Chapter 25 Monopolistic Competition 629

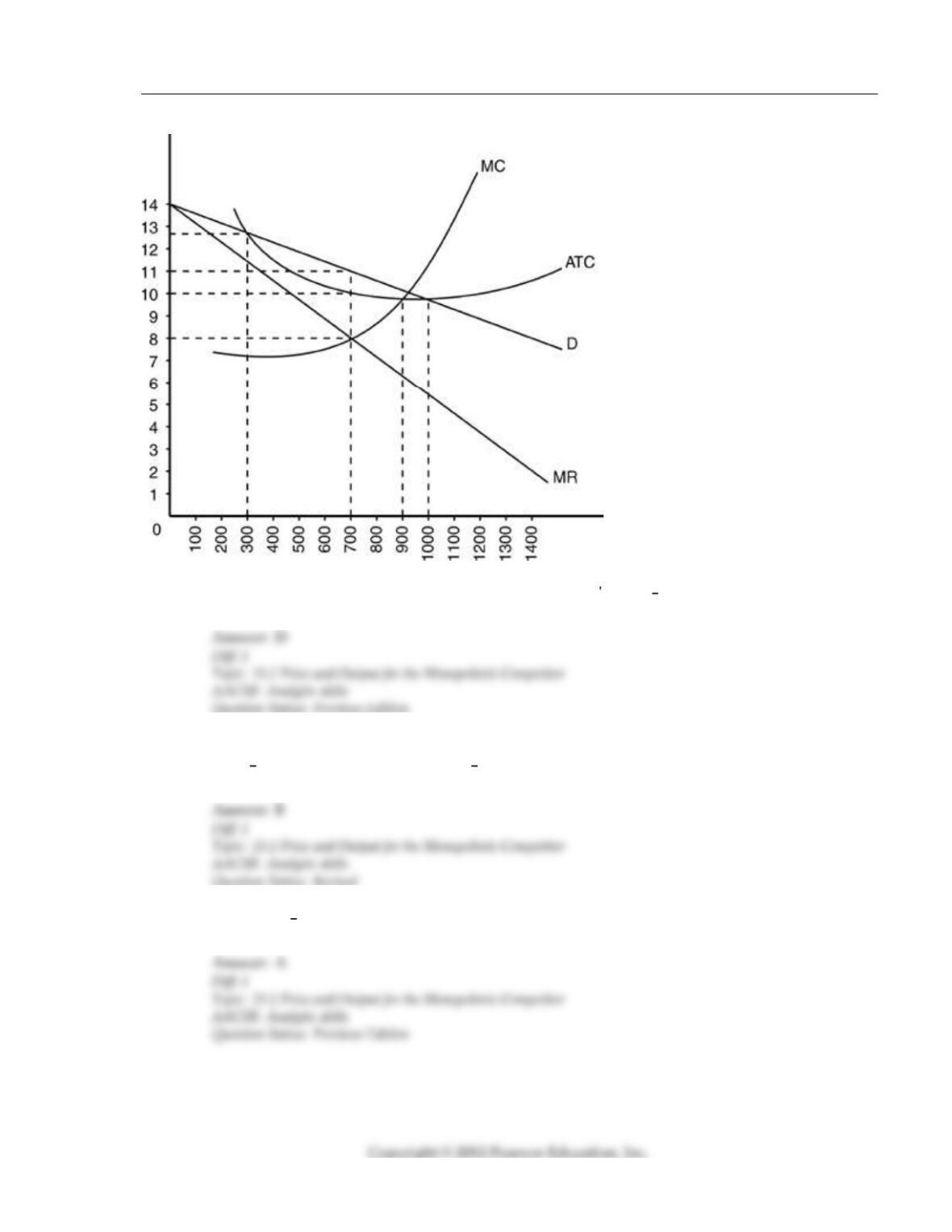

14) In the above figure, the monopolistically competitive firm s profit maximizing output is

A) 1,000 units. B) 300 units. C) 900 units. D) 700 units.

15) In the above figure, when this monopolistically competitive firm produces its

profit maximizing output, it sets a per unit price of

A) $13. B) $11. C) $10. D) $8.

16) At its profit maximizing output, the firm in the above figure incurs a total cost of production of

A) $7,000. B) $9,000. C) $6,300. D) $3,900.

17) In the above figure, this profit maximizing monopolistic competitive firm will realize an

economic profit of

A) $1,400. B) $2,100. C) $1,400. D) $700.

18) Since the firm in the above figure is operating in a monopolistically competitive industry, in the

long run we can expect to see

A) the typical firm s economic profits expand as production becomes more efficient.

B) more firms entering the industry until economic profits are zero.

C) the typical firm producing at the minimum point on its ATC curve.

D) each firm expand its share of the total market.

19) The demand curve for a monopolistically competitive firm is

A) the same as the industry demand curve.

B) more elastic than the demand curve of the perfectly competitive firm.

C) less elastic than the demand curve of the perfectly competitive firm.

D) horizontal.

20) For the monopolistically competitive firm, in both the short run and the long run

A) the demand curve is inelastic.

B) price will exceed marginal cost.

C) there will be no economic profit.

D) production will be at minimum average cost.

21) The demand curve faced by a monopolistically competitive firms is

A) horizontal. B) vertical.

C) downward sloping. D) unitary elastic.

22) The monopolistic competitive firm in short run equilibrium may experience economic profits

that are

A) always zero. B) greater than, equal to, or less than zero.

C) always positive. D) always negative.

23) In both a monopolistically competitive market and a pure monopoly market, firms

A) can make long run profits. B) set price greater than marginal cost.

C) are protected by entry barriers. D) advertise extensively.

24) The monopolistically competitive firm maximizes profit by producing to the point at which

A) ATC AVC. B) MC MR. C) MR AR. D) MC AR.

