$0.05. In the short run, a typical producer of candy canes will be making:

A)

an economic profit.

B)

zero economic profit.

C)

negative economic profit.

D)

The answer is impossible to determine from the information given.

Page 3

11.

Suppose that the market for candy canes operates under conditions of perfect

competition, that it is initially in long-run equilibrium, that the price of each candy cane

is $0.10, and that the market demand curve is downward sloping. The price of sugar

rises, increasing the marginal and average total cost of producing candy canes by $0.05;

there are no other changes in production costs. In the long run, we will observe:

A)

firms leaving the industry.

B)

firms entering the industry.

C)

some firms entering and some firms leaving.

D)

neither entry to nor exit from the industry.

12.

Suppose that the market for candy canes operates under conditions of perfect

competition, that it is initially in long-run equilibrium, that the price of each candy cane

is $0.10, and that the market demand curve is downward sloping. The price of sugar

rises, increasing the marginal and average total cost of producing candy canes by $0.05;

there are no other changes in production costs. Once all of the adjustments to long-run

equilibrium have been made, the price of candy canes will equal:

A)

$0.05.

B)

$0.10.

C)

$0.15.

D)

The question is impossible to answer without knowing exactly how many firms

entered and/or left the industry.

13.

Suppose that the market for haircuts in a community is perfectly competitive and that

the market is initially in long-run equilibrium. Subsequently, an increase in population

increases the demand for haircuts. In the short run, the market price will _____ and the

output of a typical firm will _____.

A)

rise; rise

B)

rise; fall

C)

fall; rise

D)

fall; fall

14.

Suppose that the market for haircuts in a community is perfectly competitive and that

the market is initially in long-run equilibrium. Subsequently, an increase in population

increases the demand for haircuts. In the short run, the typical firm is likely to:

A)

earn an economic profit.

B)

incur an economic loss.

C)

have no change in its economic profit.

D)

have neither an economic profit nor an economic loss.

Page 4

15.

Suppose that the market for haircuts in a community is a perfectly competitive

constant-cost industry and that the market is initially in long-run equilibrium.

Subsequently, an increase in population increases the demand for haircuts. In the long

run, firms will _____ the market, driving the price of haircuts _____ and the profits of

individual firms _____.

A)

enter; up; back to zero

B)

enter; down; back to zero

C)

leave; up; up

D)

leave; up; back to zero

16.

Assuming a downward-sloping demand curve, a decrease in production costs for firms

in a perfectly competitive market initially in long-run equilibrium will cause a(n):

A)

permanent increase in the price.

B)

economic profit for firms in the short run.

C)

increase in demand.

D)

increase in firms’ marginal revenue.

17.

In perfect competition, a change in fixed cost will:

A)

cause a change in the price in the short run.

B)

cause a change in output in the short run.

C)

encourage entry or exit in the long run such that price will change enough to leave

firms earning zero profits.

D)

cause a change in variable cost.

18.

In a perfectly competitive market:

A)

the price will change to reflect any change in production cost.

B)

the existence of profits leads firms to exit the industry, while losses lead firms to

enter the industry.

C)

economic profits are positive in the long run.

D)

perfect competition generates prices greater than marginal costs.

19.

A curve that shows the quantity of a good or service supplied at various prices after all

long-run adjustments to a price change have been completed is a long-run _____ curve.

A)

marginal revenue

B)

marginal cost

C)

industry supply

D)

production

Page 5

20.

Which statement is true?

A)

The long-run industry supply curve relates the price of a good or service to the

quantity produced after all adjustments to a price change have been made.

B)

Every point on a long-run industry supply curve shows a price and quantity

supplied at which firms in the industry are earning positive economic profit.

C)

For establishing the long-run industry supply curve, factor costs and the number of

firms are held constant.

D)

In perfectly competitive industries, the long-run supply curve is always horizontal.

21.

Lilly is the price-taking owner of an apple orchard. The price of apples is high enough

that Lilly is earning positive economic profits. In the long run, Lilly should expect

_____ apple prices due to the _____ firms.

A)

lower; entry of new

B)

higher; exit of existing

C)

lower; exit of existing

D)

higher; entry of new

22.

Which scenario is most likely to cause firms to exit a perfectly competitive industry?

A)

Consumer tastes and preferences for this product get stronger, making them more

interested in the good.

B)

A technological advance allows all firms to produce more efficiently.

C)

The price of a key variable input falls.

D)

Consumer income falls.

Use the following to answer question 23:

Page 6

23.

(Ref 26-1 Table: Lilly’s Apple Orchard) Use Table 26-1: Lilly’s Apple Orchard. Lilly is

the price-taking owner of an apple orchard; the orchard’s variable costs are given in the

table. Her orchard has fixed costs of $30. If the price of a bushel of apples is $85, we

would expect total industry output to _____ and Lilly’s output to _____ in the long run.

A)

rise; rise

B)

fall; fall

C)

fall; rise

D)

rise; fall

Use the following to answer questions 24-25:

24.

(Ref 26-2 Figure: The Perfectly Competitive Firm) Use Figure 26-2: The Perfectly

Competitive Firm. The firm faces demand curve d and maximizes profit. In a long-run

equilibrium, this firm will produce _____ units of output and sell its output for _____.

A)

100; $1.00

B)

250; $1.90

C)

300; $2.00

D)

400; $3.00

25.

(Ref 26-2 Figure: The Perfectly Competitive Firm) Use Figure 26-2: The Perfectly

Competitive Firm. The figure shows a perfectly competitive firm that faces demand

curve d and maximizes profit. The firm’s economic profit in the long run will be:

A)

$0.

B)

$250.

C)

$275.

D)

$300.

Page 7

26.

If some firms in a perfectly competitive industry are earning positive economic profits,

then in the long run, the:

A)

industry is in equilibrium.

B)

short-run industry supply curve will shift to the right.

C)

number of firms in the industry will not change.

D)

number of firms in the industry will decrease.

27.

Suppose that some firms in a perfectly competitive industry are earning positive

economic profits. In the long run, the:

A)

industry is in equilibrium.

B)

industry supply curve will shift to the left.

C)

number of firms in the industry will not change.

D)

number of firms in the industry will increase.

28.

Suppose that the market for haircuts in a community is perfectly competitive and that

the market is initially in long-run equilibrium. Subsequently, a decrease in population

decreases the demand for haircuts. In the short run, we expect that the market price will

_____ and the output of a typical firm will _____.

A)

rise; rise

B)

rise; fall

C)

fall; rise

D)

fall; fall

29.

In perfectly competitive long-run equilibrium:

A)

all firms make positive economic profits.

B)

all firms produce at the minimum point of their average total cost curves.

C)

the industry supply curve must be upward-sloping.

D)

all firms face the same price, but the value of marginal cost will vary directly with

firm size.

30.

When economic profits in an industry are zero:

A)

firms are really doing badly.

B)

firms are doing as well as they could do in other markets.

C)

firms should exit so they can make an economic profit in some other market.

D)

the industry is not in long-run equilibrium.

Page 8

31.

When a perfectly competitive firm is in long-run equilibrium, the firm is producing at

_____ cost.

A)

maximum average total

B)

maximum average variable

C)

minimum marginal

D)

minimum average total

32.

Provided that there are no external benefits or costs, resources are efficiently allocated

for a perfectly competitive firm when:

A)

P = MR.

B)

P = AVC.

C)

P = MC.

D)

MC = AVC.

33.

In a long-run equilibrium, economic profits in a perfectly competitive industry are:

A)

positive.

B)

zero.

C)

negative.

D)

indeterminate.

34.

When a perfectly competitive industry is in long-run equilibrium, its firms:

A)

earn more than zero economic profits.

B)

combine their variable and fixed resources inefficiently.

C)

are not in short-run equilibrium.

D)

allocate all of their resources efficiently.

35.

A perfectly competitive industry is in a state of long-run equilibrium. Which expression

must be true?

A)

P = MR = MC > ATC.

B)

P = MR = MC < AVC.

C)

P = MR = MC = ATC.

D)

P > MR = MC = AVC.

36.

A perfectly competitive industry is said to be efficient because the:

A)

marginal cost of production of the last unit of output is minimized in the long run.

B)

product is standardized across firms in the industry.

C)

average total cost of production of the industry’s output is minimized in the long

run.

D)

market price of the good is equal to economic profit for all firms in the industry.

Page 9

Use the following to answer questions 37-49:

37.

(Ref 26-3Table: Cherry Farm) Use Table 26-3: Cherry Farm. If Hank and Helen have

one of 100 farms in the perfectly competitive cherry industry and if the price is $5, in

the short run the industry will supply _____ pounds.

A)

100

B)

200

C)

400

D)

500

38.

(Ref 26-3Table: Cherry Farm) Use Table 26-3: Cherry Farm. If Hank and Helen have

one of 100 farms in the perfectly competitive cherry industry and if the price is $4, in

the short run the industry will supply _____ pounds.

A)

200

B)

400

C)

600

D)

700

39.

(Ref 26-3Table: Cherry Farm) Use Table 26-3: Cherry Farm. If Hank and Helen have

one of 100 farms in the perfectly competitive cherry industry and if the price is $3, in

the short run the industry will supply _____ pounds.