25) In the short run, a firm operating as a monopolistic competitor will produce to the point at

which

A) MR ATC. B) MC ATC. C) P MC. D) MR MC.

26) Which will be true for a monopolistic competitor experiencing short run losses?

A) P ATC B) P ATC C) P ATC D) P MC

27) A monopolistically competitive firm finds its profit maximizing rate of output by equating

A) the marginal revenue of advertising with the marginal cost of advertising.

B) average revenue and average total cost.

C) price and marginal cost.

D) marginal revenue and marginal cost.

28) In the short run, a monopolistically competitive firm

A) always earns positive economic profits.

B) never earns positive economic profits.

C) can earn positive, negative, or zero economic profits.

D) always earns positive accounting profits.

29) In the long run, in a monopolistically competitive market, price will be

A) equal to MR. B) equal to MC. C) greater ATC. D) equal to ATC.

30) In the long run in a monopolistically competitive market, a firm will, in theory,

A) earn economic profits. B) suffer losses.

C)

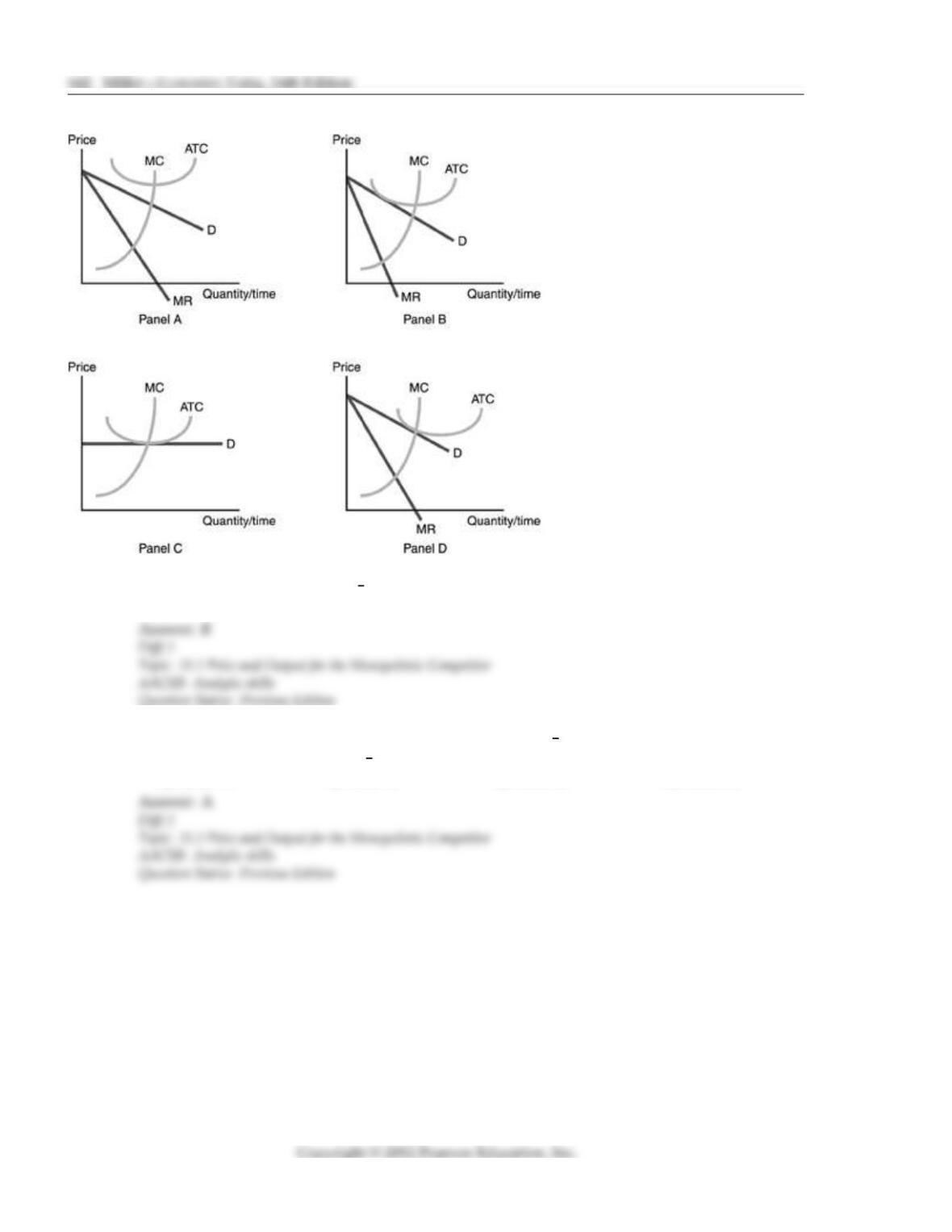

b

reak even. D) earn zero accounting profits.

31) In the long run, the monopolistically competitive firm s demand curve will

A) intersect the ATC at its minimum point.

B) intersect the ATC curve somewhere past the minimum point.

C)

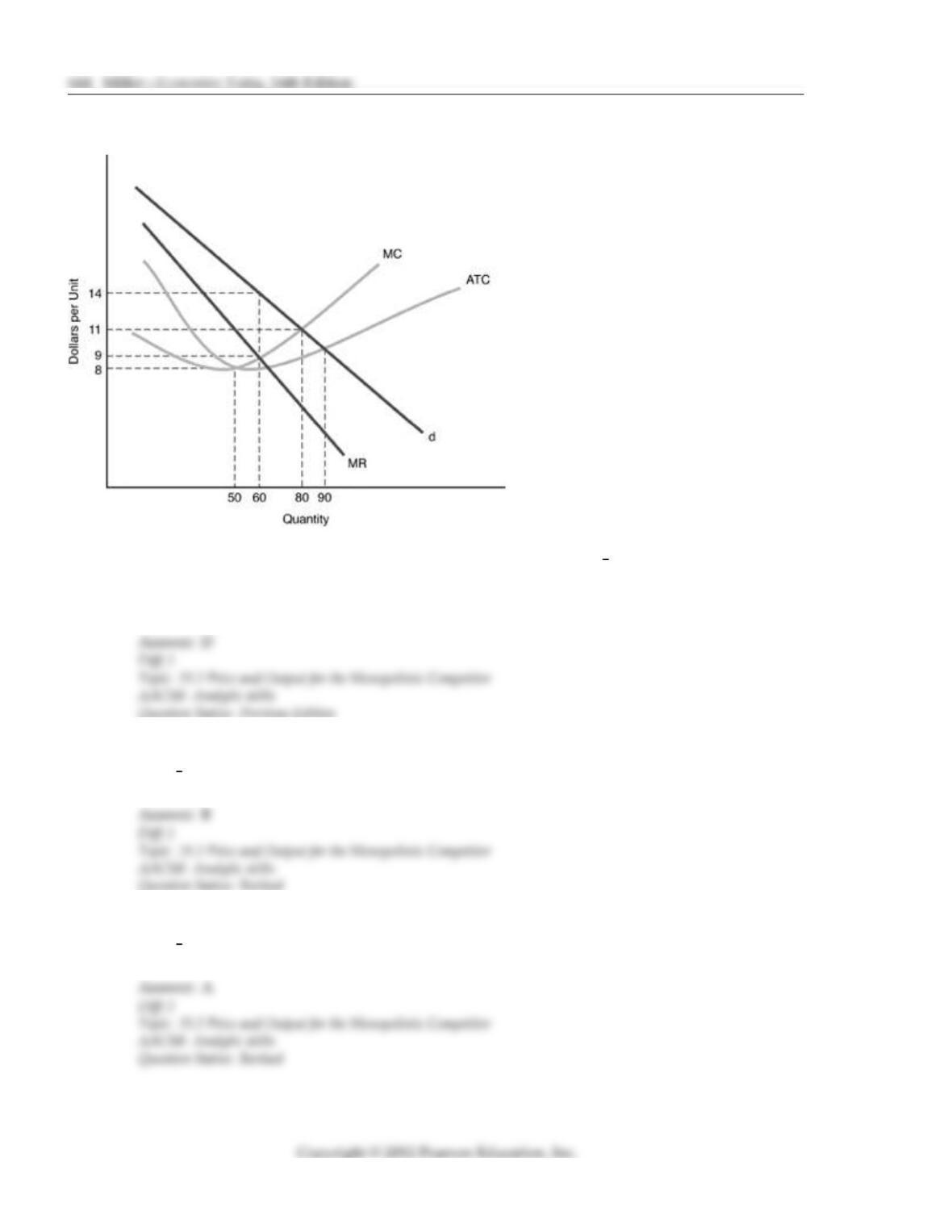

b

ecome tangent to the ATC curve at its minimum point.

D)

b

ecome tangent to the ATC curve somewhere to the left of its minimum point.