A)

0

B)

200

C)

300

D)

400

Page 10

40.

(Ref 26-3Table: Cherry Farm) Use Table 26-3: Cherry Farm. Suppose there are 100

farms in this industry with identical cost curves, as shown in the table. Which point

would fall on the industry short-run supply curve?

A)

$2, 300 pounds

B)

$11, 200 pounds

C)

$3, 500 pounds

D)

$8, 600 pounds

41.

(Ref 26-3Table: Cherry Farm) Use Table 26-3: Cherry Farm. Suppose there are 100

farms in this industry with identical cost curves, as shown in the table. Which point

would fall on the industry short-run supply curve?

A)

$5, 100 pounds

B)

$4, 200 pounds

C)

$4, 400 pounds

D)

$2, 500 pounds

42.

(Ref 26-3Table: Cherry Farm) Use Table 26-3: Cherry Farm. Suppose there are 100

farms in this industry with identical cost curves, as shown in the table. At what price

will the industry be in long-run equilibrium?

A)

$2

B)

$3

C)

$4

D)

$5

43.

(Ref 26-3Table: Cherry Farm) Use Table 26-3: Cherry Farm. Suppose there are 100

farms in this industry with identical cost curves, as shown in the table. If all farms are

the same size, how much will each farm produce in long-run equilibrium?

A)

0 pounds

B)

4 pounds

C)

5 pounds

D)

7 pounds

44.

(Ref 26-3Table: Cherry Farm) Use Table 26-3: Cherry Farm. Suppose all farms have

identical cost curves, as shown in the table. How much will the industry produce in

long-run equilibrium if there are 100 farms in the industry in the long run?

A)

600 pounds

B)

500 pounds

C)

400 pounds

D)

0 pounds

Page 11

45.

(Ref 26-3Table: Cherry Farm) Use Table 26-3: Cherry Farm. Suppose there are 100

farms in this industry with identical cost curves, as shown in the table. If all farms are

the same size, how much economic profit will each farm earn when the industry is in

long-run equilibrium?

A)

$0

B)

$100

C)

-$200

D)

$1,000

46.

(Ref 26-3Table: Cherry Farm) Use Table 26-3: Cherry Farm. Suppose there are 100

farms in this industry with identical cost curves, as shown in the table. If the price is $6

per pound:

A)

firms will enter the industry.

B)

firms will exit the industry.

C)

the industry is in long-run equilibrium.

D)

the industry has minimized average total cost.

47.

(Ref 26-3Table: Cherry Farm) Use Table 26-3: Cherry Farm. Suppose there are 100

farms in this industry with identical cost curves, as shown in the table. If the price is

$3.60 per pound:

A)

firms will enter the industry.

B)

firms will exit the industry.

C)

the industry is in long-run equilibrium.

D)

no firms will produce in the industry in the short run.

48.

(Ref 26-3Table: Cherry Farm) Use Table 26-3: Cherry Farm. Suppose there are 100

farms in this industry with identical cost curves, as shown in the table. If the price is $4

per pound:

A)

firms will enter the industry.

B)

firms will exit the industry.

C)

the industry is in long-run equilibrium.

D)

the industry has maximized average total cost.

49.

(Ref 26-3Table: Cherry Farm) Use Table 26-3: Cherry Farm. Suppose there are 100

farms in this industry with identical cost curves, as shown in the table. If the price is $10

per pound:

A)

firms will enter the industry.

B)

firms will exit the industry.

C)

the industry is in long-run equilibrium.

D)

the industry has minimized average total cost.

Page 12

Use the following to answer questions 50-59:

50.

(Ref 26-4 Figure: Game-Day Shirts) Use Figure 26-4: Game-Day Shirts. Rick is one of

10 vendors who sell game-day T-shirts at football games in a perfectly competitive

market. His costs are identical to the costs of the other 9 vendors. If the price of a shirt is

$14, the short-run industry supply will be _____ shirts.

A)

140

B)

200

C)

220

D)

240

51.

(Ref 26-4 Figure: Game-Day Shirts) Use Figure 26-4: Game-Day Shirts. Rick is one of

10 vendors who sell game-day T-shirts at football games in a perfectly competitive

market. His costs are identical to the costs of the other 9 vendors. If the price of a shirt is

$11, the short-run industry supply will be _____ shirts.

A)

140

B)

200

C)

220

D)

240

52.