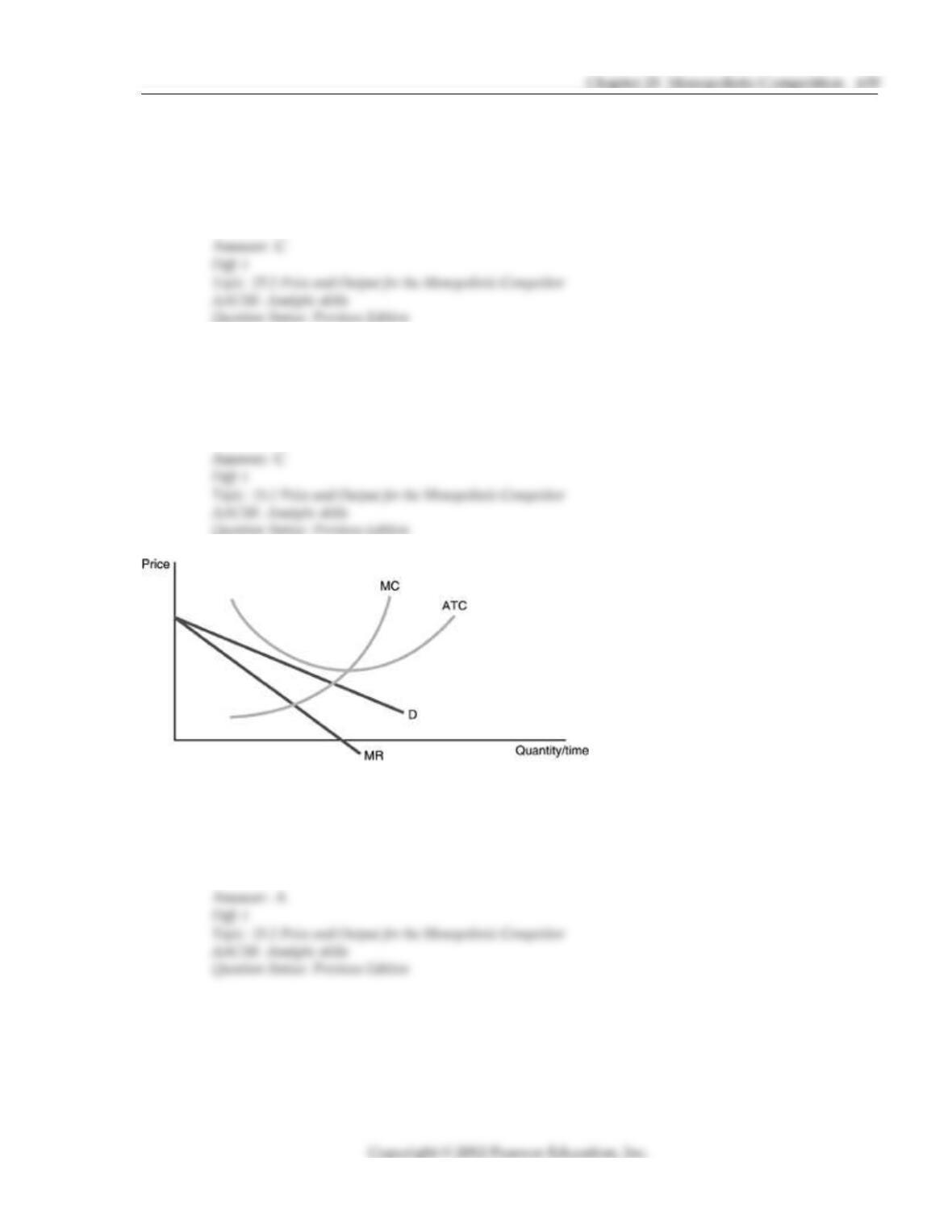

32) The monopolistically competitive firm s economic profits tend toward zero in the long run. Why

is this so?

A) Monopolistically competitive firm s are rarely able to maintain the corporate discipline

necessary to sustain profits in the long run.

B) If a monopolistically competitive firm is profitable for more than 2 years, the Justice

Department orders a corporate restructuring to pull the company back to a normal rate of

return.

C) In the long run, other firms will successfully offer substitutes for the profitable firm s

product, and competition will eliminate economic profits.

D) Even though the monopolistically competitive firm can successfully maintain barriers to

entry, keeping competition at bay becomes very expensive.

33) The long run equilibrium of monopolistic competition is characterized by

A) P MC ATC. B) P MC ATC.

C) P MR MC. D) P ATC MC.

34) In the long run, monopolistically competitive firms will not earn economic profits because

A) average total cost will shift up to meet the demand curve.

B) input prices will be bid up.

C) production will not be at minimum average cost.

D) new firms will enter the industry.

35) In the long run, if some monopolistically competitive firms are earning economic losses then

A) firms will leave the industry.

B) raise prices until they earn economic profits.

C) they will increase production until marginal costs fall.

D) new firms will enter the industry.

36) If firms in a monopolistically competitive industry are operating with economic losses, over

time we would see

A) firms alter their advertising rates until they made at least normal profits.

B) some firms exiting the industry, causing the market supply curve to shift to the left, raising

price.

C) some firms exiting the industry, causing the demand curves of the remaining firms to shift

to the right.

D) the firms working together to increase price and everyone s profitability.

37) If firms in a monopolistically competitive industry are operating with positive economic profit,

over time we would see

A) firms alter their advertising rates until they made at least normal profits.

B) some firms entering the industry, causing the market supply curve to shift to the right,

lowering price.

C) some firms entering the industry, causing the demand curves of the existing firms to shift

to the left.

D) some firms entering the industry, causing the demand curves of the existing firms to shift

to the right.

38) In the long run, firms in a monopolistically competitive market

A) usually earn positive economic profits. B) always earn monopoly profits.

C) usually earn economic losses. D) earn zero economic profits.

39) The long run equilibrium of a monopolistically competitive firm is characterized by

A) a tangency of the average total cost curve with the firm s demand curve.

B) price equal to marginal cost.

C) production at the minimum point of the firm s average total cost curve.

D) production at the minimum point of the firm s average variable cost curve.

40) Long run equilibrium is characterized by zero profits in

A) monopolistic competition only.

B) perfect competition only.

C)

b

oth perfect competition and monopolistic competition.

D) market structures in which there are barriers to entry.

41) A monopolistically competitive firm maximizes profits when it

A) produces the quantity at which marginal cost equals the market price.

B) produces the quantity at which marginal cost equals marginal revenue and uses the

demand curve to determine the market price.

C) produces the quantity at which marginal cost equals marginal revenue and sets the price

equal to the marginal cost.

D) produces the quantity at which marginal cost equals marginal revenue and sets the price

equal to the marginal revenue.

42) Which of the following statements about a monopolistically competitive firm is TRUE?

A) A monopolistically competitive firm does not always equate marginal cost to marginal

revenue because it uses other means to maximize profits.

B) A monopolistically competitive firm maximizes profits by charging a price equal to

marginal cost.

C) A monopolistically competitive firm produces the quantity at the point at which the

demand curve crosses the marginal cost curve.

D) A monopolistically competitive firm maximizes profits when it produces the quantity at

which marginal cost equals marginal revenue.

43) A monopolistic competitor finds its profit maximizing rate of output by

A) equating the marginal revenue from advertising with the marginal revenue from selling

the good.

B) setting average revenue equal to average total cost.

C) equating marginal revenue and marginal cost.

D) equating price and marginal revenue.

44) In the short run, the monopolistic competitor is just like the perfect competitor in that

A) equilibrium is determined by setting price equal to marginal cost.

B) either type of firm can earn economic profits, experience economic losses, or break even in

the short run.

C) each equates marginal revenue and marginal cost in order to maximize profits, with the

result that price exceeds marginal revenue.

D) new firms enter in the short run when firms are making profits.

45) If firms in a monopolistically competitive industry experience short run losses,

A) some firms would like to exit the industry but find they cannot.

B) firms increase prices further, until they make at least a normal return.

C) firms increase advertising spending to increase demand, until they make at least a normal

return.

D) some firms exit the industry, causing the demand curves for the remaining firms to shift to

the right until they earn a normal profit.

46) If monopolistically competitive firms earn short run economic profits, we expect to see

A) new firms enter the industry, which shifts the demand curves of the existing firms to the

left until firms earn zero economic profits.

B) new firms trying to enter the industry, but unable to do so because of barriers to entry.

C) existing firms altering their scale of plant to try to capture larger profits. The combined

effect is to cause all firms to earn zero economic profits.

D) existing firms increasing prices to try to capture larger economic profits.

47) A monopolistic competitor is like a competitive firm in the long run, because

A) it earns positive economic profits.

B) it earns zero economic profits

C)

b

oth firms will earn positive economic profits.

D)

b

oth firms will increase price to increase profits.

48) A monopolistic competitor is like a monopolist in the long run in that when economic profits are

A) equal to zero, positive economic profits are made.

B) equal to zero, economic profits are made.

C) greater than zero, changes in output are due to changes to plants by existing firms and

there is no entry.

D) greater than zero, price exceeds marginal cost.

49) A monopolistic competitor is in long run equilibrium when

A) economic profits are equal to zero and the average total cost curve is tangent to the

demand curve.

B) economic profits are equal to zero and the marginal cost curve is tangent to the demand

curve.

C) economic profits are greater than zero and the average total cost curve is tangent to the

demand curve.

D) economic profits are greater than zero and the marginal cost curve is tangent to the

demand curve.

50) Which of the following statements is true about the economic profits earned by a monopolistic

competitor firm in the long run?

A) Economic profits can be positive since firms have some degree of monopoly power.

B) Economic profits will be positive since the firm has a downward sloping demand curve.

C) Economic profits will tend towards zero since positive profits will attract new firms into

the industry.

D) Economic profits can be negative since there is so much competition in the market.

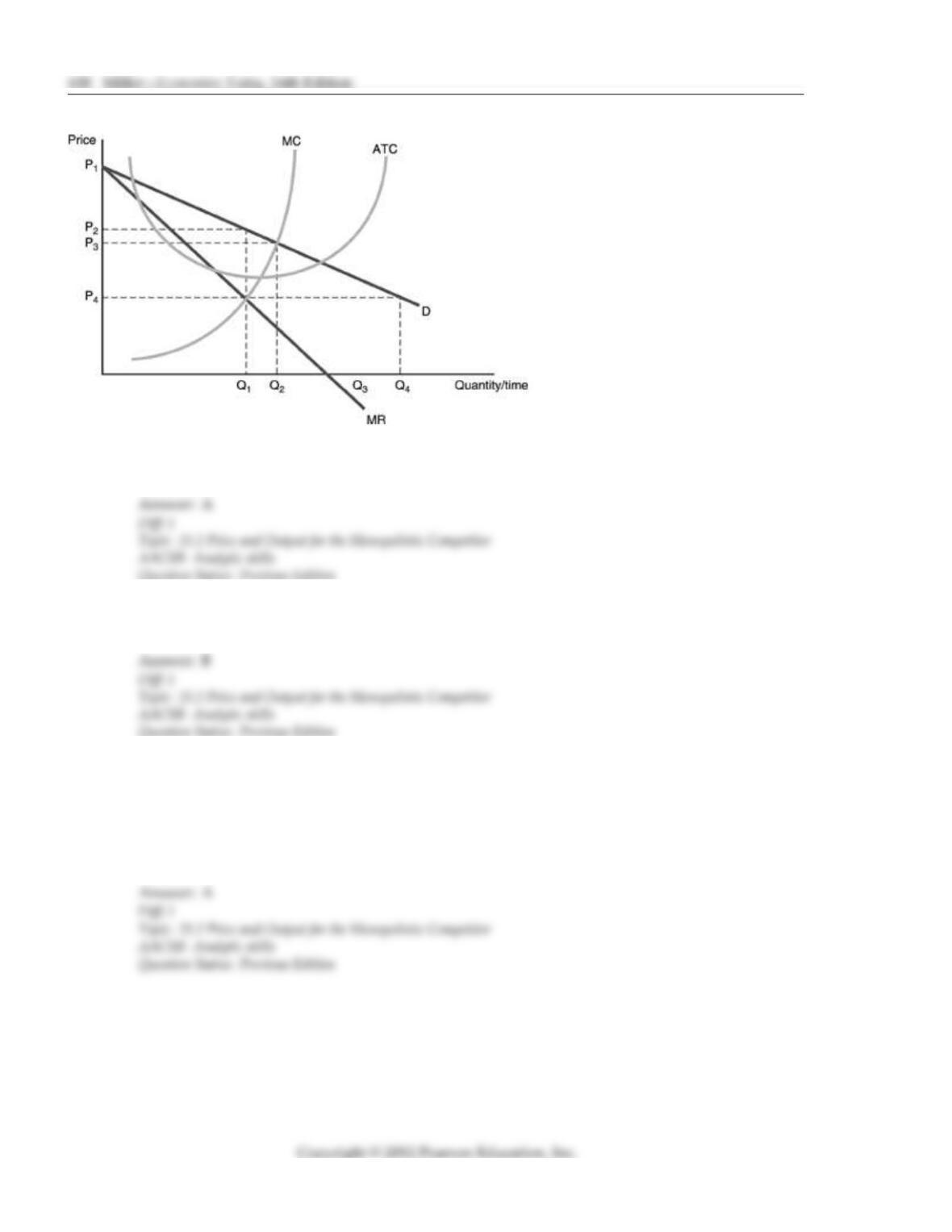

51) Refer to the above figure. The profit maximizing quantity for a monopolistic competitor is

A) Q1. B) Q2. C) Q3. D) Q4.

52) Refer to the above figure. The profit maximizing price for a monopolistic competitor is

A) P1. B) P2. C) P3. D) P4.

53) Refer to the above figure. As more and more firms are able to and actually do enter the

industry, the demand curve of each firm and its marginal revenue curve

A) will shift inward until the demand curve is tangent to the average total cost curve.

B) will become vertical.

C) will become upward sloping.

D) None of the above will occur.

54) Refer to the above figure. This firm is operating in the

A) long run since economic profits are greater than zero.

B) long run since economic profits are less than zero.

C) short run since economic profits are greater than zero.