(Ref 26-4 Figure: Game-Day Shirts) Use Figure 26-4: Game-Day Shirts. Rick is one of

10 vendors who sell game-day T-shirts at football games in a perfectly competitive

market. His costs are identical to the costs of the other 9 vendors. If the price of a shirt is

$9, the short-run industry supply will be _____ shirts.

A)

140

B)

200

C)

220

D)

240

Page 13

53.

(Ref 26-4 Figure: Game-Day Shirts) Use Figure 26-4: Game-Day Shirts. Rick is one of

10 vendors who sell game-day T-shirts at football games in a perfectly competitive

market. His costs are identical to the costs of the other 9 vendors. If the price of a shirt is

$6, the short-run industry supply will be _____ shirts.

A)

0

B)

140

C)

220

D)

240

54.

(Ref 26-4 Figure: Game-Day Shirts) Use Figure 26-4: Game-Day Shirts. Rick is one of

10 vendors who sell game-day T-shirts at football games in a perfectly competitive

market. His costs are identical to the costs of the other 9 vendors. If the industry is in

long-run equilibrium, how many shirts will each vendor sell?

A)

14

B)

20

C)

22

D)

24

55.

(Ref 26-4 Figure: Game-Day Shirts) Use Figure 26-4: Game-Day Shirts. Rick is one of

10 vendors who sell game-day T-shirts at football games in a perfectly competitive

market. His costs are identical to the costs of the other 9 vendors. If the industry is in

long-run equilibrium, the price of each shirt will be:

A)

$6.

B)

$9.

C)

$11.

D)

$14.

56.

(Ref 26-4 Figure: Game-Day Shirts) Use Figure 26-4: Game-Day Shirts. Rick is one of

10 vendors who sell game-day T-shirts at football games in a perfectly competitive

market. His costs are identical to the costs of the other 9 vendors. When the industry is

in long-run equilibrium, the price of each shirt will be _____, and the total quantity

supplied in the market will be _____.

A)

$6; 0

B)

$9; 200

C)

$11; 220

D)

$14; 240

Page 14

57.

(Ref 26-4 Figure: Game-Day Shirts) Use Figure 26-4: Game-Day Shirts. Rick is one of

10 vendors who sell game-day T-shirts at football games in a perfectly competitive

market. His costs are identical to the costs of the other 9 vendors. If the price of a shirt is

$14, in the long run:

A)

new firms will enter the industry.

B)

existing firms will exit the industry.

C)

the industry is in equilibrium.

D)

the industry has minimized average total cost.

58.

(Ref 26-4 Figure: Game-Day Shirts) Use Figure 26-4: Game-Day Shirts. Rick is one of

10 vendors who sell game-day T-shirts at football games in a perfectly competitive

market. His costs are identical to the costs of the other 9 vendors. If the price of a shirt is

$9, in the long run:

A)

new firms will enter the industry.

B)

existing firms will exit the industry.

C)

the industry is in equilibrium.

D)

the industry has minimized average total cost.

59.

(Ref 26-4 Figure: Game-Day Shirts) Use Figure 26-4: Game-Day Shirts. Rick is one of

10 vendors who sell game-day T-shirts at football games in a perfectly competitive

market. His costs are identical to the costs of the other 9 vendors. If the price of a shirt is

$11, in the long run:

A)

firms will enter the industry.

B)

firms will exit the industry.

C)

the industry is in equilibrium.

D)

the industry has maximized average total cost.

60.

The short-run industry supply curve is the sum of the marginal cost curves above

average variable cost for all of the firms in the industry, assuming that the number of

firms is constant.

A)

True

B)

False

61.

The short-run industry supply curve is the sum of the individual supply curves of all of

the firms in the industry, given a fixed number of firms.

A)

True

B)

False

Page 15

62.

In the long run, firms will leave an industry if the market price is consistently less than

their break-even price.

A)

True

B)

False

63.

The long-run industry supply curve is usually more elastic than the short-run industry

supply curve, but if entering firms make intensive use of an input that is in limited

supply, then it is possible for the long-run curve to be less elastic than the short-run

curve.

A)

True

B)

False

64.

Suppose the beef industry is perfectly competitive and the demand for beef rises. As

long as the demand does not subsequently fall, beef producers can expect to earn

economic profits in both the short run and the long run.

A)

True

B)

False

65.

A market that is in long-run equilibrium must also be in short-run equilibrium.

A)

True

B)

False

66.

The short-run industry supply curve is more elastic than is the long-run industry supply

curve.

A)

True

B)

False

67.

Lawn mowing is a perfectly competitive industry. Alex’s Lawn-Mowing Service should

close if Alex expects his long-run economic profits to equal zero.

A)

True

B)

False

68.