D) short run since economic profits are less than zero.

55) Refer to the above figure. Economic profits for this firm are

A) negative.

B) zero.

C) positive.

D) undetermined without more information.

56) Refer to the above figure. Economic profits for this firm are

A) negative.

B) zero.

C) positive.

D) undetermined without more information.

57) Refer to the above figure. Economic profits for this firm are

A) negative and equal to P2

b

cP3. B) negative and equal to P1

b

cP2.

C) positive and equal to P2

b

cP3. D) positive and equal to P1abP2.

58) A monopolistic competitor is in long run equilibrium when

A) it is making zero profits and price equals marginal cost.

B) its average total cost curve is tangent to the demand curve at the profit maximizing rate of

output.

C) price is greater than marginal cost.

D) it is making positive profits or zero profits and price is greater than marginal cost.

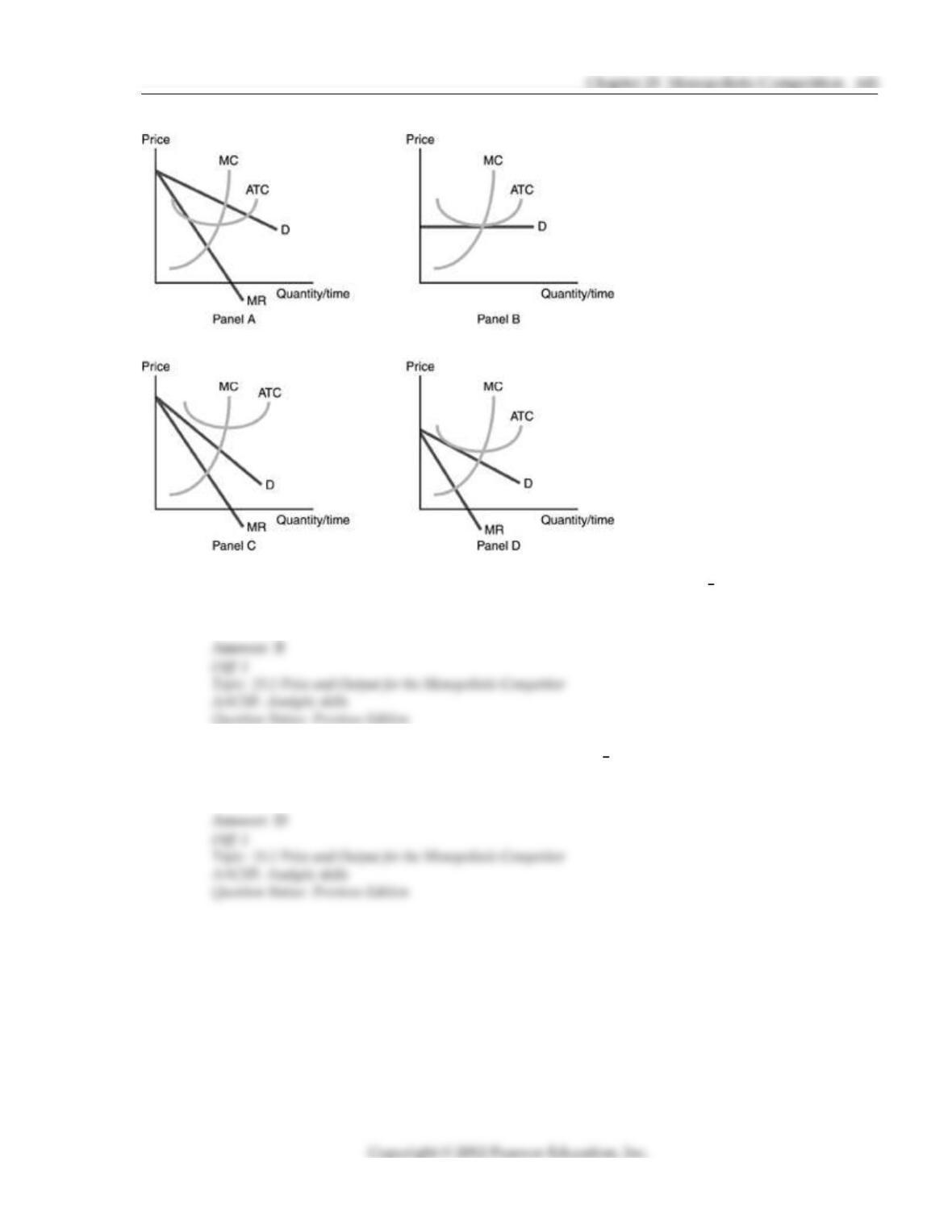

59) Refer to the above figure. Which panel does not represent a possible short run situation for a

monopolistically competitive firm?

A) Panel A. B) Panel B. C) Panel C. D) Panel D.

60) Refer to the above figure. Which panel represents the long run situation for a monopolistically

competitive firm?

A) Panel A. B) Panel B. C) Panel C. D) Panel D.