In the long run, when there are economic profits, firms enter the industry, which will

increase the market supply and increase the price until economic profits are zero.

A)

True

B)

False

Page 16

69.

In the long run, when there are economic losses, firms leave the industry, which will

decrease the market supply and increase the price until economic losses are zero.

A)

True

B)

False

70.

In the long run, when economic profit is zero, firms leave the industry, which will

increase the market supply and increase the price until economic profits are positive.

A)

True

B)

False

71.

In long-run equilibrium in a perfectly competitive market, all firms will be operating at

their lowest possible average total cost.

A)

True

B)

False

72.

In long-run equilibrium in a perfectly competitive market, all firms will be operating at

the same level of marginal cost.

A)

True

B)

False

73.

A perfectly competitive industry is in long-run equilibrium. Now suppose that the fixed

costs of firms in the industry decrease. Describe how this change will affect short-run

economic profits. How will this industry adjust in the long run?

74.

A perfectly competitive tomato industry is in long-run equilibrium. Now suppose that

some consumers are getting sick by eating tomatoes that contain salmonella. Describe

how this change will affect short-run economic profits. What will happen to the number

of tomato growers in the long run? How will price and output in this industry adjust in

the long run?

75.

Consider a perfectly competitive corn industry that has positive economic profit.

Describe how the long-run industry supply curve might slope upward, rather than be

horizontal.

76.

Explain how the long-run perfectly competitive equilibrium is efficient.

Page 17

Use the following to answer questions 77-78:

77.

(Ref 26-5 Table: Cherry Farm) Use Table 26-5: Cherry Farm. If Hank and Helen have

one of 100 identical farms in the perfectly competitive cherry industry, explain how

Hank and Helen and the industry will react in the short run and the long run to a price of

$8 per pound for cherries.

78.

(Ref 26-5 Table: Cherry Farm) Use Table 26-5: Cherry Farm. If Hank and Helen have

one of 100 identical farms in the perfectly competitive cherry industry, explain how

Hank and Helen and the industry will react in the short run and the long run to a price of

$3.75 per pound for cherries.

Use the following to answer question 79:

Page 18

79.

(Ref 26-6 Table: Lilly’s Apple Orchard) Use Table 26-6: Lilly’s Apple Orchard. Lilly is

the price-taking owner of an apple orchard. Her orchard has fixed costs of $30. If the

price of a bushel of apples is $80, how many bushels will Lilly produce? Is this a

long-run equilibrium? If not, what will be the price of a bushel of apples in the long run?

Show your work.

80.

The horizontal sum of individual firms’ MC curves (specifically the portions above

AVC) is the:

A)

short-run industry demand curve.

B)

short-run industry supply curve.

C)

long-run fixed cost curve.

D)

long-run average variable cost curve.

81.

In the long run, each firm in a perfectly competitive industry will:

A)

earn only enough to cover the opportunity costs of all resources used in production.

B)

produce where MR is greater than MC.

C)

differentiate its goods.

D)

increase its price.

82.

If the long-run market supply curve for a perfectly competitive market is horizontal,

then this industry exhibits _____ costs.

A)

constant

B)

decreasing

C)

increasing

D)

an absence of marginal

83.

In a perfectly competitive market, tastes and preferences lead to an increase in the

demand for the good. Holding everything else constant, this will lead to an increase in

price that will result in _____ in the short run, which will in turn _____, which will

_____.

A)

positive economic profits; attract new firms; reduce the price

B)

economic losses; attract new firms; reduce the price

C)

positive economic profits; lead some firms to leave the industry; further increase

the price

D)

economic losses; lead some firms to leave the industry; further increase the price

Page 19

84.

A perfectly competitive industry with constant costs initially operates in long-run

equilibrium. When demand increases:

A)

in the short run, prices and profits will be higher, but in the long run, price will fall

back to its original level and firms will again earn zero economic profit.

B)

prices and profits will be higher than before the demand increase in both the long

run and the short run.

C)

in the short run, prices and profits will fall, but in the long run, price will rise back

to its initial level, as will profits.

D)

prices and profits will be lower than before the demand increase in both the long

run and the short run.

85.

A perfectly competitive industry with constant costs initially operates in long-run

equilibrium. When demand increases, in the long run and the short run:

A)

positive economic profits will result for all firms.

B)

higher prices will result.

C)

output will increase.

D)

negative economic profits will result for some firms.

86.

In the long run, all of the firms in a perfectly competitive industry will:

A)

produce at an output level at which average total cost equals marginal cost.

B)

earn an economic profit greater than zero.

C)

exit the industry if price is greater than average total cost.

D)

produce an output level at which price is greater than average total cost.

Page 21