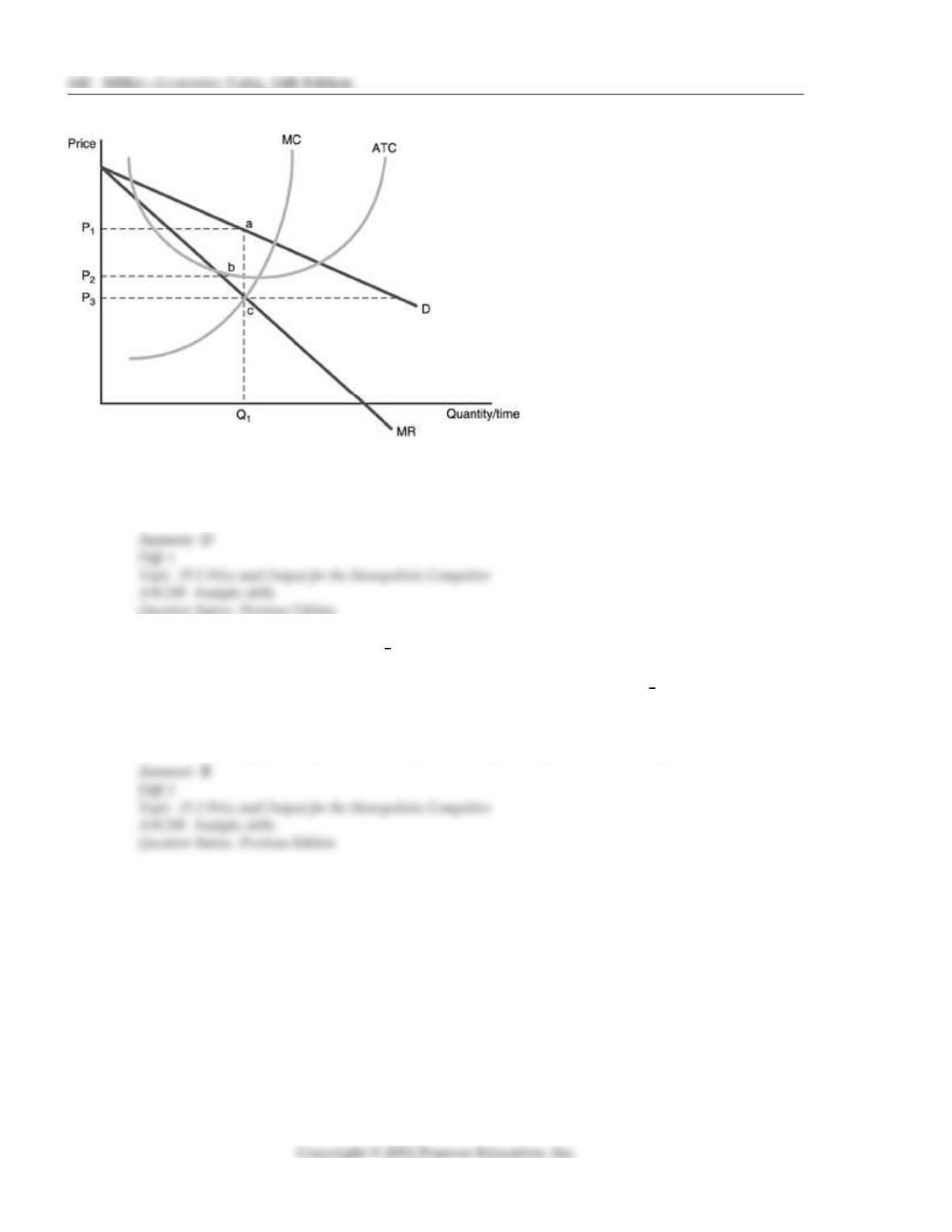

61) Refer to the above figure. A long run equilibrium in monopolistic competition is pictured by

A) Panel A. B) Panel B. C) Panel C. D) Panel D.

62) Refer to the above figure. Which panel shows a possible short run equilibrium for monopolistic

competition, but is not also a long run equilibrium?

A) Panel A. B) Panel B. C) Panel C. D) Panel D.

63) Refer to the above figure. Which of the following statements about panel D in the figure is

TRUE?

A) The figure represents a long run equilibrium for a monopolistic competitor.

B) The figure represents an industry long run equilibrium for monopolistic competition.

C) The figure is in error since it doesn t show the monopolistic competitor making profits in

the long run.

D) The figure is in error since it has marginal cost intersecting the ATC curve at a point other

than the minimum of ATC.

64) Refer to the above figure. Which panel represents a monopolistic competitor that is earning zero

economic profits?

A) Panel A. B) Panel B. C) Panel C. D) Panel D.

65) In the above figure for a monopolistically competitive firm, the profit maximizing output and

price are respectively

A) 80 units and $11. B) 50 units and $8.

C) 60 units and $9. D) 60 units and $14.

66) In the above figure for a monopolistically competitive firm, the total revenue at the

profit maximizing point is

A) $540 B) $840 C) $400 D) $880

67) In the above figure for a monopolistically competitive firm, the total cost at the

profit maximizing point is

A) $480 B) $400 C) $540 D) $880

68) In the above figure for a monopolistically competitive firm, the total economic profit at the

profit maximizing point is

A) $0 B) $240 C) $360 D) $300

69) In the above figure, what would happen to the monopolistically competitive industry in the

long run?

A) More producers would enter the market, and the share of the market to this firm would

fall, which would cause the demand curve to shift leftward until there is zero economic

profit.

B) More producers would exit the market, and the share of the market to this firm would fall,

which would cause the demand curve to shift leftward until there is zero economic profit.

C) More producers would enter the market, and the share of the market to this firm would

rise, which would cause the demand curve to shift rightward until there is zero economic

profit.

D) More producers would enter the market, and the share of the market to this firm would

fall, which would cause the demand curve to shift leftward until there is negative

economic profit.

70) For the monopolistic competitor, which of the following is INCORRECT?

A) Because the firm is not a perfect competitor, its demand curve slopes downward.

B) The marginal revenue curve is downward sloping and lies below the demand curve.

C) The profit maximizing rate of output arises at the point at which the marginal cost curve

intersects the marginal revenue curve.

D) If the firm in a monopolistically competitive industry were making economic losses, new

firms will enter the industry.

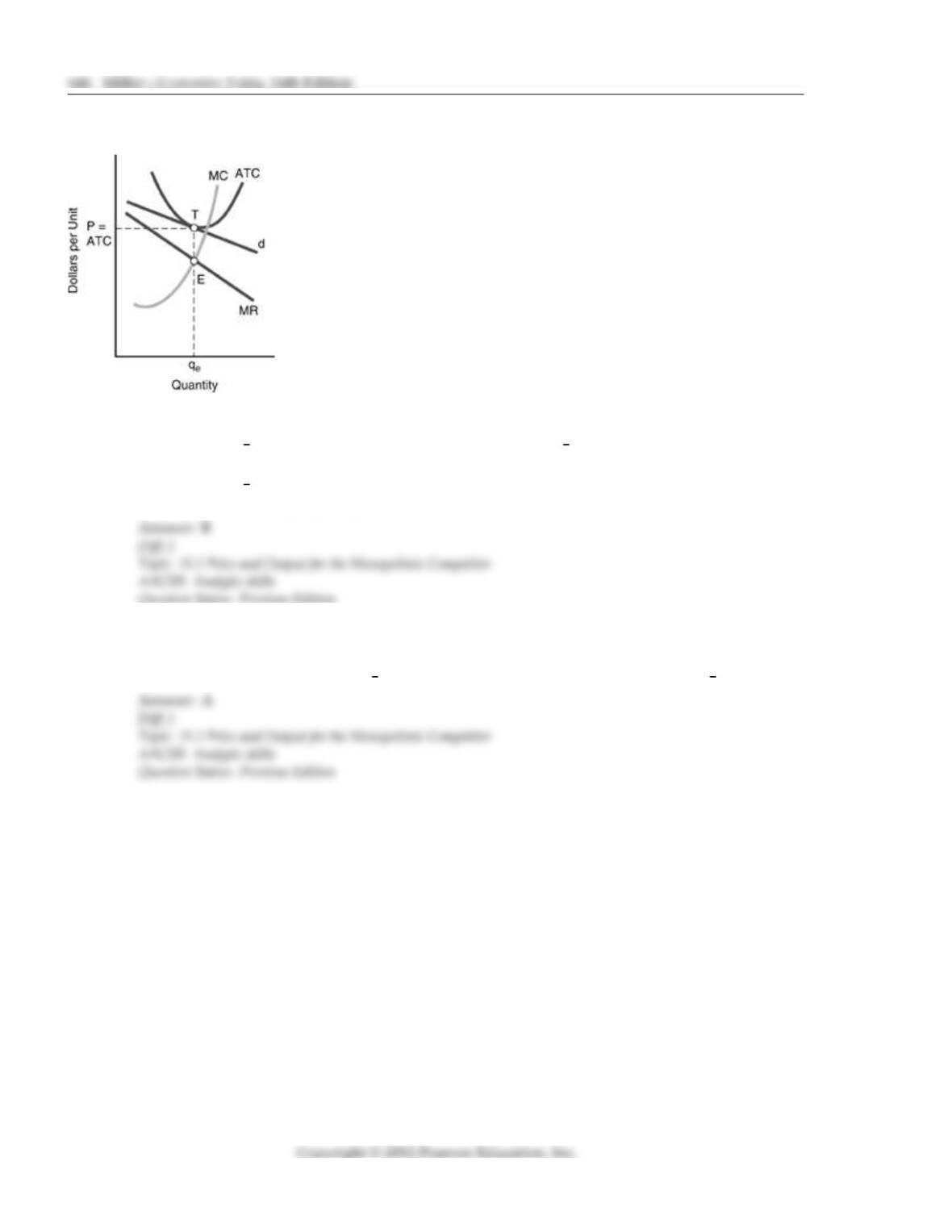

71) Use the above figure. For this monopolistic competitor, which of the following is INCORRECT?

A) The profit maximizing rate of output is qe, and the profit maximizing price is P.

B) The demand curve shows a direct relationship between price and quantity demanded.

C) The profit maximizing rate of output is at E, where MR intersects MC.

D) A downward sloping marginal revenue curve that is below the demand curve.

72) Use the above figure. The economic profit for this firm is

A) zero. B) the distance between T and E.

C) the distance between E and xaxis. D) the distance between T and x axis.

Chapter 25 Monopolistic Competition 647

Price per Marginal

Output Book ($) Cost

0 8.00 0

1 7.00 1.00

2 6.00 2.00

3 5.00 3.00

4 4.00 4.00

73) The above table depicts prices, quantities, and marginal costs faced by the campus bookstore. At

the profit maximizing level of output, what is the total revenue earned by the store?

A) $12 B) $5 C) $15 D) $6

74) The above table depicts prices, quantities, and marginal costs faced by the campus bookstore. At

the profit maximizing level of output, what is the total cost earned by the store?

A) $4 B) $9 C) $3 D) $16

75) The above table depicts prices, quantities, and marginal costs faced by the campus bookstore.

Based on marginal analysis, what is the profit maximizing level of output for the bookstore?

A) 1 book B) 2 books C) 3 books D) 4 books

76) The above table depicts prices, quantities, and marginal costs faced by the campus bookstore. At

the profit maximizing level of output, what is the profit earned by the store?

A) $15 B) $6 C) $8 D) $0

77) For a monopolistically competitive firm,

A) price equals marginal revenue at all levels of output.

B) price is less than marginal revenue at all levels of output.

C) price is greater than marginal revenue at all levels of output except for the first unit.

D) the demand curve is perfectly inelastic and marginal revenue is zero.

78) A firm in a monopolistically competitive market determines the profit maximizing output at

which

A) MR P. B) MR ATC. C) MR AVC. D) MR MC.

79) Which of the following is true of the price charged by a monopolistically competitive firm at the

profit maximizing level of output?

A) P MC B) P MC C) P MR D) P AVC

80) In the long run, a monopolistically competitive firm

A) earns positive economic profits.

B) earns zero economic profits.

C) earns negative economic profits.

D) can have positive, zero, or negative profits.

81) Which of the following short run outcomes for monopolistic competition is not possible?

A) P MR MC. B) P MC ATC.

C) P ATC. D) P ATC.